C-Type LNG Carrier Market Growth, Share, and Forecast (2026-2034)

Coverage: By Product Type (Cylindrical, Bi-Lobe, and Tri-Lobe), Application (Marine, Oil and Gas, Petrochemical, and Others), and Geography

- Status : Data Released

- Report Code : TIPRE00029686

- Category : Automotive and Transportation

- No. of Pages : 150

- Available Report Formats :

- Last update date : December 22, 2025

2025 Market Size

US$ 5.21 Mn

Base year value

2034 Forecast

US$ 9.94 Mn

Projected by 2034

CAGR 2026-2034

7.42 %

Growth rate

Addressable Market

US$ 68.22 Mn

(2026-2034)

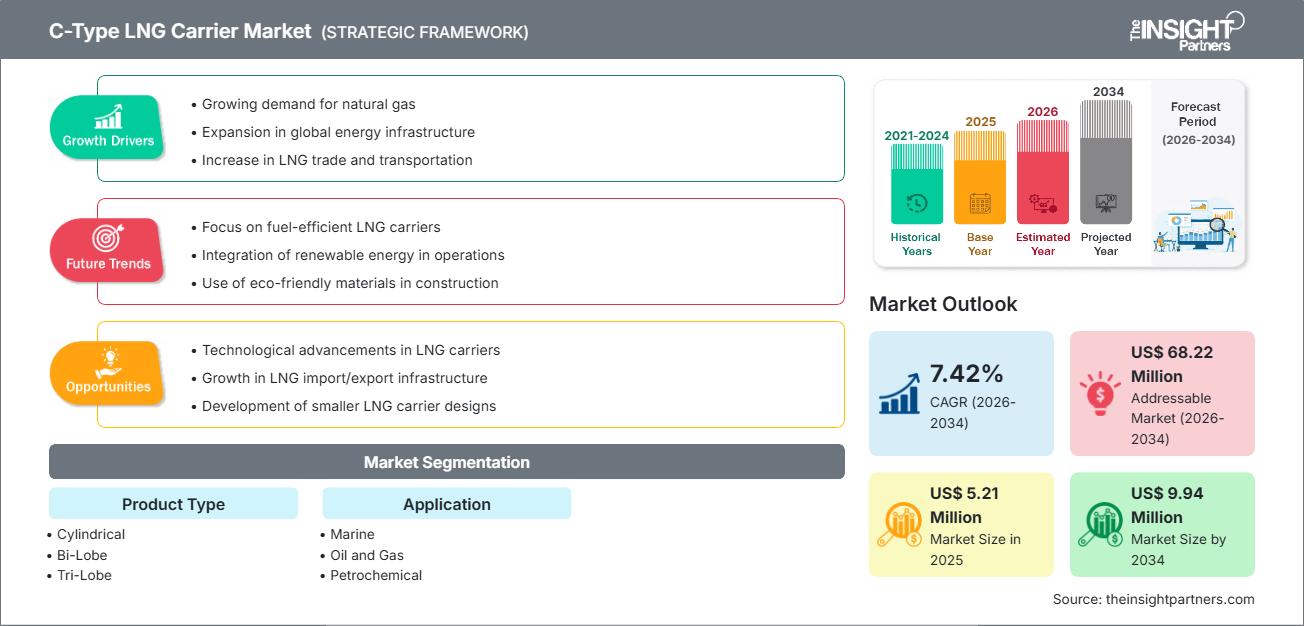

The C-type LNG carrier market size is expected to reach US$ 9.94 million by 2034 from US$ 5.21 million in 2025. The market is anticipated to register a CAGR of 7.42% during 2026–2034.

C-Type LNG Carrier Market Analysis

The C-Type LNG Carrier market is expanding due to the increasing global demand for natural gas as a cleaner transition fuel and the expansion of LNG infrastructure worldwide. C-type carriers, which utilize insulated, fully or partially pressurized cylindrical, bi-lobe, or tri-lobe tanks, are primarily used for small to mid-sized LNG carriers and other liquefied gases. They play a crucial role in facilitating international LNG trade, especially for regional distribution, bunkering, and supplying remote areas. Market growth is being fueled by new liquefaction projects, a surge in new shipbuilding contracts for LNG-fueled vessels, and the need for more versatile carriers to support the growing small-scale LNG market segment.

C-Type LNG Carrier Market Overview

A C-Type LNG Carrier is a specialized vessel designed to transport Liquefied Natural Gas (LNG) at cryogenic temperatures. The "C-type" refers to the containment system, which consists of independent cylindrical, bi-lobe, or tri-lobe shaped pressure-vessel tanks, typically installed inside the hull. This design offers enhanced structural integrity and cargo handling flexibility, making it a preferred choice for smaller to mid-scale LNG transport. The market is characterized by technological advancements focused on improving fuel efficiency and environmental sustainability, such as the adoption of dual-fuel engines.

Market Research Highlights

- Global market for C-Type LNG Carrier was valued at US$ 5.21 Million in 2025

- Annual market size is expected to reach US$ 9.94 Million by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 68.22 Million

- Market is anticipated to register a CAGR of 7.42% during the forecast period

- The United States represents a key market, supported by Growing demand for natural gas, Expansion in global energy infrastructure, Increase in LNG trade and transportation, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Technological advancements in LNG carriers, Growth in LNG import/export infrastructure, Development of smaller LNG carrier designs are expected to influence market dynamics and addressable market

- Report profiles industry participants, including China Shipbuilding Trading Co., Ltd, DSME Co., Ltd, GAS Entec, Gaslog Ltd, HYUNDAI SAMHO HEAVY INDUSTRIES CO., LTD., Knutsen OAS Shipping, Komarine Co, Mitsubishi Heavy Industries, Ltd., TGE Marine Gas Engineering GmbH, Torgy LNG AS, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

C-Type LNG Carrier Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

C-Type LNG Carrier Market Drivers and Opportunities

Market Drivers:

- Growing LNG Liquefaction Capacity Globally: The expansion of liquefaction plants and export capacity worldwide, particularly in regions like North America and Russia, creates a continuous need for carriers to transport the increased supply of LNG to consuming regions.

- Rising Demand for Natural Gas from Several Industries: Natural gas is increasingly adopted as a cleaner-burning fossil fuel alternative for power generation, industrial applications, and as a marine fuel (LNG bunkering), which directly drives demand for the necessary transport vessels.

- Surge in New Shipbuilding Contracts and New Fleet Expansion: The need for fleet modernization to comply with environmental regulations (like the IMO 2023 GHG Reduction Measures) and the expansion of LNG-fueled vessel fleets (including container ships and ferries) boost new orders for C-Type and other LNG carriers.

Market Opportunities:

- Growing Small-Scale LNG Market: C-Type carriers are ideal for the small-scale LNG market, which focuses on supplying remote areas, industrial customers, and providing LNG as a marine fuel (bunkering). The expansion of regional LNG distribution networks offers a significant niche opportunity.

- Technological Advancements in Carrier Design: Opportunities exist in developing and integrating new technologies, such as more fuel-efficient and environmentally friendly vessel designs and AI and digital systems for vessel optimization, predictive maintenance, and real-time data analysis to reduce operational costs and environmental impact.

- Expansion of LNG Infrastructure: Investments in new import terminals, regasification facilities, and LNG bunkering hubs globally create opportunities for C-Type carriers to service these new infrastructure points.

C-Type LNG Carrier Market Report Segmentation Analysis

The C-type LNG carrier market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Product Type:

- Cylindrical

- Bi-Lobe

- Tri-Lobe

By Application:

- Marine

- Oil and Gas

- Petrochemical

By Geography:

- North America

- Europe

- Asia-Pacific

- South & Central America

- Middle East & Africa

C-Type LNG Carrier Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 5.21 Million |

| Market Size by 2034 | US$ 9.94 Million |

| Global CAGR (2026 - 2034) | 7.42% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Product Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

C-Type LNG Carrier Market Players Density: Understanding Its Impact on Business Dynamics

The C-Type LNG Carrier Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

C-Type LNG Carrier Market Share Analysis by Geography

Asia-Pacific is anticipated to grow over the forecast period and account for the largest share of the market. This dominance is attributed to the region's massive and increasing demand for natural gas, high industrial growth, and the adoption of clean energy sources. China is a major market contributor, but its fleet is still highly dependent on foreign LNG carriers.

The C-type LNG carrier market shows a different growth trajectory in each region due to factors such as a surge in new shipbuilding contracts and new fleet expansion. Below is a summary of market share and trends by region:

-

North America

- Market Share: Holds a substantial market share, driven by its position as a major LNG exporter.

- Key Drivers:

- Significant expansion of LNG export capacity in the US and Canada.

- Presence of major LNG manufacturers and a robust shipping sector investment in LNG assets.

- Focus on LNG as a clean energy source.

- Trends: Investment in domestic LNG-transporting assets like LNG bunker barges.

-

Europe

- Market Share: An important market with rising liquefaction and regasification capacity.

- Key Drivers:

- Strong focus on energy security and diversifying gas supply.

- Stricter environmental regulations (e.g., IMO rules) are accelerating the adoption of LNG-fueled vessels.

- Demand for new services (e.g., small-scale distribution) at existing LNG import terminals.

- Trends: Investment in new LNG carriers, including icebreakers for Arctic routes, and a shift towards dual-fuel and environmentally compliant vessels.

-

Asia Pacific

- Market Share: Anticipated to be the fastest-growing regional market and holds a significant share, due to huge LNG import demand.

- Key Drivers:

- Rapid industrial growth and increasing energy demand.

- Government-backed adoption of cleaner energy sources like LNG.

- High LNG import volume, particularly in China and India.

- Trends: Dominance of the Marine segment in application. High focus on building regasification capacity.

-

South and Central America

- Market Share: Emerging market with growing adoption.

- Key Drivers:

- Increasing energy demand and development of gas fields.

- Investment in regional LNG infrastructure and import facilities.

- Trends: Development of automated translation tools for multilingual audiences, predictive AI for campaign optimization, and social listening platforms.

-

Middle East and Africa

- Market Share: Emerging market with strong growth potential.

- Key Drivers:

- Major national digital and energy strategies fostering innovation in gas transport.

- Key players like Qatar continue to dominate global LNG trade, driving demand for new carriers.

- Trends: AI-based audience sentiment tracking, influencer fraud detection, and multilingual content moderation through machine learning.

C-Type LNG Carrier Market Players Density: Understanding Its Impact on Business Dynamics

The C-Type LNG Carrier market is intensely competitive, with a few large global shipbuilding and shipping companies dominating newbuild orders and fleet operations. Differentiation is primarily achieved through technological innovation, compliance with stringent environmental regulations, and strategic fleet management.

The competitive landscape is driving vendors to differentiate through:

- Investing in advanced containment systems and fuel-efficient propulsion to reduce fuel consumption and emissions.

- Collaborations between shipbuilders, technology providers, and major energy companies to secure long-term contracts and financing for new vessels.

- Targeting the growing segment of the market that requires smaller, more versatile C-Type carriers for regional distribution and bunkering services.

Opportunities and Strategic Moves

- Fleet Modernization and Expansion: Companies are continuously ordering new vessels to replace older, less efficient units and to expand capacity to meet the growing global LNG trade volume.

- Integrated Value Chain: Major energy companies and large shipping firms are integrating their operations across the entire LNG value chain, from liquefaction to shipping and distribution.

- Adoption of Digital & Autonomous Technologies: Development and integration of smart shipping solutions (AI, IoT, remote monitoring) to enhance operational efficiency, safety, and predictive maintenance.

Major Companies Operating in the C-Type LNG Carrier Market Are:

- China Shipbuilding Trading Co., Ltd

- DSME Co., Ltd

- GAS Entec

- Gaslog Ltd

- HYUNDAI SAMHO HEAVY INDUSTRIES CO., LTD.

- Knutsen OAS Shipping

- Komarine Co

- Mitsubishi Heavy Industries, Ltd.

- TGE Marine Gas Engineering GmbH

Disclaimer: The companies listed above are not ranked in any particular order.

C-Type LNG Carrier Market News and Recent Developments

- For instance, in November 2024, HD KSOE announced that they signed shipbuilding contracts for a total of 25 vessels with overseas companies located in Europe, Oceania, Asia, and the Middle East. The contracts include two Very Large Ammonia Carriers (VLAC), 15 Medium-sized Product Carriers (PC), six Very Large Liquefied Petroleum Gas Carriers (VLGC), and two Liquefied Natural Gas (LNG) carriers. The total contract amount is KRW 2.82 trillion.

C-Type LNG Carrier Market Report Coverage and Deliverables

The "C-Type LNG Carrier Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- C-Type LNG Carrier Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- C-Type LNG Carrier Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- C-Type LNG Carrier Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the C-Type LNG Carrier Market. Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends