Vegan Dog Food Market Size, Trends & Demand by 2034

Coverage: By Product Type (Dry Food, Wet Food, Treats, and Others) and Distribution Channel (Supermarkets and Hypermarkets, Specialty Stores, Online Retail, and Others)

- Status : Upcoming

- Report Code : TIPRE00026059

- Category : Food and Beverages

- No. of Pages : 150

- Available Report Formats :

- Last update date : March 04, 2026

2025 Market Size

US$ 8.31 Bn

Base year value

2034 Forecast

US$ 15.03 Bn

Projected by 2034

CAGR 2026-2034

6.8 %

Growth rate

Addressable Market

US$ 105.43 Bn

(2026-2034)

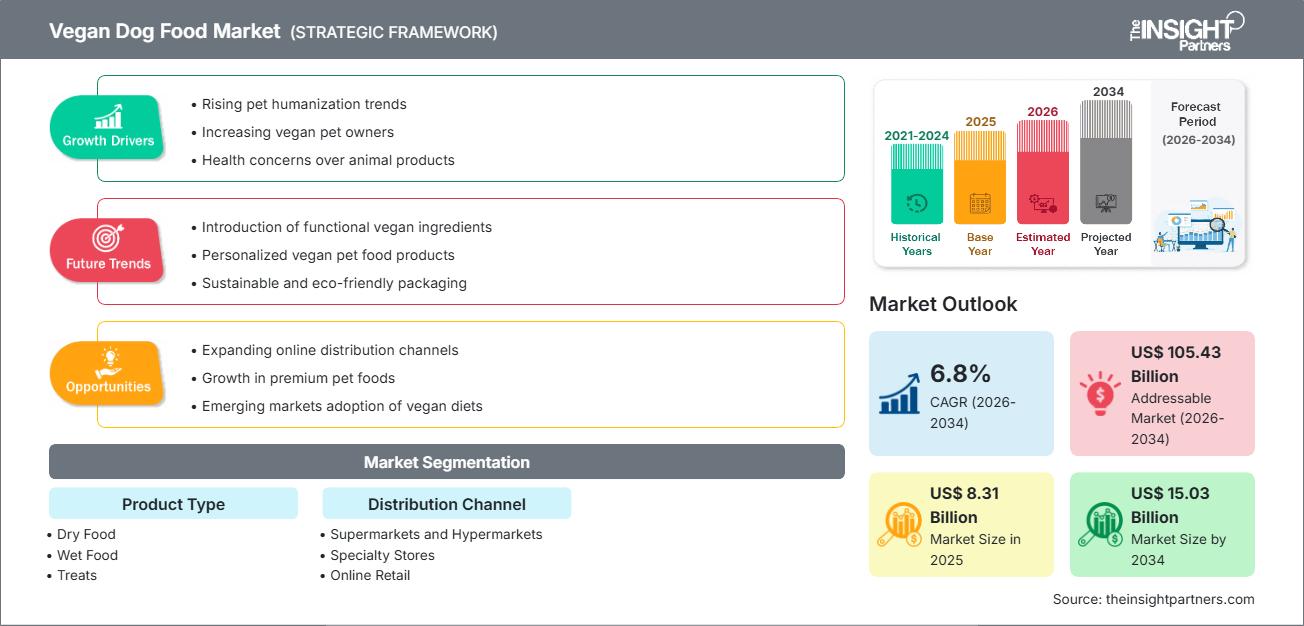

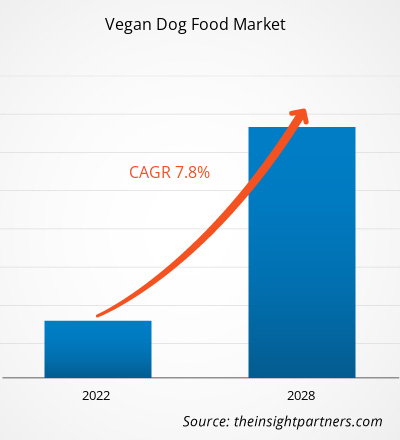

The global Vegan Dog Food market size is projected to reach US$ 15.03 billion by 2034 from US$ 8.31 billion in 2025. The market is anticipated to register a CAGR of 6.8% during the forecast period 2026–2034.

Key market dynamics include the rapid humanization of pets, where owners apply their own dietary ethics to their companions, and a rising clinical preference for plant-based proteins to manage canine food allergies and digestive sensitivities. Additionally, the market is expected to benefit from the growing environmental consciousness regarding the carbon footprint of meat-based pet food, innovations in laboratory-grown and fermented proteins, and the expansion of premium plant-based offerings in specialized veterinary retail channels.

Vegan Dog Food Market Analysis

The vegan dog food market analysis indicates a critical transition from a niche lifestyle choice to a scientifically backed nutritional category. As pet owners increasingly scrutinize ingredient labels, there is a heightened demand for complete and balanced plant-based formulations that meet AAFCO standards without the use of animal by-products. Strategic opportunities are emerging in the development of insect-based and fungi-derived protein sources, which offer high bioavailability and appeal to eco-conscious consumers. The analysis also highlights that success in this sector depends on overcoming palatability hurdles, requiring significant R&D investment in natural flavor enhancers and texturizers. Competitive differentiation now hinges on clinical validation, transparent sourcing of non-GMO crops, and the ability to provide life-stage-specific nutrition that proves plant-based diets can support long-term canine health.

Vegan Dog Food Market Overview

Vegan dog food is rapidly evolving into a mainstream segment of the global pet care industry. Once limited to a few specialty brands, vegan dog food now includes a wide array of kibble, canned pâtés, and functional treats designed to mimic the nutritional profile of traditional meat-based diets. This growth is largely fueled by the pet parent trend, where millennial and Gen Z consumers prioritize sustainability and animal welfare in every purchase. While North America and Europe remain the primary hubs for product innovation, the Asia-Pacific region is witnessing a surge in demand due to rising disposable incomes and a cultural shift toward vegetarianism in certain urban populations. Both established pet food conglomerates and agile startups are competing for market share by leveraging clean-label ingredients like ancient grains, legumes, and nutritional yeast. For instance, the market in the US represents a mature yet dynamic landscape for vegan dog food, driven by a high concentration of health-conscious pet owners. The market is characterized by a strong presence of premium independent brands and a growing acceptance of plant-based diets by veterinary professionals for managing skin and coat conditions.

Market Research Highlights

- Global market for Vegan Dog Food was valued at US$ 8.31 Billion in 2025

- Annual market size is expected to reach US$ 15.03 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 105.43 Billion

- Market is anticipated to register a CAGR of 6.8% during the forecast period

- The United States represents a key market, supported by Rising pet humanization trends, Increasing vegan pet owners, Health concerns over animal products, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Expanding online distribution channels, Growth in premium pet foods, Emerging markets adoption of vegan diets are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Antos B.V., Benevo, Bond Pet Foods, Inc., V-dog, Soopa Pets, Vegan4dogs, Wild Earth, YARRAH, Isoropimene Zootrofe Georgios Tsappis Ltd., Halo Pets, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Vegan Dog Food Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Vegan Dog Food Market Drivers and Opportunities

Market Drivers:

- Rising Prevalence of Food Allergies and Sensitivities: Many dogs suffer from sensitivities to common animal proteins like beef or chicken. Vegan dog food offers a hypoallergenic alternative that reduces inflammatory responses and skin irritations, driving adoption among pet owners seeking therapeutic relief for their animals.

- Sustainability and Environmental Impact: The high environmental cost of traditional livestock production has led consumers to seek low-carbon alternatives. Plant-based pet food requires significantly less land and water, appealing to the growing demographic of eco-warrior pet parents focused on reducing their household's ecological footprint.

- Humanization of Pets and Ethical Consumerism: The boundary between human and pet dietary habits is blurring. Owners who follow vegan or vegetarian lifestyles often seek to align their pet's diet with their personal ethical values regarding animal welfare, leading to a consistent increase in demand for cruelty-free pet products.

Market Opportunities:

- Innovation in Alternative Proteins: Beyond soy and peas, there is significant potential in utilizing micro-proteins, algae, and yeast-based fermentation. These ingredients offer meat-like amino acid profiles, providing an opportunity for brands to capture the flexitarian pet food market.

- Personalized and Subscription-Based Nutrition: The rise of D2C models allows companies to offer customized vegan meal plans based on a dog's specific breed, weight, and activity level, creating a high-margin, loyal customer base.

- Expansion into Therapeutic and Functional Treats: There is a vast untapped market for vegan functional treats that target specific health issues, such as joint mobility, dental health, and anxiety, allowing brands to diversify beyond standard daily meals.

Vegan Dog Food Market Report Segmentation Analysis

The Vegan Dog Food Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Product Type:

- Dry Food: This remains the leading segment due to its convenience, longer shelf life, and cost-effectiveness for pet owners. It is widely preferred for its dental health benefits and ease of storage.

- Wet Food: A growing segment favored for its high moisture content and superior palatability, often used as a topper or a complete meal for dogs with specific hydration needs or picky appetites.

- Treats: This fast-rising niche includes biscuits, dental chews, and jerky made from plant-based ingredients, serving as an entry point for owners testing vegan options.

- Others: Includes dehydrated, freeze-dried, and home-delivery meal kits that cater to the ultra-premium segment of the market.

By Distribution Channel:

- Supermarkets & Hypermarkets: These remain the primary volume drivers, offering a wide range of mainstream vegan brands to a broad consumer base during routine grocery shopping.

- Specialty Stores: This channel includes pet boutiques and veterinary clinics where owners seek expert advice and high-quality, scientifically formulated plant-based diets.

- Online Retail: The fastest-growing distribution channel, providing a platform for niche artisanal brands and subscription services that offer doorstep convenience and a wider product variety.

- Others: Includes direct-to-consumer (D2C) websites and health food stores that focus on holistic and organic pet care.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Vegan Dog Food Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 8.31 Billion |

| Market Size by 2034 | US$ 15.03 Billion |

| Global CAGR (2026 - 2034) | 6.8% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Product Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Vegan Dog Food Market Players Density: Understanding Its Impact on Business Dynamics

The Vegan Dog Food Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Vegan Dog Food Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for premium plant-based pet food producers and therapeutic nutrition manufacturers to expand.

The vegan dog food market is undergoing a significant transformation, moving from a niche dietary choice to a mainstream segment of the global pet care industry. Growth is driven by the rising prevalence of canine meat-protein allergies, a surge in ethical pet parenting demand, and the expansion of the sustainable pet food sector. Below is a summary of market share and trends by region:

North America

- Market Share: Holds a leading position globally, supported by a mature pet care infrastructure and high consumer spending on health-oriented pet products.

- Key Drivers:

- Rapid adoption of the clean label movement among millennial and Gen Z pet owners.

- Increasing veterinary recommendations for plant-based diets to manage chronic canine skin and digestive issues.

- Strong presence of domestic innovators and a well-established e-commerce ecosystem for niche brands.

- Trends: A significant shift toward grain-free and non-GMO vegan formulations, coupled with the integration of superfoods like ancient grains and algae-based omega-3s.

Europe

- Market Share: Holds a substantial share of the global market, anchored by a deep-seated cultural commitment to animal welfare and environmental sustainability.

- Key Drivers:

- High demand for sustainable pet food alternatives in response to the European Green Deal and climate consciousness.

- Strict regulatory frameworks that ensure high quality and nutritional transparency for plant-based pet products.

- Robust growth in vegan-friendly countries such as the UK, Germany, and France.

- Trends: A strategic focus on alternative protein diversification, including the rise of insect-based and fungi-derived hybrids, and a shift toward biodegradable and plastic-free packaging.

Asia-Pacific

- Market Share: The fastest-growing region, with high-potential markets like China, India, and Australia driving regional expansion.

- Key Drivers:

- Massive surge in pet ownership among the urban middle class and a rising cultural shift toward vegetarianism in specific markets.

- Increasing disposable incomes leading to a preference for premium, imported westernized pet nutrition.

- Rapid digitalization and high mobile commerce penetration facilitate easy access to specialty vegan brands.

- Trends: Heavy reliance on social media influencers for brand discovery and an increasing focus on beauty-from-within formulations that target coat health and anti-aging in pets.

South and Central America

- Market Share: An emerging market with a growing sector for specialized pet diets in countries like Brazil, Chile, and Argentina.

- Key Drivers:

- Rising awareness of the health benefits of plant-based nutrition for pets living in apartment settings.

- Transition from home-cooked scraps to formalized commercial pet food among middle-income segments.

- The growing humanization of pets, where owners view animals as integral family members requiring high-quality diets.

- Trends: Growth of farm-to-bowl boutique brands and the introduction of local, plant-derived ingredients like quinoa and sweet potato to differentiate from global bovine-based products.

Middle East and Africa

- Market Share: A developing market transitioning toward formalized commercial production and premiumization in high-income urban hubs.

- Key Drivers:

- High demand for hypoallergenic and shelf-stable products suitable for arid climates and sensitive breeds.

- Strategic investments in regional pet specialty retail and the modernization of local supply chains.

- Growing interest in smart agriculture to produce high-nutrient plant proteins locally.

- Trends: Implementation of modern logistics and climate-controlled storage to maintain the integrity of premium vegan diets, coupled with a focus on high-protein powders for the pediatric pet segment.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Antos B.V., Benevo, Bond Pet Foods, Inc., V-dog, Soopa Pets, Vegan4dogs, Wild Earth, YARRAH, and Isoropimene Zootrofe Georgios Tsappis Ltd, also contributing to a diverse and rapidly expanding market landscape.

This competitive environment pushes vendors to differentiate through:

- Nutritional Validation and Functional Branding: Positioning vegan dog food as a high-performance, hypoallergenic solution by emphasizing complete amino acid profiles, added taurine, and gut-friendly probiotics for health-conscious pet parents.

- Alternative Protein Innovation: Product portfolios are expanding beyond soy and peas to include novel proteins such as fungi, yeast, and insect-derived ingredients, which offer higher sustainability and better palatability for picky eaters.

- Vertical Integration and Ethical Sourcing: Producers are increasingly managing their own supply chains—from sourcing non-GMO legumes to local manufacturing—to ensure clean label transparency and meet strict animal welfare and environmental standards.

- Advanced Processing Technologies: Utilizing precision fermentation and extrusion technologies to improve the texture and flavor of plant-based kibble and wet food, making them nearly indistinguishable from traditional meat-based counterparts.

Opportunities and Strategic Moves

- Collaborate with Veterinary and Clinical Channels: Partner with veterinary clinics and nutritionists to develop medical-grade vegan diets tailored for dogs with chronic protein allergies or weight management needs, tapping into the high-margin therapeutic segment.

- Leverage Subscription-Based D2C Models: Expand presence in online retail through personalized meal plans and subscription services, facilitating direct engagement with urban millennials and Gen Z consumers who prioritize convenience and ethical sourcing.

- Incorporate Sustainable and Regenerative Certifications: Target environmentally conscious demographics by achieving Carbon Neutral or B-Corp certifications and adopting recyclable or compostable packaging to align with global net-zero goals.

Major Companies operating in the Vegan Dog Food Market are:

- Antos B.V.

- Benevo

- Bond Pet Foods, Inc.

- V-dog

- Soopa Pets

- Vegan4dogs

- Wild Earth

- YARRAH

- Isoropimene Zootrofe Georgios Tsappis Ltd.

- Halo Pets

Disclaimer: The companies listed above are not ranked in any particular order.

Vegan Dog Food Market News and Recent Developments

- In August 2025, German vegan pet food brand VEGDOG announced its expansion in Austria and Switzerland. The company expects significant sales growth in the coming years and is strengthening its management team.

- In February 2025, Marsapet introduced the first dog food formulated with FeedKind pet protein—a cultured, fermentation‑derived ingredient produced without the use of arable land or any animal-based components.

Vegan Dog Food Market Report Coverage and Deliverables

The Vegan Dog Food Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Vegan Dog Food Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Vegan Dog Food Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Vegan Dog Food Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Vegan Dog Food Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends