Glass Wafer Market Growth, Size & Forecast by 2034

Glass Wafer Market Size and Forecast (2021 - 2034), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Application (CMOS image sensor, Integrated Circuit (IC) Packaging, LED, Microfluidics, FO-WLP, and MEMs and RF) and End-Use (Energy, IT and Telecommunication, Consumer Electronics, Aerospace and Defense, Automotive, and Healthcare and Biotechnology)

Historic Data: 2021-2024 | Base Year: 2025 | Forecast Period: 2026-2034- Report Date : Apr 2026

- Report Code : TIPRE00020116

- Category : Chemicals and Materials

- Status : Upcoming

- Available Report Formats :

- No. of Pages : 150

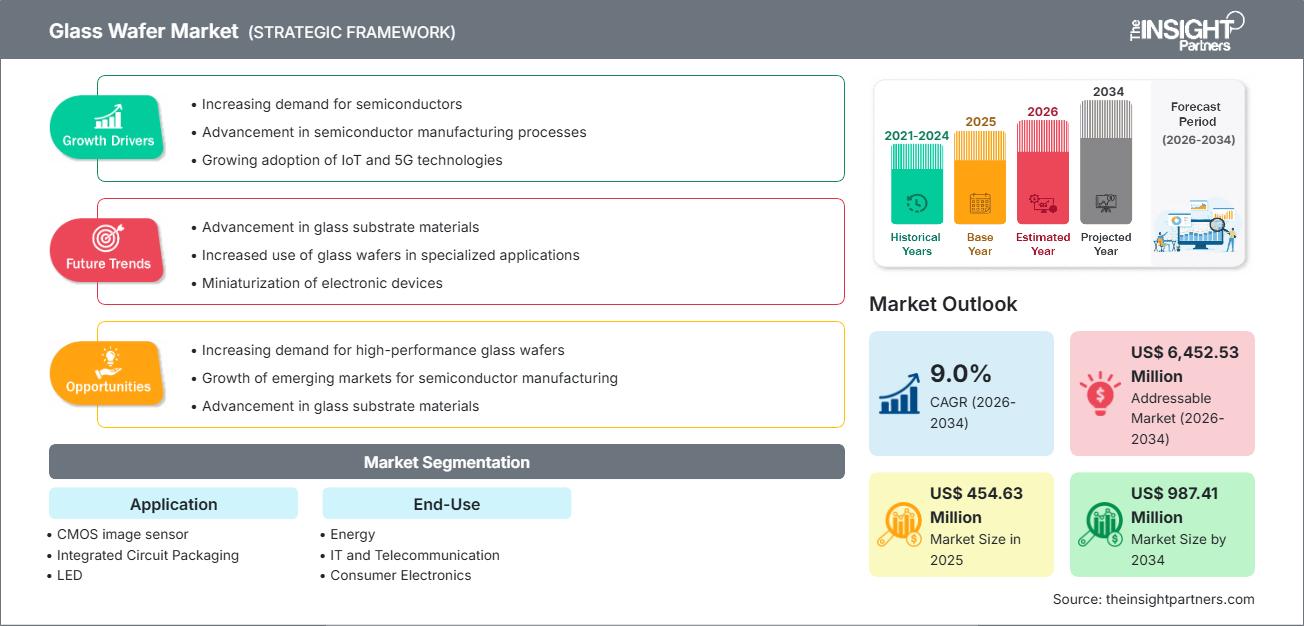

The global glass wafer market size is projected to reach US$ 987.41 million by 2034 from US$ 454.63 million in 2025. The market is anticipated to register a CAGR of 9.0% during the forecast period 2026–2034. Key market dynamics include a heightening global focus on miniaturized electronic components, rising demand for advanced packaging solutions like Fan-Out Wafer-Level Packaging (FO-WLP), and the increasing adoption of glass substrates in high-performance computing (HPC) and AI accelerators. Additionally, the market is expected to benefit from the expansion of 5G infrastructure, growing utilization of Micro-Electro-Mechanical Systems (MEMS) in the automotive sector, and the rising integration of microfluidics in medical diagnostic devices.

Glass Wafer Market Analysis

The glass wafer market analysis shows a significant shift toward high-precision substrates as the semiconductor industry moves beyond the physical limits of organic materials. Procurement trends indicate the market is splitting into traditional borosilicate-led consumer sensor sectors and high-growth TGV-exclusive export markets in the AI and data center segments. Strategic opportunities are emerging in specialty pediatric and geriatric medical microfluidics, where glass's chemical inertness and superior clarity compared to polymer alternatives offer a clear competitive advantage. The analysis also notes that market expansion depends on clean-room integrity for wafer thinning and laser-drilling efficiency for through-vias. Competitive differentiation now stands out depending on branding that highlights ultra-low surface roughness, defect-free polishing, and the ability to track material purity from the melt to the final wafer. This approach helps premium suppliers charge higher prices in a market with diverse global competitors.

Glass Wafer Market Overview

Glass wafer is shifting from a secondary handling tool to a global premium substrate. While historically focused on display technologies and simple optical carriers, glass wafer is expanding into value-added products like RF-MEMS, bio-MEMS, and specialized interposers. Both established glass manufacturers and large semiconductor foundries are part of this market, making use of the natural thermal stability and low dielectric loss found in high-purity glass. More health-conscious and tech-driven consumers in North America and Asia-Pacific are looking for advanced diagnostic and communication tools, which has helped glass wafers gain popularity as a "high-performance" choice for the AI era. Asia-Pacific is still the main producer, but North America has become a leader in innovation and advanced packaging design, especially through strategic R&D contracts for AI chipsets.

North America stands as a leading hub for glass wafer innovation, propelled by a sophisticated semiconductor ecosystem and robust R&D investment. In the United States, the market is increasingly shaped by the push for domestic chip manufacturing through the CHIPS Act. Key growth is visible in high-performance computing, where glass substrates replace traditional materials for AI accelerators and 5G components.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONGlass Wafer Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Glass Wafer Market Drivers and Opportunities

Market Drivers:

- Superior Thermal and Electrical Insulation: Glass wafers offer smaller thermal expansion and higher resistivity, which makes them easier to manage in high-density chip configurations. This physical benefit, along with growing interest in AI-driven heat management, is driving its popularity.

- Expansion of the Global CMOS Image Sensor Category: The surge in autonomous vehicles and high-end mobile photography has sustained high demand for glass-wafer inputs. As industries trade up to high-resolution sensory experiences, glass substrates continue to see stable volume gains.

- Rapid Expansion of 5G and IoT Connectivity: The rollout of next-gen networks has removed traditional frequency barriers for communication devices. This is particularly evident in the rapid adoption of glass-based RF filters and MEMS resonators in the Asia-Pacific and North America.

Market Opportunities:

- Expansion into Point-of-Care Microfluidics: Beyond traditional electronics, glass wafer technology offers significant opportunities in high-precision medical "Lab-on-a-Chip" devices for rapid testing and DNA sequencing.

- Growth in Autonomous Automotive Corridors: Forming strategic partnerships between substrate suppliers and Tier-1 automotive distributors may facilitate access to high-margin market segments where demand for LiDAR and advanced sensor substrates is increasing.

- Diversification into Specialty Certifications: There is a growing opportunity for producers to target specific demographics through certifications such as ISO-13485 (Medical) and AS9100 (Aerospace), as seen in recent successful facility expansions in the European market.

Glass Wafer Market Report Segmentation Analysis

The Glass Wafer Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Application:

- CMOS image sensor

- Integrated Circuit Packaging

- LED

- Microfluidics

- FO-WLP

- MEMs and RF

By End-Use:

- Energy

- IT and Telecommunication

- Consumer Electronics

- Aerospace and Defense

- Automotive

- Healthcare and Biotechnology

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Glass Wafer Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 454.63 Million |

| Market Size by 2034 | US$ 987.41 Million |

| Global CAGR (2026 - 2034) | 9.0% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Application

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Glass Wafer Market Players Density: Understanding Its Impact on Business Dynamics

The Glass Wafer Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Glass Wafer Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for premium substrate producers and automotive sensor manufacturers to expand.

The glass wafer market is undergoing a significant transformation, moving from a niche handling material to a global high-value functional substrate. Growth is driven by the rising complexity of AI chips, a surge in "next-gen" communication demand, and the expansion of the luxury automotive sensor sector. Below is a summary of market share and trends by region:

North America

- Market Share: Holds a significant share driven by high-performance computing (HPC) and the growth of domestic AI hardware startups.

- Key Drivers:

- Rising consumer preference for high-speed, glass-based 2.5D/3D IC packaging.

- Mainstreaming of "advanced packaging" in high-end tech clusters like Silicon Valley.

- Increased R&D in aerospace sensors alongside local "Next-Gen" semiconductor initiatives.

- Trends: Scaling of data center infrastructure and the successful adoption of TGV technologies to appeal to power-conscious tech giants.

Europe

- Market Share: Holds a strong global share, anchored by deep-seated automotive and industrial engineering ecosystems in Germany, France, and the UK.

- Key Drivers:

- High domestic consumption of iconic automotive brands requiring LiDAR and ADAS sensors.

- Established processing infrastructure and strict regulatory frameworks for high-precision glass.

- Robust government support for industrial automation and "Industry 4.0" development.

- Trends: A strategic shift toward prioritizing manufacturing capacity for high-margin, medical-grade microfluidics over simple carriers.

Asia-Pacific

- Market Share: The largest and fastest-growing region, with China, Taiwan, and South Korea acting as the primary engines for semiconductor and consumer electronics.

- Key Drivers:

- Massive consumer base in China and Southeast Asia seeking premium, high-speed smartphones and 5G devices.

- Government-supported agricultural and industrial initiatives focused on high-value "smart" manufacturing.

- Rapid urbanization leading to a preference for westernized "luxury" automotive electronics.

- Trends: Heavy reliance on B2B contracts for high-end glass wafers used in the smartphone and semiconductor industries.

South and Central America

- Market Share: Emerging market with a growing electronics assembly sector in countries like Brazil and Chile.

- Key Drivers:

- Increasing awareness of the performance superiority of glass substrates for local telecommunications upgrades.

- Modernization of assembly plants into commercial-grade fabrication units to supply regional hubs.

- Rising interest in 5G-ready devices among middle-to-high income segments.

- Trends: Growth of "regional supply" boutique brands and the introduction of glass-based medical chips to differentiate from the dominant plastic-based market.

Middle East and Africa

- Market Share: Developing market with deep cultural roots in trade, transitioning toward formalized technology production.

- Key Drivers:

- Strategic investments in "Smart Cities" requiring advanced sensor and communication hardware.

- High demand for shelf-stable, durable electronic components in arid climates.

- Regional initiatives to improve local tech security and reduce import reliance.

- Trends: Implementation of modern clean-room and laser-drilling technologies to formalize the local substrate market, coupled with a focus on high-durability glass for the defense segment.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Corning Incorporated, AGC Inc., and SCHOTT AG. Regional experts and niche players like Plan Optik AG (Germany) and TECNISCO, LTD. (Japan), alongside North American innovators such as 3DGS and Samtec, also contribute to a diverse and rapidly expanding market landscape.

This competitive environment pushes vendors to differentiate through:

- Positioning glass wafers as a superior structural alternative to silicon and organic substrates by emphasizing their higher thermal stability, transparency, and low dielectric loss for tech-conscious clients.

- Glass wafer products now include more than just standard rounds. Companies offer ultra-thin wafers for FO-WLP, laser-drilled TGV substrates, and pre-metallized interposers.

- Producers manage the entire supply chain, from raw glass melting (e.g., Borosilicate and Fused Silica) to local precision polishing. This approach ensures quality, transparency, and meets high-purity standards.

- New technologies like laser-assisted etching and high-speed TGV drilling help create high-quality glass interposers used in AI and data center products worldwide.

Opportunities and Strategic Moves

- Partner with high-end semiconductor foundries and e-commerce B2B platforms to tap into the surging demand for AI-ready and high-frequency substrates in the Asia-Pacific and North American markets.

- Incorporate sustainable manufacturing practices and green-glass certifications to appeal to environmentally conscious tech investors and corporations seeking ethical material alternatives.

Major Companies operating in the Glass Wafer Market are:

- SCHOTT

- AGC Inc.

- Corning Incorporated

- Plan Optik AG

- Bullen

- Nippon Electric Glass Co., Ltd.

- SAMTEC, Inc.

- Shin-Etsu Chemical Co., Ltd

- Coresix Precision Glass, Inc.

Disclaimer: The companies listed above are not ranked in any particular order.

Glass Wafer Market News and Recent Developments

- In September 2025, GlobalFoundries announced a collaboration effort with Corning Incorporated to develop detachable fiber connector solutions for GF’s silicon photonics platform. Corning’s GlassBridge™ solution, a glass-waveguide-based edge-coupler compatible with the platform’s v-grooves, is designed to meet the growing demands of AI datacenters for high bandwidth and power-efficient optical connectivity. Other coupling mechanisms are also being developed, including a vertically-coupled detachable fiber-to-PIC (Photonic Integrated Circuit) solution—demonstrating GlobalFoundries and Corning’s combined ability to produce multiple forms of co-packaged PIC-to-fiber connectivity.

- In September 2025, SCHOTT announced to showcase its high-performance specialty glass portfolio for advanced packaging at SEMICON Taiwan 2025. SCHOTT AG presented its latest innovations tailored for the semiconductor industry. With a focus on precision and performance, SCHOTT unveiled a diverse portfolio of high-performance solutions, including glass carrier wafers and panels engineered to meet the rigorous demands of advanced chip packaging.

Glass Wafer Market Report Coverage and Deliverables

The "Glass Wafer Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Glass Wafer Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope.

- Glass Wafer Market trends, as well as market dynamics such as drivers, restraints, and key opportunities.

- Detailed PEST and SWOT analysis.

- Glass Wafer Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments.

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Glass Wafer Market.

- Detailed company profiles.

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Get Free Sample For

Get Free Sample For