Hydrogen Storage Alloys Market Size, Trends & Growth by 2034

Hydrogen Storage Alloys Market Size and Forecast (2021 - 2034), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (AB5, AB2); Application (Rechargeable Batteries, Cooling Devices, Fuel Cells, Others)

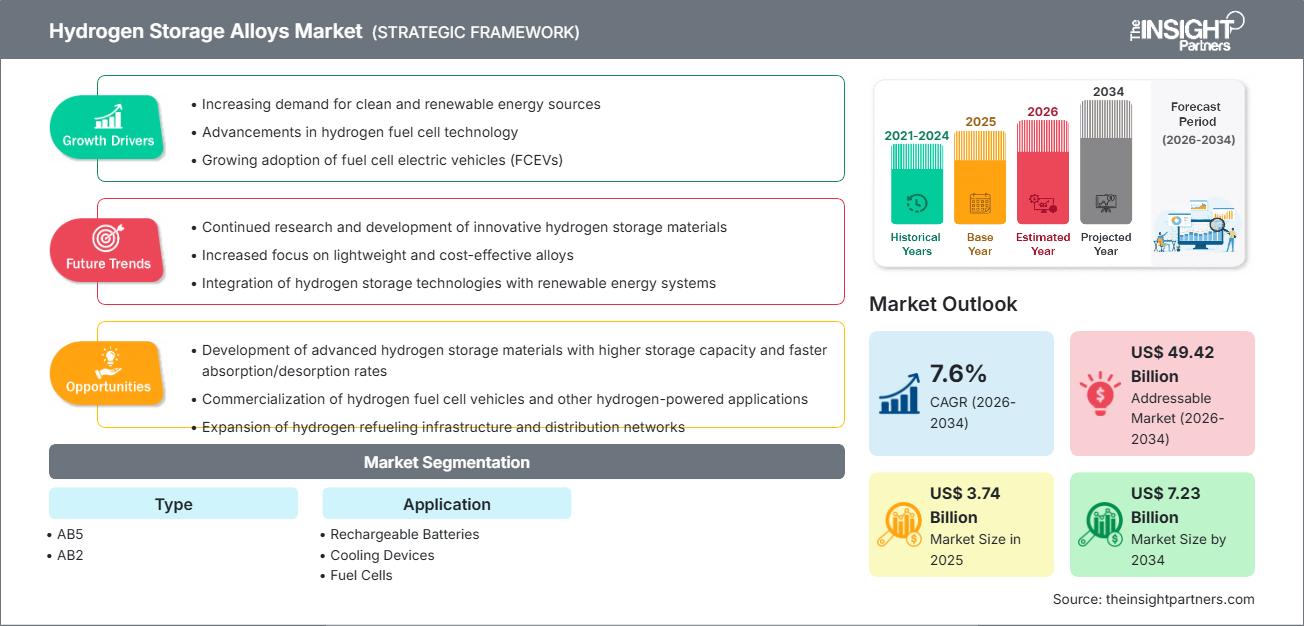

Historic Data: 2021-2024 | Base Year: 2025 | Forecast Period: 2026-2034- Report Date : Apr 2026

- Report Code : TIPRE00020902

- Category : Chemicals and Materials

- Status : Upcoming

- Available Report Formats :

- No. of Pages : 150

The global hydrogen storage alloys market size is expected to reach US$ 7.23 billion by 2034 from US$ 3.74 billion in 2025. The market is anticipated to register a CAGR of 7.6% during the forecast period 2026–2034. Key market dynamics include the rapid scaling of the global hydrogen economy, a strategic shift toward solid-state storage for enhanced safety in urban environments, and the continued reliance on nickel-metal hydride (Ni-MH) technology in hybrid electric vehicles. Additionally, the market is set to benefit from the emergence of metal-hydride-based thermal management systems, expanding industrial decarbonization mandates, and significant breakthroughs in AB2-type alloy capacities, which offer superior volumetric energy density for stationary power applications.

Hydrogen Storage Alloys Market Analysis

The hydrogen storage alloys market analysis reveals a critical transition from lab-scale intermetallic research to industrial-grade storage solutions. A focused examination of procurement trends indicates a widening gap between high-cycling AB5 powders, essential for the Ni-MH battery sector, and the emerging demand for "tank-grade" AB2 and Ti-Fe alloys intended for long-duration energy storage. Strategic opportunities are surfacing in the integration of these alloys within microgrids and telecom backup systems, where the safety profile of low-pressure metal hydrides, operating at near-ambient conditions, outperforms compressed or cryogenic alternatives. The analysis further identifies that competitive success is increasingly tied to the ability to tune plateau pressures and absorption kinetics through precise elemental substitution. Companies that can provide customized alloy formulations alongside integrated thermal management skids are positioned to capture high-value contracts in the defense, aerospace, and stationary power sectors.

Hydrogen Storage Alloys Market Overview

Hydrogen storage alloys are evolving from a specialized chemical niche into a foundational pillar of the global green energy transition. While historically dominated by the production of battery-grade materials for portable electronics and hybrid vehicles, the hydrogen storage alloys market is now pivoting toward large-scale solid-state hydrogen storage modules. The landscape features a mix of rare-earth integrated producers in Asia and specialty metallurgical firms in Europe and North America, all leveraging advanced vacuum induction melting and strip-casting technologies. As global safety regulations for hydrogen transport tighten, the "safe and compact" value proposition of metal hydrides is gaining traction in residential and indoor applications. For instance, the market in North America has seen a surge in prototype solid-state storage deployments for industrial material-handling fleets, where volumetric density and fire safety are paramount for indoor operations.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONHydrogen Storage Alloys Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Hydrogen Storage Alloys Market Drivers and Opportunities

Market Drivers:

- Enhanced Safety and Volumetric Density: Unlike high-pressure tanks, hydrogen storage alloys operate at low pressures (sub-1 MPa), significantly reducing the risk of catastrophic failure. This safety profile, combined with higher volumetric density than compressed gas, is a primary driver for adoption in built environments.

- Resilience of Ni-MH in Hybrid Mobility: Despite the rise of Lithium-ion, the Ni-MH battery market remains a stable demand base for AB5/A2B7 powders due to their safety, wide operating temperature range, and longevity in hybrid electric vehicles (HEVs) and industrial tools.

- Global Decarbonization and Hydrogen Roadmaps: National mandates for hydrogen-based power and industrial heating are catalyzing demand for efficient storage and compression materials, particularly as countries move toward decentralized energy architectures.

Market Opportunities:

- Scale-up of Tank-Grade AB2 and Ti-Fe Families: Developing cost-effective, high-capacity alloys like Ti-Fe-Mn offers significant potential for seasonal energy storage and large-scale stationary tanks, reducing reliance on expensive rare-earth elements.

- Innovation in Sorption Heat Pumps: Beyond storage, hydrogen storage alloys present a unique opportunity in thermal management, where metal-hydride heat pumps can leverage sorption cycles for high-efficiency cooling and heating in industrial processes.

- Strategic IP Development and Licensing: Active patenting around microstructure control and low-temperature desorption kinetics opens lucrative avenues for licensing agreements with hydrogen infrastructure EPCs and tank OEMs.

Hydrogen Storage Alloys Market Report Segmentation Analysis

The Hydrogen Storage Alloys Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Type:

- AB5: The industry workhorse for Ni-MH batteries and purification systems. Known for rapid activation and excellent cycle life, it remains the dominant segment by volume.

- AB2: A high-growth segment targeting stationary storage tanks and compressors. These alloys offer higher gravimetric capacity potential but require more sophisticated activation protocols.

By Application:

- Rechargeable Batteries: The largest current application, utilizing alloy powders in electrodes for HEVs, consumer electronics, and backup power.

- Cooling Devices: A specialized segment utilizing metal-hydride heat pumps and thermal sorption cycles for sustainable heating and cooling.

- Fuel Cells: The fastest-growing segment, focusing on solid-state hydrogen modules for stationary backup and mobile fuel-cell platforms.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Hydrogen Storage Alloys Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 3.74 Billion |

| Market Size by 2034 | US$ 7.23 Billion |

| Global CAGR (2026 - 2034) | 7.6% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Hydrogen Storage Alloys Market Players Density: Understanding Its Impact on Business Dynamics

The Hydrogen Storage Alloys Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Hydrogen Storage Alloys Market Share Analysis by Geography

Asia Pacific is expected to grow fastest in the coming years, driven by the manufacturing dominance of Japan and China in the battery and hydrogen infrastructure sectors. Emerging markets in Europe and North America also offer significant opportunities as they formalize their national hydrogen strategies.

The hydrogen storage alloys (HSA) market, primarily utilizing metal hydrides, is evolving as a critical alternative to high-pressure gas and cryogenic storage. This technology is increasingly favored for its high volumetric energy density and safety profiles in stationary and mobile applications. Below is a summary of market share and trends by region:

1. North America

- Market Share: A robust segment driven by R&D leadership and early adoption in stationary energy storage pilots.

- Key Drivers:

- Strong presence of specialty alloy distributors and material science innovators

- Significant DOE-funded research (e.g., Hydrogen Earthshot) into solid-state hydrogen storage

- High demand for safe, non-explosive backup power in telecom hubs and data centers

- Trends: Increasing adoption of modular metal-hydride storage for material-handling equipment (forklifts) and a strategic focus on domesticating the supply chain for critical materials like Magnesium and Titanium.

2. Europe

- Market Share: Holds a significant share, anchored by strong industrial decarbonization policies and a sophisticated specialty chemicals sector.

- Key Drivers:

- Mandatory national hydrogen roadmaps and the European Green Deal

- Strict safety regulations for indoor hydrogen use, favoring low-pressure alloy storage

- High demand for thermal management innovations in integrated energy systems

- Trends: Strategic research into Ti-Fe (Titanium-Iron) and Ti-Mn (Titanium-Manganese) systems to reduce reliance on imported rare-earth materials, alongside the integration of HSAs into large-scale "hydrogen valley" projects.

3. Asia Pacific

- Market Share: The largest and fastest-growing region globally, with Japan, China, and South Korea leading in production capacity and patent filings.

- Key Drivers:

- Integrated supply chains for rare earths, which are essential for AB5-type alloys

- Massive hybrid vehicle (NiMH battery) and fuel-cell vehicle (FCV) production

- Aggressive government subsidies for hydrogen-based "Smart Cities" and refueling infrastructure

- Trends: Consolidation of hydrogen alloy assets into dedicated energy subsidiaries and the commercialization of large-scale solid hydrogen storage modules for campus-wide power and grid stabilization.

4. South and Central America

- Market Share: An emerging market focusing on green hydrogen pilots and industrial integration, particularly in Chile and Brazil.

- Key Drivers:

- Abundance of low-cost renewable energy (solar and wind) for green hydrogen production

- The need for safe, low-maintenance storage solutions in remote, off-grid mining operations

- Growing international partnerships for hydrogen export infrastructure

- Trends: Increasing interest in packaged metal-hydride storage solutions to "smooth" renewable energy output and provide stable power for heavy-duty industrial machinery.

5. Middle East and Africa

- Market Share: A developing market with a focus on large-scale hydrogen exports and infrastructure modernization.

- Key Drivers:

- National transformation plans (e.g., Saudi Vision 2030) aiming for global hydrogen leadership

- Significant investment in "Smart Agriculture" and desalination plants powered by hydrogen

- Strategic location as a hydrogen hub for the European and Asian markets

- Trends: Adoption of high-density alloy storage for hydrogen compression and the implementation of HSA-based microgrids in arid climates where traditional battery cooling is energy-intensive.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as JMC (Japan Metals & Chemicals Co., Ltd.), Santoku Corporation, and AMG Titanium. Global distributors and integrated rare-earth specialists also play a pivotal role in the market's business dynamics, particularly in the Asia-Pacific region, which remains the dominant hub for alloy production and research.

This competitive environment pushes vendors to differentiate through:

- Custom Alloy Tuning: Providing specific equilibrium pressures and kinetics tailored to the user’s thermal management environment, optimizing thermodynamics for Mg-based and Ti-based storage systems.

- System Integration: Moving beyond raw powders to provide complete "plug-and-play" storage tanks with integrated heat exchangers, essential for stationary energy storage and backup power systems.

- Purity and Morphology Control: Utilizing advanced vacuum melting and strip-casting to ensure consistent performance across thousands of absorption-desorption cycles, minimizing degradation and hydrogen embrittlement.

- Thermodynamic Reversibility: Engineering alloys with tailored reaction enthalpies to allow for efficient hydrogen release at lower temperatures, broadening the application of solid-state storage in mobile fuel cells.

Opportunities and Strategic Moves

- Partner with renewable energy developers to integrate metal hydride storage systems into grid-balancing projects, utilizing excess solar and wind energy for long-duration stationary storage.

- Incorporate AI-driven material informatics and computational modeling to accelerate the discovery of high-entropy alloys that offer superior gravimetric density and faster refueling kinetics.

Major Companies operating in the Hydrogen Storage Alloys Market are:

- JMC (Japan Metals & Chemicals Co., Ltd.) – Japan

- Merck KGaA (Sigma-Aldrich) – Germany

- Ajax Tocco Magnethermic Corporation – United States

- Baotou Santoku Battery Materials Co. Ltd. – China

- Santoku Corporation – Japan

- American Elements – United States

- AMG Titanium Alloys & Coatings LLC – Germany

- Jiangmen Kanhoo Industry Co. Ltd – China

- Xiamen Tungsten Co. Ltd – China

Disclaimer: The companies listed above are not ranked in any particular order.

Hydrogen Storage Alloys Market News and Recent Developments

- In September 2025, HOUPU International successfully launched its solid-state hydrogen storage products made from AB2 hydrogen storage alloys in the Brazilian market. The portable, safe, and high-efficiency hydrogen storage cylinders support applications across electric vehicles, forklifts, and mobile power sources, driving adoption of hydrogen energy and promoting low-carbon industrial transformation.

- In July 2025, FDK CORPORATION launched a high-capacity AB2 type hydrogen storage alloy for hydrogen storage tanks, offering approximately 20% higher hydrogen storage per unit weight, stable release pressure, and easy activation. The alloy supports applications in hydrogen stations, fuel cells, and small mobility solutions, enhancing efficiency and practicality in the Hydrogen Storage Alloys Market.

Hydrogen Storage Alloys Market Report Coverage and Deliverables

The "Hydrogen Storage Alloys Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Hydrogen Storage Alloys Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Hydrogen Storage Alloys Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Hydrogen Storage Alloys Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Hydrogen Storage Alloys Market

- Detailed company profiles

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Get Free Sample For

Get Free Sample For