数字健康市场战略、主要参与者、增长机会、2031 年分析和预测

数字健康市场规模和预测(2021-2031 年)、全球和区域份额、趋势和增长机会分析报告范围:按产品(服务、软件和硬件)、类型(移动医疗、远程医疗、医疗保健分析和数字健康系统)、1mhealth(应用程序和耳机)、12 远程医疗(远程医疗和远程医疗)、应用(慢性疾病管理、行为健康、健康和健身等)、最终用户(医院和诊所、患者和消费者等)和地理位置(北美、欧洲、亚太地区、中东和非洲、南美洲和中美洲)

- 状态 : 已发布

- 报告代码 : TIPHE100000867

- 类别 : 科技、媒体和电信

- 页数 : 328

- 可用报告格式 :

- 最后更新日期 : December 02, 2025

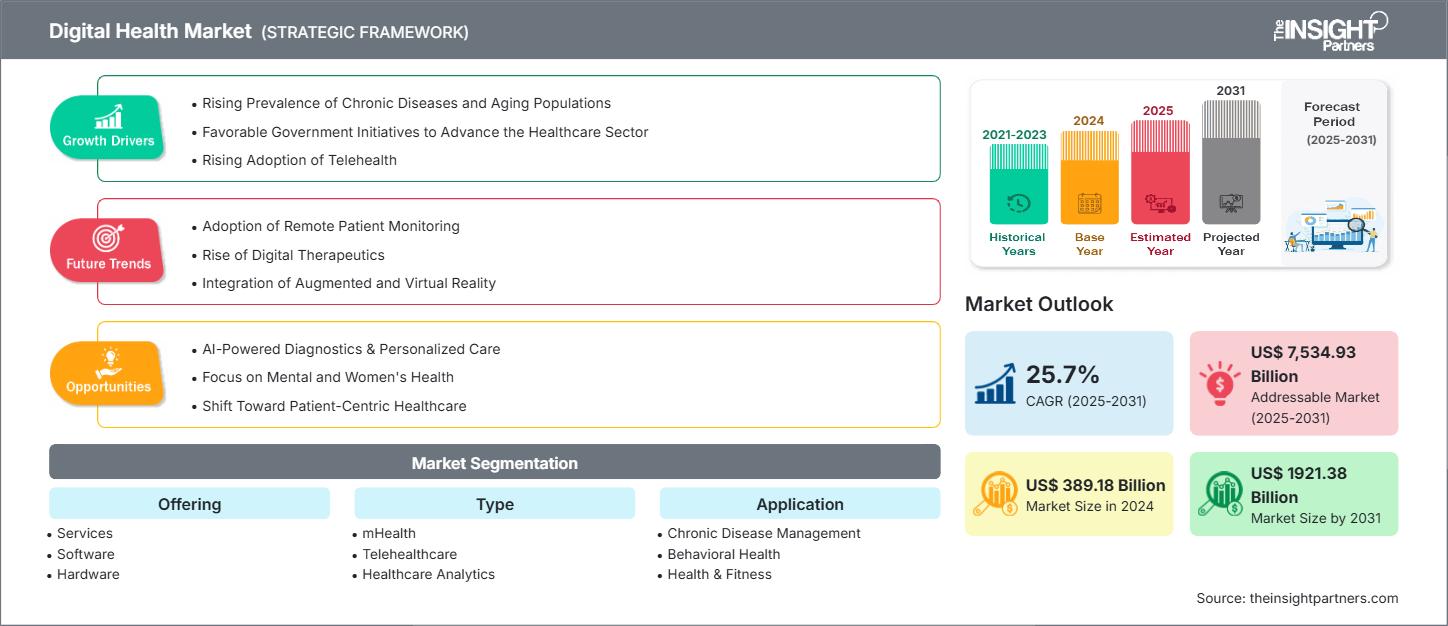

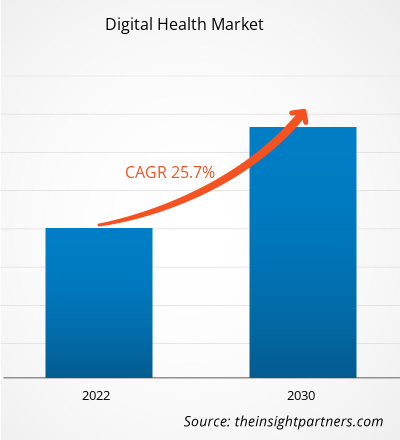

[研究报告] 预计数字健康市场规模将从2022年的3064.4304亿美元增长到2030年的19095.2456亿美元;预计2022年至2030年期间的复合年增长率为25.7%。

分析师观点:

数字健康市场预测可以帮助该市场的利益相关者规划其增长战略。互联网连接和智能设备普及率的提高、政府监管支持和政策举措的加强以及医疗IT基础设施的技术发展等因素推动了数字健康市场的增长。然而,与数据和隐私泄露相关的安全问题阻碍了市场的增长。

数字健康是指在医疗保健行业中使用信息和通信技术来远程管理慢性疾病。数字健康市场涵盖移动医疗 (mHealth)、可穿戴设备、远程医疗和远程医疗、健康信息技术 (IT) 以及定制医疗。它为消费者提供各种服务,包括早期识别危及生命的疾病和慢性病管理。数字健康带来的优势将对数字健康市场规模产生积极影响。

市场洞察:

不断增加的政府监管支持和政策举措推动数字健康市场增长

监管支持和政府举措对于塑造和推进数字健康至关重要。这些努力涵盖各种政策、法规、融资机制和战略举措,旨在提高数字健康解决方案的采用率、整合度和有效性。例如,美国国际开发署 (USAID) 设想利用数字技术使个人能够获取关键信息和服务,从而实现健康富足的生活。该机构制定了专门的政策指南“数字健康行动愿景”,用于指导其对支持合作伙伴国家健康项目的数字技术的投资。同样,印度政府于2022年启动了“阿育吠陀印度数字健康计划”(ABDM),旨在打造数字健康生态系统。同样,2021年10月,法国政府投资超过6.5亿美元,用于增强其国家数字健康基础设施。

此外,世界卫生组织(WHO)在其国家电子健康战略或数字健康工具包中将数字健康定义为“信息和通信技术(ICT)在健康领域的应用”。据WHO称,2020年,超过75%的符合条件的医疗机构和90%的符合条件的医院因参与政府鼓励医院允许患者查看、下载和传输其健康信息的计划而获得了资金。2020年5月,美国联邦政府提出了《2020-2025年联邦卫生IT战略计划》,要求医疗机构使用电子健康记录(EHR)。

因此,上述因素将促进数字健康市场份额的扩大

自定义此报告以满足您的要求

您将免费获得任何报告的定制,包括本报告的部分内容,或国家级分析、Excel 数据包,以及为初创企业和大学提供超值优惠和折扣

数字健康市场: 战略洞察

-

获取本报告的主要市场趋势。这个免费样本将包括数据分析,从市场趋势到估计和预测。

报告细分和范围:

“数字健康市场分析”通过考虑以下细分领域进行:产品、技术、应用和最终用户。

全球数字健康市场根据产品、技术、应用、最终用户和地域进行细分。数字健康市场按产品细分为软件、服务和硬件。按技术细分为移动医疗、远程医疗、数字健康系统等。按应用细分为慢性病管理、行为健康、健康和健身等。按最终用户细分为医院和诊所、患者和消费者等。医院和诊所占据了数字健康市场的最大份额。

从地理上看,全球数字健康市场报告分为北美(美国、加拿大和墨西哥)、欧洲(德国、法国、意大利、英国、西班牙和欧洲其他地区)、亚太地区(中国、日本、印度、澳大利亚、韩国和亚太其他地区)、中东和非洲(南非、沙特阿拉伯、阿联酋和中东和非洲其他地区)以及南美洲和中美洲(巴西、阿根廷和南美洲和中美洲其他地区)。

基于产品的洞察

数字健康市场根据产品分为软件、服务和硬件。服务细分市场在 2022 年占据最大市场份额,预计在 2022 年至 2030 年期间的复合年增长率最高。

基于技术的洞察

按技术划分,数字健康市场可细分为移动医疗、远程医疗、数字健康系统等。移动医疗细分市场在 2022 年占据最大市场份额。预计远程医疗细分市场在 2022 年至 2030 年期间的增长速度最快。

基于应用的洞察

按应用划分,数字健康市场可细分为慢性病管理、行为健康、健康和健身等。2022 年,慢性病管理细分市场占据最大市场份额。

基于最终用户的洞察

根据最终用户,数字健康市场可细分为医院和诊所、患者和消费者以及其他。 2022 年,医院和诊所部门占据了最大的市场份额。

区域分析:

根据地域划分,全球数字健康市场分为亚太地区、欧洲、中东和非洲、北美以及南美和中美洲。2022 年,北美占据全球市场的最大份额。预计 2022 年至 2030 年期间,亚太地区的复合年增长率最高。

北美的数字健康市场分为美国、加拿大和墨西哥。数字医疗的转型和智能医疗解决方案的日益普及,包括移动应用程序、智能可穿戴设备以及 EHR 和远程医疗服务等电子健康服务等各种技术,这些技术允许远程患者监控,是推动市场发展的主要动力。其他因素,例如医疗保健领域先进软件技术的引入、医院数量的增加以及政府战略政策的实施,也有助于推动数字健康市场的发展。

美国是北美乃至全球数字健康市场的最大贡献者。2020年9月,美国食品药品监督管理局(FDA)成立了数字健康卓越中心。该中心的成立是FDA履行其推动数字健康技术进步承诺的重要一步。这包括移动健康设备、软件即医疗设备(SaMD)、用作医疗设备的可穿戴设备以及用于研究医疗产品的技术。此外,美国主要市场参与者的存在及其发展也可能有利于市场的增长。

数字健康市场区域洞察

The Insight Partners 的分析师已详尽阐述了预测期内影响数字健康市场的区域趋势和因素。本节还探讨了北美、欧洲、亚太地区、中东和非洲以及南美和中美洲的数字健康市场细分和地域分布。

数字健康市场报告范围

| 报告属性 | 细节 |

|---|---|

| 市场规模 2024 | US$ 389.18 Billion |

| 市场规模 2031 | US$ 1921.38 Billion |

| 全球复合年增长率 (2025 - 2031) | 25.7% |

| 历史数据 | 2021-2023 |

| 预测期 | 2025-2031 |

| 涵盖的领域 |

By 产品

|

| 覆盖地区和国家 |

北美

|

| 市场领导者和主要公司简介 |

|

数字健康市场参与者密度:了解其对业务动态的影响

数字健康市场正在快速增长,这得益于终端用户需求的不断增长,而这些需求的驱动因素包括消费者偏好的不断变化、技术进步以及对产品优势的认知度不断提高。随着需求的增长,企业正在扩展其产品线,不断创新以满足消费者需求,并抓住新兴趋势,从而进一步推动市场增长。

- 获取 数字健康市场 主要参与者概述

行业发展与未来机遇:

- 2022年10月,Medulance与Reliance Jio合作推出了一款5G救护车。该救护车配备智能设备和摄像头,具有双向音视频通信、高清视频传输、位置追踪以及通过高速互联网向远程医生实时传输患者健康数据的功能。

- 2021年6月,亚马逊推出了数字健康加速器AWS Healthcare Accelerator,以支持医疗保健虚拟护理和分析领域的初创企业。该项目优先考虑远程患者监控、数据分析、患者参与、语音技术和虚拟护理。

- 2021年10月,德勤和沃达丰宣布建立战略联盟,通过与德勤合作的沃达丰健康中心,在欧洲各地扩大医疗保健服务覆盖面。此次合作旨在加快互联医疗的普及。该虚拟中心将沃达丰的互联医疗解决方案与德勤的医疗咨询专业知识相结合,使个人无论何时何地都能更便捷地获得医疗保健服务。

Cerner Corporation、Eclinicalworks、Allscripts Healthcare Solutions Inc.、霍尼韦尔国际公司、思科系统公司、通用电气医疗集团、荷兰皇家飞利浦电子公司、西门子医疗股份公司、高通技术公司和 Fitbit 公司等均是本数字医疗市场报告中重点介绍的知名公司。这些领先企业专注于扩大和多元化其市场影响力和客户群,以挖掘数字医疗市场的商机。

Ankita 是一位充满活力的市场研究和咨询专家,在科技、媒体、信息通信技术 (ICT) 以及电子和半导体领域拥有超过 8 年的经验。她成功领导并完成了 100 多项咨询和研究项目,服务对象包括微软、甲骨文、NEC Corporation、SAP、毕马威和 Expeditors International 等全球客户。她的核心能力包括市场评估、数据分析、预测、战略制定、竞争情报和报告撰写。

Ankita 擅长处理完整的项目周期——从售前的方案设计和客户洽谈,到售后提供切实可行的洞察。她擅长管理跨职能团队、构建复杂的研究模块,并根据客户特定的业务目标调整解决方案。她卓越的沟通能力、领导能力和演讲能力使她能够在快速变化的市场环境中持续提供价值驱动的成果。

- 全面的市场规模与预测分析

- 详细的细分市场分析

- 深入的市场动态评估

- 区域及国家级洞察

- 竞争格局与企业对标分析

- 战略性商业情报

客户评价

Insight Partners 的 SCADA 系统市场报告内容全面,对当前趋势和未来预测提供了宝贵的见解。该团队始终高度专业、响应迅速且乐于助人。我们非常满意,强烈推荐他们的服务。

兰·凯德姆 伙伴, Reali Technologies LTD我请求一份关于特定软件市场的报告,团队在几天内就完成了。报告信息非常相关,而且呈现得非常出色。之后,我请求对报告进行一些修改和补充。团队再次迅速响应,不到一周我就收到了最终报告。

让-埃尔韦·詹恩 主席, 未来分析公司我们与 Insight Partners 合作进行了一项重要的市场研究和预测。他们清晰地洞察了机遇和风险,帮助我们制定了计划。他们的研究简单易用,数据可靠,帮助我们做出了明智而自信的决策。我们强烈推荐他们。

皮尤什·纳格帕尔 高级副总裁, 远光全球Insight Partners 凭借其深厚的行业专业知识,提供了富有洞察力、结构合理的市场研究。他们的团队始终专业且响应迅速。用户友好的网站让访问行业报告变得顺畅无阻。我们强烈推荐他们可靠、高质量的研究服务。

安达幸彦 首席执行官, 深蓝有限责任公司这是我第一次从The Insight Partners购买市场报告。起初我有些犹豫,但访问了他们的网站后,我更放心地冒险购买市场报告。我对报告的质量和客户服务非常满意。我对最初的报告有一些疑问和意见,但在与他们的分析师通过电子邮件沟通了几次后,我相信这份报告可以作为我们战略规划流程的参考。非常感谢您抽出宝贵的时间,让这次体验如此愉快。我一定会向其他人推荐你们的服务,当我们需要更多市场数据时,你们将是我的首选。

约翰·铃木 总裁兼首席执行官、董事会董事, BK科技感谢您在处理我关于尼日利亚传染病体外诊断市场信息请求的过程中所展现的支持和专业精神。感谢您的耐心、指导,以及您愿意提供的折扣,最终促成了这笔交易。我期待未来与 Insight Partners 继续合作,这一切都要归功于您与我初次接触后留下的良好印象。

奇吉奥克博士 ONYIA 董事总经理, PineCrest 医疗保健有限公司购买理由

- 明智的决策

- 了解市场动态

- 竞争分析

- 客户洞察

- 市场预测

- 风险规避

- 战略规划

- 投资论证

- 识别新兴市场

- 优化营销策略

- 提升运营效率

- 顺应监管趋势