到 2034 年,拖车预浸料市场规模、增长和需求预测

历史数据 : 2021-2024 | 基准年 : 2025 | 预测期 : 2026-2034丝束预浸料市场规模及预测(2021-2034 年),全球及区域份额、趋势及增长机会分析报告涵盖范围:按纤维类型(碳纤维、玻璃纤维及其他)、树脂类型(环氧树脂、酚醛树脂及其他)和最终用途行业(航空航天与国防、汽车与交通运输、体育与休闲、石油与天然气及其他)划分

- 状态 : 数据发布

- 报告代码 : TIPRE00020903

- 类别 : 化学品和材料

- 页数 : 150

- 可用报告格式 :

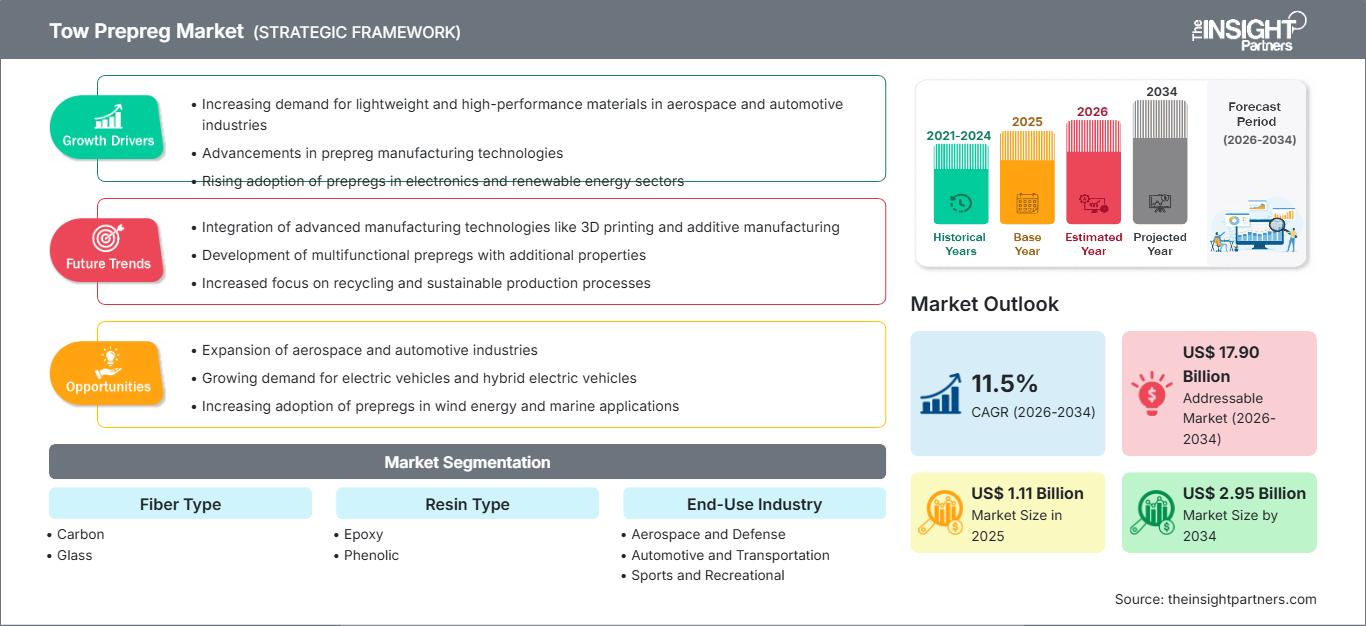

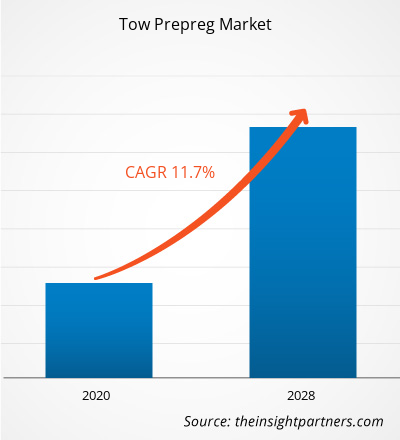

全球预浸料丝束市场规模预计将从2025年的11.1亿美元增长至2034年的29.5亿美元。预计在2026年至2034年的预测期内,该市场将以11.5%的复合年增长率增长。市场的主要驱动因素包括:全球对高速自动化复合材料制造的日益重视、行业对预浸料丝束优异的强度重量比的认识不断提高,以及对氢能储存和清洁能源解决方案的显著需求增长。此外,城市空中交通(UAM)的日益普及、航空航天中心自动化纤维铺放(AFP)技术的扩展,以及预浸料丝束在职业自行车和高尔夫等高价值运动领域的应用日益广泛,预计也将推动市场增长。

拖车预浸料市场分析

纤维束预浸料市场分析显示,随着制造商优先考虑可重复的质量和更短的生产周期,市场正向高通量批量生产转型。采购趋势表明,市场正在分化为航空航天级高模量纤维束市场和用于压力容器的高增长工业缠绕市场。氢能经济正在涌现战略机遇,其中IV型和V型储罐需要精确缠绕且树脂含量可控的碳纤维束,以确保安全性和结构完整性。分析还指出,市场扩张取决于树脂的保质期稳定性以及能够缩短烘箱或高压釜固化时间的快速固化化学技术的开发。如今,纤维-树脂系统的集成已成为竞争差异化的关键,该系统能够提供一致的横截面,并在高速缠绕过程中最大限度地减少起毛,从而帮助生产商在高成本材料市场中降低废品率。

拖车预浸料市场概览

丝束预浸料正从航空航天领域的利基专业材料转变为全球先进自动化工业的通用材料。丝束预浸料过去主要应用于军用飞机和航天硬件,如今正拓展至电动汽车传动轴、压缩天然气气瓶和热塑性工业管道等高附加值产品领域。一级航空航天供应商和专业复合材料加工商均参与到这一市场中,充分利用了触感干燥、易于自动化处理的材料的天然优势。北美和亚太地区更注重效率的制造商正在寻找传统湿式缠绕工艺的替代方案,这使得丝束预浸料作为“清洁工厂”的理想选择而广受欢迎。欧洲仍然是符合FST标准的酚醛树脂体系的中心,但北美在采用室温可储存环氧树脂丝束方面处于领先地位。在北美,受国内航空航天业复苏和商业航天项目规模化发展的推动,该市场正经历着快速增长。美国仍然是 AFP(自动纤维铺放)技术开发的主要中心,而蓬勃发展的氢气存储行业和汽车轻量化标准的现代化进一步促进了区域扩张。

根据您的需求定制此报告

获取免费定制服务拖车预浸料市场:战略洞察

-

获取本报告的主要市场趋势。这份免费样品将包含数据分析,内容涵盖市场趋势、估算和预测等。

拖车预浸料市场驱动因素和机遇

市场驱动因素:

- 卓越的自动化兼容性:预浸丝束专为 AFP、ATL 和高速长丝缠绕而设计,与手动湿式缠绕工艺相比,可提供更高的产量和更好的树脂一致性。

- 交通运输领域的轻量化要求:全球减少排放的压力正在推动航空航天和汽车底盘采用碳纤维预浸料,以在不影响安全性的前提下最大限度地减轻重量。

- 树脂体系创新:快速固化、低挥发性且符合 REACH 法规的环氧树脂和酚醛树脂体系的开发,使复合材料制造更加高效环保。

市场机遇:

- 拓展氢气储存领域:向氢能经济的转型为高性能预浸料在制造高压 IV 型和 V 型氢气罐方面提供了重要机遇。

- 热塑性预浸丝的增长:开发可回收的热塑性基丝束为实现循环经济目标和加快大批量汽车生产中的“节拍”周期提供了途径。

- 向亚太地区本土航空航天中心多元化发展:随着区域飞机生产规模的扩大,与中国和印度的新兴航空航天集群建立战略伙伴关系,可能有助于进入高利润细分市场。

拖车预浸料市场报告细分分析

对拖车预浸料市场份额进行多维度分析,以更清晰地了解其结构、增长潜力及新兴趋势。以下是大多数行业报告中常用的标准细分方法:

按纤维类型:

- 碳:由于其无与伦比的刚度重量比和抗疲劳性,成为主要的价值驱动因素,尤其是在航空航天和高压存储领域。

- 玻璃:一种经济实惠的替代品,越来越受到介电应用、工业管道和对价格敏感的体育用品的青睐。

按树脂类型:

- 环氧树脂:凭借其成熟的加工参数和优异的机械性能,仍然是结构应用的首选材料。

- 酚醛树脂:飞机内饰和公共交通的关键组成部分,因为阻燃、防烟和防毒 (FST) 合规性是强制性的安全要求。

按最终用途行业划分:

- 航空航天与国防:高模量牵引的主要渠道,用于主要结构、次要部件和下一代航天发射器。

- 汽车和运输:增长最快的工业渠道,专注于商用车的传动轴、钢板弹簧和氢燃料箱系统。

- 体育和休闲:为自行车车架、网球拍和射箭器材等消费品提供高端细分市场。

- 石油和天然气:对高强度复合管道和海上压力容器有稳定的需求。

按地理位置:

- 北美

- 欧洲

- 亚太地区

- 南美洲和中美洲

- 中东和非洲

拖车预浸料市场区域洞察

The Insight Partners 的分析师对预测期内影响拖车预浸料市场的区域趋势和因素进行了详尽的阐述。本节还探讨了北美、欧洲、亚太、中东和非洲以及南美和中美洲等地区的拖车预浸料市场细分和地域分布。

拖车预浸料市场报告范围

| 报告属性 | 细节 |

|---|---|

| 2025年市场规模 | 11.1亿美元 |

| 到2034年市场规模 | 29.5亿美元 |

| 全球复合年增长率(2026-2034 年) | 11.5% |

| 史料 | 2021-2024 |

| 预测期 | 2026-2034 |

| 涵盖的领域 |

按纤维类型

|

| 覆盖地区和国家 |

北美

|

| 市场领导者和主要公司简介 |

|

预浸料市场参与者密度:了解其对业务动态的影响

The Tow Prepreg Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Tow Prepreg Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for advanced material suppliers and composite manufacturers to expand.

The tow prepreg market is undergoing a significant transformation, moving from a manual labor-intensive process to a global high-value automated solution. Growth is driven by the rising demand for fuel efficiency, the surge in space exploration, and the expansion of the green energy sector. Below is a summary of market share and trends by region:

1. North America

Market Share: Holds a significant portion of the global market, driven by a massive aerospace defense base and commercial space innovation.

Key Drivers:

- High concentration of AFP/ATL machine installations in aerospace manufacturing hubs.

- Heavy R&D investment from the Department of Defense and NASA into solid-state rocket motor casings.

- Presence of major aerospace OEMs like Boeing and Lockheed Martin and space pioneers like SpaceX.

Trends: Scaling of OOA processing to reduce manufacturing energy footprints and the successful adoption of room-temperature-stable towpregs for industrial applications.

2. Europe

- Market Share: A dominant force in FST-compliant (Fire, Smoke, Toxicity) materials and premium automotive composites, anchored by Airbus and luxury automotive clusters in Germany and Italy.

- Key Drivers:

- Strict EU "Green Deal" mandates requiring lightweighting and carbon emission reductions in transport.

- Advanced carbon fiber production infrastructure led by companies like SGL Carbon and Solvay.

- Strong demand for offshore wind energy components using high-durability towpregs.

- Trends: A strategic shift toward thermoplastic towpregs for easier recycling and the integration of bio-based resins to meet sustainability targets.

3. Asia-Pacific

Market Share: The fastest-growing region, with China, Japan, and India acting as primary engines for fiber production and clean energy infrastructure.

Key Drivers:

- Massive investments in domestic aircraft programs (e.g., COMAC C919) and regional defense modernization.

- Government-supported hydrogen initiatives, particularly for fuel-cell buses and heavy-duty trucks in China and Japan.

- Rising production of high-end sporting goods (golf shafts, rackets, bikes) using high-modulus carbon towpregs.

Trends: Rapid expansion of domestic carbon fiber manufacturing capacity and a heavy reliance on B2B contracts for high-volume consumer and industrial composites.

4. South and Central America

Market Share: An emerging segment with a focused aerospace presence in Brazil (Embraer) and growing industrial interest in Argentina’s automotive corridor.

Key Drivers:

- Increasing localization of composite supply chains to serve regional aerospace offsets and Tier 1 suppliers.

- Modernization of oil and gas infrastructure requiring corrosion-resistant composite piping.

- Regional expansion of the CNG (Compressed Natural Gas) vehicle market.

Trends: Growth of Maintenance, Repair, and Overhaul (MRO) applications using towpregs and the introduction of composite pressure vessels for the regional transport sector.

5. Middle East and Africa

- Market Share: A developing market with strategic investments in aerospace and high-tech manufacturing hubs to diversify oil-dependent economies.

- Key Drivers:

- High demand for high-strength, corrosion-resistant composite pipes in the regional oil and gas sector.

- "Smart Factory" and "Industry 4.0" initiatives in the UAE and Saudi Arabia attracting composite innovators.

- Strategic location as a logistics hub between European fiber producers and Asian manufacturing centers.

- Trends: Implementation of high-speed filament winding for energy infrastructure and a focus on high-performance materials for regional defense and maritime security.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Hexcel Corporation, SGL Carbon, and Teijin Limited. Regional experts like Arisawa Manufacturing (Japan) and niche players like TCR Composites (USA) and Red Composites (UK) also contribute to a diverse and rapidly expanding market landscape. This competitive environment pushes vendors to differentiate through:

- Processing Speed: Developing tows that allow for winding speeds exceeding 300 m/min to dramatically improve factory ergonomics, reduce lead times, and increase throughput for mass-market applications.

- Handling Characteristics: Innovations in "tack-free" or "low-tack" tows that prevent machine fouling and enable cleaner, more precise automated fiber placement (AFP) and filament winding.

- Strength Translation: Ensuring that the high tensile strength of the fiber is fully utilized in the final cured part through optimized resin-to-fiber wetting and superior impregnation technologies.

- Customized Resin Chemistries: Formulating specialized epoxy and phenolic systems that offer specific curing profiles and thermal stability for extreme environments, such as satellite structures and hydrogen tanks.

Opportunities and Strategic Moves

- Hydrogen Storage Pressure Vessels: Capitalize on the global energy transition by optimizing carbon fiber tow prepreg for Type IV hydrogen tanks, which require high strength-to-weight ratios for fuel-cell vehicles and stationary storage.

- 航空航天现代化和电动垂直起降飞行器:与城市空中交通 (UAM) 开发商合作,提供经认证的牵引预浸料,以支持下一代电动飞机轻型、高性能机身的快速生产。

在拖车预浸料市场运营的主要公司有:

- 有泽制造株式会社

- 三菱化学株式会社

- 红色复合材料有限公司

- SGL碳

- TCR复合材料公司

- 帝人有限公司

- ENEOS公司

- 赫克斯尔公司

- 波尔彻工业

- 东丽株式会社

免责声明:以上列出的公司不分先后顺序。

拖车预浸料市场新闻及最新动态

- 2024年3月,Hexcel推出了新型HexTow® IM9 24K碳纤维,该产品具有更高的拉伸强度和更优的性价比,适用于先进的航空航天复合材料应用。该产品支持高速生产,并与多种树脂体系兼容,从而积极推动丝束预浸料市场的创新和性能提升。

- 2024年3月,TeXtreme公司推出了TeXtreme® Gapped UD,这是一种创新的铺展式碳纤维增强材料,其性能媲美单向预浸料,同时提高了树脂灌注工艺的渗透性和成本效益。该产品专为航空航天和工业应用而设计,旨在满足市场对高性能、非热压罐成型复合材料解决方案日益增长的需求,从而积极推动铺展式预浸料市场的发展。

拖车预浸料市场报告涵盖范围和交付成果

《拖车预浸料市场规模及预测(2021-2034)》报告对市场进行了详细分析,涵盖以下领域:

- 本报告涵盖全球、区域和国家层面的所有关键细分市场,并对牵引预浸料市场规模进行预测。

- 拖车预浸料市场趋势,以及市场动态,例如驱动因素、制约因素和关键机遇。

- 详细的PEST和SWOT分析

- 拖车预浸料市场分析,涵盖关键市场趋势、全球和区域框架、主要参与者、法规以及近期市场发展动态。

- 行业格局和竞争分析,包括市场集中度、热力图分析、主要参与者以及拖车预浸料市场的最新发展。

- 公司详细概况

- 历史分析(2 年)、基准年、预测(7 年)及复合年增长率

- PEST和SWOT分析

- 市场规模、价值/数量 - 全球、区域、国家

- 行业和竞争格局

- Excel 数据集

客户评价

Insight Partners 的 SCADA 系统市场报告内容全面,对当前趋势和未来预测提供了宝贵的见解。该团队始终高度专业、响应迅速且乐于助人。我们非常满意,强烈推荐他们的服务。

兰·凯德姆 伙伴, Reali Technologies LTD我请求一份关于特定软件市场的报告,团队在几天内就完成了。报告信息非常相关,而且呈现得非常出色。之后,我请求对报告进行一些修改和补充。团队再次迅速响应,不到一周我就收到了最终报告。

让-埃尔韦·詹恩 主席, 未来分析公司我们与 Insight Partners 合作进行了一项重要的市场研究和预测。他们清晰地洞察了机遇和风险,帮助我们制定了计划。他们的研究简单易用,数据可靠,帮助我们做出了明智而自信的决策。我们强烈推荐他们。

皮尤什·纳格帕尔 高级副总裁, 远光全球Insight Partners 凭借其深厚的行业专业知识,提供了富有洞察力、结构合理的市场研究。他们的团队始终专业且响应迅速。用户友好的网站让访问行业报告变得顺畅无阻。我们强烈推荐他们可靠、高质量的研究服务。

安达幸彦 首席执行官, 深蓝有限责任公司这是我第一次从The Insight Partners购买市场报告。起初我有些犹豫,但访问了他们的网站后,我更放心地冒险购买市场报告。我对报告的质量和客户服务非常满意。我对最初的报告有一些疑问和意见,但在与他们的分析师通过电子邮件沟通了几次后,我相信这份报告可以作为我们战略规划流程的参考。非常感谢您抽出宝贵的时间,让这次体验如此愉快。我一定会向其他人推荐你们的服务,当我们需要更多市场数据时,你们将是我的首选。

约翰·铃木 总裁兼首席执行官、董事会董事, BK科技感谢您在处理我关于尼日利亚传染病体外诊断市场信息请求的过程中所展现的支持和专业精神。感谢您的耐心、指导,以及您愿意提供的折扣,最终促成了这笔交易。我期待未来与 Insight Partners 继续合作,这一切都要归功于您与我初次接触后留下的良好印象。

奇吉奥克博士 ONYIA 董事总经理, PineCrest 医疗保健有限公司购买理由

- 明智的决策

- 了解市场动态

- 竞争分析

- 客户洞察

- 市场预测

- 风险规避

- 战略规划

- 投资论证

- 识别新兴市场

- 优化营销策略

- 提升运营效率

- 顺应监管趋势

获取免费样品 - 拖车预浸料市场

获取免费样品 - 拖车预浸料市场