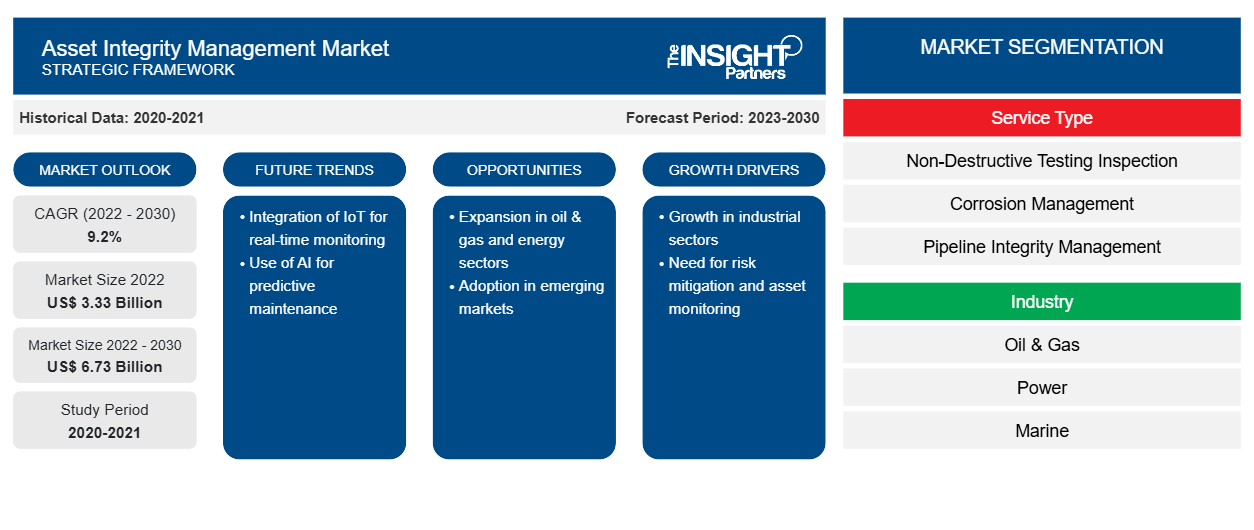

[تقرير بحثي] تم تقييم سوق إدارة سلامة الأصول بمبلغ 3.33 مليار دولار أمريكي في عام 2022 ومن المتوقع أن يصل إلى 6.73 مليار دولار أمريكي بحلول عام 2030؛ ومن المتوقع أن يسجل معدل نمو سنوي مركب بنسبة 9.2٪ من عام 2022 إلى عام 2030. تشمل اتجاهات سوق إدارة سلامة الأصول دمج إنترنت الأشياء الصناعي مع حلول إدارة سلامة الأصول.

وجهة نظر المحلل:

يمكن أن تساعد توقعات سوق إدارة سلامة الأصول أصحاب المصلحة في هذا السوق في التخطيط لاستراتيجيات النمو الخاصة بهم. يرتبط نظام إدارة سلامة الأصول بأي أنشطة للأصول مثل الحوكمة والمراقبة من أجل الحفاظ على نجاح تشغيل الشركة مع تقليل المخاطر. إن الارتفاع في الحاجة إلى السلامة التشغيلية للأصول القديمة في الصناعات القائمة على المخاطر هو الذي يدفع سوق إدارة سلامة الأصول.

تعتبر الكفاءة التشغيلية للأصول في صناعات النفط والغاز والتعدين والطاقة من أهم الأمور؛ وبالتالي، فإن الصيانة المنتظمة لهذه الأصول مهمة لتحقيق أقصى قدر من الإنتاجية. تعتبر المواد الكيميائية ومنتجات النفط والغاز قابلة للتآكل والاشتعال، وبالتالي تتطلب الفحص والصيانة المستمرة للمعدات لتحقيق الكفاءة التشغيلية والسلامة بشكل عام. علاوة على ذلك، من المتوقع أن يؤدي توسع صناعة النفط والغاز مع زيادة الطلب على النفط والغاز والنمو في صناعة الطاقة عبر العديد من البلدان إلى خلق العديد من الفرص لنمو سوق إدارة سلامة الأصول خلال فترة التنبؤ.

مع تزايد التحول الرقمي في مجموعة واسعة من الصناعات، تلعب صناعة النفط والغاز دورًا رئيسيًا في الثورة الصناعية والنمو الاقتصادي في جميع أنحاء العالم. العامل الرئيسي الذي يدفع تطور هذه الصناعة هو الطلب المرتفع على الكهرباء والطاقة والسيارات والطائرات بسبب النمو السكاني السريع. ومن المتوقع أن يزداد المعروض من النفط على مستوى العالم بسرعة لتلبية ارتفاع الطلب على الطاقة بسبب استنفاد احتياطيات النفط الحالية. ووفقًا لوكالة الطاقة الدولية، فمن المتوقع أن يزداد الطلب العالمي على النفط بنسبة 6٪ بين عامي 2022 و 2028 اعتبارًا من يونيو 2023 ليصل إلى 105.7 مليون برميل يوميًا بسبب الطلب الهائل من صناعات البتروكيماويات والطيران. وبالتالي، فإن الطلب المتزايد على النفط والغاز في قطاعي البتروكيماويات والطيران يدفع أيضًا صناعة النفط والغاز، مما يسهل توسيع حصة سوق إدارة سلامة الأصول.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق إدارة سلامة الأصول:

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

نظرة عامة على سوق إدارة سلامة الأصول:

إدارة سلامة الأصول هي شكل من أشكال معايير إدارة الأصول التي تركز على حماية المعدات والصحة والبيئة. وهي تعمل بشكل فعال وكفء للحفاظ على الأداء المتسق للأصول وتقدم العديد من المزايا، بما في ذلك تقليل المخاطر وتحسين الموثوقية وزيادة السلامة وتحسين الأداء البيئي. تُستخدم هذه الطريقة بشكل شائع في صناعات النفط والغاز والتعدين والفضاء وغيرها.

من المتوقع أن يشهد سوق إدارة سلامة الأصول نموًا في السنوات القادمة. ويعزى ذلك إلى عوامل مختلفة، بما في ذلك زيادة الحاجة إلى السلامة التشغيلية للأصول القديمة في الصناعات القائمة على المخاطر واللوائح الصارمة للسلامة التي تقودها الحكومة. علاوة على ذلك، من المتوقع أن يؤدي توسع صناعة النفط والغاز، جنبًا إلى جنب مع زيادة الطلب على النفط والغاز، إلى خلق فرص نمو للاعبين في السوق في السنوات القادمة. ومع ذلك، فإن التكلفة المترتبة على الصيانة غير ذات القيمة المضافة والتشغيل غير السليم للأصول تعيق نمو سوق إدارة سلامة الأصول.

محرك سوق إدارة سلامة الأصول:

زيادة الحاجة إلى السلامة التشغيلية للأصول القديمة في الصناعات القائمة على المخاطر

تحمي برامج إدارة سلامة الأصول قدرة الأصل على أداء وظائفه بشكل فعال، فضلاً عن إدارة أصول الشركة لتحقيق الربحية. تقدم برامج إدارة سلامة الأصول خدمات متنوعة، بما في ذلك التصميم والتفتيش والصيانة والعمليات، والتي تؤثر بشكل كبير على سلامة البنية التحتية والمعدات. كما توفر التدقيق والتفتيش وعمليات الجودة الشاملة وأدوات أخرى لإدارة سلامة الأصول بشكل فعال. تختار الصناعات مثل البتروكيماويات والنفط والغاز والطاقة المتجددة والطاقة والبنية التحتية هذه الخدمات لتحقيق إنتاجية متزايدة مع تلبية المخاوف البيئية والسلامة. تعتمد هذه الصناعات على المخاطر وتعتمد بشكل كبير على الأصول؛ وبالتالي، فإن صيانة وتفتيش هذه الأصول أمر ضروري. في صناعة النفط والغاز، تعتمد مستويات الأداء والمخاطر التشغيلية على سلامة الأصول، مثل المعدات تحت سطح البحر، وجوانب المنصات، والهياكل، ومصانع معالجة الغاز، وخطوط الأنابيب، والمصافي، والضواغط، وشبكات توزيع الغاز، في جميع أنحاء سلسلة القيمة. تعد الكفاءة التشغيلية للأصول ضرورية للغاية في صناعات النفط والغاز والتعدين والطاقة؛ وبالتالي، فإن الصيانة المنتظمة لهذه الأصول مهمة لتحقيق أقصى قدر من الإنتاجية. ومن ثم، فإن ضرورة السلامة التشغيلية بمساعدة حلول إدارة سلامة الأصول هي التي تقود سوق إدارة سلامة الأصول.

تعتبر المواد الكيميائية ومنتجات النفط والغاز قابلة للتآكل والاشتعال وتتطلب فحصًا مستمرًا وصيانة للمعدات لتحقيق الكفاءة التشغيلية والسلامة بشكل عام. تضمن خدمات إدارة سلامة الأصول تحسين الموثوقية والإنتاجية وسلامة المعدات لتحقيق أداء عالي الجودة بشكل مستدام. يوفر العديد من اللاعبين في السوق في جميع أنحاء العالم برامج إدارة سلامة الأصول لإدارة الأداء والمخاطر التشغيلية. على سبيل المثال، توفر DNV Group AS مجموعة برامج سلامة الأصول Synergi، والتي تقدم منصة أساسية لدعم إدارة السلامة الفعالة القائمة على المخاطر في الصناعات القائمة على المخاطر مثل النفط والغاز. وبالتالي، فإن الحاجة إلى السلامة التشغيلية للأصول القديمة في الصناعات القائمة على المخاطر هي من بين العوامل التي تساهم في نمو حجم سوق إدارة سلامة الأصول.

تحليل القطاعات:

ينقسم سوق إدارة سلامة الأصول إلى نوع الخدمة والصناعة. بناءً على نوع الخدمة، يتم تقسيم السوق إلى فحص الاختبار غير المدمر (NDT) ، وإدارة التآكل، وإدارة سلامة خطوط الأنابيب، وإدارة سلامة الهياكل، والتفتيش القائم على المخاطر (RBI)، وغيرها. بناءً على الصناعة، يتم تقسيم السوق إلى النفط والغاز، والطاقة، والبحرية، والتعدين، والفضاء الجوي، وغيرها.

التحليل الإقليمي:

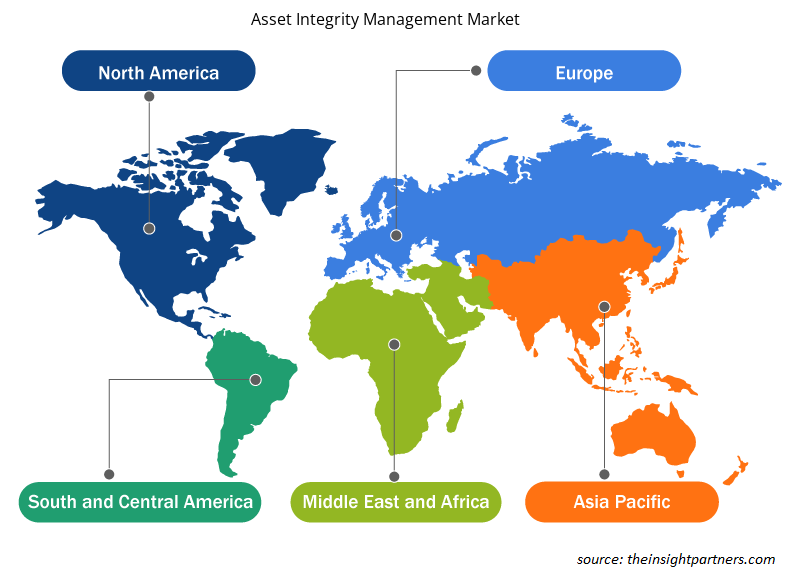

يتضمن تقرير سوق إدارة سلامة الأصول أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى. من حيث الإيرادات، سيطرت أمريكا الشمالية على حصة سوق إدارة سلامة الأصول. ينقسم سوق إدارة سلامة الأصول في أمريكا الشمالية إلى الولايات المتحدة وكندا والمكسيك. تشهد البلدان الثلاثة زيادة في تبني خدمات إدارة سلامة الأصول خلال السنوات القليلة الماضية. تعتمد صناعات النفط والغاز والمواد الكيميائية والطاقة والموارد الطبيعية على البنية التحتية الخاصة لتشغيل عملياتها، وهذه البنية التحتية تتقادم بسرعة، مما يزيد من خطر الفشل.

في صناعة النفط والغاز، تكون البنية الأساسية لمعظم حقول النفط الناضجة قديمة، مما يؤدي إلى التآكل والتقشر وتلف معدات الآبار ويسبب مشاكل أخرى تتعلق بسلامة الآبار. وتزيد هذه المشكلات من المخاطر التشغيلية للشركات والمرافق، مما يتطلب المزيد من رأس المال في مشاريع ترقية البنية الأساسية. تحتاج صناعة النفط والغاز في أمريكا الشمالية إلى اتباع العديد من السياسات واللوائح الحكومية لحماية البيئة والحفاظ على الموارد الثقافية وحماية صحة العمال وسلامتهم. البنية الأساسية في المنبع والمصب في المنطقة هائلة.

الولايات المتحدة هي أكبر منتج للنفط والغاز الطبيعي، والذي يتضمن أنشطة الاستكشاف والتكرير والنقل. كما أضافت شركات الحفر في الولايات المتحدة منصات نفطية جديدة، مما رفع العدد الإجمالي لمنصات النفط إلى 862. تمتلك الولايات المتحدة أكثر من 2.5 مليون كيلومتر من خطوط أنابيب النفط والغاز، في حين تمتلك كندا حوالي 800000 كيلومتر من خطوط الأنابيب. نتيجة لبنيتها التحتية الضخمة والقديمة، من المرجح أن تهيمن أمريكا الشمالية على السوق خلال فترة التوقعات. علاوة على ذلك، تمتلك الولايات المتحدة بعضًا من أقدم أنظمة توليد الطاقة في العالم. الولايات المتحدة هي أكبر منتج للطاقة في العالم، والتكسير الهيدروليكي والحفر الأفقي هي تقنيات ساعدت في زيادة إنتاج الطاقة في هذا البلد. وبالتالي، من المتوقع أن تولد اللوائح الحكومية الصارمة ووجود شبكة ضخمة من خطوط أنابيب الغاز فرصًا لزيادة اعتماد إدارة سلامة الأصول عبر مختلف الصناعات، مما من المرجح أن يغذي نمو سوق إدارة سلامة الأصول في أمريكا الشمالية.

تحليل اللاعب الرئيسي:

ويستند تحليل سوق إدارة سلامة الأصول على الأداء السنوي للاعبين الرئيسيين مثل SGS AG؛ وIntertek Group plc؛ وAker Solutions ASA؛ وBureau Veritas SA؛ وFluor Corporation؛ وDNV GL AS؛ وJohn Wood Group PLC؛ وOceaneering International, Inc.؛ وRosen Group؛ وCybernetix SA.تم تحليل العديد من اللاعبين الأساسيين الآخرين في سوق إدارة سلامة الأصول للحصول على رؤية شاملة للسوق ونظامه البيئي. ويؤكد تقرير سوق إدارة سلامة الأصول على العوامل الرئيسية التي تدفع السوق وتطورات اللاعبين البارزين.

رؤى إقليمية حول سوق إدارة سلامة الأصول

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق إدارة سلامة الأصول طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق إدارة سلامة الأصول والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق إدارة سلامة الأصول

نطاق تقرير سوق إدارة سلامة الأصول

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2022 | 3.33 مليار دولار أمريكي |

| حجم السوق بحلول عام 2030 | 6.73 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2022 - 2030) | 9.2% |

| البيانات التاريخية | 2020-2021 |

| فترة التنبؤ | 2023-2030 |

| القطاعات المغطاة | حسب نوع الخدمة

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في سوق إدارة سلامة الأصول: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق إدارة سلامة الأصول نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق إدارة سلامة الأصول هي:

- شركة اس جي اس اس ايه

- مجموعة إنترتك المحدودة

- شركة اكر سوليوشنز ايه اس ايه

- بيرو فيريتاس إس إيه

- شركة فلور

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق إدارة سلامة الأصول

التطورات الأخيرة:

تركز الشركات العاملة في سوق إدارة سلامة الأصول على كل من الاستراتيجيات غير العضوية والعضوية لنمو أعمالها. وفيما يلي قائمة ببعض التطورات الرئيسية الأخيرة في السوق من قبل اللاعبين في سوق إدارة سلامة الأصول المذكورة أعلاه:

- في مايو 2023، شاركت شركة إس جي إس في مؤتمر ومعرض إدارة سلامة الأصول في الشرق الأوسط (AIMCS) في أبوظبي، الإمارات العربية المتحدة. تم تنظيم الحدث تحت الرئاسة الفنية لشركة أدنوك لمعالجة الغاز. تمت دعوة أكثر من 300 خبير ومتخصص في الصناعة لمناقشة أحدث الاتجاهات وأفضل الممارسات في إدارة سلامة الأصول.

- في مارس 2021، حصلت شركة Stork، وهي شركة تابعة لشركة Fluor، على تمديد عقد لمدة عامين من شركة Chrysaor Holdings Limited لتقديم خدمات سلامة الأصول المتخصصة المتكاملة في الخارج في المملكة المتحدة. ستواصل الشركة تقديم مجموعة شاملة من حلول وقدرات إدارة الأصول لتمديد دورة حياة الأصول البحرية من خلال هذا العقد لمنصات Armada وEverest وLomond في وسط بحر الشمال.

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

- Fish Protein Hydrolysate Market

- Artificial Intelligence in Defense Market

- Emergency Department Information System (EDIS) Market

- Extracellular Matrix Market

- Bioremediation Technology and Services Market

- Ceiling Fans Market

- Joint Pain Injection Market

- Customer Care BPO Market

- Biopharmaceutical Tubing Market

- Medical Devices Market

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

The non-destructive testing (NDT) inspection segment led the asset integrity management market with a significant share in 2022 and corrosion management segment is expected to grow with the highest CAGR.

Increase in need for operational safety of aging assets in risk-based industries and stringent government safety regulations are driving factors of asset integrity management market.

The asset integrity management market was estimated to be valued at US$ 3.33 billion in 2022 and is projected to reach US$ 6.73 billion by 2030; it is expected to grow at a CAGR of 9.2% during the forecast period.

APAC is anticipated to grow with the highest CAGR over the forecast period.

The key players holding majority shares in the asset integrity management market include Fluor Corporation, Aker Solutions, Intertek Group plc, John Wood Group PLC, and Bureau Veritas.

The integration of digital twin and IIoT with asset integrity management software is expected to drive the growth of the asset integrity management market in the coming years.

The asset integrity management market is expected to reach US$ 6.73 billion by 2030.

The List of Companies - Asset Integrity Management Market

- SGS SA

- Intertek Group Plc

- Aker Solutions ASA

- Bureau Veritas SA

- Fluor Corp

- DNV Group AS

- John Wood Group Plc

- ROSEN Group

- TechnipFMC plc

- Oceaneering International Inc

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير