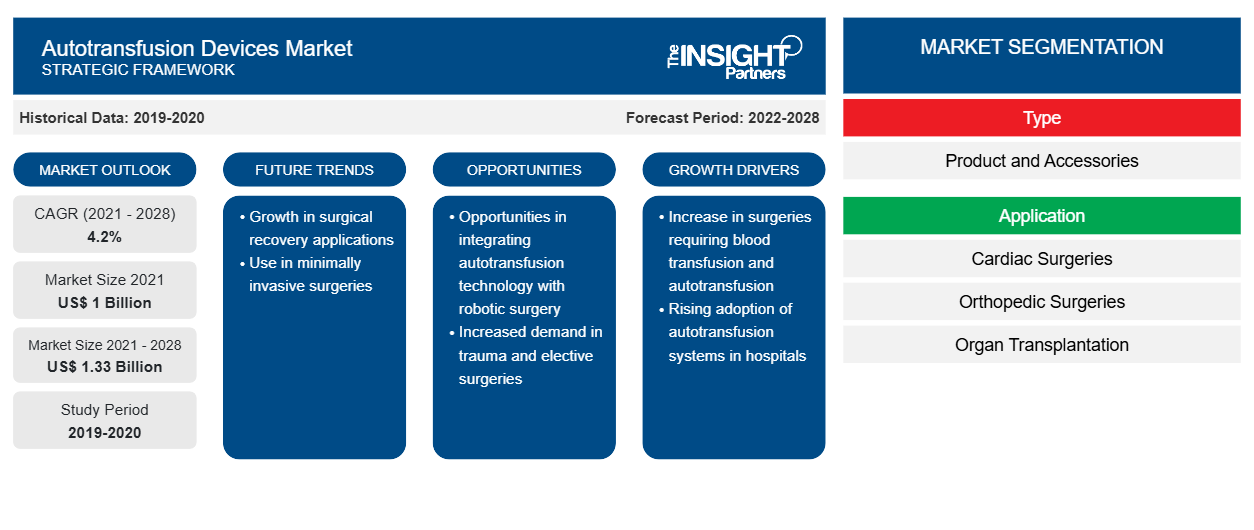

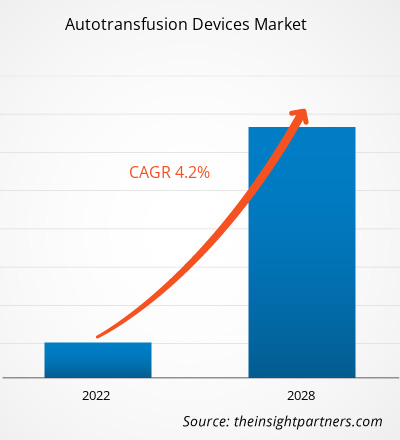

من المتوقع أن ينمو سوق أجهزة نقل الدم الذاتي من 1,000.26 مليون دولار أمريكي في عام 2021 إلى 1,331.99 مليون دولار أمريكي بحلول عام 2028؛ ومن المتوقع أن ينمو بمعدل نمو سنوي مركب قدره 4.2٪ من عام 2021 إلى عام 2028.

زراعة الأعضاء هي عملية جراحية تُجرى في حالة فشل الأعضاء. وعادةً ما تُجرى زراعة الأعضاء لأعضاء مثل القلب والكبد والكلى؛ ومع ذلك، مع ارتفاع حالات الأمراض المزمنة، هناك حاجة إلى زراعة أعضاء أخرى مثل الرئتين والبنكرياس والقرنية والأنسجة الوعائية. تستغرق هذه الإجراءات عادةً ساعات، ويحدث فقدان كبير للدم، ويعد نقل الدم الذاتي أحد الطرق القيمة لمنع فقدان الدم. ووفقًا للشبكة المتحدة لمشاركة الأعضاء (UNOS)، فقد زادت عمليات زراعة الأعضاء التي تُجرى في الولايات المتحدة باستمرار، حيث أُجريت أكثر من 41000 عملية زراعة في عام 2021. وبالمثل، وفقًا لبيانات سجل زراعة الأعضاء العالمي، شكلت إسبانيا 20% من جميع التبرعات بالأعضاء في الاتحاد الأوروبي في عام 2019 و6% من التبرعات في جميع أنحاء العالم. تحسن معدل التبرع بالأعضاء في أستراليا في السنوات الأخيرة، حيث ارتفع إلى 21.8 متبرعًا لكل مليون نسمة في عام 2019.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق أجهزة نقل الدم الذاتية:

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

وبالمثل، يبلغ عدد المتبرعين في كندا 22.2 لكل مليون نسمة، ويشهد هذا المعدل تحسناً مطرداً، ويعزى ذلك جزئياً إلى عدد "أطباء التبرع" - أطباء العناية المركزة المسؤولين عن التبرع بالأعضاء. ووفقاً لسجل زراعة الأعضاء العالمي، كان لدى الصين 5818 متبرعاً في عام 2019، أو 4.1 لكل مليون نسمة، وكان لدى الهند 715 متبرعاً أو 0.5 لكل مليون نسمة في عام 2019. من ناحية أخرى، كان لدى روسيا معدل أعلى قليلاً بلغ 5.1 متبرعاً لكل مليون نسمة. وقد ساهمت الشراكة بين القطاعين العام والخاص بالتعاون مع منسقي عمليات زراعة الأعضاء بشكل كبير في تحسين زراعة الأعضاء. وشهدت كل من البلدان النامية والمتقدمة زيادة في جراحات زراعة الأعضاء. على سبيل المثال، تبرز البلدان النامية مثل الهند وسنغافورة كوجهات للسياحة الطبية في منطقة آسيا والمحيط الهادئ. وتتقدم البلدان من حيث توفير علاجات طبية أفضل وأكثر تقدماً. وبالتالي، فإن الحاجة المتزايدة إلى زراعة الأعضاء هي من بين العوامل الرئيسية التي تدفع الطلب على تشخيصات زراعة الأعضاء مثل أجهزة نقل الدم الذاتي.

تتضمن عملية نقل الدم الذاتي إعادة ضخ دم المريض. يتم جمع الدم من تجويف الصفاق أو منطقة الصدر. يمكن إجراء العملية قبل الجراحة أو أثناء الجراحة وبعدها باستخدام نظام نقل الدم الذاتي. تتطلب الإجراءات الطبية، مثل استبدال المفاصل وجراحات العمود الفقري والقلب، من بين أمور أخرى، نقل الدم الذاتي. يساعد ذلك في تقليل خطر العدوى، كما أنه يزيل المشاكل والمضاعفات المرتبطة بتخزين وإدارة دم المتبرع المتماثل. يساعد ذلك في منع انتقال الأمراض المنقولة بالدم المرتبطة بنقل الدم بين المرضى.

رؤى السوق

التطورات التكنولوجية في أجهزة نقل الدم الذاتية

تُستخدم أجهزة نقل الدم الذاتية عادةً أثناء العمليات الجراحية التي تستغرق ساعات طويلة، مثل زراعة الكلى، وفي حالات الطوارئ. ترتبط هذه العمليات الجراحية باحتمالات فقدان الدم المفرط، مما يجعل من الصعب تعويض فقدان الدم بدم جديد، خاصة في حالة فصائل الدم النادرة. ونظرًا للطلب الكبير، يقدم اللاعبون الرئيسيون في سوق أجهزة نقل الدم الذاتية أجهزة نقل دم ذاتية متقدمة وآلية بالكامل تقلل من التدخلات البشرية. على سبيل المثال، في أبريل 2021، تمت الموافقة على جهاز B-Capta من LivaNova PLC من قبل إدارة الغذاء والدواء الأمريكية. أثناء جراحات مجازة القلب والرئة المعقدة للأطفال والبالغين، يساعد هذا الجهاز في المراقبة السريعة والدقيقة لمعلمات الوريد وغازات الدم. وبالمثل، في أبريل 2019، أطلقت BD وسائط مراقبة الجودة BD BACTEC في جميع أنحاء العالم للمساعدة في تحديد وحدات الصفائح الدموية الملوثة أثناء عمليات نقل الدم.

علاوة على ذلك، وظفت العديد من الشركات أنشطة استراتيجية مثل عمليات الاستحواذ والشراكة وغيرها للاستحواذ على السوق. على سبيل المثال، استحوذت شركة Medtronics على شركة AV Medical Technologies في أكتوبر 2019. وفي ديسمبر 2019، اشترت شركة Getinge شركة Applikon Biotechnology، وهي شركة عالمية رائدة في تطوير وتوريد أنظمة المفاعلات الحيوية المبتكرة من المختبر إلى النطاق الصناعي. وبالتالي، من المرجح أن تؤدي مثل هذه التطورات إلى ظهور اتجاهات جديدة في سوق أجهزة نقل الدم الذاتية في السنوات القادمة.

رؤى قائمة على التطبيق

بناءً على التطبيق، يتم تقسيم سوق أجهزة نقل الدم الذاتي إلى جراحات القلب، وجراحات العظام، وزرع الأعضاء، وإجراءات الصدمات، وغيرها. استحوذ قطاع جراحات القلب على أكبر حصة من السوق في عام 2021، في حين من المتوقع أيضًا أن يسجل قطاع زراعة الأعضاء أعلى معدل نمو سنوي مركب في السوق خلال فترة التوقعات.

يتبنى لاعبو سوق أجهزة نقل الدم الذاتي استراتيجيات عضوية مثل إطلاق المنتج والتوسع لتوسيع نطاق وجودهم ومحفظة منتجاتهم عالميًا وتلبية الطلب المتزايد. تم وصف التطورات التي أجرتها الشركات في سوق أجهزة نقل الدم الذاتي بأنها تطورات عضوية وغير عضوية. تركز العديد من الشركات على الاستراتيجيات العضوية، مثل إطلاق المنتج والتوسع. كانت استراتيجيات النمو غير العضوية التي شهدتها سوق أجهزة نقل الدم الذاتي عبارة عن شراكات وتعاون. ساعدت استراتيجيات النمو هذه لاعبي سوق أجهزة نقل الدم الذاتي في توسيع أعمالهم وتعزيز وجودهم الجغرافي. بالإضافة إلى ذلك، ساعدت استراتيجيات النمو مثل عمليات الاستحواذ والشراكات في تعزيز قاعدة عملائهم وزيادة محفظة المنتجات. لقد حققت الشركات أقصى قدر من نموها من خلال العديد من الاستراتيجيات غير العضوية لتعزيز قيمة سوق أجهزة نقل الدم الذاتي ومكانتها في سوق أجهزة نقل الدم الذاتي. تشكل التطورات العضوية 66.67٪ من إجمالي التطورات الاستراتيجية في سوق أجهزة نقل الدم الذاتي. في حين تمثل الاستراتيجيات غير العضوية 33.33٪ من نمو الشركات.

تم تقسيم سوق أجهزة نقل الدم الذاتي على النحو التالي:

يتم تقسيم سوق أجهزة نقل الدم الذاتي بناءً على النوع والتطبيق والمستخدم النهائي. بناءً على النوع، يتم تقسيم سوق أجهزة نقل الدم الذاتي إلى منتجات وملحقات. يتم تقسيم سوق أجهزة نقل الدم الذاتي، بناءً على التطبيق، إلى جراحات القلب، وجراحات العظام، وزرع الأعضاء، وإجراءات الصدمات، وغيرها.

ينقسم سوق أجهزة نقل الدم الذاتي، حسب المستخدم النهائي، إلى المستشفيات والعيادات المتخصصة ومراكز الجراحة الخارجية.

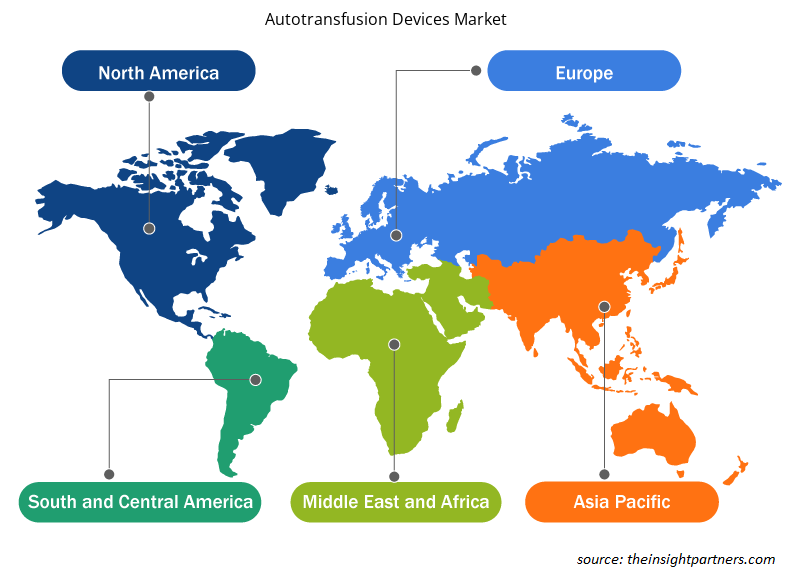

رؤى إقليمية حول سوق أجهزة نقل الدم الذاتي

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق أجهزة نقل الدم الذاتي طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق أجهزة نقل الدم الذاتي والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق أجهزة نقل الدم الذاتي

نطاق تقرير سوق أجهزة نقل الدم الذاتي

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2021 | 1 مليار دولار أمريكي |

| حجم السوق بحلول عام 2028 | 1.33 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2021 - 2028) | 4.2% |

| البيانات التاريخية | 2019-2020 |

| فترة التنبؤ | 2022-2028 |

| القطاعات المغطاة | حسب النوع

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

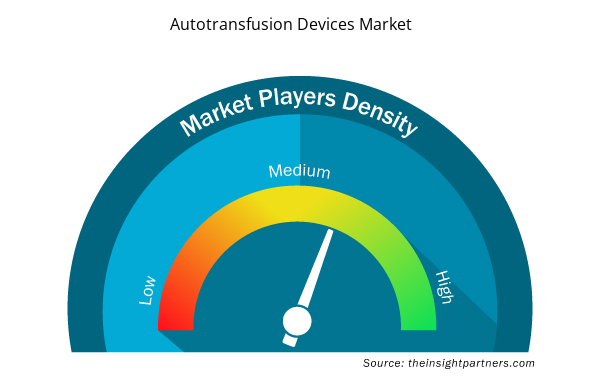

كثافة اللاعبين في السوق: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق أجهزة نقل الدم الذاتي نموًا سريعًا، مدفوعًا بالطلب المتزايد من جانب المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق أجهزة نقل الدم الذاتي هي:

- ميدترونيك

- شركة فريسينيوس اس اي اند كو. كيه جي ايه

- شركة تليفليكس المحدودة

- بنغلاديش

- زيمر بيوميت

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق أجهزة نقل الدم الذاتي

نبذة عن الشركات في سوق أجهزة نقل الدم الذاتية

- بنغلاديش

- برايل بيوميديكا

- شركة فريسينيوس اس اي اند كو. كيه جي ايه

- شركة هيمونيتيك

- شركة ليفانوفا المحدودة

- ميدترونيك

- ريداكس سبا

- شركة سارستدت ايه جي وشركاه

- شركة تليفليكس المحدودة

- زيمر بيوميت

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

The autotransfusion devices market majorly consists of the players such as Medtronic; Fresenius SE & Co. KGaA; Teleflex Incorporated; BD; Zimmer Biomet; Braile Biomedica; Haemonetics Corporation; SARSTEDT AG and Co. KG; LivaNova PLC; Redax S.p.A. among others.

Global autotransfusion devices market is segmented by region into North America, Europe, Asia Pacific, Middle East & Africa and South & Central America. In North America, the U.S. is the largest market for autotransfusion devices. The US is estimated to hold the largest share in the autotransfusion devices market during the forecast period. The growth of the market is attributed to factors such as increasing prevalence of cancer in the US, and cancer awareness initiatives undertaken by local governments and global health organizations. In addition, growth involvement of rare blood groups, rising number of transplant procedures and rising prevalence of chronic diseases in the region stimulate the growth of autotransfusion devices market in North America. On the other hand, need for reinfusion of blood, and advancements in healthcare facilities and infrastructure in the Asia Pacific are expected to account for the fastest growth of the region during the coming years.

The ambulatory surgery centers segment dominated the global autotransfusion devices market and accounted for the largest revenue share of 30.12% in 2021.

The organ transplantation segment dominated the global autotransfusion devices market and held the largest revenue share of 3.22% in 2021.

The accessories segment dominated the global autotransfusion devices market and held the largest revenue share of 55.66% in 2021.

The intraoperative autotransfusion systems segment dominated the global autotransfusion devices market and held the largest revenue share of 71.70% in 2021

Key factors that are driving the growth of this market are rapid increase in chronic diseases, rise in transplant, and difficulty in obtaining blood of rare groups.

The autotransfusion process involves the reinfusion of the patient's blood collected from the peritoneal cavity or thorax region. The process can be accomplished before surgery or during and after the surgery using the autotransfusion system. Medical procedures, such as joint replacement, spinal surgeries, and cardiac surgery require autotransfusion. It helps reduce the risk of infection, and abolishes the problems and complications associated with the banking and administration of homologous donor blood. It also prevents transmission of transfusion-related blood-borne diseases in patients.

The List of Companies - Autotransfusion Devices Market

- Medtronic

- Fresenius SE & Co. KGaA

- Teleflex Incorporated

- BD

- Zimmer Biomet

- Braile Biomedica

- Haemonetics Corporation

- SARSTEDT AG and Co. KG

- LivaNova PLC

- Redax S.p.A.

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير