تقرير سوق البنية التحتية للبث 2028 حسب القطاعات والجغرافيا والديناميكيات والتطورات الأخيرة والرؤى الاستراتيجية

البيانات التاريخية : 2019-2020 | سنة الأساس : 2021 | فترة التنبؤ : 2022-2028توقعات سوق البنية التحتية للبث حتى عام 2028 - تأثير كوفيد-19 والتحليل العالمي حسب المكونات (الأجهزة والبرامج والخدمات)، والتكنولوجيا (البث الرقمي والتناظري)، والتطبيق (OTT، والبث الأرضي، والأقمار الصناعية، وIPTV، وغيرها)

- تاريخ التقرير : Sep 2021

- رمز التقرير : TIPRE00010798

- الفئة : الإلكترونيات وأشباه الموصلات

- الحالة : نُشرت

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 198

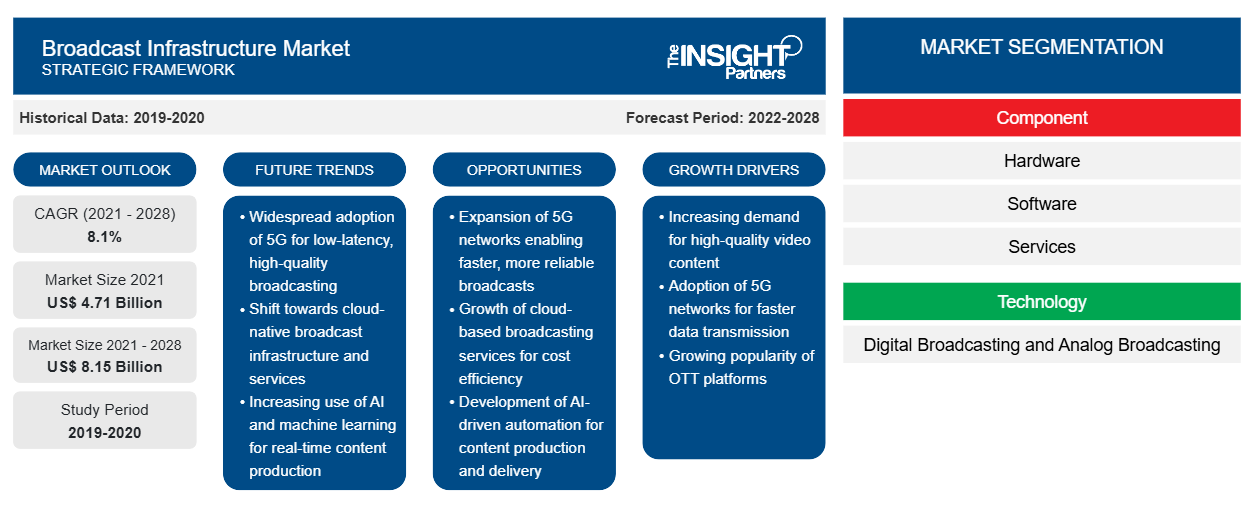

[تقرير بحثي] تم تقييم سوق البنية التحتية للبث بمبلغ 4،713.7 مليون دولار أمريكي في عام 2021 ومن المتوقع أن يصل إلى 8،145.7 مليون دولار أمريكي بحلول عام 2028؛ ومن المتوقع أن ينمو بمعدل نمو سنوي مركب قدره 8.1٪ من عام 2021 إلى عام 2028.

لقد أدى التحول النموذجي لصناعة البث من التكنولوجيا التناظرية إلى الرقمية إلى إدخال بنية تحتية متقدمة للبث، وهي معقدة نسبيًا. تشهد صناعة البث طلبًا كبيرًا على تقنيات البث الجديدة مثل تلفزيون بروتوكول الإنترنت (IPTV) وتلفزيون الويب والتلفزيون عالي الدقة (HDTV) والدفع مقابل المشاهدة. ومن المتوقع أن يمهد الطلب على تجارب الفيديو الغنية الطريق أمام شركات البث في جميع أنحاء العالم، وخاصة في آسيا. وهناك عامل رئيسي آخر يدفع سوق البنية التحتية للبث وهو المنصات المتكاملة المكونة من الخوادم وأجهزة فك التشفير وأنظمة حماية محتوى الفيديو، إلى جانب الأدوات المناسبة والبرامج الوسيطة والفوترة، مما يسمح بتوفير مجموعة متنوعة من خدمات التلفزيون في العديد من التنسيقات، مثل الفيديو عند الطلب والبث المباشر والتلفزيون المتغير زمنيًا، استنادًا إلى مجموعة من شبكات IP الأساسية وأنظمة DSL أو الوصول البصري. في الوقت الحاضر، ينتقل البائعون من البنية التحتية القائمة على الأجهزة إلى البنية التحتية القائمة على البرامج بسبب التكلفة العالية للبنية التحتية لأجهزة البث وتكلفة الصيانة العالية والترقيات المتكررة للأجهزة. لقد شهدت صناعة البث ابتكارات ثورية مع التطورات التكنولوجية لتوفير تجربة أفضل للمستخدمين وخلق فرص لبائعي البنية التحتية للبث.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق البنية التحتية للبث: رؤى استراتيجية

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

تأثير جائحة كوفيد-19 على سوق البنية التحتية للبث

في ظل جائحة كوفيد-19، يعمل عدد كبير من الأفراد من المنزل ويقضون وقتًا أطول على الإنترنت ويفتخرون بالتحول إلى العالم الرقمي. ويزيد هذا الطلب على الموارد الرقمية من الضغط على أنظمة العديد من منظمات البرمجيات والمنصات ويعيق قدرتها على تقديم الخدمات بموثوقية وجودة. ومع ذلك، فقد أثر تفشي كوفيد-19 سلبًا على اللاعبين المشاركين في تقديم محتوى الفيديو للمستخدمين النهائيين، بسبب إغلاق الأعمال وندرة العمالة. كما قلبت أزمة كوفيد-19 العمليات بشكل كبير عبر سلسلة القيمة، من شبكات الموردين إلى تجربة توصيل العملاء بسبب إغلاق الأعمال وحظر السفر وانقطاعات سلسلة التوريد.

رؤى السوق – سوق البنية التحتية للبث

تزايد اعتماد تقنيات البث الجديدة

مع التحسن المستمر في التحول الرقمي وزيادة الدخل المتاح، يشهد السوق معدل تبني مرتفع لـ IPTV و HDTV. ومن المتوقع أن يمهد الطلب على تجارب الفيديو الغنية الطريق أمام شركات البث في جميع أنحاء العالم، وخاصة في آسيا. ويتزايد انتشار النطاق العريض في جميع أنحاء منطقة آسيا والمحيط الهادئ، وذلك بسبب المشاهدة الاستهلاكية عند الطلب. وعلاوة على ذلك، تكتسب منصات OTT القائمة على الاشتراك مثل Netflix قوة دفع في آسيا. ومن المتوقع أن يؤدي زيادة الإنفاق الحكومي على البنية التحتية القائمة على السحابة والحلول القائمة على السحابة والخدمات المدارة والشبكات الهجينة إلى تعزيز نمو سوق البنية التحتية للبث. كما ستشجع المخاوف الأمنية المتزايدة والحفاظ على ثقة العملاء شركات البث على تبني نماذج توصيل جديدة. ومن المرجح أن يكون لجميع التطورات والتقدم تأثير إيجابي على نمو السوق خلال فترة التنبؤ.

رؤى قائمة على المكونات

بناءً على المكون، يتم تقسيم سوق البنية التحتية للبث إلى أجهزة وبرامج وخدمات. احتل قطاع البرامج الحصة الأكبر في السوق في عام 2020.

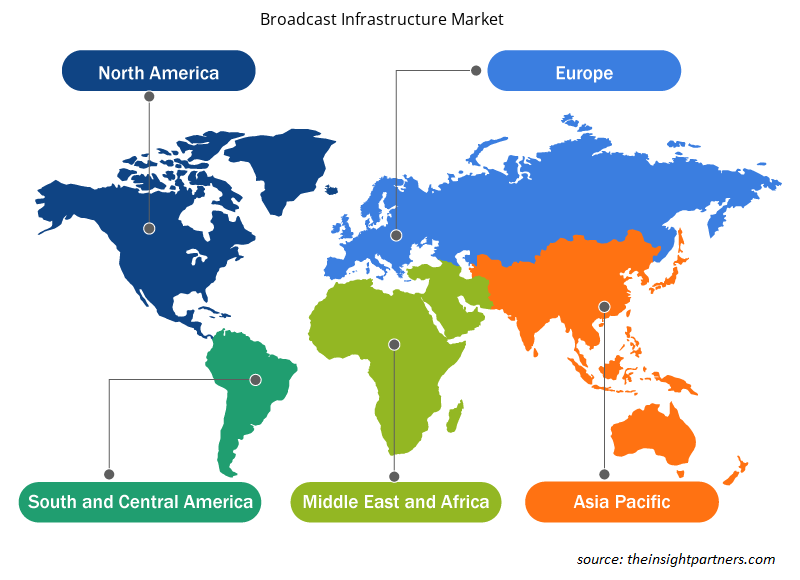

رؤى إقليمية حول سوق البنية التحتية للبث

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق البنية التحتية للبث طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق البنية التحتية للبث والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق البنية التحتية للبث

نطاق تقرير سوق البنية التحتية للبث

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2021 | 4.71 مليار دولار أمريكي |

| حجم السوق بحلول عام 2028 | 8.15 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2021 - 2028) | 8.1% |

| البيانات التاريخية | 2019-2020 |

| فترة التنبؤ | 2022-2028 |

| القطاعات المغطاة | حسب المكون

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

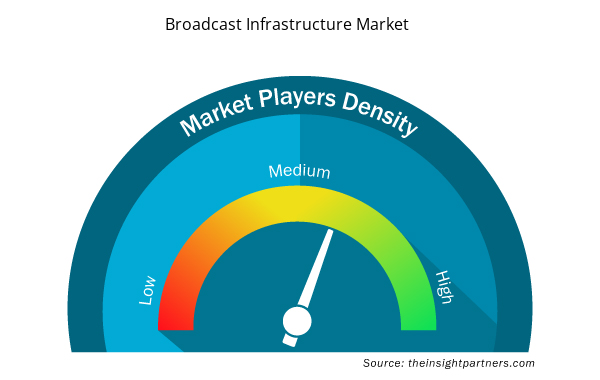

كثافة اللاعبين في السوق: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق البنية التحتية للبث نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلك المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق البنية التحتية للبث هي:

- شركة سيسكو سيستمز

- تكنولوجيا البث كلايد

- شركة سي إس لأنظمة الكمبيوتر المحدودة

- شركة داكاست

- شركة EVS لمعدات البث

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق البنية التحتية للبث

يركز اللاعبون العاملون في سوق البنية التحتية للبث بشكل أساسي على تطوير المنتجات المتقدمة والفعالة.

- في يونيو 2021، أعلنت شركة EVS، المزود الرائد لتكنولوجيا الفيديو المباشر للبث والإنتاج الإعلامي الجديد، عن شراكتها مع شركة Gravity Media لتزويدها بنظام مراجعة Xeebra متعدد الكاميرات باعتباره التكنولوجيا الأساسية لحل التحكيم عبر الفيديو والاتصالات المتكامل الجديد للشركة.

- في يونيو 2021، أعلنت شركة Ross Video عن الاستحواذ على شركة Primestream، وهي شركة حلول سير عمل أصول الوسائط. يستخدم العملاء هذه الحلول في مختلف القطاعات السوقية، بما في ذلك المؤسسات والوسائط الرقمية والرياضة والبث. تم تصميم حلولهم لحل التحديات الإبداعية والتجارية والتكنولوجية الفريدة والمعقدة بشكل متزايد في كل سوق. من خلال هذا الاستحواذ، ستسعى شركة Ross بشكل طبيعي إلى دمج حل إدارة أصول الوسائط Streamline مع منتجات Primestream بمرور الوقت، لإنشاء منصة إدارة أصول الرسوميات والإنتاج المتقاربة بالكامل.

تم تقسيم سوق البنية التحتية للبث على النحو التالي:

سوق البنية التحتية للبث – حسب المكون

- الأجهزة

- برمجة

- خدمات

سوق البنية التحتية للبث – حسب التكنولوجيا

- البث الرقمي

- البث التناظري

سوق البنية التحتية للبث – حسب التطبيق

- أو تي تي

- أرضي

- القمر الصناعي

- اي بي تي في

- آحرون

سوق البنية التحتية للبث – حسب المنطقة الجغرافية

- أمريكا الشمالية

- نحن

- كندا

- المكسيك

- أوروبا

- ألمانيا

- فرنسا

- إيطاليا

- المملكة المتحدة

- روسيا

- بقية أوروبا

- آسيا والمحيط الهادئ (APAC)

- أستراليا

- الصين

- الهند

- اليابان

- كوريا الجنوبية

- بقية منطقة آسيا والمحيط الهادئ

- الشرق الأوسط وأفريقيا

- المملكة العربية السعودية

- الامارات العربية المتحدة

- جنوب أفريقيا

- باقي منطقة الشرق الأوسط وأفريقيا

- أمريكا الجنوبية (SAM)

- البرازيل

- الأرجنتين

- بقية سام

سوق البنية التحتية للبث – نبذة عن الشركة

- شركة سيسكو سيستمز

- تكنولوجيا البث كلايد

- شركة سي إس لأنظمة الكمبيوتر المحدودة

- شركة داكاست

- شركة EVS لمعدات البث

- وادي العشب

- كالتورا

- نيفيون

- شركة روس فيديو المحدودة

- زيكسي

نافين خبيرٌ متمرسٌ في أبحاث السوق والاستشارات، يتمتع بخبرةٍ تزيد عن 9 سنوات في مشاريع مُخصصة ومُشتركة واستشارية. يشغل حاليًا منصب نائب الرئيس المساعد، وقد نجح في إدارة أصحاب المصلحة عبر سلسلة قيمة المشاريع، وألّف أكثر من 100 تقرير بحثي وأكثر من 30 مهمة استشارية. يمتد نطاق عمله ليشمل مشاريع صناعية وحكومية، مساهمًا بشكل كبير في نجاح العملاء واتخاذ القرارات القائمة على البيانات.

نافين حاصلٌ على شهادة في هندسة الإلكترونيات والاتصالات من جامعة فرجينيا التقنية، كارناتاكا، وشهادة ماجستير في إدارة الأعمال في التسويق والعمليات من جامعة مانيبال. وهو عضوٌ نشطٌ في معهد مهندسي الكهرباء والإلكترونيات (IEEE) لمدة 9 سنوات، حيث شارك في مؤتمراتٍ وندواتٍ تقنية، وتطوّع على مستوى الأقسام والمناطق. قبل منصبه الحالي، عمل مستشارًا استراتيجيًا مساعدًا في IndustryARC، ومستشارًا للخوادم الصناعية في شركة هيوليت باكارد (HP Global).

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

تقارير ذات صلة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق البنية التحتية للبث

احصل على عينة مجانية ل - سوق البنية التحتية للبث