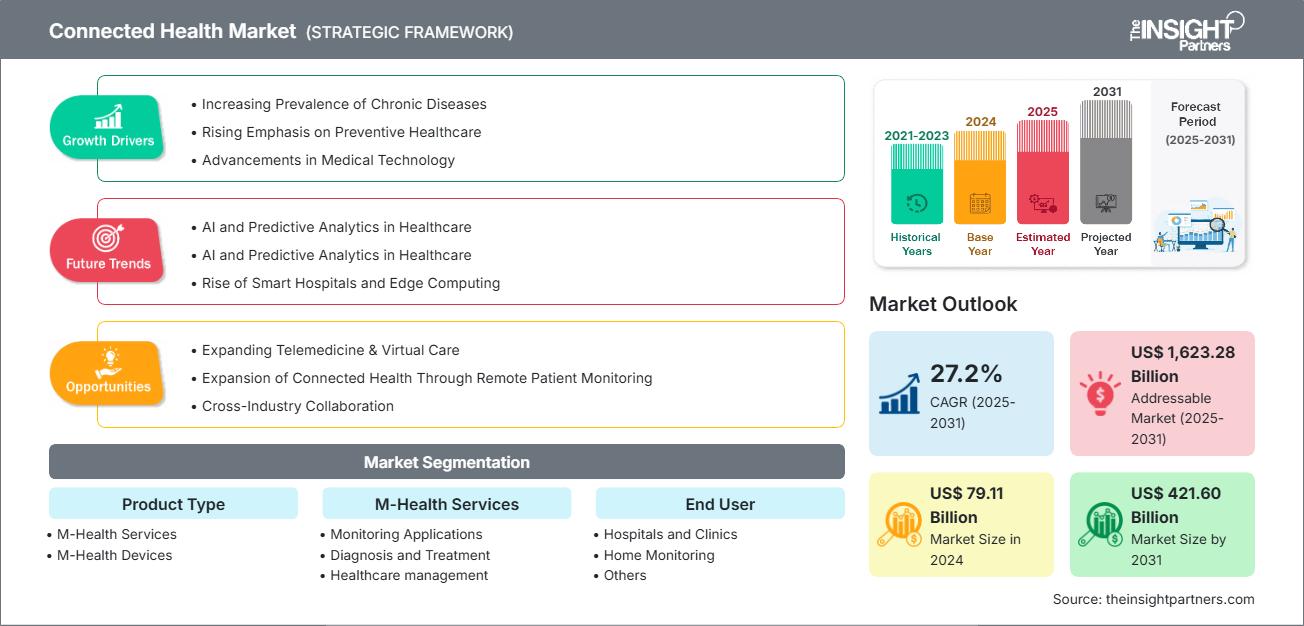

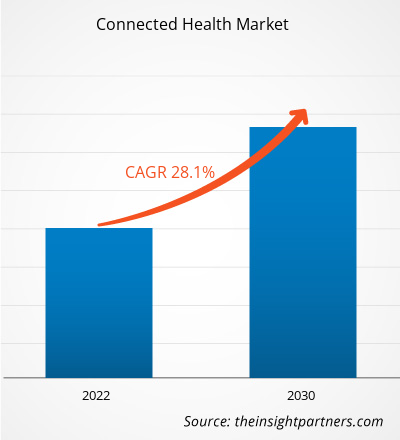

من المتوقع أن يصل حجم سوق الصحة المتصلة إلى 421.5 مليار دولار أمريكي بحلول عام 2031 من 79.1 مليار دولار أمريكي في عام 2024. ومن المتوقع أن يسجل السوق معدل نمو سنوي مركب بنسبة 27.2٪ خلال الفترة 2025-2031.

تحليل سوق الصحة المتصلة

يشهد سوق الرعاية الصحية المتصلة نموًا متسارعًا بفضل عدة عوامل رئيسية، منها تزايد انتشار الأمراض المزمنة، والتركيز المتزايد على الرعاية الصحية الوقائية، والتطورات في التكنولوجيا الطبية. كما أن توسيع الرعاية الصحية عن بُعد، وتوسيع نطاق الرعاية الصحية المتصلة من خلال مراقبة المرضى عن بُعد، والتعاون بين مختلف القطاعات، كلها عوامل تُتيح فرص نمو كبيرة. بالإضافة إلى ذلك، تُنبئ التقنيات القابلة للارتداء، وتكامل الذكاء الاصطناعي، بنمو هائل، وتُحدث تحولًا جذريًا في أنظمة تقديم الرعاية الصحية العالمية.

نظرة عامة على سوق الرعاية الصحية المتصلة

تشير الصحة المتصلة إلى نموذج شامل لتقديم الرعاية الصحية يستخدم التقنيات الرقمية لتوفير رعاية طبية سهلة المنال وفعالة وشخصية. وهي تشمل مجموعة واسعة من الأدوات والمنصات مثل التطبيب عن بُعد (RPM) وتطبيقات الصحة المحمولة والأجهزة القابلة للارتداء والسجلات الصحية الإلكترونية ( EHRs ). تتيح هذه التقنيات التفاعل المستمر بين المرضى ومقدمي الرعاية الصحية، مما يحسن نتائج المرضى ويبسط عمليات الرعاية الصحية. تشمل الفوائد الرئيسية تحسين مشاركة المرضى وتقليل إعادة دخول المستشفى وتحسين إدارة الأمراض المزمنة وتوفير التكاليف. تجد الصحة المتصلة تطبيقات في مراقبة الأمراض المزمنة ورعاية المسنين واللياقة البدنية والعافية والصحة النفسية ورعاية ما بعد الحادة. تشمل الأنواع الرئيسية خدمات التطبيب عن بُعد وتطبيقات الصحة المحمولة وأنظمة RPM ومنصات الصحة الرقمية، حيث يساهم كل منها في نهج سلس واستباقي للرعاية الصحية.

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق الرعاية الصحية المتصلة:

- احصل على أهم اتجاهات السوق الرئيسية من هذا التقرير.ستتضمن هذه العينة المجانية تحليل البيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

محركات وفرص سوق الرعاية الصحية المتصلة

محركات السوق:

تزايد انتشار الأمراض المزمنة:

يُعد الانتشار المتزايد للأمراض المزمنة محركًا محوريًا لنمو سوق الرعاية الصحية المتصلة. تتطلب الحالات المزمنة مثل داء السكري وأمراض القلب والأوعية الدموية واضطرابات الجهاز التنفسي مراقبة وإدارة مستمرة لمنع المضاعفات ودخول المستشفى. توفر حلول الصحة المتصلة، التي تدمج الأدوات الرقمية وأجهزة المراقبة عن بُعد وخدمات الرعاية الصحية عن بُعد ، نهجًا سلسًا لإدارة هذه الأمراض طويلة الأمد من خلال تمكين التتبع في الوقت الفعلي والرعاية الشخصية خارج الإعدادات السريرية التقليدية. في عام 2023، أطلقت وزارة الصحة ورعاية الأسرة مبادرة طموحة تهدف إلى وضع 75 مليون فرد مصاب بارتفاع ضغط الدم أو داء السكري على الرعاية القياسية بحلول عام 2025. تؤكد هذه المبادرة التزام الحكومة بدمج حلول الصحة الرقمية في إدارة الأمراض المزمنة، مما يسهل المراقبة المستمرة والتدخلات في الوقت المناسب. مع تزايد انتشار الأمراض المزمنة عالميًا، سيستمر الطلب على حلول الصحة المتصلة في الارتفاع.التركيز المتزايد على الرعاية الصحية الوقائية:

إن القوة الرئيسية التي تدفع نمو سوق الصحة المتصلة هي التركيز العالمي المتزايد على الرعاية الصحية الوقائية. ومع تحول أنظمة الرعاية الصحية في جميع أنحاء العالم من النماذج التفاعلية إلى النماذج الاستباقية، أصبح تكامل التقنيات المتصلة أمرًا محوريًا في تحديد عوامل الخطر مبكرًا وإدارة الأمراض المزمنة وتعزيز أنماط الحياة الصحية. تعمل الأجهزة القابلة للارتداء وأدوات المراقبة عن بُعد وتطبيقات الصحة المحمولة والمنصات التي تعمل بالذكاء الاصطناعي على تمكين الأفراد من تتبع صحتهم في الوقت الفعلي، مما يعزز ثقافة الوقاية على العلاج. في مايو 2025، كشف مركز الابتكار التابع لمراكز الرعاية الطبية والخدمات الطبية ( CMS ) عن اتجاهه الاستراتيجي لعام 2025، والذي يركز على الوقاية القائمة على الأدلة، ووضع الرعاية الوقائية في قلب النماذج المستقبلية. ويشمل ذلك أدوات لفتح الوصول إلى البيانات، وتمكين الأفراد عبر تطبيقات الهاتف المحمول، ودمج الخدمات الوقائية في تقديم الرعاية. ومع تقدم سكان العالم في السن وانتشار الأمراض المزمنة، ستظل تقنيات الصحة المتصلة التي تدعم التدخل المبكر وإدارة نمط الحياة بالغة الأهمية.

فرص السوق:

توسيع نطاق الطب عن بعد والرعاية الافتراضية:

يشهد سوق الرعاية الصحية المتصلة تحولاً كبيراً، مدفوعاً بدمج التطبيب عن بعد والرعاية الافتراضية في تقديم الرعاية الصحية السائدة. تقدم هذه الابتكارات الرقمية أكثر من مجرد الراحة؛ فهي تعيد تشكيل كيفية الوصول إلى الرعاية وتقديمها وإدارتها. وبينما تكافح أنظمة الرعاية الصحية في جميع أنحاء العالم مع الطلب المتزايد والموارد المحدودة والتركيز المتزايد على الرعاية الشخصية، توفر التطبيب عن بعد والمنصات الافتراضية مساراً استراتيجياً لتوسيع نطاق خدمات الرعاية الصحية بكفاءة مع الحفاظ على جودة النتائج. . وفي إطار بوابة سانجيفاني التابعة للمخطط الوطني للصحة، وسعت حكومة تيلانجانا خدمات التطبيب عن بعد بشكل كبير. ومن عامي 2022-2023 و2023-2024، ارتفع عدد المستخدمين من 5.3 مليون إلى 7.8 مليون استشارة؛ وبحلول مارس 2025، وصلت التوقعات إلى 8.7 مليون. وتغطي الخدمات الرعاية العامة والمتخصصة، وتستفيد منها بشكل خاص السكان النائيين والقبليين من خلال المراكز الفرعية ومراكز الرعاية الصحية الأولية ومراكز الرعاية الصحية الأولية الحضرية. مع تطور أنظمة الرعاية الصحية، لم تعد خدمات الطب عن بعد والرعاية الافتراضية مجرد أدوات، بل أصبحت عوامل تمكينية لبنية تحتية صحية متصلة ومتجاوبة وشاملة، مما يضع الأساس للنمو المستدام في سوق الصحة المتصلة.

تحليل تجزئة تقرير سوق الرعاية الصحية المتصلة

يُصنَّف سوق الرعاية الصحية المتصلة إلى قطاعات مُمَيَّزة لتوفير فهم شامل لهيكله وآفاق نموه واتجاهاته الناشئة. فيما يلي نهج التقسيم القياسي المُستخدم في معظم تقارير القطاع:

حسب نوع المنتج:

خدمات الصحة المتنقلة:

تستفيد خدمات الصحة المتنقلة (الرعاية الصحية المتنقلة) من تكنولوجيا الهاتف المحمول لتقديم حلول الرعاية الصحية، وتحسين تفاعل المرضى، وتبسيط العمليات السريرية. تشمل هذه الخدمات مراقبة المرضى عن بُعد، والاستشارات الطبية عن بُعد، ونشر المعلومات الصحية، والتشخيصات المتنقلة، وتذكير المرضى بالأدوية. وقد حاز هذا القطاع على أكبر حصة سوقية في مجال الرعاية الصحية المتصلة في عام ٢٠٢٤.أجهزة الصحة المتنقلة:

أجهزة الصحة المتنقلة هي أدوات محمولة، قابلة للارتداء، أو متصلة بالهاتف المحمول، مصممة لجمع البيانات الصحية ومراقبتها ونقلها لاسلكيًا. وتشمل هذه الأجهزة أجهزة تتبع اللياقة البدنية، والساعات الذكية المزودة بمستشعرات صحية، وأجهزة مراقبة تخطيط القلب المحمولة، وأجهزة قياس نسبة الجلوكوز في الدم، وأجهزة قياس نسبة الأكسجين في الدم، والأجهزة الطبية المزودة بتقنية البلوتوث. تُمكّن هذه الأجهزة، المدمجة مع تطبيقات الهاتف المحمول أو المنصات السحابية، من تتبع الصحة في الوقت الفعلي ومشاركة البيانات بسلاسة مع أخصائيي الرعاية الصحية.

حسب التطبيق:

تطبيقات المراقبة:

تلعب تطبيقات المراقبة دورًا محوريًا في سوق الرعاية الصحية المتصلة، إذ توفر رؤى آنية حول الحالات الصحية للمرضى. تشمل هذه التطبيقات مراقبة المرضى عن بُعد (RPM)، وأدوات إدارة الأمراض المزمنة، والتقنيات القابلة للارتداء التي تتتبع العلامات الحيوية مثل معدل ضربات القلب، وضغط الدم، ومستويات الجلوكوز، وغيرها. من خلال الاستفادة من أجهزة إنترنت الأشياء، وخوارزميات الذكاء الاصطناعي، والمنصات السحابية، يمكن لمقدمي الرعاية الصحية مراقبة المرضى باستمرار خارج نطاق المرافق السريرية التقليدية. وقد حاز هذا القطاع على أكبر حصة سوقية في مجال الرعاية الصحية المتصلة في عام 2024.

التثقيف والتوعية:

يركز قطاع التثقيف والتوعية في سوق الرعاية الصحية المتصلة على تمكين الأفراد من اتخاذ قرارات صحية مدروسة. تتيح هذه التطبيقات للمستخدمين الوصول إلى معلومات صحية دقيقة ومخصصة من خلال تطبيقات الهاتف المحمول، وبوابات الويب، والمنصات التفاعلية.العافية والوقاية:

يُعدّ قطاع العافية والوقاية مجالاً سريع النمو في سوق الرعاية الصحية المتصلة، ويهدف إلى تشجيع أنماط حياة صحية والحد من الإصابة بالأمراض المزمنة. يشمل هذا القطاع أجهزة تتبع اللياقة البدنية، وتطبيقات الحمية الغذائية، ومنصات الصحة النفسية، وأجهزة مراقبة النوم، وأدوات الفحص الوقائي.إدارة الرعاية الصحية:

تُعد تطبيقات إدارة الرعاية الصحية أدوات أساسية في منظومة الرعاية الصحية المتصلة، إذ تُسهّل تنسيق الرعاية بسلاسة، وتحسين سير العمل السريري، وتحقيق الكفاءة الإدارية. تدعم هذه التطبيقات السجلات الصحية الإلكترونية (EHRs)، وجدولة مواعيد المرضى، والفوترة، وإدارة الوصفات الطبية، والاستشارات الطبية عن بُعد.آحرون:

يشمل القطاع الآخر في سوق الرعاية الصحية المتصلة مجموعة متنوعة من التطبيقات الناشئة والمتخصصة التي لا تندرج مباشرةً ضمن الفئات الرئيسية. قد تشمل هذه التطبيقات مجالات مثل العلاجات الرقمية، ومنصات البحث السريري، ومحاكاة التدريب الطبي، وأدوات الامتثال للأدوية.

بواسطة المستخدم النهائي:

- المستشفيات والعيادات

- مراقبة المنزل

- آحرون

حسب الجغرافيا:

- أمريكا الشمالية

- أوروبا

- آسيا والمحيط الهادئ

- أمريكا الجنوبية والوسطى

- الشرق الأوسط وأفريقيا

من المتوقع أن يشهد سوق الرعاية الصحية المتصلة في منطقة آسيا والمحيط الهادئ أسرع نمو. ويساهم تزايد الطلب على الرعاية الصحية، واعتماد الهواتف المحمولة، والمبادرات الحكومية، وعبء الأمراض المزمنة، والابتكار التكنولوجي في نمو سريع لقطاع الرعاية الصحية المتصلة في منطقة آسيا والمحيط الهادئ.

رؤى إقليمية حول سوق الرعاية الصحية المتصلة

قام محللو شركة "ذا إنسايت بارتنرز" بشرح شامل للاتجاهات والعوامل الإقليمية المؤثرة في سوق الرعاية الصحية المتصلة خلال فترة التوقعات. ويناقش هذا القسم أيضًا قطاعات سوق الرعاية الصحية المتصلة ونطاقها الجغرافي في أمريكا الشمالية، وأوروبا، وآسيا والمحيط الهادئ، والشرق الأوسط وأفريقيا، وأمريكا الجنوبية والوسطى.

نطاق تقرير سوق الصحة المتصلة

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2024 | 79.11 مليار دولار أمريكي |

| حجم السوق بحلول عام 2031 | 421.60 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2025 - 2031) | 27.2% |

| البيانات التاريخية | 2021-2023 |

| فترة التنبؤ | 2025-2031 |

| القطاعات المغطاة | حسب نوع المنتج

|

| المناطق والبلدان المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في سوق الرعاية الصحية المتصلة: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق الرعاية الصحية المتصلة نموًا سريعًا، مدفوعًا بتزايد طلب المستخدمين النهائيين نتيجةً لعوامل مثل تطور تفضيلات المستهلكين، والتقدم التكنولوجي، وزيادة الوعي بفوائد المنتج. ومع تزايد الطلب، تعمل الشركات على توسيع عروضها، والابتكار لتلبية احتياجات المستهلكين، والاستفادة من الاتجاهات الناشئة، مما يعزز نمو السوق.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق الصحة المتصلة

تحليل حصة سوق الرعاية الصحية المتصلة حسب المنطقة الجغرافية

من المتوقع أن تشهد منطقة آسيا والمحيط الهادئ أسرع نمو في السنوات القليلة المقبلة. كما تزخر الأسواق الناشئة في أمريكا الجنوبية والوسطى والشرق الأوسط وأفريقيا بالعديد من الفرص غير المستغلة لتوسع مقدمي الرعاية الصحية المتصلين.

ينمو سوق الرعاية الصحية المتصلة بشكل متفاوت في كل منطقة، وذلك بفضل التبني الرقمي، وشيخوخة السكان، والأمراض المزمنة، والطلب على الرعاية الصحية عن بُعد، وسياسات الرعاية الصحية الداعمة. فيما يلي ملخص لحصة السوق واتجاهاتها حسب المنطقة:

1. أمريكا الشمالية

الحصة السوقية:

تمتلك حصة كبيرة من السوق العالميةالعوامل الرئيسية:

- البنية التحتية المتقدمة للرعاية الصحية

- اعتماد كبير على الرعاية الصحية عن بعد والتكنولوجيا القابلة للارتداء

- دعم حكومي وتأميني قوي للصحة الرقمية.

الاتجاهات:

التحول نحو الرعاية المبنية على القيمة وأنظمة المراقبة عن بعد المتكاملة.

2. أوروبا

الحصة السوقية:

حصة كبيرة بسبب اللوائح الصارمة المبكرة للاتحاد الأوروبيالعوامل الرئيسية:

- مبادرات الصحة الرقمية الممولة من الحكومة

- شيخوخة السكان وانتشار الأمراض المزمنة

- التركيز على قابلية التشغيل المتبادل للبيانات وخصوصية المريض.

الاتجاهات:

توسيع خدمات الطب عن بعد عبر الحدود والتعاون في مجال الصحة الرقمية.

3. آسيا والمحيط الهادئ

الحصة السوقية:

المنطقة الأسرع نموًا مع حصة سوقية مهيمنةالعوامل الرئيسية:

- ارتفاع معدل انتشار الهاتف المحمول والإنترنت

- الطلب المتزايد على الرعاية الصحية في الدول ذات الكثافة السكانية العالية (الصين والهند)

- الاستثمارات الحكومية في البنية التحتية للرعاية الصحية الرقمية.

الاتجاهات:

ارتفاع في عدد الشركات الناشئة في مجال التكنولوجيا الصحية ومنصات الرعاية الصحية التي تعتمد على الذكاء الاصطناعي.

4. الشرق الأوسط وأفريقيا

الحصة السوقية:

على الرغم من صغر حجمها، إلا أنها تنمو بسرعةالعوامل الرئيسية:

- ارتفاع الاستثمار في البنية التحتية للرعاية الصحية الذكية

- التحضر وزيادة المعرفة الرقمية

- مبادرات الوصول إلى الرعاية الصحية في المناطق المحرومة.

الاتجاهات:

اعتماد حلول الرعاية الصحية المتنقلة للوصول إلى السكان النائيين.

5. أمريكا الجنوبية والوسطى

الحصة السوقية:

سوق متنامية مع تقدم مطردالعوامل الرئيسية:

- توسيع خدمات الرعاية الصحية عن بعد بعد جائحة كوفيد

- دعم الحكومة لتوفير الرعاية الصحية في المناطق الريفية

- تزايد استخدام الهواتف الذكية والأجهزة القابلة للارتداء.

الاتجاهات:

النمو في منصات الرعاية الصحية التي تركز على الهاتف المحمول لإدارة الرعاية المزمنة والعافية.

كثافة اللاعبين في سوق الرعاية الصحية المتصلة: فهم تأثيرها على ديناميكيات الأعمال

كثافة السوق العالية والمنافسة

تشتد المنافسة بفضل وجود شركات عالمية كبرى مثل كونينكليكي فيليبس، وآبل، وأومرون، وآي بي إم، وآي بي إم، ومختبرات أبوت. كما أن وجود مزودين إقليميين ومتخصصين مثل ميدترونيك بي إل سي (أوروبا)، وجنرال إلكتريك هيلث كير تكنولوجيز (الولايات المتحدة)، وفيتبيت إل إل سي (الولايات المتحدة)، وبوسطن ساينتيفيك (الولايات المتحدة)، وسامسونج إلكترونيكس (كوريا الجنوبية) يُسهم في تنويع المشهد التنافسي.

هذا المستوى العالي من المنافسة يحث الشركات على التميز من خلال تقديم:

- حلول صحية مخصصة باستخدام الذكاء الاصطناعي والبيانات الضخمة

- منصات قابلة للتشغيل المتبادل تتكامل بسلاسة مع أنظمة الرعاية الصحية الحالية

- تعزيز أمن البيانات والامتثال للخصوصية (على سبيل المثال، HIPAA، وGDPR)

- تجارب مستخدم مبتكرة من خلال تطبيقات الهاتف المحمول والأجهزة القابلة للارتداء

- أنظمة الرعاية الشاملة، من المراقبة عن بعد إلى الاستشارات الافتراضية.

الفرص والتحركات الاستراتيجية

- تكامل الذكاء الاصطناعي وتحليلات البيانات: الاستفادة من الذكاء الاصطناعي للحصول على رؤى صحية تنبؤية وخطط رعاية مخصصة.

- إدارة الأمراض المزمنة: ارتفاع معدل انتشار مرض السكري وأمراض القلب وأمراض الجهاز التنفسي التي تتطلب مراقبة مستمرة.

الشركات الرئيسية العاملة في سوق الصحة المتصلة هي:

- Koninklijke Philips (Europe)

- شركة أبل (الولايات المتحدة)

- شركة أومرون (اليابان)

- شركة آي بي إم للآلات التجارية (الولايات المتحدة)

- مختبرات أبوت (الولايات المتحدة)

- شركة ميدترونيك بي إل سي (أوروبا)

- شركة GE HealthCare Technologies Inc (الولايات المتحدة)

- شركة فيتبيت ذ.م.م (الولايات المتحدة)

- شركة بوسطن العلمية (الولايات المتحدة)

- شركة سامسونج للإلكترونيات المحدودة (كوريا الجنوبية)

إخلاء المسؤولية: الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

الشركات الأخرى التي تم تحليلها أثناء البحث:

- صحة بابل

- أمويل

- شركة سيرنر

- ألسكريبتس

- بروتيوس للصحة الرقمية

- ويذينغز

- ريس ميد

- جارمين للرعاية الصحية

- Livongo Health (الآن جزء من Teladoc)

- كوالكوم لايف

- تقنيات اي ريثم

- القياس الحيوي عن بعد (الآن جزء من شركة فيليبس)

- محفز الصحة

- كوالكوم تكنولوجيز

- حلول هانيويل للعناية بالحياة

- سيربو هيلث

- دوكبلانر

- هوما (ميدوباد سابقًا)

- كايزر بيرماننتي

- ريس ميد

- جارمين للرعاية الصحية

- ليفونغو

أخبار سوق الصحة المتصلة والتطورات الأخيرة

أعلنت شركة فيليبس عن شراكة موسعة مع شركة ميدترونيك، يوليو 2025:

أعلنت شركة فيليبس عن شراكة موسعة مع شركة ميدترونيك لتطوير تقنيات مراقبة المرضى. وتستند هذه الاتفاقية متعددة السنوات، التي تُبنى على تعاون بدأ عام ١٩٩٢، إلى نظام مراقبة المرضى من فيليبس الذي يتضمن نظام قياس التأكسج النبضي Nellcor من ميدترونيك، ونظام مراقبة الدماغ BIS، ونظام تخطيط ثاني أكسيد الكربون Microstream. ويهدف هذا النظام إلى توفير حل مراقبة شامل ومعتمد وآمن إلكترونيًا، يُبسط عملية الشراء ويضمن جودة عالية للأطباء، مما يُمكّنهم من التركيز بشكل أكبر على رعاية المرضى.أبرمت شركة OMRON Healthcare شراكة مع شركة Tricog Health، في أبريل 2025:

أعلنت شركة أومرون للرعاية الصحية، الرائدة في سوق حلول مراقبة الصحة المنزلية، عن المرحلة التالية من شراكتها الاستراتيجية مع شركة تريكوغ هيلث، وهي شركة رائدة في مجال التكنولوجيا الطبية متخصصة في رعاية القلب والأوعية الدموية. واستنادًا إلى تعاونهما الذي بدأ عام ٢٠٢٣ لدخول قطاع مراقبة وإدارة القلب عن بُعد، تُطلق الشركتان الآن منصة "كيبو هيلث"، وهي منصة رعاية قلبية متصلة تعمل بالذكاء الاصطناعي. صُمم هذا الحل لتحسين إدارة قصور القلب من خلال تمكين المراقبة المستمرة عن بُعد وتقديم رعاية شخصية قائمة على البيانات. تعكس هذه المبادرة التزام كلتا المؤسستين بتطوير الرعاية الصحية الرقمية وتحسين نتائج المرضى من خلال حلول مبتكرة قائمة على التكنولوجيا.

تغطية تقرير سوق الرعاية الصحية المتصلة والنتائج المتوقعة

يقدم تقرير "حجم سوق الرعاية الصحية المتصلة والتوقعات (2021-2031)" تحليلاً مفصلاً للسوق يغطي المجالات التالية:

- حجم سوق الصحة المتصلة وتوقعاته على المستويات العالمية والإقليمية والوطنية لجميع قطاعات السوق الرئيسية التي يغطيها النطاق

- اتجاهات سوق الرعاية الصحية المتصلة، بالإضافة إلى ديناميكيات السوق مثل المحركات والقيود والفرص الرئيسية

- تحليل مفصل لـ PEST و SWOT

- تحليل سوق الصحة المتصلة الذي يغطي اتجاهات السوق الرئيسية والإطار العالمي والإقليمي والجهات الفاعلة الرئيسية واللوائح والتطورات الأخيرة في السوق

- تحليل المشهد الصناعي والمنافسة الذي يغطي تركيز السوق، وتحليل خريطة الحرارة، واللاعبين البارزين، والتطورات الأخيرة لسوق الصحة المتصلة

- ملفات تعريف الشركة التفصيلية

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

The Monitoring Applications segment is experiencing significant growth due to it plays a pivotal role in the connected health market, offering real-time insights into patients' health conditions. These applications include remote patient monitoring (RPM), chronic disease management tools, and wearable technologies that track vital signs such as heart rate, blood pressure, glucose levels, and more. By leveraging IoT devices, AI algorithms, and cloud-based platforms, healthcare providers can continuously monitor patients outside traditional clinical settings.

Top trends include:1. Integration with AI and Machine Learning2. Expansion of Wearables & IoT Devices3. Interoperability & Integrated Health Ecosystems4. Rise of Remote Patient Monitoring5. Value-Based & Preventive Care Models

While Asia-Pacific and North America currently dominate, Europe, Middle East & Africa, and parts of the South & Central America are expected to witness rapid growth owing to digital adoption, aging populations, chronic diseases, telehealth demand, and supportive healthcare policies.

As of 2024, the global connected health market is valued at approximately USD 79.10 billion. It is projected to reach USD 421.5 billion by 2031, growing at a compound annual growth rate (CAGR) of 27.2% during the forecast period from 2025 to 2031.

The market is primarily driven by:1. Increasing Prevalence of Chronic Diseases: The increasing prevalence of chronic diseases stands as a pivotal driver for the growth of the connected health market. Chronic conditions such as diabetes, cardiovascular diseases, and respiratory disorders require continuous monitoring and management to prevent complications and hospitalizations. Connected Health solutions, which integrate digital tools, remote monitoring devices, and telehealth services, offer a seamless approach to managing these long-term illnesses by enabling real-time tracking and personalized care outside traditional clinical settings.2. Rising Emphasis on Preventive Healthcare: A key force propelling the growth of the connected health market is the rising global emphasis on preventive healthcare. As healthcare systems worldwide shift from reactive to proactive models, the integration of connected technologies has become central in identifying risk factors early, managing chronic conditions, and promoting healthier lifestyles.

AI and ML are revolutionizing connected health by:1. Predictive Analytics for Early Diagnosis: AI and ML algorithms analyze patient data from EHRs, wearables, and medical devices to detect patterns and predict potential health issues before symptoms appear. This enables proactive care, reduces hospitalizations, and improves outcomes—especially in chronic diseases like heart failure and diabetes.2. Personalized and Precision Medicine: Machine learning models use individual patient data (including genetics, lifestyle, and real-time vitals) to deliver personalized treatment plans. This improves treatment effectiveness, reduces adverse drug reactions, and supports more targeted interventions.

Major players include Koninklijke Philips NV, Apple Inc., OMRON Corp., International Business Machines Corp., Abbott Laboratories, and among others.

Challenges include:Data Privacy & Security Risks: Handling vast amounts of sensitive patient data increases vulnerability to breaches and cyberattacks. Ensuring compliance with HIPAA, GDPR, and other regional regulations is complex and costly.

The List of Companies - Connected Health Market

- Koninklijke Philips (Europe)

- Apple Inc. (US)

- OMRON Corp. (Japan)

- International Business Machines Corp.(US)

- Abbott Laboratories (US)

- Medtronic Plc (Europe)

- GE HealthCare Technologies Inc (US)

- Fitbit LLC (US)

- Boston Scientific Corp (US)

- Samsung Electronics Co Ltd (South Korea)

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير