Marktanteil, Größe und Nachfrage von 3D-gedruckten Medizinprodukten bis 2034

Marktgröße und Prognose für medizinische 3D-Druckgeräte (2021–2034), globaler und regionaler Marktanteil, Trend- und Wachstumspotenzialanalyse. Berichtsabdeckung: Nach Komponenten [Software und Dienstleistungen, Ausrüstung (3D-Drucker und 3D-Biodrucker) und Materialien (Kunststoffe, Metalle und Metalllegierungen, Biodruckmaterialien, Wachsmaterialien und Sonstige)], Technologie [Laserstrahlschmelzen (Direktes Metall-Lasersintern, Selektives Lasersintern, Selektives Laserschmelzen und Laserschweißen), Photopolymerisation (Stereolithographie und Sonstige), Tropfenauftrags-/Extrusionstechnologien (Schmelzverfahren, Mehrphasenverfestigung und Niedertemperatur-Abscheidungsfertigung) und Elektronenstrahlschmelzen], Anwendung [Maßgefertigte Prothesen und Implantate (kraniomaxillofaziale Implantate, maßgefertigte Zahnprothesen und -implantate sowie maßgefertigte orthopädische Implantate), chirurgische Schablonen (zahnorthopädische, kraniofaziale und Wirbelsäulenschablonen)]. Produkte für das Tissue Engineering (Knochen- und Knorpelgerüste sowie Gerüste für Bänder und Sehnen), chirurgische Instrumente (chirurgische Befestigungselemente, Skalpelle und Retraktoren), Hörgeräte, tragbare medizinische Geräte sowie Standardprothesen und -implantate] und Endnutzer (Krankenhäuser und chirurgische Zentren, zahnärztliche und orthopädische Zentren, Medizintechnikunternehmen, Pharma- und Biotechnologieunternehmen, akademische und Forschungsinstitute und andere) sowie Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPMD00002652

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : April 09, 2026

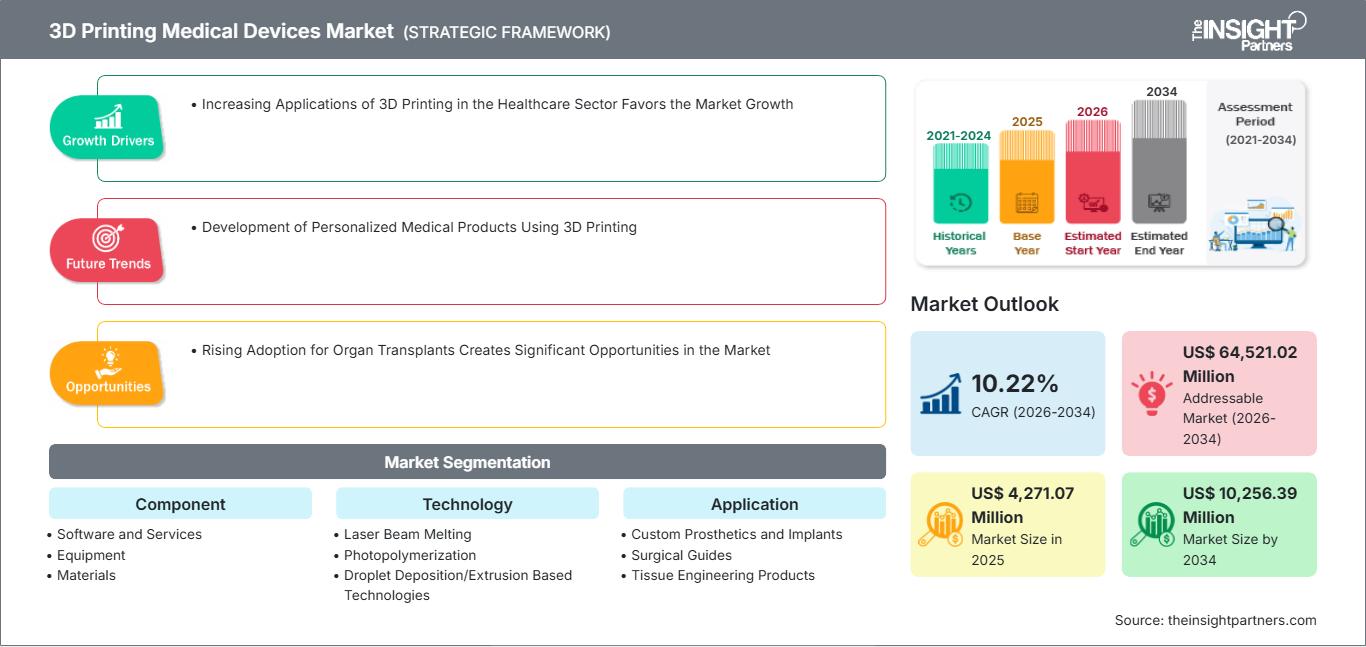

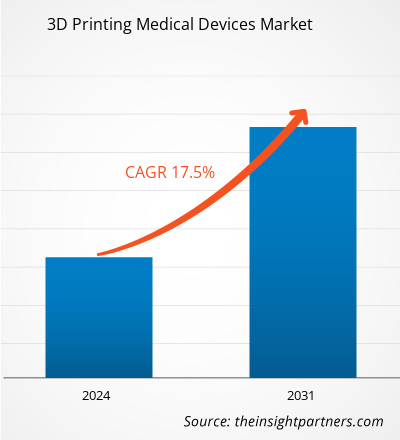

Der Markt für medizinische Geräte, die mittels 3D-Druck hergestellt werden, wird voraussichtlich bis 2034 ein Volumen von 10.256,39 Millionen US-Dollar erreichen, gegenüber 4.271,07 Millionen US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Prognosezeitraum 2026–2034 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 10,22 % verzeichnen wird.

Marktanalyse für medizinische 3D-Druckgeräte

Der Markt für im 3D-Druckverfahren hergestellte Medizinprodukte ist etabliert. Der zunehmende Einsatz von 3D-Druck im Gesundheitswesen treibt die Akzeptanz an und trägt zum Gesamtwachstum des Marktes bei. Die steigende Anzahl von Organtransplantationen hat die Nachfrage nach 3D-gedruckten Medizinprodukten erhöht. Dieser positive Faktor wirkt sich auf das Wachstum des Gesamtmarktes aus. Schon bald wird die Herstellung individualisierter Medizinprodukte mittels 3D-Druck ein vielversprechendes Marktpotenzial bieten.

Marktübersicht für medizinische 3D-Druckgeräte

In den letzten Jahrzehnten hat die Verwendung von 3D-Drucktechnologie bei implantierbaren Medizinprodukten aufgrund ihrer Präzision und optimalen Materialausnutzung deutlich zugenommen. Besonders die Traumatologie, Orthopädie und Zahnmedizin profitieren von diesen Instrumenten. Unabhängig von ihrer Komplexität lassen sich implantierbare Medizinprodukte jeder Form mithilfe der 3D-Drucktechnologie problemlos herstellen. Sie kann die Herausforderungen bei der Entwicklung und Produktion komplexer Implantate lösen. Auch personalisierte und maßgefertigte Implantate können mit dem 3D-Druckverfahren hergestellt werden.

Karies ist weltweit die zweithäufigste Zahnerkrankung. Kieferorthopädische Probleme treten, abgesehen von geringfügigen geschlechtsspezifischen Unterschieden, bei beiden Geschlechtern häufig auf. Das Potenzial für individualisierte Produkte treibt die Entwicklung des 3D-Drucks für medizinische und zahnmedizinische Anwendungen voran. Dies führt zu Kosteneinsparungen bei Kleinserien, einer einfacheren Weitergabe und Verarbeitung von Patientendaten sowie zu Verbesserungen in der Ausbildung. Bisher gibt es nur wenige Veröffentlichungen zu Anwendungen in der Parodontologie und Endodontie. Die 3D-Drucktechnik konzentriert sich primär auf Anwendungen in der Oralchirurgie und Prothetik, gefolgt von der Kieferorthopädie. Dank des klinischen Einsatzes der 3D-Drucktechnologie können Chirurgen Operationen an einem realistischen anatomischen Modell mit fortschrittlicher Bildverarbeitung durchführen.

Highlights der Marktforschung

- Der globale Markt für medizinische 3D-Druckgeräte wurde im Jahr 2025 auf 4.271,07 Millionen US-Dollar geschätzt.

- Es wird erwartet, dass das jährliche Marktvolumen bis 2034 10.256,39 Millionen US-Dollar erreichen wird.

- Der gesamte adressierbare Markt (TAM) wird im Zeitraum 2026–2034 voraussichtlich rund 64.521,02 Millionen US-Dollar erreichen.

- Es wird erwartet, dass der Markt im Prognosezeitraum eine durchschnittliche jährliche Wachstumsrate (CAGR) von 10,22 % verzeichnen wird.

- Die Vereinigten Staaten stellen einen Schlüsselmarkt dar, der durch die zunehmenden Anwendungen des 3D-Drucks im Gesundheitswesen, die das Marktwachstum begünstigen, sowie durch die sich entwickelnde Branchendynamik unterstützt wird.

- Die Marktanalyse umfasst Nordamerika, Europa, den asiatisch-pazifischen Raum, Süd- und Mittelamerika, den Nahen Osten und Afrika, wobei das Wachstum über den gesamten Prognosezeitraum bewertet wird.

- Marktchancen wie die zunehmende Akzeptanz von Organtransplantationen schaffen erhebliche Marktmöglichkeiten und werden voraussichtlich die Marktdynamik und den adressierbaren Markt beeinflussen.

- Der Bericht stellt Branchenteilnehmer wie EOS GmbH Electro Optical Systems, Renishaw PLC, Stratasys Ltd., 3D Systems, Inc., EnvisionTech, Inc., Concept Laser GmbH (General Electric), 3T RPD Ltd., Proadways Group, SLM Solution Group AG und CELLINK vor und analysiert Wettbewerbsstrategien und Innovationsentwicklungen.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für medizinische 3D-Druckgeräte: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen für medizinische 3D-Druckgeräte

Die zunehmenden Anwendungen des 3D-Drucks im Gesundheitswesen begünstigen das Marktwachstum.

Eine breite Palette medizinischer Geräte mit komplexer Geometrie oder patientenspezifischen Merkmalen wird mithilfe von 3D-Druckern hergestellt. Ausgehend von einem Standarddesign werden zunächst einige Geräte gedruckt, anschließend werden zahlreiche Repliken desselben Geräts erstellt. Die patientenspezifischen Bilddaten dienen der Entwicklung weiterer, auch patientenangepasster oder patientenspezifischer Geräte genannter Geräte. Der Verwendungszweck der gedruckten Produkte und die Benutzerfreundlichkeit des Druckers sind zwei wichtige Kriterien bei der Wahl der 3D-Drucktechnologie. Die gängigste Technologie für den 3D-Druck medizinischer Geräte ist das Pulverbett-Schmelzverfahren. Dieses Verfahren eignet sich für verschiedene Materialien, darunter Nylon und Titan, die in der Medizintechnik verwendet werden. Mithilfe von CT- und MRT-Scans ermöglicht der 3D-Druck die kostengünstige und einfache Erstellung taktiler Referenzmodelle, die individuell auf jeden Patienten zugeschnitten sind. Durch die Darstellung einer anderen Perspektive unterstützen diese Modelle Ärzte bei der besseren Operationsvorbereitung und reduzieren so den Zeit- und Kostenaufwand für den eigentlichen Eingriff im Operationssaal erheblich. Patienten profitieren davon durch höhere Zufriedenheit, weniger Angst und eine schnellere Genesung.

Darüber hinaus ermöglicht die Einführung neuartiger biokompatibler Materialien für den 3D-Druck in der Medizin die Entwicklung neuer chirurgischer Instrumente und Methoden, die allesamt darauf abzielen, das Operationserlebnis für Patienten zu verbessern. Sterilisierbare Fixierungsschalen, Konturierungsschablonen und Implantat-Größenbestimmungsmodelle gehören zu den Instrumenten, die mittels 3D-Druck hergestellt werden können. Diese können zur Größenbestimmung von Implantaten im Operationssaal vor dem ersten Schnitt verwendet werden, was Chirurgen Zeit spart und die Präzision bei komplexen Eingriffen erhöht.

Die zunehmende Akzeptanz von Organtransplantationen schafft bedeutende Chancen auf dem Markt.

Der Einsatz von 3D-Drucktechnologie in der Organtransplantation hat sich zunehmend als vorteilhaft erwiesen. 3D-Biodrucker wurden mehrfach weiterentwickelt und verbessert, um den Qualitätsanforderungen und Erwartungen gerecht zu werden. Dadurch schreitet die Entwicklung von 3D-Druckern stetig voran und ihr Anwendungsspektrum erweitert sich. Durch die Beschleunigung der Produktion medizinischer Geräte tragen 3D-Drucker dazu bei, Leben zu retten. Sie helfen, den Mangel an Spenderorganen und die Abstoßungsreaktionen der Empfänger zu überwinden. Zudem ermöglichen sie es Medizinern, eine große Anzahl von Patienten schnell zu behandeln. Ohne leicht zugängliche Umgebungen, die Blut, Sauerstoff und lebenswichtige Nährstoffe liefern, können Organe nicht überleben. Mithilfe der 3D-Drucktechnologie lassen sich sichere Umgebungen für transplantierte Organe schaffen. Da die Organe biogedruckt und nicht kastriert werden, haben 3D-Drucker einen bedeutenden Einfluss auf den Organersatz in der Medizin. Dies verkürzt die Suche nach geeigneten Spendern. Daher werden erhebliche positive Auswirkungen auf die Gesellschaft erwartet, insbesondere im Hinblick auf die Lebensqualität. Zu den vielversprechenden Einsatzmöglichkeiten des 3D-Biodrucks gehört die Herstellung künstlicher Gewebe und Organe, was das Gebiet der regenerativen Medizin grundlegend verändern könnte.

Marktbericht für medizinische 3D-Druckgeräte: Segmentierungsanalyse

Die wichtigsten Segmente, die zur Erstellung der Marktanalyse für medizinische 3D-Druckgeräte beigetragen haben, sind Komponenten, Technologie, Anwendung und Endnutzer.

- Basierend auf den Komponenten ist der Markt für medizinische 3D-Druckgeräte in Software und Dienstleistungen, Ausrüstung und Materialien unterteilt. Das Segment Ausrüstung hatte 2023 den größten Marktanteil.

- Technologisch lässt sich der Markt in Laserstrahlschmelzen, Photopolymerisation, Tropfenauftrags-/Extrusionsverfahren und Elektronenstrahlschmelzen unterteilen. Das Segment der Photopolymerisation hielt 2023 den größten Marktanteil.

- Nach Anwendungsgebiet ist der Markt in individuelle Prothesen und Implantate, Produkte für das Tissue Engineering, chirurgische Schablonen, chirurgische Instrumente, tragbare medizinische Geräte, Hörgeräte, Standardprothesen und -implantate sowie Sonstiges unterteilt. Das Segment der individuellen Prothesen und Implantate hatte 2023 den größten Marktanteil.

- Laut Endnutzer ist der Markt in Krankenhäuser und chirurgische Zentren, zahnärztliche und orthopädische Zentren, Medizintechnikunternehmen, akademische und Forschungsinstitute, Pharma- und Biotechnologieunternehmen sowie Sonstige unterteilt. Das Segment der Krankenhäuser und chirurgischen Zentren hielt 2023 den größten Marktanteil.

Marktanteilsanalyse für medizinische 3D-Druckgeräte nach Regionen

Der geografische Umfang des Marktberichts für 3D-gedruckte medizinische Geräte ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten & Afrika sowie Süd- & Mittelamerika.

Nordamerika besteht aus drei Ländern: den USA, Kanada und Mexiko. Die USA sind der größte Markt für medizinische 3D-Druckprodukte, gefolgt von Kanada und Mexiko. Allein in den Vereinigten Staaten werden jährlich fast 200.000 Amputationen durchgeführt. Prothesenersatz oder -anpassungen können kostspielig und zeitaufwendig sein und zwischen 5.000 und 50.000 US-Dollar kosten. Da Prothesen so individuell angefertigt werden, muss jede einzelne an die Bedürfnisse des Trägers angepasst werden. Heutzutage wird die additive Fertigung (AM) häufig eingesetzt, um Prothesenkomponenten herzustellen, die exakt auf die Anatomie jedes Patienten zugeschnitten sind und so eine perfekte Passform gewährleisten. AM kommt überall dort zum Einsatz, wo Prothesen mit Patienten in Berührung kommen, da sie die Herstellung komplexer Geometrien aus verschiedenen Materialien ermöglicht. Die AM-Technologie hat eine breite Produktpalette hervorgebracht, von komfortablen Beinprothesenverbindungen bis hin zu komplexen, hochgradig individualisierten Gesichtsprothesen für Krebspatienten.

Organovo, ein US-amerikanisches medizinisches Labor- und Forschungsunternehmen, experimentiert mit dem 3D-Druck von Darm- und Lebergewebe, um die In-vitro-Untersuchung von Organen und die Entwicklung von Medikamenten für bestimmte Krankheiten zu unterstützen. Das Unternehmen veröffentlichte im Mai 2018 präklinische Daten zur Funktionalität des Lebergewebes in einem Programm zur Behandlung von Tyrosinämie Typ 1. Tyrosin ist eine Aminosäure, die der Körper aufgrund eines Enzymmangels nicht verstoffwechseln kann.

Marktbericht über medizinische Geräte mit 3D-Druck: Umfang

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 4.271,07 Millionen US-Dollar |

| Marktgröße bis 2034 | 10.256,39 Millionen US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 10,22 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nach Komponente

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte bei 3D-gedruckten Medizinprodukten: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für medizinische 3D-Druckgeräte wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile der Produkte. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen für die Bedürfnisse der Verbraucher und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

Marktneuigkeiten und aktuelle Entwicklungen im Bereich medizinischer 3D-Druckgeräte

Der Markt für medizinische 3D-Druckgeräte wird anhand qualitativer und quantitativer Daten aus Primär- und Sekundärforschung analysiert. Zu den relevanten Quellen zählen wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken. Einige Entwicklungen auf diesem Markt sind im Folgenden aufgeführt:

- Align Technology, Inc., ein weltweit führendes Medizintechnikunternehmen, das das Invisalign-System mit transparenten Zahnschienen, iTero-Intraoralscanner und die exocad CAD/CAM-Software für digitale Kieferorthopädie und restaurative Zahnheilkunde entwickelt, herstellt und vertreibt, gab die Übernahme der Cubicure GmbH bekannt, einem Pionier im Bereich direkter 3D-Drucklösungen für die additive Fertigung von Polymeren. Cubicure entwickelt, produziert und vertreibt innovative Materialien, Anlagen und Verfahren für neuartige 3D-Drucklösungen. (Quelle: Align Technology, Inc., Pressemitteilung, Januar 2024)

Marktbericht zu 3D-gedruckten Medizinprodukten: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für medizinische 3D-Druckgeräte (2021–2031)“ bietet eine detaillierte Analyse des Marktes und deckt folgende Bereiche ab:

- Marktgröße und Prognose für medizinische 3D-Druckgeräte auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt werden

- Markttrends für medizinische 3D-Druckgeräte sowie Marktdynamiken wie Treiber, Hemmnisse und wichtige Chancen

- Detaillierte PEST-/Porter-Fünf-Kräfte- und SWOT-Analyse

- Marktanalyse für medizinische 3D-Druckgeräte mit Fokus auf wichtige Markttrends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Bestimmungen und aktuelle Marktentwicklungen.

- Branchenlandschafts- und Wettbewerbsanalyse mit Fokus auf Marktkonzentration, Heatmap-Analyse, führende Akteure und aktuelle Entwicklungen im Markt für medizinische 3D-Druckgeräte

- Detaillierte Unternehmensprofile

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends