Marktanteil, Wachstum und Nachfrage im Kfz-Reifen-Ersatzteilmarkt bis 2034

Marktgröße und Prognose für den Kfz-Reifen-Ersatzteilmarkt (2021–2034), globaler und regionaler Marktanteil, Trends und Wachstumspotenzialanalyse. Berichtsabdeckung: Nach Reifentyp (Radialreifen und Diagonalreifen), Vertriebskanal (Erstausrüster und unabhängiger Händler), Felgengröße (13–15, 16–18, 19–21 und mehr als 21 Zoll), Fahrzeugtyp (Pkw, leichte Nutzfahrzeuge und schwere Nutzfahrzeuge) und Region

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00028388

- Kategorie : Automobil- und Transportwesen

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : April 09, 2026

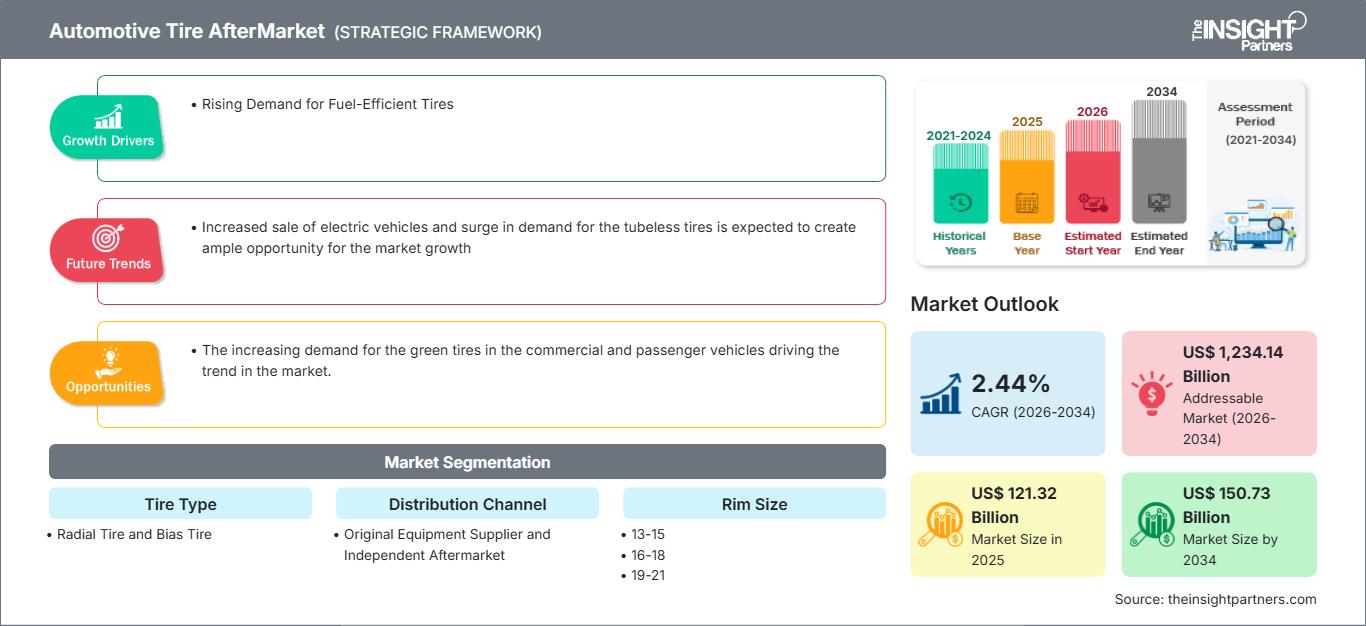

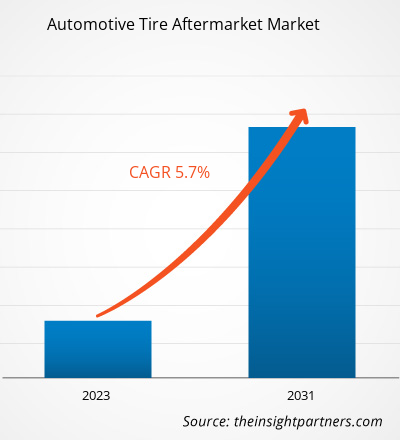

Der Markt für Kfz-Reifen-Ersatzteile wird bis 2034 voraussichtlich ein Volumen von 150,73 Milliarden US-Dollar erreichen, gegenüber 121,32 Milliarden US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Prognosezeitraum 2026–2034 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 2,44 % verzeichnen wird.

Marktanalyse für den Kfz-Reifen-Ersatzteilmarkt

Hersteller von Bremsbelägen stehen vor einer großen Herausforderung, da Fahrzeugkomponenten immer länger halten. OEMs bevorzugen langlebige Bremsbeläge, die dank kontrollierter Reibung, reduziertem Verschleiß, geringerer Geräuschentwicklung und sanfterer Lauffläche weniger schnell an Leistung verlieren. Darüber hinaus berücksichtigen OEMs und Hersteller bei der Entwicklung von Bremsbelägen die Beständigkeit gegenüber Wasserauswaschung, einen breiten Betriebstemperaturbereich, die saubere Montage von Bremssattelkomponenten, Straßenschmutz und Oxidation. Regeneratives Bremsen wird seit einigen Jahren in batteriebetriebenen Elektrofahrzeugen eingesetzt. Die Hersteller von Elektrofahrzeugen verwenden fortschrittliche Bremsbeläge, um einen reibungslosen Betrieb der Fahrzeuge zu gewährleisten. In der Elektrofahrzeugproduktion kommen Bremsscheiben aus Metall zum Einsatz. Mit den steigenden Verkaufszahlen von Elektrofahrzeugen wächst die Nachfrage im Markt für Kfz-Reifenersatzteile im Prognosezeitraum rasant, da diese Bremsbeläge leichter und hocheffizient sind. Daher wird angesichts der steigenden Nachfrage nach umweltfreundlichen Transportmitteln und der hohen Nachfrage nach Elektrofahrzeugen mit einem starken Wachstumspotenzial im Markt für Kfz-Reifenersatzteile gerechnet.

Marktübersicht für den Kfz-Reifen-Ersatzteilmarkt

Der wichtigste Bestandteil eines Fahrzeugs ist der Reifen, der auf den Felgen sitzt und den Fahrzeugantrieb überträgt. Reifen absorbieren und reduzieren zudem die Stöße verschiedener Fahrbahnbeschaffenheiten. Zur Herstellung von Autoreifen werden Materialien wie Gewebe, Draht, Naturkautschuk, Ruß, Synthesekautschuk und andere chemische Verbindungen verwendet. Reifenhersteller investieren kontinuierlich in Forschung und Entwicklung, um Hochleistungsreifen zu produzieren und Nanotechnologie in die Reifenherstellung zu integrieren.

Ein Autoreifen besteht aus Lauffläche und Karkasse. Die Lauffläche sorgt für die Bodenhaftung, während die Karkasse die komprimierte Luft einschließt. Bevor Gummi entwickelt wurde, bestanden die ersten Reifen aus einfachen Metallbändern, die um Holzräder gewickelt wurden, um Verschleiß zu verhindern. Frühe Gummireifen waren Vollgummireifen (nicht luftgefüllt). Luftreifen werden heute an vielen Fahrzeugen eingesetzt, darunter Autos, Fahrräder, Motorräder, Busse, Lkw, Baumaschinen und Flugzeuge. Metallreifen werden weiterhin an Lokomotiven und Schienenfahrzeugen verwendet; Vollgummireifen (oder Reifen aus anderen Polymeren) kommen jedoch in verschiedenen Anwendungen außerhalb des Automobilbereichs zum Einsatz, beispielsweise bei Rollen, Karren, Rasenmähern und Schubkarren.

Highlights der Marktforschung

- Der globale Markt für den Kfz-Reifen-Ersatzteilmarkt wurde im Jahr 2025 auf 121,32 Milliarden US-Dollar geschätzt.

- Es wird erwartet, dass das jährliche Marktvolumen bis 2034 150,73 Milliarden US-Dollar erreichen wird.

- Der gesamte adressierbare Markt (TAM) wird im Zeitraum 2026-2034 voraussichtlich rund 1.234,14 Milliarden US-Dollar erreichen.

- Es wird erwartet, dass der Markt im Prognosezeitraum eine durchschnittliche jährliche Wachstumsrate (CAGR) von 2,44 % verzeichnen wird.

- Die Vereinigten Staaten stellen einen Schlüsselmarkt dar, der durch die steigende Nachfrage nach kraftstoffsparenden Reifen sowie die sich wandelnde Branchendynamik gestützt wird.

- Die Marktanalyse umfasst Nordamerika, Europa, den asiatisch-pazifischen Raum, Süd- und Mittelamerika, den Nahen Osten und Afrika, wobei das Wachstum über den gesamten Prognosezeitraum bewertet wird.

- Marktchancen wie die steigende Nachfrage nach umweltfreundlichen Reifen bei Nutz- und Personenfahrzeugen, die den Markttrend antreibt, werden voraussichtlich die Marktdynamik und den adressierbaren Markt beeinflussen.

- Der Bericht stellt Branchenteilnehmer wie APOLLO TIRES LTD, Continental AG, PIRELLI und CSPA, Sumitomo Rubber Industries, Ltd., THE GOODYEAR TIRE AND RUBBER COMPANY, YOKOHAMA RUBBER CO., LTD, ZHONGCE RUBBER GROUP CO. LTD., NEXEN TIRE AMERICA INC, BRIDGESTONE CORPORATION und MICHELIN vor und analysiert Wettbewerbsstrategien und Innovationsentwicklungen.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für Kfz-Reifen im Ersatzteilmarkt: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Treiber und Chancen des Kfz-Reifen-Ersatzteilmarktes

Steigende Nachfrage nach kraftstoffsparenden Reifen

Kraftstoff gehört zu den Gütern, deren Preise ständig schwanken. In den letzten Jahren sind sie eher gestiegen als gefallen. Verbraucher können Geld sparen, indem sie kraftstoffsparende Reifen an ihren Fahrzeugen montieren. Diese Reifen werden auch als rollwiderstandsarme Reifen bezeichnet. Der Rollwiderstand ist die Kraft, die nötig ist, um ein Fahrzeug mit einer bestimmten Geschwindigkeit in Bewegung zu halten. Der Grad der Reibung an den Reifen bestimmt die Menge an Kraftstoff und Energie, die verbraucht wird. Rollwiderstandsarme Reifen benötigen weniger Energie zum Rollen und reduzieren so den Gesamtverbrauch. Aufgrund der steigenden Verbrauchernachfrage, des Klimawandels und ihrer geringeren CO₂-Bilanz im Vergleich zu Standardreifen sind rollwiderstandsarme Reifen sehr gefragt. Beispielsweise gilt der Michelin Energy Saver A/S All-Season als einer der besten kraftstoffsparenden Reifen und ist bei vielen Autofahrern beliebt. Diese Faktoren tragen zum Wachstum des Marktes für Autoreifen bei.

Der steigende Absatz von Elektrofahrzeugen und die sprunghaft ansteigende Nachfrage nach schlauchlosen Reifen dürften dem Markt reichlich Wachstumschancen eröffnen.

Elektrofahrzeuge benötigen spezielle Reifen. Laut Herstellerangaben müssen diese ein höheres Gewicht aufweisen als Reifen von Verbrennern und beim Anfahren nach dem Stand mehr Drehmoment auf die Straße übertragen. Reifengeräusche sind bei Elektrofahrzeugen aufgrund ihrer nahezu geräuschlosen Antriebe, die größtenteils vom Motorengeräusch überdeckt werden, deutlicher wahrnehmbar als bei Verbrennern. Die Einführung von Elektrofahrzeugen und ihre deutlich geringere Antriebsgeräuschemission ermöglichen eine präzisere Messung der Reifen-Fahrbahn-Geräusche mittels Fahrtmessungen, selbst bei Geschwindigkeiten, bei denen ein Verbrennungsmotor die Messergebnisse normalerweise verfälschen würde. Der vom EU-Reifenlabel angegebene Rollwiderstand dient als primäres Auswahlkriterium für potenzielle Reifen für Elektrofahrzeuge.

Marktsegmentierungsanalyse für den Kfz-Reifen-Ersatzteilmarkt

Zu den wichtigsten Segmenten, die zur Ableitung der Marktanalyse für den Kfz-Reifen-Ersatzteilmarkt beigetragen haben, gehören Reifentyp, Vertriebskanal, Felgengröße, Fahrzeugtyp und Geografie.

- Basierend auf dem Reifentyp wird der Markt in Radialreifen und Diagonalreifen unterteilt. Radialreifen werden aufgrund der steigenden Automobilproduktion im Jahr 2023 einen größeren Marktanteil haben.

- Basierend auf dem Vertriebskanal ist der Markt in OES und IAM unterteilt. Unter diesen haben die Originalgerätehersteller im Jahr 2023 den größten Marktanteil.

- Je nach Felgengröße wird der Markt in 13-15, 16-18, 19-21 und mehr als 21 unterteilt.

- Je nach Fahrzeugtyp ist der Markt in Pkw, leichte Nutzfahrzeuge und schwere Nutzfahrzeuge unterteilt. Pkw haben 2023 den größten Marktanteil, was auf die weltweit steigenden Pkw-Verkäufe zurückzuführen ist.

Marktanteilsanalyse des Kfz-Reifen-Ersatzteilmarktes nach Regionen

Der geografische Umfang des Marktberichts für den Kfz-Reifen-Ersatzteilmarkt ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten & Afrika sowie Süd- & Mittelamerika.

Der asiatisch-pazifische Raum (APAC) gilt als die am schnellsten wachsende Wirtschaftsregion, wobei China und Indien die weltweit am schnellsten bzw. drittschnellsten wachsenden Volkswirtschaften sind. Japan ist das technologisch fortschrittlichste Land der Region und bietet somit Potenzial für die Entwicklung des Marktes für Autoreifen. In den aufstrebenden Volkswirtschaften Südostasiens wie Vietnam, Malaysia und Indonesien steigen die Verkaufszahlen von Pkw, wodurch die Nachfrage nach Autoreifen im Ersatzteilmarkt voraussichtlich zunehmen wird.

Die Automobilindustrie trägt maßgeblich zum europäischen Wohlstand bei, da sie einen erheblichen Anteil am regionalen BIP ausmacht und zahlreichen Menschen Arbeit bietet. Aus diesem Grund hat die Europäische Kommission verschiedene Initiativen zur Förderung der Automobilindustrie in Europa ergriffen, darunter den Aktionsplan CARS 2020 und GEAR 2030. Diese Initiativen der europäischen Regierung sollen das nachhaltige Wachstum der Automobilindustrie in Europa unterstützen. Dies wiederum wird das Wachstum des europäischen Ersatzteilmarktes für Autoreifen begünstigen.

Autoreifen-Ersatzteilmarkt

Berichtsumfang zum Markt für Kfz-Reifen-Ersatzteile

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 121,32 Milliarden US-Dollar |

| Marktgröße bis 2034 | 150,73 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 2,44 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nach Reifentyp

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte im Kfz-Reifen-Ersatzteilmarkt: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Kfz-Reifen im Ersatzteilmarkt wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile der Produkte. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Kundenbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

Neuigkeiten und aktuelle Entwicklungen im Kfz-Reifen-Ersatzteilmarkt

Der Markt für Kfz-Reifen im Ersatzteilmarkt wird anhand qualitativer und quantitativer Daten nach Primär- und Sekundärforschung analysiert. Diese umfasst wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken. Einige Entwicklungen im Markt für Kfz-Reifen im Ersatzteilmarkt sind nachfolgend aufgeführt:

- MRF, Indiens größter Reifenhersteller, hat kürzlich die neuen STEEL BRACE Radialreifen für Hochleistungsmotorräder auf den Markt gebracht. Die Steel Brace Radialreifen sind hochspezialisierte Reifen, die speziell für High-End-Motorräder entwickelt wurden, die unter extremen Bedingungen außergewöhnliche Leistung erfordern. (Quelle: Unternehmenswebsite, Juli 2023)

- Continental hat heute seinen bisher nachhaltigsten Serienreifen vorgestellt – den UltraContact NXT. Mit bis zu 65 Prozent erneuerbaren, recycelten und massenbilanzzertifizierten Materialien vereint er einen bemerkenswert hohen Anteil an nachhaltigen Werkstoffen mit maximaler Sicherheit und Leistung. Continental ist der erste Hersteller, der einen Reifen mit sowohl einem hohen Anteil an nachhaltigen Materialien als auch maximaler Leistung gemäß dem EU-Reifenlabel in Serie produziert. (Quelle: Pressemitteilung, Juni 2023)

Marktbericht zum Kfz-Reifen-Ersatzteilmarkt: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für den Kfz-Reifen-Ersatzteilmarkt (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die folgende Bereiche abdeckt:

- Marktgröße und Prognose für den Kfz-Reifen-Ersatzteilmarkt auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt werden

- Trends im Kfz-Reifen-Ersatzteilmarkt sowie Marktdynamiken wie Treiber, Hemmnisse und wichtige Chancen

- Detaillierte PEST- und SWOT-Analyse

- Analyse des Kfz-Reifen-Ersatzteilmarktes: Wichtige Markttrends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Rahmenbedingungen und aktuelle Marktentwicklungen

- Branchenlandschafts- und Wettbewerbsanalyse mit Marktkonzentration, Heatmap-Analyse, führenden Akteuren und aktuellen Entwicklungen im Markt für Kfz-Reifen-Ersatzteile

- Detaillierte Unternehmensprofile

Naveen ist ein erfahrener Marktforschungs- und Beratungsexperte mit über 9 Jahren Erfahrung in kundenspezifischen, syndizierten und Beratungsprojekten. In seiner aktuellen Funktion als Associate Vice President hat er erfolgreich Stakeholder entlang der gesamten Projektwertschöpfungskette gemanagt und ist Autor von über 100 Forschungsberichten und über 30 Beratungsaufträgen. Seine Arbeit erstreckt sich auf Industrie- und Regierungsprojekte und trägt maßgeblich zum Kundenerfolg und zur datengesteuerten Entscheidungsfindung bei.

Naveen hat einen Ingenieursabschluss in Elektronik und Kommunikation von der VTU, Karnataka, und einen MBA in Marketing und Operations von der Manipal University. Er ist seit 9 Jahren aktives IEEE-Mitglied und nimmt an Konferenzen und technischen Symposien teil und engagiert sich ehrenamtlich auf Sektions- und regionaler Ebene. Vor seiner aktuellen Position arbeitete er als Associate Strategic Consultant bei IndustryARC und als Industrial Server Consultant bei Hewlett Packard (HP Global).

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends