Cuota de mercado, crecimiento y demanda del mercado de repuestos para neumáticos de automóviles hasta 2034.

Tamaño y pronóstico del mercado de repuestos para neumáticos automotrices (2021-2034), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por tipo de neumático (neumático radial y neumático diagonal), canal de distribución (proveedor de equipo original y IAM), tamaño de llanta (13-15, 16-18, 19-21 y más de 21), tipo de vehículo (automóviles de pasajeros, vehículos comerciales ligeros y vehículos comerciales pesados) y geografía.

- Estado : Datos publicados

- Código de informe : TIPRE00028388

- Categoría : Automoción y transporte

- Número de páginas : 150

- Formatos de informe disponibles :

- Fecha de última actualización : April 09, 2026

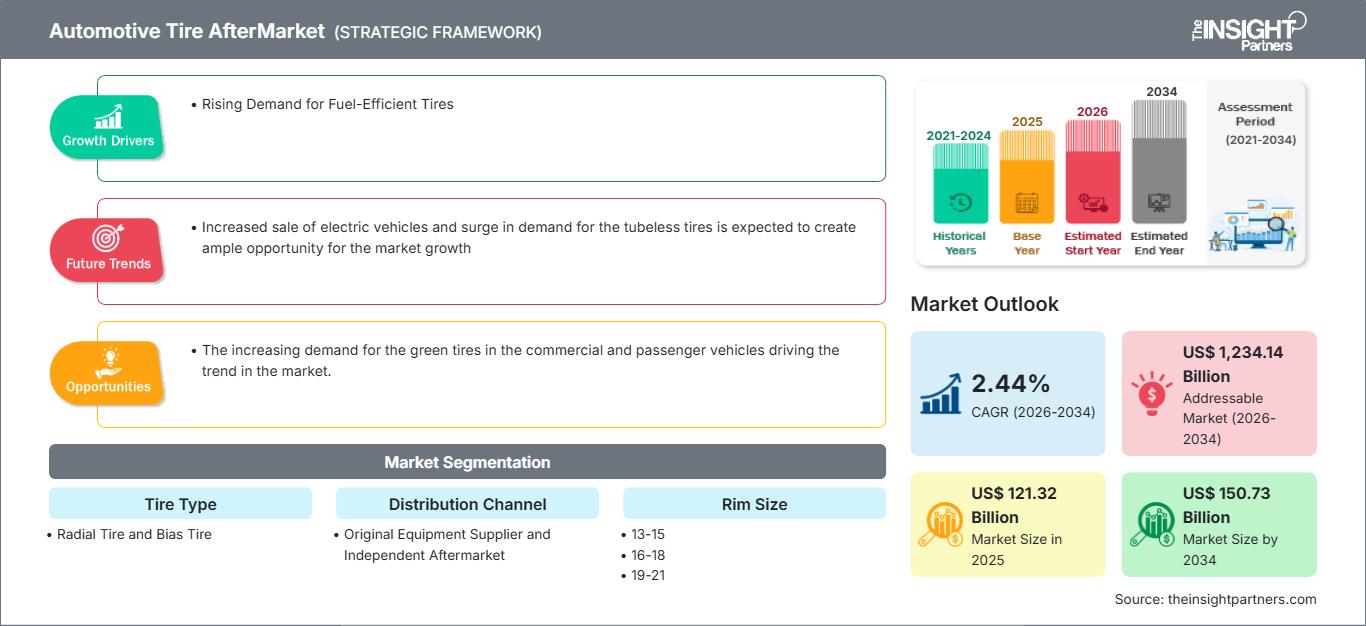

Se prevé que el mercado de repuestos para neumáticos de automóviles alcance los 150.730 millones de dólares estadounidenses en 2034, frente a los 121.320 millones de dólares estadounidenses en 2025. Se espera que el mercado registre una tasa de crecimiento anual compuesta (CAGR) del 2,44% durante el período de previsión 2026-2034.

Análisis del mercado de repuestos para neumáticos de automóviles

Los fabricantes de productos de fricción para frenos se enfrentan a un desafío importante a medida que los componentes de los vehículos tienen una vida útil más larga. Los fabricantes de equipos originales (OEM) prefieren productos de fricción de larga duración que se desgasten menos rápidamente debido a una fricción controlada, un menor desgaste, un menor ruido y una menor aspereza. Además, al desarrollar productos de fricción para frenos, los OEM y los fabricantes consideran la durabilidad en términos de resistencia al lavado con agua, un amplio rango de temperatura de servicio, un ensamblaje limpio de los componentes de la pinza de freno, contaminantes de la carretera y oxidación. El frenado regenerativo se ha utilizado en vehículos eléctricos a batería en los últimos años. Los fabricantes de vehículos eléctricos están adoptando productos de fricción avanzados para un funcionamiento suave de los vehículos. En la fabricación de vehículos eléctricos se utilizan discos de rotor metálicos. Con el aumento de las ventas de vehículos eléctricos, la demanda del mercado de repuestos para neumáticos de automóviles está creciendo a un ritmo acelerado durante el período de pronóstico, ya que estos productos de fricción para frenos son más ligeros y altamente eficientes. Por lo tanto, con la creciente demanda de transporte ecológico y la alta demanda de vehículos eléctricos, se espera que exista una amplia oportunidad para el crecimiento del mercado de repuestos para neumáticos de automóviles.

Panorama general del mercado de repuestos para neumáticos de automóviles

La parte más importante de un vehículo es el neumático, que se coloca sobre las llantas y transmite la propulsión. Los neumáticos también absorben y reducen los impactos de las diferentes condiciones de la carretera. Para la fabricación de neumáticos se utilizan materiales como tela, alambre, caucho natural, negro de humo, caucho sintético y otros compuestos químicos. Los fabricantes de neumáticos invierten constantemente en investigación y desarrollo para producir neumáticos de alto rendimiento e incorporar la nanotecnología en su fabricación.

Un neumático de automóvil consta de una banda de rodadura y una carcasa. La banda de rodadura proporciona tracción, mientras que la carcasa contiene una cantidad de aire comprimido. Antes del desarrollo del caucho, las primeras versiones de neumáticos eran simplemente bandas de metal colocadas alrededor de ruedas de madera para evitar el desgaste. Los primeros neumáticos de caucho eran macizos (no neumáticos). Actualmente, los neumáticos neumáticos se utilizan en muchos vehículos, incluidos automóviles, bicicletas, motocicletas, autobuses, camiones, maquinaria pesada y aeronaves. Los neumáticos metálicos todavía se utilizan en locomotoras y vagones de ferrocarril; sin embargo, los neumáticos de caucho macizo (u otros polímeros) se utilizan en diversas aplicaciones no automotrices, como ruedas giratorias, carros, cortadoras de césped y carretillas.

Aspectos destacados de la investigación de mercado

- El mercado global de repuestos para neumáticos de automóviles alcanzó un valor de 121.320 millones de dólares estadounidenses en 2025.

- Se prevé que el tamaño del mercado anual alcance los 150.730 millones de dólares estadounidenses para el año 2034.

- Se prevé que el mercado total disponible (TAM) durante el período 2026-2034 alcance aproximadamente los 1.234,14 mil millones de dólares estadounidenses.

- Se prevé que el mercado registre una tasa de crecimiento anual compuesta (CAGR) del 2,44% durante el período de pronóstico.

- Estados Unidos representa un mercado clave, impulsado por la creciente demanda de neumáticos de bajo consumo de combustible, así como por la evolución de la dinámica del sector.

- El análisis de mercado abarca América del Norte, Europa, Asia-Pacífico, América del Sur y Central, Oriente Medio y África, con un crecimiento evaluado durante el período de pronóstico.

- Se espera que las oportunidades de mercado, como la creciente demanda de neumáticos ecológicos en vehículos comerciales y de pasajeros, influyan en la dinámica del mercado y en el mercado potencial.

- El informe presenta perfiles de participantes de la industria, incluyendo APOLLO TIRES LTD, Continental AG, PIRELLI AND CSPA, Sumitomo Rubber Industries, Ltd., THE GOODYEAR TIRE AND RUBBER COMPANY, YOKOHAMA RUBBER CO., LTD, ZHONGCE RUBBER GROUP CO. LTD., NEXEN TIRE AMERICA INC, BRIDGESTONE CORPORATION, MICHELIN, al tiempo que analiza estrategias competitivas y desarrollos innovadores.

Personaliza este informe para adaptarlo a tus necesidades.

Obtén PERSONALIZACIÓN GRATUITAMercado de repuestos para neumáticos de automóviles: Perspectivas estratégicas

-

Descubra las principales tendencias del mercado que se recogen en este informe.Esta muestra GRATUITA incluirá análisis de datos, que abarcan desde tendencias de mercado hasta estimaciones y pronósticos.

Factores impulsores y oportunidades del mercado de repuestos para neumáticos de automóviles

Creciente demanda de neumáticos de bajo consumo de combustible

El combustible es uno de esos productos básicos cuyos precios fluctúan constantemente. En los últimos años, su precio ha seguido subiendo en lugar de bajar. Los consumidores podrían ahorrar dinero instalando neumáticos de bajo consumo en sus vehículos. Estos neumáticos también se conocen como neumáticos de baja resistencia a la rodadura. La resistencia a la rodadura es la fuerza necesaria para que el automóvil se mantenga en movimiento a una velocidad determinada. El grado de fricción ejercida sobre los neumáticos determina la cantidad de combustible y energía que se utiliza. Los neumáticos de baja resistencia a la rodadura requieren menos potencia para mantener el movimiento, reduciendo así el consumo total de combustible. La demanda de neumáticos de baja resistencia a la rodadura es alta debido a la creciente demanda de los consumidores, el cambio climático y la menor huella de carbono que generan en comparación con los neumáticos estándar. Por ejemplo, el Michelin Energy Saver A/S All-Season es ampliamente reconocido como uno de los mejores neumáticos de bajo consumo y es una opción popular entre la mayoría de los conductores. Estos factores impulsan el crecimiento del mercado de repuestos para neumáticos de automóviles.

Se espera que el aumento de las ventas de vehículos eléctricos y el auge de la demanda de neumáticos sin cámara creen amplias oportunidades para el crecimiento del mercado.

Los vehículos eléctricos requieren neumáticos específicos. Según el fabricante, sus neumáticos deben tener mayor peso que los de los coches de combustión interna y transmitir más par motor a la carretera al arrancar tras detenerse. El ruido de los neumáticos es más perceptible en los coches eléctricos que en los de combustión interna debido a sus sistemas de propulsión prácticamente silenciosos, enmascarados principalmente por el ruido del motor. La introducción de los vehículos eléctricos y su emisión de ruido de propulsión significativamente menor permiten evaluar el ruido de la carretera con mayor precisión mediante mediciones en carretera, incluso a velocidades en las que un sistema de propulsión con motor de combustión normalmente alteraría los resultados de la medición. El índice de resistencia a la rodadura proporcionado por la etiqueta de neumáticos de la Unión Europea se ha utilizado como criterio principal de selección para los neumáticos potenciales de los vehículos eléctricos.

Análisis de segmentación del informe de mercado de repuestos para neumáticos de automóviles

Los segmentos clave que contribuyeron a la elaboración del análisis del mercado de repuestos para neumáticos de automóviles son el tipo de neumático, el canal de distribución, el tamaño de la llanta, el tipo de vehículo y la geografía.

- Según el tipo de neumático, el mercado se divide en neumáticos radiales y neumáticos diagonales. De estos, los neumáticos radiales tuvieron una mayor cuota de mercado en 2023, debido al aumento de la producción automotriz.

- Según el canal de distribución, el mercado se divide en OES e IAM. Entre estos, los proveedores de equipos originales (OEM) tuvieron la mayor cuota de mercado en 2023.

- Según el tamaño de la llanta, el mercado se divide en 13-15, 16-18, 19-21 y más de 21.

- Según el tipo de vehículo, el mercado se divide en turismos, vehículos comerciales ligeros y vehículos comerciales pesados. De estos, los turismos representaron la mayor cuota de mercado en 2023, debido al aumento de sus ventas a nivel mundial.

Análisis de la cuota de mercado del mercado de repuestos para neumáticos de automóviles por región geográfica

El alcance geográfico del informe sobre el mercado de repuestos para neumáticos de automóviles se divide principalmente en cinco regiones: América del Norte, Asia Pacífico, Europa, Oriente Medio y África, y América del Sur y Central.

La región de Asia-Pacífico (APAC) se considera la de mayor crecimiento económico, con China e India como la primera y la tercera economías de mayor crecimiento a nivel mundial. Japón es el país tecnológicamente más avanzado de la región, lo que ofrece una oportunidad para el desarrollo del mercado de neumáticos para automóviles. Las economías emergentes del sudeste asiático, como Vietnam, Malasia e Indonesia, están experimentando un crecimiento en sus ventas de automóviles de pasajeros, por lo que se prevé un aumento en la demanda del mercado de repuestos para neumáticos.

La industria automotriz desempeña un papel fundamental en el crecimiento de la prosperidad europea, ya que representa una parte significativa del PIB de la región y genera empleo para un gran número de personas. Por ello, la Comisión Europea ha impulsado diversas iniciativas para el desarrollo de la industria automotriz en la región, como el Plan de Acción CARS 2020 y GEAR 2030. Se espera que estas iniciativas del gobierno europeo contribuyan al crecimiento sostenible de la industria automotriz en la región, lo que a su vez impulsará el crecimiento del mercado de repuestos para neumáticos en Europa.

Mercado de repuestos para neumáticos de automóviles

Alcance del informe de mercado de repuestos para neumáticos de automóviles

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2025 | 121.320 millones de dólares estadounidenses |

| Tamaño del mercado para 2034 | 150.730 millones de dólares estadounidenses |

| Tasa de crecimiento anual compuesta global (2026 - 2034) | 2,44% |

| Datos históricos | 2021-2024 |

| Período de pronóstico | 2026-2034 |

| Segmentos cubiertos |

Por tipo de neumático

|

| Regiones y países incluidos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de los actores del mercado de repuestos para neumáticos de automóviles: comprender su impacto en la dinámica empresarial.

El mercado de repuestos para neumáticos de automóviles está experimentando un rápido crecimiento, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor concienciación sobre los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

Noticias y novedades del mercado de repuestos para neumáticos de automóviles

El mercado de repuestos para neumáticos de automóviles se evalúa mediante la recopilación de datos cualitativos y cuantitativos tras una investigación primaria y secundaria, que incluye publicaciones corporativas importantes, datos de asociaciones y bases de datos. A continuación, se enumeran algunos de los avances en el mercado de repuestos para neumáticos de automóviles:

- MRF, el mayor fabricante de neumáticos de la India, lanzó recientemente los nuevos neumáticos radiales STEEL BRACE para motocicletas de alto rendimiento. Los Steel Brace son neumáticos altamente especializados, diseñados específicamente para motocicletas de alta gama que exigen un rendimiento excepcional en condiciones extremas. (Fuente: Sitio web de la empresa, julio de 2023)

- Continental presentó hoy su neumático de serie más sostenible hasta la fecha: el UltraContact NXT. Con hasta un 65 % de materiales renovables, reciclados y con certificación de balance de masas, combina una proporción excepcionalmente alta de materiales sostenibles con la máxima seguridad y rendimiento. Continental es el primer fabricante en lanzar un neumático con una alta proporción de materiales sostenibles y que cumple con la máxima normativa europea de neumáticos en producción en serie. (Fuente: Comunicado de prensa, junio de 2023)

Cobertura y entregables del informe de mercado de repuestos para neumáticos de automóviles

El informe “Tamaño y pronóstico del mercado de repuestos para neumáticos de automóviles (2021–2031)” proporciona un análisis detallado del mercado que abarca las siguientes áreas:

- Tamaño y pronóstico del mercado de repuestos para neumáticos de automóviles a nivel mundial, regional y nacional para todos los segmentos clave del mercado cubiertos en el alcance.

- Tendencias del mercado de repuestos para neumáticos de automóviles, así como la dinámica del mercado, tales como factores impulsores, limitaciones y oportunidades clave.

- Análisis detallado PEST y FODA

- Análisis del mercado de repuestos para neumáticos de automóviles, que abarca las principales tendencias del mercado, el marco global y regional, los principales actores, las regulaciones y los desarrollos recientes del mercado.

- Análisis del panorama de la industria y de la competencia, que abarca la concentración del mercado, el análisis de mapas de calor, los principales actores y los desarrollos recientes para el mercado de repuestos de neumáticos para automóviles.

- Perfiles detallados de las empresas

Naveen es un experimentado profesional en investigación de mercados y consultoría con más de 9 años de experiencia en proyectos personalizados, sindicados y de consultoría. Actualmente se desempeña como Vicepresidente Asociado, donde ha gestionado con éxito a las partes interesadas en toda la cadena de valor del proyecto y ha redactado más de 100 informes de investigación y más de 30 proyectos de consultoría. Su trabajo abarca proyectos industriales y gubernamentales, contribuyendo significativamente al éxito de los clientes y a la toma de decisiones basada en datos.

Naveen es licenciado en Ingeniería Electrónica y Comunicaciones por la VTU (Karnataka) y tiene un MBA en Marketing y Operaciones por la Universidad de Manipal. Ha sido miembro activo del IEEE durante 9 años, participando en conferencias, simposios técnicos y realizando voluntariado tanto a nivel de sección como regional. Antes de su puesto actual, trabajó como Consultor Estratégico Asociado en IndustryARC y como Consultor de Servidores Industriales en Hewlett Packard (HP Global).

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias