Part de marché, croissance et demande du marché de l'après-vente des pneumatiques automobiles d'ici 2034

Marché de la rechange de pneumatiques automobiles : taille et prévisions (2021-2034), parts de marché mondiales et régionales, tendances et analyse des opportunités de croissance. Couverture du rapport : par type de pneumatique (radial et diagonal), canal de distribution (équipementier d’origine et revendeur agréé), taille de jante (13-15, 16-18, 19-21 et plus de 21 pouces), type de véhicule (voitures particulières, véhicules utilitaires légers et poids lourds) et zone géographique.

- Statut : Données publiées

- Code du rapport : TIPRE00028388

- Catégorie : Automobile et transport

- Nombre de pages : 150

- Formats de rapport disponibles :

- Date de dernière mise à jour : April 09, 2026

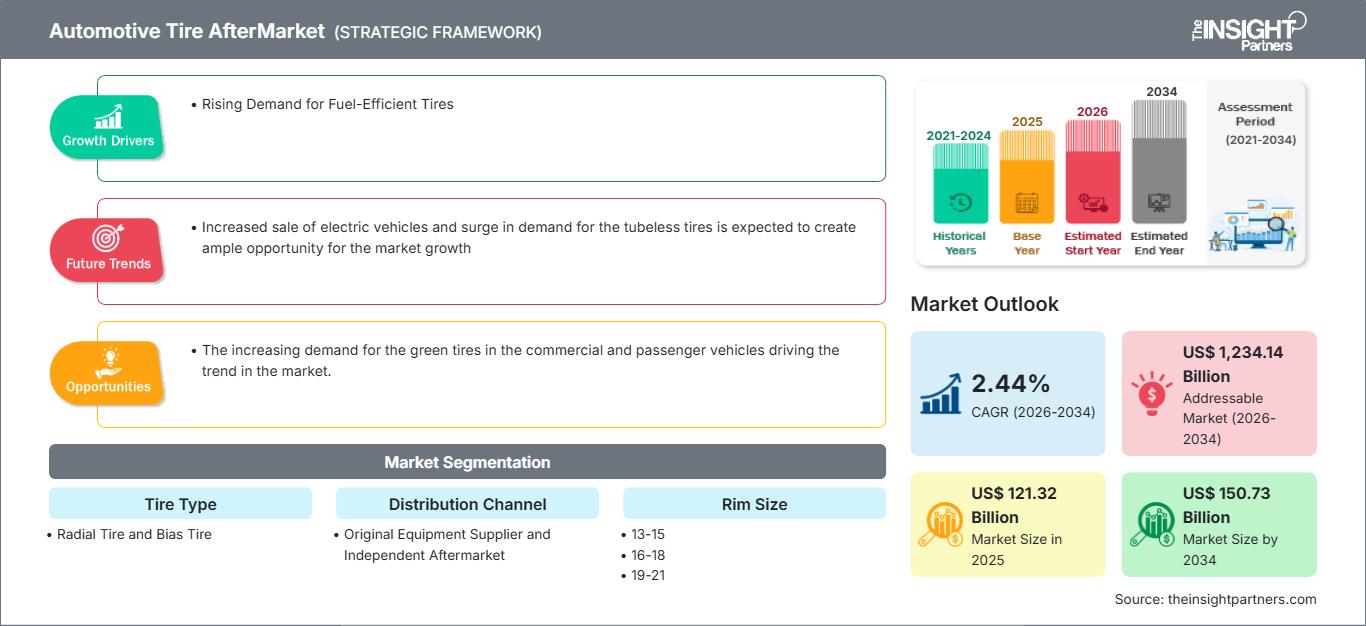

Le marché de l'après-vente des pneumatiques automobiles devrait atteindre 150,73 milliards de dollars américains d'ici 2034, contre 121,32 milliards de dollars américains en 2025. Ce marché devrait enregistrer un TCAC de 2,44 % au cours de la période de prévision 2026-2034.

Analyse du marché de l'après-vente des pneus automobiles

Les fabricants de produits de friction pour freins sont confrontés à un défi majeur : l’allongement de la durée de vie des composants automobiles. Les constructeurs automobiles privilégient des produits de friction durables, dont l’efficacité diminue grâce à un frottement contrôlé, une usure réduite, un niveau sonore et une rugosité moindres. De plus, lors du développement de ces produits, les constructeurs et les fabricants prennent en compte la durabilité, notamment la résistance au lessivage par l’eau, une large plage de températures de service, un assemblage propre des étriers de frein, les contaminants routiers et l’oxydation. Le freinage régénératif est utilisé depuis quelques années sur les véhicules électriques à batterie. Les constructeurs de véhicules électriques adoptent des produits de friction de pointe pour un fonctionnement optimal. Les disques de frein métalliques sont utilisés dans la fabrication de ces véhicules. Avec l’augmentation des ventes de véhicules électriques, la demande sur le marché de l’après-vente des pneumatiques automobiles connaît une croissance rapide, ces produits de friction étant plus légers et plus performants. Par conséquent, la demande croissante de transports écologiques, notamment de véhicules électriques, devrait offrir de nombreuses opportunités de croissance au marché de l’après-vente des pneumatiques automobiles.

Aperçu du marché de la rechange des pneus automobiles

L'élément le plus important d'un véhicule est le pneu, monté sur la jante et assurant la transmission de la propulsion. Les pneus absorbent et réduisent également les chocs liés aux différentes conditions routières. Des matériaux tels que le tissu, le fil d'acier, le caoutchouc naturel, le noir de carbone, le caoutchouc synthétique et d'autres composés chimiques sont utilisés pour fabriquer des pneus automobiles. Les fabricants de pneus investissent constamment dans la recherche et le développement afin de produire des pneus haute performance et d'intégrer les nanotechnologies à leur fabrication.

Un pneu automobile se compose d'une bande de roulement et d'une carcasse. La bande de roulement assure l'adhérence tandis que la carcasse contient de l'air comprimé. Avant l'invention du caoutchouc, les premiers pneus étaient de simples bandes de métal fixées autour de roues en bois pour les protéger de l'usure. Les premiers pneus en caoutchouc étaient pleins (non pneumatiques). Aujourd'hui, de nombreux véhicules, tels que les voitures, les vélos, les motos, les bus, les camions, les engins de chantier et les avions, sont équipés de pneus pneumatiques. Les pneus métalliques sont encore utilisés sur les locomotives et les wagons ; cependant, les pneus pleins en caoutchouc (ou autres polymères) sont employés dans diverses applications non automobiles, comme les roulettes, les chariots, les tondeuses à gazon et les brouettes.

Points saillants de l'étude de marché

- Le marché mondial des pièces de rechange pour pneumatiques automobiles était évalué à 121,32 milliards de dollars américains en 2025.

- La taille annuelle du marché devrait atteindre 150,73 milliards de dollars américains d'ici 2034.

- Le marché total adressable (TAM) devrait atteindre environ 1 234,14 milliards de dollars américains entre 2026 et 2034.

- Le marché devrait enregistrer un TCAC de 2,44 % au cours de la période de prévision.

- Les États-Unis représentent un marché clé, soutenu par la demande croissante de pneus à faible consommation de carburant, ainsi que par l'évolution de la dynamique du secteur.

- L'analyse de marché couvre l'Amérique du Nord, l'Europe, l'Asie-Pacifique, l'Amérique du Sud et centrale, le Moyen-Orient et l'Afrique, la croissance étant évaluée sur toute la période prévisionnelle.

- Les opportunités de marché, telles que la demande croissante de pneus verts pour les véhicules commerciaux et de tourisme, qui stimule la tendance du marché, devraient influencer la dynamique et le marché potentiel.

- Le rapport dresse le profil des acteurs du secteur, notamment APOLLO TIRES LTD, Continental AG, PIRELLI ET CSPA, Sumitomo Rubber Industries, Ltd., THE GOODYEAR TIRE AND RUBBER COMPANY, YOKOHAMA RUBBER CO., LTD, ZHONGCE RUBBER GROUP CO. LTD., NEXEN TIRE AMERICA INC, BRIDGESTONE CORPORATION et MICHELIN, tout en analysant leurs stratégies concurrentielles et leurs innovations.

Personnalisez ce rapport selon vos besoins.

Bénéficiez d'une PERSONNALISATION GRATUITEMarché de l'après-vente des pneumatiques automobiles : perspectives stratégiques

-

Découvrez les principales tendances du marché présentées dans ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Facteurs et opportunités du marché de l'après-vente des pneumatiques automobiles

Demande croissante de pneus à faible consommation de carburant

Le carburant fait partie de ces matières premières dont le prix fluctue constamment. Ces dernières années, son prix a continué d'augmenter. Les consommateurs peuvent réaliser des économies en installant des pneus à faible résistance au roulement sur leurs véhicules. Ces pneus sont également appelés pneus à faible résistance au roulement. La résistance au roulement correspond à la force nécessaire pour maintenir le véhicule en mouvement à une vitesse donnée. Le degré de friction exercé sur les pneus détermine la quantité de carburant et d'énergie consommée. Les pneus à faible résistance au roulement nécessitent moins de puissance pour rouler, réduisant ainsi la consommation totale de carburant. La demande pour ces pneus est forte en raison de la demande croissante des consommateurs, du changement climatique et de leur empreinte carbone globale plus faible que celle des pneus standards. Par exemple, le pneu Michelin Energy Saver A/S toutes saisons est largement reconnu comme l'un des meilleurs pneus à faible résistance au roulement et est un choix populaire auprès de nombreux conducteurs. Ces facteurs contribuent à la croissance du marché des pièces détachées pour pneumatiques.

L'augmentation des ventes de véhicules électriques et la forte demande de pneus sans chambre à air devraient créer de nombreuses opportunités de croissance pour le marché.

Les véhicules électriques nécessitent des pneumatiques spécifiques. Selon le constructeur, ces pneumatiques doivent être plus lourds que ceux des voitures thermiques et transmettre un couple plus important à la route lors des redémarrages. Le bruit de roulement est plus perceptible sur les voitures électriques que sur les véhicules thermiques en raison du fonctionnement quasi silencieux de leur groupe motopropulseur, principalement masqué par le bruit du moteur. L'arrivée des véhicules électriques et leurs émissions sonores considérablement réduites permettent désormais d'évaluer le bruit de roulement avec une plus grande précision grâce à des mesures en vitesse de croisière, même à des vitesses où un moteur thermique perturberait habituellement les mesures. L'indice de résistance au roulement, indiqué par l'étiquette européenne des pneumatiques, est le principal critère de sélection des pneumatiques pour véhicules électriques.

Analyse de segmentation du rapport sur le marché de l'après-vente des pneumatiques automobiles

Les principaux segments ayant contribué à l'élaboration de l'analyse du marché de l'après-vente des pneumatiques automobiles sont le type de pneu, le canal de distribution, la taille de la jante, le type de véhicule et la zone géographique.

- Selon le type de pneumatique, le marché se divise en pneumatiques radiaux et pneumatiques diagonaux. En 2023, les pneumatiques radiaux détenaient la part de marché la plus importante, en raison de l'augmentation de la production automobile.

- Selon le canal de distribution, le marché se divise en équipementiers d'origine (OES) et en fournisseurs de services d'intégration (IAM). Parmi ces derniers, les équipementiers d'origine détenaient la plus grande part de marché en 2023.

- En fonction de la taille de la jante, le marché est divisé en 13-15, 16-18, 19-21 et plus de 21.

- Selon le type de véhicule, le marché se divise en voitures particulières, véhicules utilitaires légers et véhicules utilitaires lourds. En 2023, les voitures particulières détenaient la part la plus importante du marché, en raison de la hausse des ventes à travers le monde.

Analyse des parts de marché du marché de la rechange des pneumatiques automobiles par zone géographique

La portée géographique du rapport sur le marché de l'après-vente des pneumatiques automobiles est principalement divisée en cinq régions : Amérique du Nord, Asie-Pacifique, Europe, Moyen-Orient et Afrique, et Amérique du Sud et centrale.

La région Asie-Pacifique est considérée comme la zone économique à la croissance la plus rapide, la Chine et l'Inde occupant respectivement la première et la troisième place mondiales en termes de croissance. Le Japon, pays le plus avancé technologiquement de la région, offre des perspectives de développement pour le marché des pneumatiques automobiles. Les économies émergentes d'Asie du Sud-Est, telles que le Vietnam, la Malaisie et l'Indonésie, connaissent une croissance de leurs ventes de voitures particulières, ce qui devrait stimuler la demande sur le marché de l'après-vente des pneumatiques automobiles.

L'industrie automobile joue un rôle majeur dans la prospérité de l'Europe, contribuant de manière significative à son PIB et fournissant des emplois à de nombreux citoyens. C'est pourquoi la Commission européenne a lancé plusieurs initiatives pour le développement de ce secteur, telles que le plan d'action CARS 2020 et GEAR 2030. Ces initiatives, prises par les pouvoirs publics européens, devraient favoriser une croissance durable de l'industrie automobile en Europe, contribuant ainsi au développement du marché de l'après-vente des pneumatiques.

Marché secondaire des pneus automobiles

Portée du rapport sur le marché de la rechange des pneus automobiles

| Attribut du rapport | Détails |

|---|---|

| Taille du marché en 2025 | 121,32 milliards de dollars américains |

| Taille du marché d'ici 2034 | 150,73 milliards de dollars américains |

| TCAC mondial (2026 - 2034) | 2,44% |

| Données historiques | 2021-2024 |

| Période de prévision | 2026-2034 |

| Segments couverts |

Par type de pneu

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché de l'après-vente des pneumatiques automobiles : comprendre son impact sur la dynamique commerciale

Le marché de la rechange pour pneumatiques automobiles connaît une croissance rapide, portée par une demande croissante des utilisateurs finaux. Cette demande est alimentée par l'évolution des préférences des consommateurs, les progrès technologiques et une meilleure connaissance des avantages des produits. Face à cette demande grandissante, les entreprises diversifient leur offre, innovent pour répondre aux besoins des consommateurs et tirent parti des tendances émergentes, ce qui contribue à la croissance du marché.

Actualités et développements récents du marché de la rechange des pneumatiques automobiles

Le marché de la rechange des pneumatiques automobiles est évalué à partir de données qualitatives et quantitatives recueillies après des recherches primaires et secondaires, notamment des publications d'entreprises importantes, des données d'associations et des bases de données. Voici quelques-unes des évolutions de ce marché :

- MRF, le plus grand fabricant de pneumatiques d'Inde, a récemment lancé les nouveaux pneus radiaux STEEL BRACE destinés aux motos hautes performances. Ces pneus hautement spécialisés sont conçus spécifiquement pour les motos haut de gamme exigeant des performances exceptionnelles dans des conditions extrêmes. (Source : Site web de l'entreprise, juillet 2023)

- Continental a présenté aujourd'hui son pneu le plus durable à ce jour : l'UltraContact NXT. Composé jusqu'à 65 % de matériaux renouvelables, recyclés et certifiés conformes aux normes d'équilibre massique, il allie une part remarquablement élevée de matériaux durables à une sécurité et des performances optimales. Continental est le premier fabricant à commercialiser en grande série un pneu présentant à la fois une forte proportion de matériaux durables et une performance maximale selon l'étiquetage européen. (Source : Communiqué de presse, juin 2023)

Couverture et livrables du rapport sur le marché de l'après-vente des pneumatiques automobiles

Le rapport « Taille et prévisions du marché de l’après-vente des pneumatiques automobiles (2021-2031) » fournit une analyse détaillée du marché couvrant les domaines suivants :

- Taille et prévisions du marché de l'après-vente des pneumatiques automobiles aux niveaux mondial, régional et national pour tous les segments clés couverts par le périmètre de l'étude

- Tendances et dynamiques du marché de l'après-vente des pneumatiques automobiles, notamment les facteurs moteurs, les contraintes et les principales opportunités.

- Analyse PEST et SWOT détaillée

- Analyse du marché de l'après-vente des pneumatiques automobiles couvrant les principales tendances du marché, le cadre mondial et régional, les principaux acteurs, la réglementation et les développements récents du marché.

- Analyse du paysage industriel et de la concurrence, incluant la concentration du marché, l'analyse par carte thermique, les principaux acteurs et les développements récents du marché de l'après-vente des pneumatiques automobiles.

- Profils d'entreprise détaillés

Naveen est un professionnel expérimenté des études de marché et du conseil, fort de plus de 9 ans d'expertise dans des projets personnalisés, syndiqués et de conseil. Actuellement vice-président associé, il a géré avec succès les parties prenantes tout au long de la chaîne de valeur des projets et a rédigé plus de 100 rapports de recherche et plus de 30 missions de conseil. Son expertise couvre des projets industriels et gouvernementaux, contribuant significativement à la réussite de ses clients et à la prise de décision fondée sur les données.

Naveen est titulaire d'un diplôme d'ingénieur en électronique et communication de la VTU, Karnataka, et d'un MBA en marketing et opérations de l'Université de Manipal. Membre actif de l'IEEE depuis 9 ans, il a participé à des conférences et des colloques techniques et s'est porté volontaire au niveau des sections et des régions. Avant d'occuper ce poste, il a travaillé comme consultant stratégique associé chez IndustryARC et comme consultant en serveurs industriels chez Hewlett Packard (HP Global).

- Analyse complète de la taille du marché et prévisions

- Analyse détaillée de la segmentation

- Évaluation approfondie de la dynamique du marché

- Aperçus par région et par pays

- Paysage concurrentiel et analyse comparative des entreprises

- Intelligence économique stratégique

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires