Quota di mercato, crescita e domanda del mercato dei ricambi per pneumatici automobilistici entro il 2034

Dimensioni e previsioni del mercato aftermarket degli pneumatici per autoveicoli (2021-2034), quota globale e regionale, trend e analisi delle opportunità di crescita. Copertura del rapporto: per tipo di pneumatico (pneumatico radiale e pneumatico diagonale), canale di distribuzione (fornitore di apparecchiature originali e IAM), dimensione del cerchio (13-15, 16-18, 19-21 e oltre 21), tipo di veicolo (autovetture, veicoli commerciali leggeri e veicoli commerciali pesanti) e area geografica.

- Stato : Dati rilasciati

- Codice del report : TIPRE00028388

- Categoria : Automotive e trasporti

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : April 09, 2026

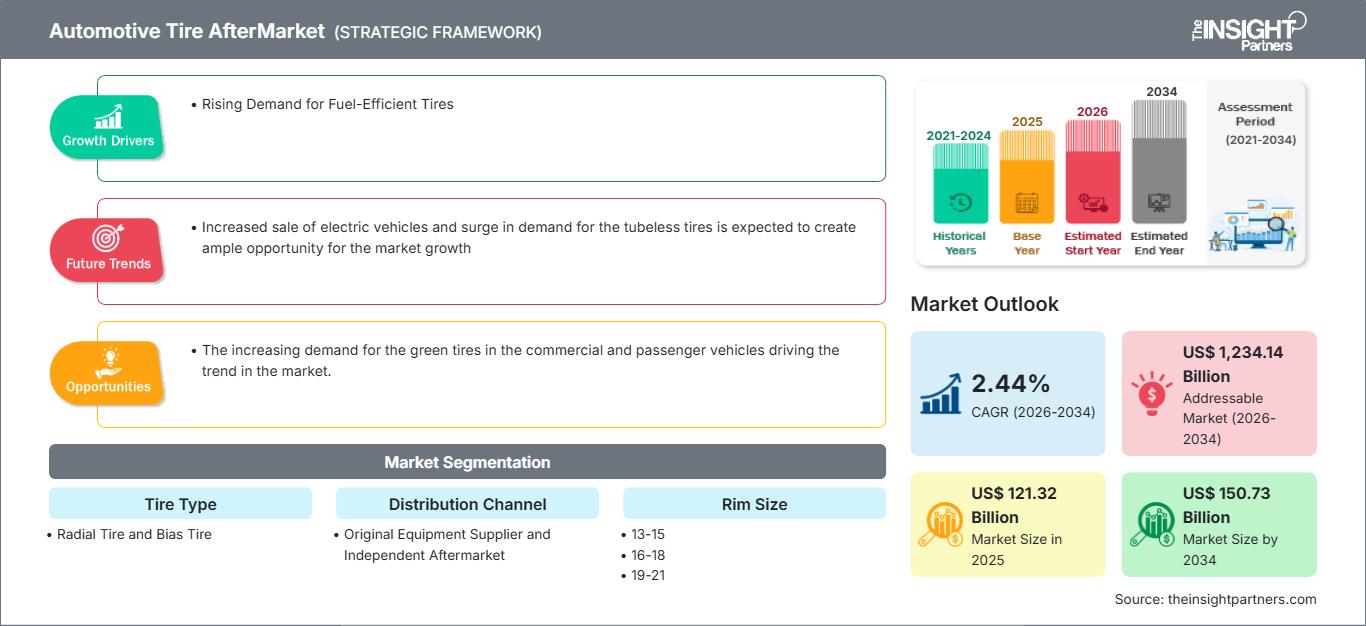

Si prevede che il mercato dei ricambi per pneumatici per autoveicoli raggiungerà un valore di 150,73 miliardi di dollari entro il 2034, rispetto ai 121,32 miliardi di dollari del 2025. Si prevede inoltre che il mercato registrerà un tasso di crescita annuo composto (CAGR) del 2,44% nel periodo di previsione 2026-2034.

Analisi del mercato dei ricambi per pneumatici automobilistici

I produttori di prodotti per l'attrito dei freni si trovano ad affrontare una sfida significativa, poiché la durata dei componenti dei veicoli è destinata a prolungarsi. I produttori di apparecchiature originali (OEM) prediligono prodotti per l'attrito dei freni di lunga durata che si deteriorino meno rapidamente grazie all'attrito controllato, alla riduzione dell'usura, alla minore rumorosità e alla minore rugosità. Inoltre, i produttori di OEM e di altri produttori considerano la durabilità in termini di resistenza al dilavamento da parte dell'acqua, un ampio intervallo di temperature di esercizio, un assemblaggio pulito dei componenti della pinza freno, la resistenza ai contaminanti stradali e all'ossidazione, durante lo sviluppo dei prodotti per l'attrito dei freni. La frenata rigenerativa è stata utilizzata negli ultimi anni nei veicoli elettrici a batteria. I produttori di veicoli elettrici stanno adottando prodotti per l'attrito avanzati per garantire un funzionamento fluido dei veicoli. I dischi freno in metallo sono utilizzati nella produzione di veicoli elettrici. Con l'aumento delle vendite di veicoli elettrici, la domanda per il mercato aftermarket degli pneumatici per autoveicoli sta crescendo rapidamente durante il periodo di previsione, poiché questi prodotti per l'attrito dei freni sono più leggeri e altamente efficienti. Pertanto, con la crescente domanda di trasporti ecocompatibili e l'elevata richiesta di veicoli elettrici, si prevede un'ampia opportunità di crescita per il mercato aftermarket degli pneumatici per autoveicoli.

Panoramica del mercato dei ricambi per pneumatici automobilistici

La parte più importante di un veicolo è il pneumatico, che si trova sui cerchioni e trasmette la propulsione del veicolo. I pneumatici assorbono e riducono anche gli impatti derivanti dalle diverse condizioni stradali. Materiali come tessuto, filo metallico, gomma naturale, nerofumo, gomma sintetica e altri composti chimici vengono utilizzati per la produzione di pneumatici per autoveicoli. I produttori di pneumatici investono costantemente in ricerca e sviluppo per produrre pneumatici ad alte prestazioni e integrare le nanotecnologie nella produzione di pneumatici.

Uno pneumatico per autoveicoli è costituito da un battistrada e da una carcassa. Il battistrada fornisce trazione, mentre la carcassa contiene una quantità di aria compressa. Prima dello sviluppo della gomma, le prime versioni di pneumatici erano semplicemente fasce di metallo montate attorno a ruote di legno per prevenire l'usura. I primi pneumatici in gomma erano pieni (non pneumatici). Oggi gli pneumatici sono utilizzati su molti veicoli, tra cui automobili, biciclette, motociclette, autobus, camion, macchinari pesanti e aeromobili. Gli pneumatici in metallo sono ancora utilizzati su locomotive e vagoni ferroviari; tuttavia, gli pneumatici in gomma piena (o altri polimeri) sono utilizzati in diverse applicazioni non automobilistiche, come rotelle, carrelli, tosaerba e carriole.

Punti salienti della ricerca di mercato

- Il mercato globale dei ricambi per pneumatici automobilistici (AfterMarket) aveva un valore di 121,32 miliardi di dollari nel 2025.

- Si prevede che il valore annuo del mercato raggiungerà i 150,73 miliardi di dollari entro il 2034.

- Si prevede che il mercato totale indirizzabile (TAM) nel periodo 2026-2034 raggiungerà circa 1.234,14 miliardi di dollari USA.

- Si prevede che il mercato registrerà un CAGR del 2,44% durante il periodo di previsione.

- Gli Stati Uniti rappresentano un mercato chiave, supportato dalla crescente domanda di pneumatici a basso consumo di carburante, nonché dalle dinamiche di settore in continua evoluzione.

- L'analisi di mercato copre Nord America, Europa, Asia-Pacifico, Sud e Centro America, Medio Oriente e Africa, con una valutazione della crescita per tutto il periodo di previsione.

- Opportunità di mercato come la crescente domanda di pneumatici ecologici nei veicoli commerciali e per passeggeri, che sta guidando la tendenza del mercato, dovrebbero influenzare le dinamiche di mercato e il mercato potenziale.

- Il rapporto delinea i profili dei partecipanti al settore, tra cui APOLLO TIRES LTD, Continental AG, PIRELLI AND CSPA, Sumitomo Rubber Industries, Ltd., THE GOODYEAR TIRE AND RUBBER COMPANY, YOKOHAMA RUBBER CO., LTD, ZHONGCE RUBBER GROUP CO. LTD., NEXEN TIRE AMERICA INC, BRIDGESTONE CORPORATION, MICHELIN, analizzando al contempo le strategie competitive e gli sviluppi innovativi.

Personalizza questo report in base alle tue esigenze

Ottieni la PERSONALIZZAZIONE GRATUITAMercato dei ricambi per pneumatici automobilistici: approfondimenti strategici

-

Scopri le principali tendenze di mercato di questo report.Questo campione GRATUITO includerà un'analisi dei dati, che spazierà dalle tendenze di mercato alle stime e alle previsioni.

Fattori trainanti e opportunità del mercato dei ricambi per pneumatici automobilistici

Aumento della domanda di pneumatici a basso consumo di carburante.

Il carburante è una di quelle materie prime i cui prezzi sono in continua evoluzione. Negli ultimi anni, il prezzo ha continuato ad aumentare anziché diminuire. I consumatori potrebbero risparmiare denaro installando pneumatici a basso consumo di carburante sui propri veicoli. I pneumatici a basso consumo di carburante sono anche noti come pneumatici a bassa resistenza al rotolamento. La resistenza al rotolamento è la forza necessaria per mantenere l'automobile in movimento a una data velocità. Il grado di attrito esercitato sui pneumatici determina la quantità di carburante e di energia utilizzata. I pneumatici a bassa resistenza al rotolamento richiedono meno potenza per mantenere la rotazione, riducendo così il consumo totale di carburante. I pneumatici a bassa resistenza al rotolamento sono molto richiesti a causa della crescente domanda dei consumatori, dei cambiamenti climatici e della minore impronta di carbonio complessiva dei pneumatici a basso consumo di carburante rispetto ai pneumatici standard. Ad esempio, il Michelin Energy Saver A/S All-Season è ampiamente considerato uno dei migliori pneumatici a basso consumo di carburante ed è una scelta popolare tra la maggior parte degli automobilisti. Questi fattori contribuiscono alla crescita del mercato dei pneumatici per autoveicoli.

L'aumento delle vendite di veicoli elettrici e l'impennata della domanda di pneumatici tubeless dovrebbero creare ampie opportunità di crescita per il mercato.

I veicoli elettrici richiedono pneumatici specifici. Secondo il costruttore, i pneumatici elettrici devono avere un peso maggiore rispetto a quelli delle auto con motore a combustione interna e trasmettere più coppia alla strada durante la ripresa della marcia dopo una sosta. Il rumore dei pneumatici è più evidente nelle auto elettriche rispetto ai veicoli con motore a combustione interna a causa della quasi totale silenziosità dei loro propulsori, in gran parte mascherata dal rumore del motore. L'introduzione dei veicoli elettrici e le loro emissioni sonore di propulsione significativamente inferiori consentono di valutare il rumore pneumatico-strada con maggiore precisione tramite misurazioni a velocità di crociera, anche a velocità in cui un sistema di propulsione con motore a combustione interna solitamente altererebbe i risultati della misurazione. L'indice di resistenza al rotolamento fornito dall'etichetta dei pneumatici dell'Unione Europea è stato utilizzato come criterio di selezione principale per i potenziali pneumatici per veicoli elettrici.

Analisi di segmentazione del mercato aftermarket degli pneumatici per autoveicoli

I segmenti chiave che hanno contribuito alla definizione dell'analisi di mercato del mercato aftermarket degli pneumatici per autoveicoli sono il tipo di pneumatico, il canale di distribuzione, la dimensione del cerchio, il tipo di veicolo e l'area geografica.

- In base alla tipologia, il mercato si divide in pneumatici radiali e pneumatici diagonali. Tra questi, i pneumatici radiali detengono una quota maggiore nel 2023, grazie all'aumento della produzione automobilistica.

- In base al canale di distribuzione, il mercato si suddivide in OES (Original Equipment Supplier) e IAM (Independent Asset Management). Tra questi, i fornitori di apparecchiature originali detengono la quota maggiore nel 2023.

- In base alla dimensione del cerchio, il mercato è suddiviso in 13-15, 16-18, 19-21 e oltre 21.

- A seconda della tipologia di veicolo, il mercato si suddivide in autovetture, veicoli commerciali leggeri e veicoli commerciali pesanti. Tra questi, le autovetture detengono una quota maggiore nel 2023, grazie all'aumento delle vendite di autovetture a livello globale.

Analisi delle quote di mercato del mercato dei ricambi per pneumatici automobilistici per area geografica

Il rapporto sul mercato dei ricambi per pneumatici automobilistici si articola principalmente in cinque regioni geografiche: Nord America, Asia Pacifico, Europa, Medio Oriente e Africa, e Sud e Centro America.

La regione Asia-Pacifico (APAC) è considerata l'area economica a più rapida crescita, con Cina e India rispettivamente al primo e terzo posto tra le economie a più rapida crescita al mondo. Il Giappone è il paese tecnologicamente più avanzato della regione, offrendo opportunità per lo sviluppo del mercato degli pneumatici per autoveicoli. Le economie emergenti del Sud-est asiatico, come Vietnam, Malesia e Indonesia, stanno registrando una crescita nelle vendite di autovetture, pertanto si prevede un aumento della domanda di pneumatici per autoveicoli nel mercato dei ricambi.

L'industria automobilistica svolge un ruolo significativo nella crescita e nella prosperità dell'Europa, in quanto contribuisce in modo considerevole al PIL regionale e offre lavoro a un gran numero di persone. Per questi motivi, la Commissione europea ha intrapreso diverse iniziative per lo sviluppo del settore automobilistico nella regione. Tra queste, il Piano d'azione CARS 2020 e GEAR 2030. Si prevede che queste iniziative del governo europeo sosterranno la crescita sostenibile dell'industria automobilistica nella regione. Questo fattore contribuirà ulteriormente alla crescita del mercato dei ricambi per pneumatici in Europa.

Pneumatici per autoveicoli (mercato dei ricambi)

Ambito del rapporto sul mercato dei ricambi per pneumatici automobilistici

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2025 | 121,32 miliardi di dollari |

| Dimensioni del mercato entro il 2034 | 150,73 miliardi di dollari |

| Tasso di crescita annuo composto (CAGR) globale (2026-2034) | 2,44% |

| Dati storici | 2021-2024 |

| periodo di previsione | 2026-2034 |

| Segmenti trattati |

Per tipologia di pneumatico

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori nel mercato dei ricambi per pneumatici automobilistici: comprenderne l'impatto sulle dinamiche di business

Il mercato dei ricambi per pneumatici per autoveicoli è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

Notizie e recenti sviluppi del mercato dei ricambi per pneumatici automobilistici

Il mercato dei ricambi per pneumatici per autoveicoli viene valutato raccogliendo dati qualitativi e quantitativi a seguito di ricerche primarie e secondarie, che includono importanti pubblicazioni aziendali, dati di associazioni e database. Di seguito sono elencati alcuni degli sviluppi nel mercato dei ricambi per pneumatici per autoveicoli:

- MRF, il più grande produttore di pneumatici in India, ha recentemente lanciato i nuovi pneumatici radiali STEEL BRACE per motociclette ad alte prestazioni. I pneumatici radiali Steel Brace sono pneumatici altamente specializzati, realizzati specificamente per motociclette di alta gamma che richiedono prestazioni straordinarie in condizioni estreme. (Fonte: sito web aziendale, luglio 2023)

- Continental ha presentato oggi il suo pneumatico di serie più sostenibile di sempre: l'UltraContact NXT. Con fino al 65% di materiali rinnovabili, riciclati e certificati per il bilancio di massa, combina una percentuale straordinariamente elevata di materiali sostenibili con la massima sicurezza e prestazioni. Continental è il primo produttore a lanciare un pneumatico con un'alta percentuale di materiali sostenibili e le massime prestazioni previste dall'etichetta UE per i pneumatici, in un prodotto di serie. (Fonte: Comunicato stampa, giugno 2023)

Copertura e risultati del rapporto sul mercato dei ricambi per pneumatici automobilistici

Il rapporto "Dimensioni e previsioni del mercato dei ricambi per pneumatici automobilistici (2021-2031)" fornisce un'analisi dettagliata del mercato, coprendo le seguenti aree:

- Dimensioni e previsioni del mercato aftermarket degli pneumatici per autoveicoli a livello globale, regionale e nazionale per tutti i principali segmenti di mercato coperti dall'ambito

- Tendenze del mercato dei ricambi per pneumatici automobilistici, nonché dinamiche di mercato quali fattori trainanti, vincoli e opportunità chiave.

- Analisi PEST e SWOT dettagliata

- Analisi del mercato dei ricambi per pneumatici automobilistici, con particolare attenzione alle principali tendenze di mercato, al quadro globale e regionale, ai principali operatori, alle normative e ai recenti sviluppi del mercato.

- Analisi del panorama industriale e della concorrenza, con particolare attenzione alla concentrazione del mercato, all'analisi tramite mappa di calore, ai principali operatori e agli sviluppi recenti del mercato dei ricambi per pneumatici automobilistici.

- Profili aziendali dettagliati

Naveen è un professionista esperto in ricerche di mercato e consulenza con oltre 9 anni di esperienza in progetti personalizzati, sindacati e di consulenza. Attualmente Vicepresidente Associato, ha gestito con successo gli stakeholder lungo l'intera catena del valore del progetto e ha redatto oltre 100 report di ricerca e oltre 30 incarichi di consulenza. Il suo lavoro spazia tra progetti industriali e governativi, contribuendo in modo significativo al successo dei clienti e al processo decisionale basato sui dati.

Naveen ha conseguito una laurea in Ingegneria Elettronica e delle Comunicazioni presso la VTU, Karnataka, e un MBA in Marketing e Operations presso la Manipal University. È membro attivo dell'IEEE da 9 anni, partecipando a conferenze, simposi tecnici e svolgendo attività di volontariato sia a livello di sezione che regionale. Prima del suo attuale ruolo, ha lavorato come Consulente Strategico Associato presso IndustryARC e come Consulente Server Industriali presso Hewlett Packard (HP Global).

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative