Marktgröße, Marktanteil und Trends im Bereich der elektronischen Kriegsführung bis 2034

Marktgröße und Prognose für elektronische Kampfführung (2021–2034), globaler und regionaler Marktanteil, Trends und Wachstumschancenanalyse. Berichtsabdeckung: Nach Komponenten (Hardware, Software und Dienstleistungen), Anwendung (Elektronischer Angriff, Elektronischer Schutz und Unterstützung der elektronischen Kampfführung), Produkttyp (Gegenmaßnahmensysteme, Störsender, Sensorsysteme, Waffensysteme und Sonstige) und Geografie.

- Status : Veröffentlichte Daten

- Berichtscode : TIPTE100000942

- Kategorie : Luft- und Raumfahrt und Verteidigung

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : April 09, 2026

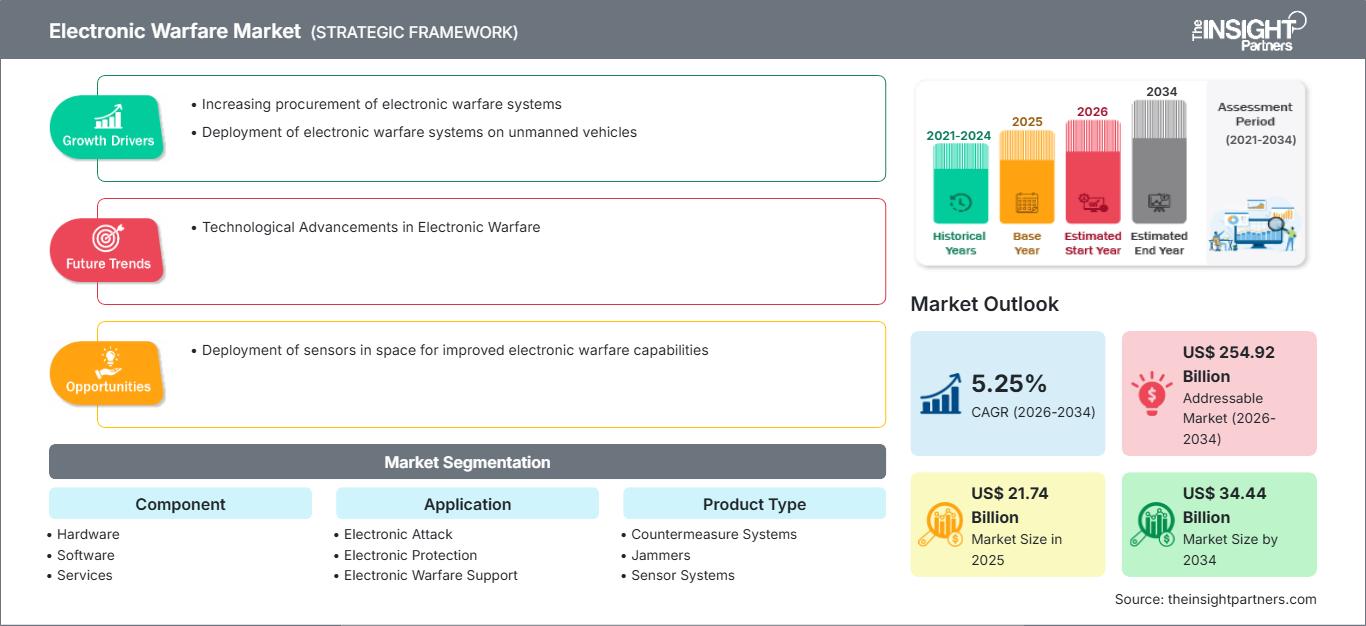

Der Markt für elektronische Kriegsführung wird voraussichtlich bis 2034 ein Volumen von 34,44 Milliarden US-Dollar erreichen, gegenüber 21,74 Milliarden US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Prognosezeitraum 2026–2034 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 5,25 % verzeichnen wird.

Marktanalyse für elektronische Kriegsführung

Zu den wichtigsten Akteuren im globalen Markt für elektronische Kampfführung zählen Rohstofflieferanten (Hardware und Komponenten), Hersteller elektronischer Kampfführungssysteme, Regierungsbehörden, Aufsichtsbehörden und Endkunden. Komponenten- und Hardwarelieferanten stellen Herstellern elektronischer Kampfführungssysteme diverse Komponenten und Teile zur Verfügung. Zu den in diesem Bericht genannten führenden Herstellern elektronischer Kampfführungssysteme gehören L3Harris Technologies, Inc., Raytheon Technology Corporation, Lockheed Martin Corporation, Saab AB, BAE Systems Plc, Thales Group, Northrop Grumman Corporation, Cobham Plc (Eaton), Leonardo Spa und Textron. Die wichtigsten Marktteilnehmer arbeiten kontinuierlich an der Weiterentwicklung von Systemen für die elektronische Kampfführung.

Marktübersicht Elektronische Kampfführung

Systemintegratoren spielen eine entscheidende Rolle bei der Installation von Systemen für die elektronische Kampfführung an den benötigten Standorten. Sie sind damit beauftragt, diese Systeme in ein vernetztes System zu integrieren und Feldversuche durchzuführen, um die Integration und die Wirkung der Systeme zu demonstrieren und zu testen. Zu diesen Akteuren zählen unter anderem Regierungsbehörden und Aufsichtsbehörden verschiedener Länder, darunter das US-Verteidigungsministerium (DoD, USDOD oder DOD), das russische Verteidigungsministerium, das chinesische Verteidigungsministerium, das israelische Verteidigungsministerium, das indische Verteidigungsministerium, das deutsche Bundesministerium für Verteidigung (BMVG) und das britische Verteidigungsministerium (MOD oder MoD).

Highlights der Marktforschung

- Der globale Markt für elektronische Kriegsführung wurde im Jahr 2025 auf 21,74 Milliarden US-Dollar geschätzt.

- Es wird erwartet, dass das jährliche Marktvolumen bis 2034 34,44 Milliarden US-Dollar erreichen wird.

- Der gesamte adressierbare Markt (TAM) wird im Zeitraum 2026-2034 voraussichtlich rund 254,92 Milliarden US-Dollar erreichen.

- Es wird erwartet, dass der Markt im Prognosezeitraum eine durchschnittliche jährliche Wachstumsrate (CAGR) von 5,25 % verzeichnen wird.

- Die Vereinigten Staaten stellen einen Schlüsselmarkt dar, was durch die zunehmende Beschaffung von Systemen für die elektronische Kampfführung, den Einsatz von Systemen für die elektronische Kampfführung auf unbemannten Fahrzeugen sowie die sich entwickelnde Dynamik der Branche gestützt wird.

- Die Marktanalyse umfasst Nordamerika, Europa, den asiatisch-pazifischen Raum, Süd- und Mittelamerika, den Nahen Osten und Afrika, wobei das Wachstum über den gesamten Prognosezeitraum bewertet wird.

- Marktchancen wie der Einsatz von Sensoren im Weltraum zur Verbesserung der Fähigkeiten der elektronischen Kriegsführung dürften die Marktdynamik und den adressierbaren Markt beeinflussen.

- Der Bericht stellt Branchenteilnehmer wie L3Harris Technologies, Inc., Raytheon Technologies Corporation, Lockheed Martin Corporation, Saab AB, BAE Systems, Thales Group, Northrop Grumman Corporation, Cobham Limited, Leonardo SpA und Textron Inc. vor und analysiert Wettbewerbsstrategien und Innovationsentwicklungen.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für elektronische Kriegsführung: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen im Bereich der elektronischen Kriegsführung

Einsatz von Systemen für die elektronische Kampfführung auf unbemannten Fahrzeugen

Streitkräfte und nichtstaatliche Gruppen setzen unbemannte Luftfahrtsysteme ein. Selbst kleinste kommerzielle Drohnen können bewaffnet werden und katastrophale Schäden anrichten. Die Entwicklung von Strategien zur Abwehr dieser bewaffneten Drohnen ist angesichts ihrer zunehmenden Verbreitung auf dem Schlachtfeld von höchster Priorität. Elektronische Kommunikationstechnologien sind für autonome und ferngesteuerte Fahrzeuge unerlässlich. Mit der wachsenden Anzahl an Aufgaben, die unbemannten Systemen übertragen werden, steigt auch der Bedarf an Abwehrsystemen für unbemannte Luftfahrtsysteme (UAS) und Technologien für die elektronische Kampfführung (EK). Unbemannte Luftfahrzeuge sind weltweit zu einem wichtigen Bestandteil der Streitkräfte geworden. Die Verarbeitung von Überwachungs- und Bilddaten wird durch den Einsatz von EK-Geräten auf unbemannten Plattformen erleichtert. Verschiedene unbemannte EK-Missionen profitieren von der Integration unbemannter Systeme mit Kommunikationsstörsendern oder elektronischer Überwachungstechnik. Darüber hinaus benötigen unbemannte EK-Flugzeuge kein Personal, wodurch das Risiko menschlicher Verluste sinkt. Aufgrund dieser Vorteile planen Länder wie die USA, Indien und China die Anschaffung und den Einsatz weiterer UAVs in ihren Streitkräften.

Technologische Fortschritte in der elektronischen Kriegsführung

Im Informationszeitalter werden die Kämpfer der nächsten Generation auf ein völlig neues Umfeld der elektronischen Kriegsführung und elektronischen Aufklärung treffen. Rasante technologische Fortschritte werden die Konflikte des 21. Jahrhunderts maßgeblich beeinflussen, da fortschrittliche Systeme ein verbessertes Lagebewusstsein, eine präzisere Bedrohungsanalyse und einen genaueren, zeitnahen und automatisierten Abgleich aktiver Signale mit den Ressourcen weitverzweigter Datenbanken ermöglichen. In einer verteilten virtuellen Umgebung können Bediener und Analysten in Echtzeit zusammenarbeiten. Sie konfigurieren, starten und steuern hocheffiziente Software-Agenten, um geografisch verteilte Aktivitäten und komplexe Analysen in einem dynamischen operativen Kontext effizient und schnell durchzuführen.

Durch die Entwicklungen in der Informationstechnologie eröffnen sich spannende neue Möglichkeiten, die das Interesse von Militärs wecken und zu Anforderungen führen, die die neuesten Technologien nutzen und gleichzeitig weitere technologische Fortschritte vorantreiben. Die Instrumente der elektronischen Kriegsführung entwickeln sich rasant, und das Pentagon, das Hauptquartier der US-Verteidigung, bereitet sich bereits jetzt auf deren zukünftigen militärischen Einsatz im Hinblick auf operative Kriegsführung vor.

Marktbericht Elektronische Kampfführung: Segmentierungsanalyse

Die wichtigsten Segmente, die zur Ableitung der Marktanalyse für elektronische Kriegsführung beigetragen haben, sind Komponente, Anwendung und Produkttyp.

- Basierend auf den Komponenten ist der Markt für elektronische Kriegsführung in Hardware, Software und Dienstleistungen unterteilt. Das Hardware-Segment hatte 2023 den größten Marktanteil.

- Basierend auf der Anwendung ist der Markt für elektronische Kriegsführung in elektronische Angriffe, elektronischen Schutz und Unterstützung der elektronischen Kriegsführung unterteilt. Das Segment Unterstützung der elektronischen Kriegsführung hielt 2023 den größten Marktanteil.

- Nach Produkttyp ist der Markt in Gegenmaßnahmensysteme, Störsender, Sensorsysteme, Waffensysteme und Sonstiges unterteilt. Das Segment der Sensorsysteme hielt 2023 den größten Marktanteil.

Marktanteilsanalyse für elektronische Kriegsführung nach Regionen

Der geografische Umfang des Marktberichts zur elektronischen Kriegsführung ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Europa, Asien-Pazifik, Naher Osten & Afrika und Südamerika.

Nordamerika dominierte den Markt im Jahr 2023, gefolgt von Europa und dem asiatisch-pazifischen Raum. Der asiatisch-pazifische Raum dürfte in den kommenden Jahren das höchste durchschnittliche jährliche Wachstum (CAGR) verzeichnen. Globale Streitkräfte haben nicht länger die Befugnis, den Zugang zu Aktivitäten im Weltraum einzuschränken oder zu verweigern. Auf dem internationalen Markt wird das Wissen über Weltraumsysteme und Methoden zu deren Abwehr zunehmend verfügbar. Staaten können die Fähigkeit erwerben, die Weltraumsysteme eines Gegners zu stören oder zu zerstören, indem sie dessen Satelliten im Orbit, dessen Boden- und Weltraumkommunikationsknoten oder die Bodenstationen, die die Satelliten steuern, angreifen. Antisatellitenwaffen, Täuschungs- und Abwehrtaktiken, Störsender, der Einsatz von Kleinsatelliten, Hacking und die Detonation von Atomwaffen sind nur einige Beispiele für bestehende Fähigkeiten, mit denen Weltraumsysteme und die dazugehörigen terrestrischen Anlagen gestört, blockiert oder physisch zerstört werden können.

Berichtsumfang zum Markt für elektronische Kriegsführung

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 21,74 Milliarden US-Dollar |

| Marktgröße bis 2034 | 34,44 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 5,25 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nach Komponente

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte im Bereich der elektronischen Kriegsführung: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für elektronische Kampfführung wächst rasant, angetrieben durch die steigende Nachfrage der Endnutzer. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Kundenbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

Neuigkeiten und aktuelle Entwicklungen im Bereich der elektronischen Kriegsführung

Der Markt für elektronische Kriegsführung wird anhand qualitativer und quantitativer Daten nach Primär- und Sekundärforschung analysiert. Zu den erhobenen Daten zählen wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken. Einige Entwicklungen im Bereich der elektronischen Kriegsführung sind nachfolgend aufgeführt:

Die US-Marine hat Raytheon, ein Unternehmen der RTX-Gruppe (NYSE: RTX), im Rahmen einer Vorauswahl einen Auftrag über 80 Millionen US-Dollar zur Entwicklung eines Prototyps für ein fortschrittliches elektronisches Kampfführungssystem (Advanced Electronic Warfare, ADVEW) für die F/A-18 E/F Super Hornet erteilt. Dieser Prototyp soll die bestehende integrierte elektronische Gegenmaßnahme AN/ALQ-214 und den Radarwarnempfänger AN/ALR-67(V)3 ersetzen und eine konsolidierte Lösung bieten, die dem Rückgrat der Flugzeugträgerstaffel der Marine überlegene Fähigkeiten zur elektronischen Kampfführung verleiht. (Quelle: Raytheon Technologies Corp., Pressemitteilung, Dez. 2023)

- L3Harris Technologies hat diesen Monat ein Angebot für die Ausschreibung der US Navy für den Next Generation Jammer – Low Band (NGJ-LB) eingereicht. L3Harris hatte den ursprünglichen Auftrag im Dezember 2020 mit einer technisch herausragenden Lösung gewonnen, was zu einem Protest eines Mitbewerbers führte. Das Programm umfasst die Entwicklung von Prototypen und die Lieferung taktischer Störsender zur Modernisierung der Fähigkeiten des EA-18G Growler im Bereich der elektronischen Kampfführung (EW). (Quelle: L3Harris Technologies, Pressemitteilung, August 2023)

Marktbericht Elektronische Kampfführung: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für elektronische Kriegsführung (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die folgende Bereiche abdeckt:

- Marktgröße und Prognose für die elektronische Kriegsführung auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt werden

- Trends im Markt für elektronische Kriegsführung sowie Marktdynamiken wie Treiber, Hemmnisse und wichtige Chancen

- Detaillierte Analyse der fünf Wettbewerbskräfte nach Porter

- Marktanalyse für elektronische Kriegsführung mit Fokus auf wichtige Markttrends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Rahmenbedingungen und aktuelle Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse mit Fokus auf Marktkonzentration, Heatmap-Analyse, prominente Akteure und aktuelle Entwicklungen im Markt für elektronische Kriegsführung

- Detaillierte Unternehmensprofile

Naveen ist ein erfahrener Marktforschungs- und Beratungsexperte mit über 9 Jahren Erfahrung in kundenspezifischen, syndizierten und Beratungsprojekten. In seiner aktuellen Funktion als Associate Vice President hat er erfolgreich Stakeholder entlang der gesamten Projektwertschöpfungskette gemanagt und ist Autor von über 100 Forschungsberichten und über 30 Beratungsaufträgen. Seine Arbeit erstreckt sich auf Industrie- und Regierungsprojekte und trägt maßgeblich zum Kundenerfolg und zur datengesteuerten Entscheidungsfindung bei.

Naveen hat einen Ingenieursabschluss in Elektronik und Kommunikation von der VTU, Karnataka, und einen MBA in Marketing und Operations von der Manipal University. Er ist seit 9 Jahren aktives IEEE-Mitglied und nimmt an Konferenzen und technischen Symposien teil und engagiert sich ehrenamtlich auf Sektions- und regionaler Ebene. Vor seiner aktuellen Position arbeitete er als Associate Strategic Consultant bei IndustryARC und als Industrial Server Consultant bei Hewlett Packard (HP Global).

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends