Markt für grünen Wasserstoff: Wichtige Unternehmen und SWOT-Analyse bis 2031

Historische Daten : 2021-2023 | Basisjahr : 2024 | Prognosezeitraum : 2025-2031Marktgröße und Prognose für grünen Wasserstoff (2021–2031), globaler und regionaler Marktanteil, Trend- und Wachstumspotenzialanalyse – Berichtsabdeckung: Nach Technologie (alkalische Elektrolyse und PEM-Elektrolyse), erneuerbarer Energiequelle (Windenergie, Solarenergie und Sonstige), Endverbrauchsbranche (Chemie, Energie, Lebensmittel und Getränke, Medizin, Petrochemie und Sonstige) und Geografie

- Status : Veröffentlicht

- Berichtscode : TIPRE00029371

- Kategorie : Energie und Leistung

- Anzahl der Seiten : 192

- Verfügbare Berichtsformate :

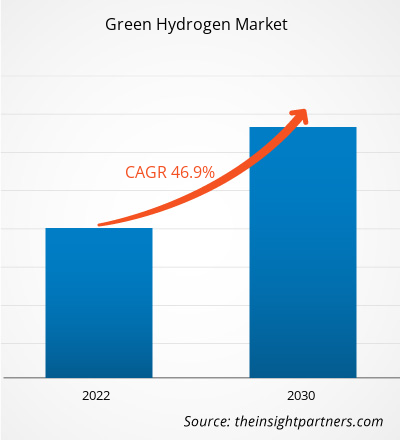

Der Markt für grünen Wasserstoff dürfte von 8,38 Milliarden US-Dollar im Jahr 2024 auf 71,31 Milliarden US-Dollar im Jahr 2031 wachsen; von 2025 bis 2031 wird eine durchschnittliche jährliche Wachstumsrate (CAGR) von 37,8 % erwartet. Die deutlich steigenden staatlichen Investitionen in erneuerbare Energien dürften ein wichtiger Trend auf dem Markt für grünen Wasserstoff bleiben.

Marktanalyse für grünen Wasserstoff

Regierungen weltweit erkennen die Vorteile von grünem Wasserstoff als saubere und nachhaltige Energielösung. Sie ergreifen proaktive Maßnahmen, um dessen Entwicklung und Einsatz in verschiedenen Sektoren zu unterstützen. Der zunehmende Fokus auf Dekarbonisierung und Klimaschutz veranlasst Regierungen, Investitionen in grünen Wasserstoff als Mittel zur Reduzierung der CO2-Emissionen zu priorisieren. So stellte beispielsweise Protium, eines der führenden Unternehmen für grüne Wasserstoffenergie in Großbritannien, im Juni 2022 durchgängige Netto-Null-Energielösungen bereit. Daher wird erwartet, dass steigende Investitionen in grüne Wasserstoffprojekte in den kommenden Jahren lohnende Möglichkeiten zur Marktexpansion schaffen.

Marktübersicht für grünen Wasserstoff

Elektrolyse dient zur Erzeugung von grünem Wasserstoff durch die Trennung von Wassermolekülen in Sauerstoff und Wasserstoff mithilfe von Elektrizität. Technologische Fortschritte in der Elektrolyse tragen dazu bei, die Effizienz, Wirtschaftlichkeit und Skalierbarkeit der Produktion, Speicherung und Nutzung von grünem Wasserstoff zu verbessern. Verbesserte Elektrolyseur-Designs, fortschrittliche Katalysatormaterialien und optimierte Betriebsbedingungen sind einige Faktoren, die zu höheren Energieumwandlungswirkungsgraden, kürzeren Reaktionszeiten und einer längeren Lebensdauer der Geräte führen können. Im Juli 2023 präsentierte das Korea Research Institute of Standards & Science (KRISS) eine potenzielle Lösung für den langlebigen und effizienten Ladungsträgertransport einer Photoanode mit Schutzfolie zur Entwicklung der Produktion von grünem Wasserstoff. Solche Fortschritte erweitern auch das Anwendungsspektrum von grünem Wasserstoff. Daher wird erwartet, dass technologische Fortschritte im Zusammenhang mit grünem Wasserstoff das Marktwachstum im Prognosezeitraum vorantreiben werden.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten

Markt für grünen Wasserstoff: Strategische Einblicke

-

Informieren Sie sich über die wichtigsten Markttrends in diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, von Markttrends bis hin zu Schätzungen und Prognosen.

Treiber und Chancen des Marktes für grünen Wasserstoff

Steigende Nachfrage nach FCEV begünstigt den Markt

Brennstoffzellen-Elektrofahrzeuge (FCEVs) nutzen Wasserstoff als Kraftstoff und erzeugen mithilfe von Brennstoffzellen Strom. Sie bieten eine saubere und leistungsstarke Alternative zu herkömmlichen Fahrzeugen mit Verbrennungsmotor. Da Länder bestrebt sind, ihre CO2-Emissionen zu reduzieren und auf kohlenstoffarme Mobilität umzusteigen, steigt die Nachfrage nach FCEVs weltweit. Daher engagieren sich verschiedene Marktteilnehmer in strategischen Entwicklungen wie Partnerschaften, Kooperationen und Vereinbarungen, um ihr Produktangebot zu erweitern und die wachsende Nachfrage nach FCEVs zu decken. Die Einführung von FCEVs treibt den Bedarf an grüner Wasserstoffproduktion voran, da dieser die primäre Kraftstoffquelle dieser Fahrzeuge darstellt.

Zunehmende Errichtung großer Anlagen zur Erzeugung von grünem Wasserstoff – eine Chance auf dem Markt für grünen Wasserstoff

Der Bau großer Anlagen zur Erzeugung von grünem Wasserstoff zieht erhebliche Investitionen sowohl aus dem öffentlichen als auch aus dem privaten Sektor an. Im Juni 2023 kündigte eine Unternehmensgruppe an, 79,75 US-Dollar in ein Projekt zur Erweiterung einer Wasserstoffproduktionsanlage und einer Wasserstoffverflüssigungsanlage in Queensland, Australien, zu investieren. Zu der Unternehmensgruppe gehören die Kansai Electric Power Company (Japan), die Marubeni Corporation (Japan), die Iwatani Corporation (Japan), die Keppel Infrastructure (Singapur) und die Stanwell Corporation (Australien). Der verstärkte Infrastrukturausbau dürfte ein positives Umfeld für die Einführung von grünem Wasserstoff in verschiedenen Sektoren schaffen und den Marktteilnehmern im Prognosezeitraum voraussichtlich Wachstumsaussichten bieten.

Segmentierungsanalyse des Marktberichts für grünen Wasserstoff

Wichtige Segmente, die zur Ableitung der Marktanalyse für grünen Wasserstoff beigetragen haben , sind Technologie, erneuerbare Quellen und Endverbrauch.

- Basierend auf der Technologie wurde der Markt für grünen Wasserstoff in alkalische Elektrolyse und PEM-Elektrolyse unterteilt. Das Segment der alkalischen Elektrolyse hatte im Jahr 2022 einen größeren Marktanteil.

- Im Hinblick auf erneuerbare Energien wurde der Markt in Windenergie, Solarenergie und andere segmentiert. Das Segment Solarenergie dominierte den Markt im Jahr 2022.

- In Bezug auf die Endverbrauchsindustrie wurde der Markt in die Branchen Chemie, Energie, Lebensmittel und Getränke, Medizin, Petrochemie und andere segmentiert. Das Energiesegment dominierte den Markt im Jahr 2022.

Analyse der Marktanteile von grünem Wasserstoff nach geografischen Gesichtspunkten

Der geografische Umfang des Marktberichts für grünen Wasserstoff ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Südamerika/Süd- und Mittelamerika.

Europa ist führend auf dem Markt für grünen Wasserstoff. Mehrere europäische Länder, darunter Spanien, Frankreich, Deutschland und Portugal, haben Schritte unternommen, um zusammenzuarbeiten und bis 2030 eine Wasserstoffpipeline zu bauen. Diese Pipeline wird den Transport von jährlich ca. 2 Millionen Tonnen Wasserstoff von diesen Ländern nach Frankreich ermöglichen. Da Europa seine Energieversorgung sichern und den Übergang zu einer kohlenstoffneutralen Zukunft beschleunigen möchte, erweist sich grüner Wasserstoff als unverzichtbare Ressource und Schlüssellösung, um die Abhängigkeit von fossilen Brennstoffen zu reduzieren und ehrgeizige Klimaziele zu erreichen. Deutschland, Frankreich, Italien und Großbritannien gehören zu den führenden Ländern auf dem Markt für grünen Wasserstoff in Europa. Die deutsche Regierung hat bereits Schritte zur Förderung der Wasserstoffwirtschaft unternommen, darunter die Verabschiedung einer Nationalen Wasserstoffstrategie. So kündigte Deutschland im März 2022 an, 572 Millionen US-Dollar zu einer neuen globalen grünen Wasserstoffwirtschaft beizutragen. Dies ist ein wichtiger Schritt, um die Einführung und Entwicklung sauberer Energielösungen weltweit zu fördern.

Regionale Einblicke in den Markt für grünen Wasserstoff

Die Analysten von Insight Partners haben die regionalen Trends und Faktoren, die den Markt für grünen Wasserstoff im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage in Nordamerika, Europa, Asien-Pazifik, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Markt für grünen Wasserstoff

Umfang des Marktberichts über grünen Wasserstoff

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2024 | 8,38 Milliarden US-Dollar |

| Marktgröße bis 2031 | 71,31 Milliarden US-Dollar |

| Globale CAGR (2025 – 2031) | 37,8 % |

| Historische Daten | 2021-2023 |

| Prognosezeitraum | 2025–2031 |

| Abgedeckte Segmente |

Nach Technologie

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte für grünen Wasserstoff: Auswirkungen auf die Geschäftsdynamik

Der Markt für grünen Wasserstoff wächst rasant. Die steigende Endverbrauchernachfrage ist auf Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile zurückzuführen. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Verbraucherbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte beschreibt die Verteilung der in einem bestimmten Markt oder einer bestimmten Branche tätigen Unternehmen. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu dessen Größe oder Gesamtmarktwert präsent sind.

Die wichtigsten Unternehmen, die auf dem Markt für grünen Wasserstoff tätig sind, sind:

- Air Liquide

- Siemens Energy

- Cummins Inc.

- Linde Plc

- NEL ASA

- ?rsted A/S

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für grünen Wasserstoff

Neuigkeiten und aktuelle Entwicklungen zum Markt für grünen Wasserstoff

Der Markt für grünen Wasserstoff wird durch die Erhebung qualitativer und quantitativer Daten aus Primär- und Sekundärforschung bewertet, die wichtige Unternehmenspublikationen, Verbandsdaten und Datenbanken umfasst. Im Folgenden finden Sie eine Liste der Entwicklungen im Markt für Innovationen, Geschäftserweiterungen und Strategien:

- Im Oktober 2022 unterzeichneten NTPC und Siemens Ltd. eine Absichtserklärung (MoU) zur Demonstration der Mitverbrennung von Wasserstoff mit Erdgas in Siemens V94.2-Gasturbinen im NTPC-Gaskraftwerk Faridabad. (Quelle: Siemens Ltd., Pressemitteilung/Unternehmenswebsite/Newsletter)

- Im Dezember 2022 lieferte Cummins Inc. ein 35-Megawatt-Protonenaustauschmembran-Elektrolyseursystem (PEM) für Lindes neue Wasserstoffproduktionsanlage in Niagara Falls, New York. (Quelle: Cummins Inc., Pressemitteilung/Unternehmenswebsite/Newsletter)

Marktbericht zu grünem Wasserstoff – Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für grünen Wasserstoff (2020–2030)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Marktgröße und Prognose für grünen Wasserstoff auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt sind

- Marktdynamik wie Treiber, Hemmnisse und wichtige Chancen

- Markttrends für grünen Wasserstoff

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für grünen Wasserstoff mit wichtigen Markttrends, globalen und regionalen Rahmenbedingungen, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Markt für grünen Wasserstoff: Branchen-, Landschafts- und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und jüngsten Entwicklungen

- Detaillierte Firmenprofile

Nivedita ist eine versierte Forschungsexpertin mit über 9 Jahren Erfahrung in Marktforschung und Unternehmensberatung. Sie ist derzeit als Projektmanagerin im IKT-Bereich bei The Insight Partners tätig und verfügt über umfassende Fachkenntnisse in der Leitung und Durchführung von syndizierten, kundenspezifischen, abonnementbasierten und beratenden Forschungsaufträgen in unterschiedlichen Technologiesektoren.

Mit einer nachgewiesenen Erfolgsbilanz bei der Bereitstellung datengestützter Analysen und umsetzbarer Erkenntnisse war Nivedita maßgeblich an mehreren kritischen Projekten beteiligt. Ihre Arbeit umfasst die vollständige Projektabwicklung – vom Verständnis der Kundenziele über die Analyse von Markttrends bis hin zur Ableitung strategischer Empfehlungen. Sie hat umfassend mit führenden IKT-Unternehmen zusammengearbeitet und ihnen geholfen, Marktchancen zu erkennen und Branchenveränderungen zu meistern.

Nivedita hat einen MBA in Management vom IMS, Dehradun. Vor ihrem Eintritt bei The Insight Partners sammelte sie wertvolle Erfahrungen bei MarketsandMarkets und Future Market Insights in Pune, wo sie verschiedene Forschungspositionen innehatte und sich ein solides Fundament in Branchenanalyse und Kundenbindung erarbeitete.

- Historische Analyse (2 Jahre), Basisjahr, Prognose (7 Jahre) mit CAGR

- PEST- und SWOT-Analyse

- Marktgröße Wert/Volumen – Global, Regional, Land

- Branchen- und Wettbewerbslandschaft

- Excel-Datensatz

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends

Exklusive Berichtsrabatte freischalten

Jetzt anfragen

Kostenlose Probe anfordern für - Markt für grünen Wasserstoff

Kostenlose Probe anfordern für - Markt für grünen Wasserstoff