Marktübersicht zum Wachstum des Marktes für neonatale Versorgungsgeräte bis 2034

Marktgröße und Prognose für neonatale Pflegegeräte (2021–2034), globaler und regionaler Marktanteil, Trends und Wachstumspotenzialanalyse. Berichtsabdeckung: Nach Produkt (Wärmebetten für Säuglinge, Inkubatoren für Neugeborene, Kombi-Wärmebetten und -Inkubatoren, Phototherapiegeräte für Neugeborene, Geräte für die Beatmungstherapie, Überwachungsgeräte für Neugeborene, Geräte für die neonatale Bildgebung, Pflegegeräte); Endnutzer (Krankenhäuser, Kinder- und Neonatologiekliniken); und Region

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00029525

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : January 27, 2026

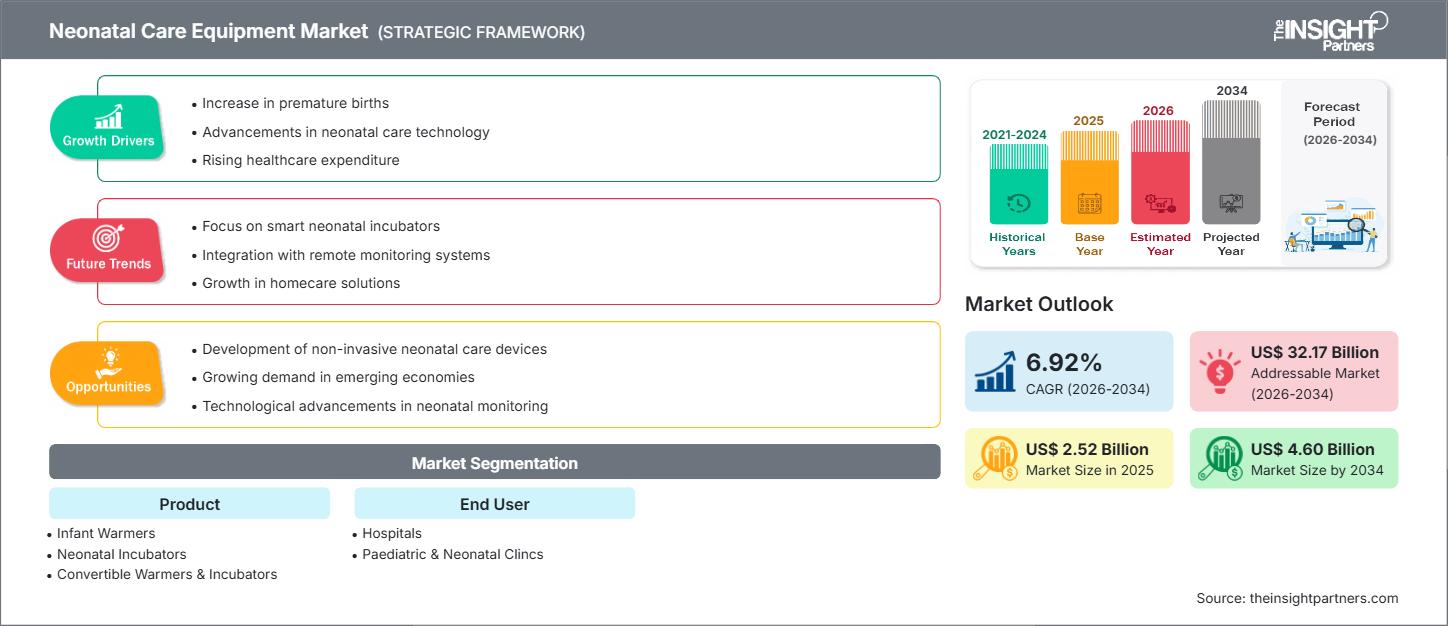

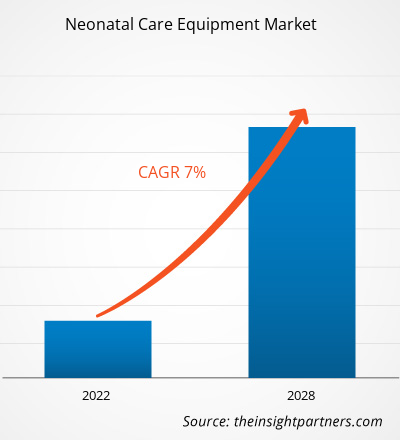

Der Markt für Ausrüstung zur Neugeborenenversorgung wird bis 2034 voraussichtlich ein Volumen von 4,60 Milliarden US-Dollar erreichen, gegenüber 2,52 Milliarden US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Zeitraum 2026–2034 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 6,92 % verzeichnen wird.

Marktanalyse für Ausrüstung zur Neugeborenenversorgung

Der Markt für neonatale Versorgungsgeräte wächst stetig, vor allem aufgrund der weltweit steigenden Zahl von Frühgeburten und der zunehmenden Häufigkeit von Komplikationen bei Neugeborenen wie Gelbsucht und Unterkühlung. Diese Faktoren treiben die Nachfrage nach Spezialgeräten wie Inkubatoren, Phototherapiegeräten und Beatmungssystemen auf neonatologischen Intensivstationen (NICUs) an. Technologische Fortschritte, darunter die Integration KI-gestützter Analysen, nicht-invasiver Überwachung und tragbarer Geräte, verbessern die Präzision und Qualität der Versorgung deutlich. Regierungen und Gesundheitsorganisationen weltweit konzentrieren sich verstärkt auf die Senkung der Säuglingssterblichkeit durch Investitionen in die NICU-Infrastruktur und spezialisierte Schulungen, insbesondere in Schwellenländern. Das Marktwachstum wird zudem durch steigende Gesundheitsausgaben und die Entwicklung moderner, integrierter neonataler Arbeitsstationen unterstützt.

Marktübersicht für Ausrüstung zur Neugeborenenversorgung

Neonatale Pflegegeräte umfassen spezialisierte medizinische Geräte und Technologien, die die Gesundheit und das Überleben von Neugeborenen, insbesondere von Frühgeborenen oder schwerkranken Kindern, unterstützen. Diese Geräte sind unerlässlich für die Aufrechterhaltung einer stabilen, lebensnotwendigen Umgebung und beinhalten Systeme zur Wärmeregulierung, Atemunterstützung, Überwachung und Behandlung von Neugeborenengelbsucht. Hauptziel dieser Geräte ist die Behandlung kritischer Zustände wie Atemnot, Unterkühlung und Neugeborenengelbsucht, um die Behandlungsergebnisse für die Patienten zu verbessern. Technologische Innovationen konzentrieren sich auf die Entwicklung nicht-invasiver, schonender und hochpräziser Überwachungs- und Behandlungssysteme, die für die sensible Neugeborenenpflege von entscheidender Bedeutung sind. Der steigende Bedarf ist besonders in Krankenhäusern und spezialisierten Geburtskliniken spürbar, wo eine hochspezialisierte Versorgung erforderlich ist.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für Ausrüstung zur Neugeborenenversorgung: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen im Bereich Ausrüstung für die Neugeborenenversorgung

Markttreiber:

- Zunehmende Häufigkeit von Frühgeburten und niedrigem Geburtsgewicht: Weltweit steigende Raten von Frühgeborenen und untergewichtigen Babys erfordern eine verlängerte, spezialisierte Betreuung auf neonatologischen Intensivstationen, was die Nachfrage nach fortschrittlichen neonatalen Geräten wie Inkubatoren und Beatmungsgeräten direkt antreibt.

- Technologische Fortschritte bei Geräten für die Säuglingspflege: Kontinuierliche Innovationen, darunter die Entwicklung von KI-integrierten Monitoren, intelligenten Inkubatoren (z. B. geschlossenen doppelwandigen Systemen) und nicht-invasiven Beatmungsgeräten, verbessern die Präzision der Pflege und die Behandlungsergebnisse und beschleunigen die Markteinführung.

- Zunehmende Investitionen von Regierung und Gesundheitswesen in die Infrastruktur von Neonatologie-Intensivstationen: Regierungsinitiativen und Fördermittel in verschiedenen Ländern, insbesondere in Entwicklungsländern wie Indien und China, konzentrieren sich auf die Einrichtung und Modernisierung von Neonatologie-Intensivstationen, um die Säuglingssterblichkeit zu senken und die Beschaffung von hochmoderner neonataler Ausrüstung zu erhöhen.

Marktchancen:

- Integration von KI und nicht-invasiven Technologien: Die Chance liegt in der Entwicklung KI-gestützter prädiktiver Analysetools zur Früherkennung von Krankheiten und der Erweiterung nicht-invasiver Behandlungsmöglichkeiten, um Risiken zu reduzieren und die Ergebnisse zu verbessern.

- Marktchancen in Schwellenländern: Entwicklungsländer in den Regionen Asien-Pazifik (APAC) und Naher Osten & Afrika (MEA) bieten aufgrund hoher Geburtenraten, einer sich ausweitenden Gesundheitsinfrastruktur und eines zunehmenden Fokus der Regierungen auf die Mütter- und Kindergesundheit ein erhebliches Wachstumspotenzial, wodurch eine Nachfrage nach kosteneffektiven und skalierbaren Lösungen entsteht.

- Entwicklung tragbarer Geräte und Geräte für die häusliche Pflege: Der Wandel hin zu kontinuierlicher Überwachung und häuslicher Pflege für stabile Säuglinge schafft ein großes Potenzial für tragbare/transportable Geräte und am Körper tragbare Überwachungsgeräte für Neugeborene, unterstützt durch Telemedizinlösungen.

Marktbericht: Segmentierungsanalyse für Ausrüstung zur Neugeborenenversorgung

Der Markt für neonatale Pflegegeräte wird in verschiedenen Segmenten analysiert, um ein besseres Verständnis seiner Struktur, seines Wachstumspotenzials und der aufkommenden Trends zu ermöglichen.

Nach Produkt:

- Babywärmer

- Neugeborenen-Inkubatoren

- Konvertierbare Wärmeschränke und Inkubatoren

- Phototherapiegeräte für Neugeborene

- Geräte zur Atemtherapie

- Neonatale Überwachungsgeräte

- Neonatale diagnostische Bildgebungsgeräte

- Pflegeausrüstung

Vom Endbenutzer:

- Krankenhäuser

- Pädiatrische und neonatale Kliniken

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Süd- und Mittelamerika

- Naher Osten und Afrika

Markt für Ausrüstung zur Neugeborenenversorgung – Regionale Einblicke

Die regionalen Trends und Einflussfaktoren auf den Markt für neonatale Pflegegeräte im gesamten Prognosezeitraum wurden von den Analysten von The Insight Partners eingehend erläutert. Dieser Abschnitt behandelt außerdem die Marktsegmente und die geografische Verteilung des Marktes für neonatale Pflegegeräte in Nordamerika, Europa, Asien-Pazifik, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika.

Umfang des Marktberichts zu Geräten für die Neugeborenenversorgung

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 2,52 Milliarden US-Dollar |

| Marktgröße bis 2034 | 4,60 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 6,92 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nebenprodukt

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte der Akteure im Markt für neonatale Versorgungsgeräte: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für neonatale Pflegegeräte wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile der Produkte. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen für die Bedürfnisse der Verbraucher und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

- Verschaffen Sie sich einen Überblick über die wichtigsten Akteure auf dem Markt für neonatale Pflegeausrüstung.

Marktanteilsanalyse für Ausrüstung zur Neugeborenenversorgung nach Regionen

Nordamerika dominiert derzeit den Markt für neonatale Versorgungstechnik und erzielt den größten Umsatzanteil. Der asiatisch-pazifische Raum dürfte der am schnellsten wachsende regionale Markt sein. Der Nahe Osten und Afrika sowie Süd- und Mittelamerika bieten erhebliches Wachstumspotenzial, da die digitale Transformation und nationale Gesundheitsstrategien auf die Senkung der Säuglingssterblichkeit abzielen und somit den Bedarf an skalierbaren und kostengünstigen neonatalen Lösungen steigern.

Nordamerika

- Marktanteil: Besitzt den größten Marktanteil, was auf eine robuste, gut etablierte Gesundheitsinfrastruktur mit einem dichten Netz von hochmodernen Neonatologie-Intensivstationen und hohen Gesundheitsausgaben zurückzuführen ist.

- Wichtigste Einflussfaktoren: Hohe Akzeptanz von fortschrittlichen, technologisch hochentwickelten Geräten; Präsenz führender Medizinproduktehersteller; und erhebliche private und staatliche Investitionen in die Mütter- und Kindergesundheit.

- Trends: Frühe Einführung von KI-gestützter prädiktiver Analytik und integrierten High-End-NICU-Workstations.

Europa

- Marktanteil: Hält einen bedeutenden Marktanteil, was auf den Fokus auf Patientensicherheit und die Präsenz großer Medizintechnikunternehmen zurückzuführen ist.

- Wichtigste Einflussfaktoren: Strenge regulatorische Standards für Medizinprodukte; öffentlich-private Partnerschaften zur Verbesserung der Infrastruktur für die Neugeborenenversorgung; und Nachfrage nach fortschrittlichen Systemen zur Beatmungsunterstützung und -überwachung.

- Trends: Zunahme nicht-invasiver Beatmungstechniken und Fokus auf ergonomisches, benutzerfreundliches Gerätedesign.

Asien-Pazifik

- Marktanteil: Es wird erwartet, dass es sich um den am schnellsten wachsenden regionalen Markt handelt, angetrieben durch die rasch expandierende Kapazität der Neonatologie und die hohen Geburtenraten.

- Wichtigste Einflussfaktoren: Staatlich unterstützte Initiativen zur Verbesserung der Säuglingssterblichkeitsrate (z. B. Ausbau der Spezialstationen für Neugeborene in Indien); steigende Investitionen im Gesundheitswesen; und zunehmendes Bewusstsein für die Gesundheit von Neugeborenen.

- Trends: Starke Nachfrage nach kosteneffektiven, skalierbaren Lösungen und der Integration grundlegender KI-Analysen für die lokale Plattformüberwachung und Früherkennung.

Süd- und Mittelamerika

- Marktanteil: Aufstrebende Region mit zunehmender Akzeptanz.

- Wichtigste Einflussfaktoren: Zunehmender Fokus auf digitales Marketing und E-Commerce im gesamten Gesundheitswesen; schrittweise Modernisierung der digitalen Gesundheitsinfrastruktur.

- Trends: Ausbau kostengünstiger, cloudbasierter Monitoring-Lösungen und Entwicklung automatisierter Tools für die mehrsprachige Kommunikation.

Naher Osten und Afrika

- Marktanteil: Aufstrebender Markt mit starkem Wachstumspotenzial, angeführt von Initiativen zur digitalen Transformation in Ländern wie den Vereinigten Arabischen Emiraten und Saudi-Arabien.

- Wichtigste Einflussfaktoren: Umfassende nationale Digitalisierungs- und KI-Strategien; zunehmende Integration von Community-Management-Systemen und klinischer Entscheidungsunterstützung.

- Trends: KI-gestütztes Tracking der Publikumsstimmung, Aufdeckung von Influencer-Betrug und mehrsprachige Inhaltsmoderation durch maschinelles Lernen.

Marktdichte der Akteure im Markt für neonatale Versorgungsgeräte: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für neonatale Versorgungsgeräte ist stark konsolidiert, wobei führende globale Medizintechnikkonzerne einen bedeutenden Marktanteil halten. Der Wettbewerb wird durch Innovationen in den Bereichen Konnektivität, Präzision und Benutzerfreundlichkeit angetrieben und zwingt die Anbieter, fortschrittliche Technologien in ihre Produkte zu integrieren.

Der Wettbewerb zwingt die Anbieter dazu, sich durch Folgendes zu differenzieren:

- Die Hersteller integrieren mehrere Funktionen (Wärme, Überwachung, Beatmung) in einzelne, einheitliche Arbeitsplätze für die Neonatologie, um den Arbeitsablauf und die Patientensicherheit zu verbessern.

- Zu den Lösungen gehören heute KI-Algorithmen für prädiktive Analysen, Echtzeit-Überwachung der Vitalfunktionen und klinische Entscheidungsunterstützung zur Förderung frühzeitiger Interventionen.

- Als Reaktion auf die Nachfrage aus Schwellenländern entwickeln die Anbieter kostengünstige und robuste Geräte, die für ressourcenarme Umgebungen geeignet sind.

Chancen und strategische Schritte

- Fokus auf nicht-invasive und tragbare Lösungen: Unternehmen investieren stark in die Entwicklung kleiner, nicht-invasiver und tragbarer Monitore und Phototherapiegeräte, um sowohl den innerklinischen Transport als auch den wachsenden Bereich der häuslichen Pflege zu unterstützen.

- Strategische Akquisitionen und Kooperationen: Große Unternehmen übernehmen spezialisierte Technologie-Startups, die sich auf KI/ML und Sensortechnologie konzentrieren, oder gehen Partnerschaften mit ihnen ein, um neue, fortschrittliche Funktionen schnell in ihre Produktportfolios zu integrieren.

- Schwerpunkt auf Service und Schulung: Die Anbieter differenzieren sich durch umfassende Kundendienstleistungen, Wartungsverträge und spezialisierte Schulungsprogramme für das Personal der Neonatologie-Intensivstation, insbesondere in Regionen mit einem Mangel an geschultem Personal.

Die wichtigsten Unternehmen auf dem Markt für Ausrüstung zur Neugeborenenversorgung sind:

- GE Healthcare

- Koninklijke Philips NV

- Medtronic

- Drägerwerk AG & Co. KGaA

- Nihon Kohden Corporation

- Natus Medical Incorporated

- Fisher & Paykel Healthcare Limited.

- Masimo

- BD

Hinweis: Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge geordnet.

Neuigkeiten und aktuelle Entwicklungen auf dem Markt für Geräte zur Neugeborenenversorgung

- Beispielsweise erweitert Dräger am 24. März 2025 sein Portfolio im Bereich der Neonatologie mit der Einführung von BiliPredics, einer prädiktiven Softwarelösung von NeoPredics zur Vorhersage des dynamischen Bilirubinverlaufs. Mithilfe eines klinisch validierten Algorithmus ermöglicht BiliPredics medizinischem Fachpersonal, den Bilirubinverlauf bis zu 60 Stunden im Voraus zu prognostizieren und so zeitnahe und fundierte klinische Entscheidungen zu unterstützen.

- Das All India Institute of Medical Sciences (AIIMS) in Neu-Delhi unterzeichnete im Dezember 2024 eine Absichtserklärung mit Wipro GE Healthcare Pvt Ltd, einem weltweit führenden Anbieter von Gesundheitstechnologien, zur Einrichtung eines KI-gestützten Innovationszentrums für das Gesundheitswesen. Dieses Zentrum wird sich auf die Entwicklung von Produkten und Lösungen konzentrieren, die das Potenzial haben, die Gesundheitsversorgung und -ergebnisse durch präzisere Diagnostik, innovative Behandlungsprotokolle und die Echtzeit-Erfassung von Patientendaten zu verbessern.

- Im Dezember 2023 gab Masimo, ein weltweit führender Anbieter innovativer Überwachungstechnologien für Top-Krankenhäuser, die FDA-Zulassung für Stork bekannt, ein revolutionäres Babyüberwachungssystem zur rezeptpflichtigen Anwendung bei gesunden und kranken Babys im Alter von 0 bis 18 Monaten.

Marktbericht zu Geräten für die Neugeborenenversorgung: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für Geräte zur Neugeborenenversorgung (2021–2034)“ bietet eine detaillierte Analyse des Marktes, die folgende Bereiche abdeckt:

- Marktgröße und Prognose für Ausrüstung zur neonatalen Versorgung auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt werden

- Markttrends für Ausrüstung zur Neugeborenenversorgung sowie Marktdynamiken wie Treiber, Hemmnisse und wichtige Chancen

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für neonatale Pflegegeräte: Wichtige Markttrends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Rahmenbedingungen und aktuelle Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse mit Fokus auf Marktkonzentration, Heatmap-Analyse, führende Akteure und aktuelle Entwicklungen im Markt für neonatale Pflegegeräte. Ausführliche Unternehmensprofile.

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends