Marktgröße, Wachstum und Trends für ultradünnes Glas bis 2034

Marktgröße und Prognosen für ultradünnes Glas (2021–2034), globaler und regionaler Marktanteil, Trends und Wachstumspotenzialanalyse. Berichtsabdeckung: Nach Herstellungsverfahren (Float- und Fusionsglas), Anwendung (Halbleitersubstrat, Flachbildschirme und Touch-Bedienelemente, Automobilverglasung und Sonstiges), Endverbrauchsbranche (Unterhaltungselektronik, Automobilindustrie, Medizin und Gesundheitswesen und Sonstiges) und Region

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00009965

- Kategorie : Chemikalien und Materialien

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 11, 2026

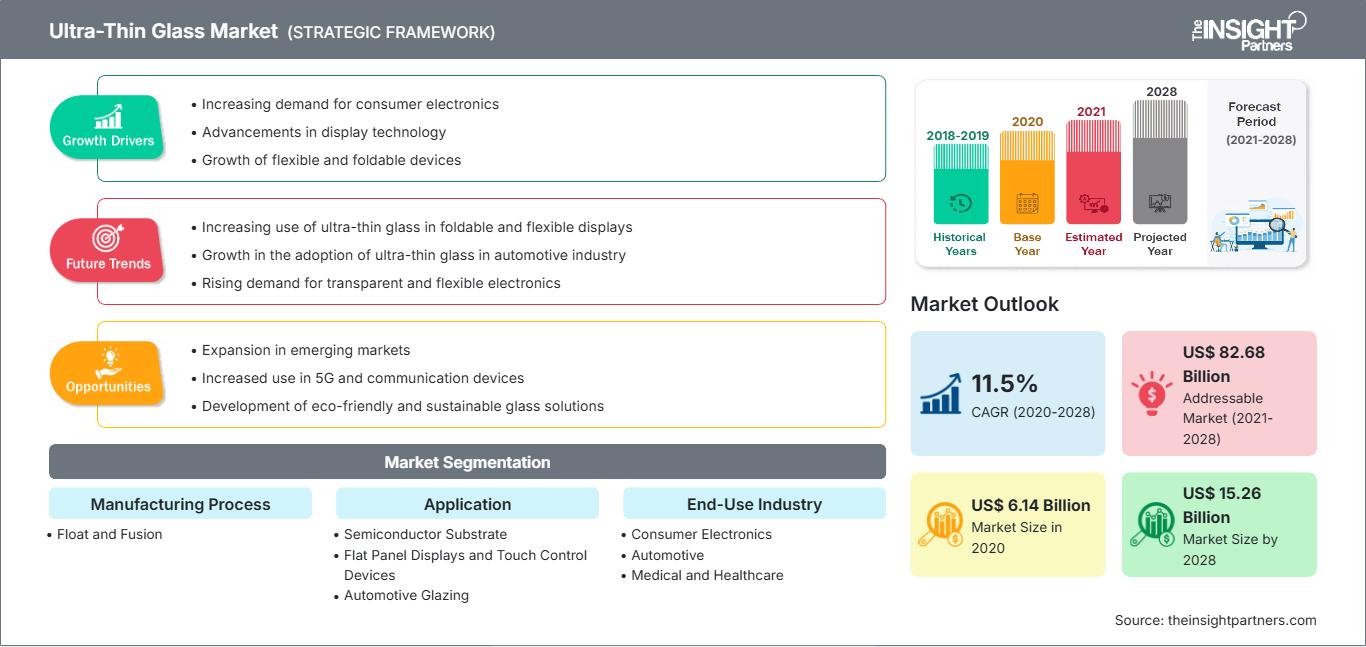

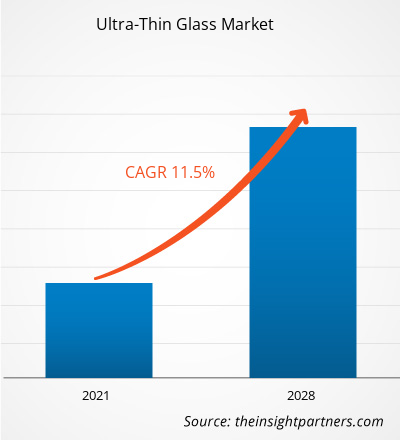

Der globale Markt für ultradünnes Glas wird bis 2034 voraussichtlich ein Volumen von 55,85 Milliarden US-Dollar erreichen, gegenüber 23,44 Milliarden US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Prognosezeitraum 2026–2034 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 10,13 % verzeichnen wird.

Zu den wichtigsten Marktdynamiken zählen der weltweit zunehmende Fokus auf leichte und leistungsstarke elektronische Bauteile, das steigende Bewusstsein der Verbraucher für die überlegene Haltbarkeit und Kratzfestigkeit von Glas gegenüber Kunststoffpolymeren sowie der deutliche Trend hin zu faltbaren und flexiblen Gerätearchitekturen. Darüber hinaus dürfte der Markt von der wachsenden Beliebtheit von Elektrofahrzeugen mit integrierten Smart Cockpits, den steigenden Anforderungen an Halbleitergehäuse für 5G- und KI-Hardware sowie dem zunehmenden Einsatz von ultradünnem Glas in hochwertigen medizinischen Segmenten wie diagnostischen Biosensoren und tragbaren Gesundheitsmonitoren profitieren.

Marktanalyse für ultradünnes Glas

Die Marktanalyse für ultradünnes Glas zeigt eine Verlagerung hin zu hochwertigen Funktionssubstraten, da Hersteller optische Klarheit und mechanische Flexibilität priorisieren. Der Markt diversifiziert sich in die traditionellen, vom Floatglas geprägten Bereiche Automobil und Display sowie in wachstumsstarke Märkte für das Schmelzziehverfahren zur Herstellung hochwertiger faltbarer Elektronik. Strategische Chancen eröffnen sich in Spezialanwendungen der Halbleiter- und Biotechnologie, wo die überlegene thermische Stabilität und chemische Beständigkeit von ultradünnem Glas im Vergleich zu organischen Alternativen einen klaren Wettbewerbsvorteil bietet. Die Marktexpansion hängt von der Ausbeuteoptimierung beim Präzisionsschneiden und der Zuverlässigkeit automatisierter Handhabungssysteme für die extrem empfindlichen Glasscheiben ab. Wettbewerbsdifferenzierung ergibt sich heute vor allem durch proprietäre Härtungstechniken wie die chemische Ionenaustauschhärtung und die Möglichkeit, multifunktionale Beschichtungen für Antireflexion und Fingerabdruckresistenz anzubieten. Dieser Ansatz ermöglicht es führenden Glasherstellern, in einem Markt, der höchste technische Präzision erfordert, höhere Preise zu erzielen.

Marktübersicht für ultradünnes Glas

Ultradünnes Glas hat sich von Nischenanwendungen im Labor zu gängigen Hightech-Industrieprodukten entwickelt. Der Markt umfasst ultraflexibles Deckglas für Smartphones, Hochfrequenzsubstrate für Chipgehäuse und Leichtbauverglasungen für die Luft- und Raumfahrt- sowie die Automobilindustrie. Globale Glaskonzerne und spezialisierte Materialwissenschaftsunternehmen konkurrieren in diesem Markt und nutzen fortschrittliche Fertigungstechniken, um Glas herzustellen, das dünner als ein menschliches Haar ist. Die steigende Nachfrage nach schlankerer und tragbarerer Elektronik bei technikaffinen Verbrauchern im asiatisch-pazifischen Raum und in Nordamerika hat die Beliebtheit von ultradünnem Glas als erstklassige Schutz- und Schnittstellenlösung erhöht. Der asiatisch-pazifische Raum ist aufgrund seines etablierten Zentrums für die Elektronikfertigung umsatzstärkster Markt, während Nordamerika in der Luft- und Raumfahrt sowie bei Innovationen in der Medizintechnik Fortschritte erzielt. Der Weltmarkt ist in Regionen mit hoher Konzentration an Displaypanel-Produktion am weitesten entwickelt, angetrieben durch die breite Verfügbarkeit von OLED- und Micro-LED-Technologien. Der Wettbewerb zwischen den Marken fördert Innovationen in der Glaszusammensetzung und führt zur Entwicklung spezieller Aluminosilikat- und Borosilikatvarianten. Der US-Markt ist ein zentraler Knotenpunkt für Materialinnovationen, gestützt durch ein starkes Halbleiter-Ökosystem und eine hohe Dichte an großen Herstellern von Unterhaltungselektronik. Die Inlandsnachfrage konzentriert sich zunehmend auf faltbare Bauformen und fortschrittliche Halbleitergehäuse. Strategische Investitionen in lokale Fertigungsanlagen fördern die Verbreitung hochpräziser Glassubstrate.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für ultradünnes Glas: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen für ultradünnes Glas

Markttreiber:

- Überragende optische und mechanische Eigenschaften: Ultradünnes Glas bietet eine höhere Transparenz und eine hochwertigere Haptik als Kunststofffolien. Seine Beständigkeit gegenüber Hitze und Chemikalien macht es ideal für die anspruchsvollen Fertigungsprozesse moderner hochauflösender Displays.

- Die zunehmende Verbreitung faltbarer Geräte: Die wachsende Nachfrage nach faltbaren Smartphones und Laptops sorgt für eine anhaltend hohe Nachfrage nach flexiblen Glaskomponenten. Da Verbraucher vermehrt auf flexible Geräte umsteigen, verzeichnet ultradünnes Glas weiterhin stetige Absatzsteigerungen gegenüber Polyimid-Kunststoffen.

- Rasante Verbreitung von 5G und Halbleitertechnologien: Hochfrequente Datenübertragung erfordert Substrate mit geringen dielektrischen Verlusten. Ultradünnes Glas wird zunehmend in fortschrittlichen Halbleitergehäusen eingesetzt, um die Infrastruktur von 5G und Hochleistungsrechnern zu unterstützen.

Marktchancen:

- Expansion in die Bereiche Fahrzeugverglasung und intelligente Innenausstattung: Neben mobilen Endgeräten bietet ultradünnes Glas bedeutende Möglichkeiten bei leichten Fenstern und großflächigen, gebogenen Armaturenbrettdisplays für Elektrofahrzeuge der nächsten Generation.

- Wachstum in den Bereichen Medizin und Biotechnologie: Die Bildung strategischer Partnerschaften zwischen Glasherstellern und Medizintechnikunternehmen kann den Zugang zu margenstarken Segmenten in der patientennahen Diagnostik erleichtern, wo ultradünnes Glas als stabiles Substrat für mikrofluidische Chips dient.

- Diversifizierung hin zu nachhaltiger Energie: Für Hersteller bietet sich eine wachsende Chance, den Sektor der erneuerbaren Energien durch leichtes, flexibles Glas für gebäudeintegrierte Photovoltaik (BIPV) und tragbare Solarladegeräte ins Visier zu nehmen.

Marktbericht für ultradünnes Glas: Segmentierungsanalyse

Der Marktanteil von ultradünnem Glas wird in verschiedenen Segmenten analysiert, um ein besseres Verständnis seiner Struktur, seines Wachstumspotenzials und der sich abzeichnenden Trends zu ermöglichen. Nachfolgend ist der in den meisten Branchenberichten verwendete Standard-Segmentierungsansatz dargestellt:

Nach Herstellungsprozess:

- Floatglas: Der dominierende Volumentreiber, insbesondere in den Bereichen Automobilverglasung und großflächige Displays, aufgrund etablierter Produktionskapazitäten für große Stückzahlen und Kosteneffizienz bei der Herstellung von Glasdicken bis hinunter zu 0,1 mm.

- Fusion: Ein schnell wachsendes Technologiesegment, das Glas mit überragender Oberflächenqualität und präziser Dickenkontrolle herstellt. Es wird zunehmend für hochwertige Elektronikanwendungen eingesetzt, bei denen makellose, berührungsempfindliche Oberflächen ohne zusätzliches Polieren erforderlich sind.

Auf Antrag:

- Flachbildschirme und Touch-Bedienelemente: Bleiben der Hauptabsatzkanal für ultradünnes Glas und profitieren von der weltweiten Nachfrage nach Smartphones, Tablets und High-End-Fernsehern.

- Halbleitersubstrat: Das am schnellsten wachsende Anwendungssegment, insbesondere für hochdichte Chipgehäuse und Interposer, ermöglicht kompaktere und effizientere elektronische Bauteile.

- Automotive Glazing: Bietet eine ausgewählte, aber stetig wachsende Palette von Anwendungen zur Gewichtsreduzierung und ästhetischen Aufwertung des Fahrzeuginnenraums im modernen Fahrzeugdesign.

- Sonstige: Dazu gehören Nischenanwendungen in Sensoren, biotechnologischen Substraten und Solarenergiekomponenten.

Nach Endverbrauchsbranche:

- Unterhaltungselektronik: Der größte Sektor, angetrieben durch den kontinuierlichen Zyklus der Geräteminiaturisierung und den Aufstieg der faltbaren Bildschirmtechnologie.

- Automobilindustrie: Ein bedeutender Wachstumsbereich mit Fokus auf die Reduzierung des Fahrzeugleergewichts und die Förderung der Digitalisierung des Fahrzeuginnenraums.

- Medizin und Gesundheitswesen: Nutzt ultradünnes Glas für hochpräzise Diagnoseinstrumente, Mikroskop-Objektträger und tragbare medizinische Sensoren.

- Sonstige: Umfasst Luft- und Raumfahrt, Verteidigung und spezialisierte industrielle Fertigung.

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Süd- und Mittelamerika

- Naher Osten und Afrika

Berichtsumfang zum Markt für ultradünnes Glas

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 23,44 Milliarden US-Dollar |

| Marktgröße bis 2034 | 55,85 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 10,13 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Durch den Herstellungsprozess

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmer im Bereich ultradünnes Glas: Dichte und ihre Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für ultradünnes Glas wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Kundenbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

Marktanteilsanalyse für ultradünnes Glas nach Regionen

Der asiatisch-pazifische Raum wird voraussichtlich in den kommenden Jahren das schnellste Wachstum verzeichnen. Auch die aufstrebenden Märkte in Nordamerika und Europa bieten zahlreiche ungenutzte Möglichkeiten für hochwertige Glasanwendungen im Medizin- und Automobilsektor.

Der Markt für ultradünnes Glas befindet sich in einem tiefgreifenden Wandel und entwickelt sich von einer Nischenkomponente der Elektronik zu einem vielseitigen Hightech-Material. Das Wachstum wird durch die steigende Nachfrage nach flexibler Elektronik und die Expansion des Premium-Automobilsektors angetrieben. Nachfolgend finden Sie eine Zusammenfassung der Marktanteile und Trends nach Regionen:

1. Nordamerika

- Marktanteil: Ein Nischensegment, das jedoch schnell expandiert und durch die frühe Einführung faltbarer Geräte sowie durch High-End-Anwendungen in der Luft- und Raumfahrt getrieben wird.

-

Wichtigste Einflussfaktoren:

- Starke Präsenz globaler Technologiepioniere und ein etablierter Markt für Luxus-Smartphones.

- Steigende Nachfrage nach Glas-Interposern in KI-gesteuerten Halbleitergehäusen.

- Expansion des Medizin- und Diagnosesektors, der hochreine Glassubstrate benötigt.

- Trends: Erhebliche Investitionen in biotechnologische Anwendungen und die Etablierung von robustem ultradünnem Glas für tragbare Waffen im militärischen und industriellen Bereich.

2. Europa

- Marktanteil: Hält einen bedeutenden Marktanteil, der vor allem auf die führende Automobilindustrie der Region und den Sektor für nachhaltiges Architekturglas zurückzuführen ist.

-

Wichtigste Einflussfaktoren:

- Hohe Nachfrage nach leichten, aerodynamischen Verglasungen seitens der Automobilgiganten in Deutschland und Frankreich.

- Etablierter Forschungs- und Entwicklungsrahmen für erneuerbare Energien und energieeffiziente Baumaterialien.

- Strenge Umweltauflagen drängen auf eine Gewichtsreduzierung im Transportwesen.

- Trends: Strategischer Fokus auf die Prinzipien der Kreislaufwirtschaft, wobei die Recyclingfähigkeit von Dünnglas und dessen Integration in gebäudeintegrierte Photovoltaik (BIPV) Priorität haben.

3. Asien-Pazifik

- Marktanteil: Besitzt weltweit den größten Marktanteil, der durch die weltweit dominantesten Cluster der Elektronikfertigung in China, Südkorea, Taiwan und Japan verankert ist.

-

Wichtigste Einflussfaktoren:

- Massive Konzentration von Produktionsanlagen für OLED- und Micro-LED-Panels.

- Staatliche Initiativen zur Förderung der Halbleiter-Selbstversorgung und der 5G-Infrastruktur.

- Die rasante Urbanisierung treibt die Nachfrage nach hochwertigen, ultradünnen Unterhaltungselektronikgeräten an.

- Trends: Eine strategische Verlagerung hin zur lokalen Produktion von ultradünnem Glas (UTG), um die Abhängigkeit von der Lieferkette zu verringern, verbunden mit intensiver Forschung und Entwicklung im Bereich der Fertigung für hocheffizientes Glasschneiden.

4. Süd- und Mittelamerika

- Marktanteil: Aufstrebender Markt mit wachsender Produktionspräsenz in Brasilien und Chile.

-

Wichtigste Einflussfaktoren:

- Erweiterung der Montagelinien für regionale Marken der Unterhaltungselektronik.

- Modernisierung der automobilen Lieferkette hin zu digitalen Schnittstellen im Fahrzeuginnenraum.

- Trends: Zunehmende Importe von Hightech-Glasplatten für die lokale Smartphone-Finishierung und ein Anstieg der spezialisierten industriellen Sensorproduktion.

5. Naher Osten und Afrika

- Marktanteil: Entwicklungsmarkt im Übergang zu einer formalisierten industriellen Produktion.

-

Wichtigste Einflussfaktoren:

- Strategische Investitionen in Städte (z. B. NEOM), die fortschrittliche Display- und Verglasungslösungen benötigen.

- Wachstum im Solarenergiesektor, insbesondere bei hocheffizienten, leichten Paneelen.

- Trends: Implementierung moderner Logistik- und Fertigungszentren zur Überbrückung der Lücke zwischen asiatischer Produktion und der Nachfrage in der EMEA-Region.

Die wichtigsten Unternehmen, die auf dem Markt für ultradünnes Glas tätig sind, sind:

- Corning Incorporated

- AGC Inc.

- Nippon Electric Glass Co., Ltd.

- SCHOTT AG

- Central Glass Co., Ltd.

- CSG Holding Co., Ltd.

- Emerge Glass

- Nippon Sheet Glass Co., Ltd

- Xinyi Glass Holdings Limited

- Luoyang Glass Co., Ltd.

Hinweis: Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge geordnet.

Neuigkeiten und aktuelle Entwicklungen auf dem Markt für ultradünnes Glas

- Im November 2025 gab Alpen High Performance Products (Alpen) eine Kooperation mit Corning Incorporated bekannt, einem der weltweit führenden Innovatoren in den Bereichen Glas, Keramik und Materialwissenschaften. Im Rahmen dieser Zusammenarbeit wird Alpen Corning® Enlighten™ Glas als ultradünne Mittelscheibe für seine Dreifach- und Vierfachverglasungen verwenden und so die Markteinführung von Fenstern der nächsten Generation für den US-Markt vorantreiben.

- Im September 2025 gab Nippon Electric Glass Co., Ltd. bekannt, dass ihre ultradünne Glasscheibe Dinorex UTG™, die speziell für die chemische Härtung entwickelt wurde, für die Abdeckung des inneren Hauptdisplays des neuesten faltbaren Smartphones von HONOR, dem Magic V Flip2, verwendet wird. HONOR ist ein Hersteller von intelligenten Geräten, der weltweit schnell an Anerkennung gewinnt.

Marktbericht zu ultradünnem Glas: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für ultradünnes Glas (2021–2034)“ bietet eine detaillierte Analyse des Marktes und deckt folgende Bereiche ab:

- Marktgröße und Prognose für ultradünnes Glas auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt werden

- Trends im Markt für ultradünnes Glas sowie Marktdynamiken wie Treiber, Hemmnisse und wichtige Chancen

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für ultradünnes Glas: Wichtige Markttrends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Rahmenbedingungen und aktuelle Marktentwicklungen

- Branchenlandschafts- und Wettbewerbsanalyse mit Fokus auf Marktkonzentration, Heatmap-Analyse, prominente Akteure und aktuelle Entwicklungen auf dem Markt für ultradünnes Glas.

- Detaillierte Unternehmensprofile

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends