Descripción general del mercado de pantallas 3D, crecimiento, tendencias, análisis, informe de investigación (2021-2028)

Descripción general del mercado de pantallas 3D, crecimiento, tendencias, análisis, informe de investigación (2021-2028)

- Estado : Publicada

- Código de informe : TIPTE100000774

- Categoría : Electrónica y semiconductores

- Número de páginas : 188

- Formatos de informe disponibles :

- Fecha de última actualización : June 12, 2024

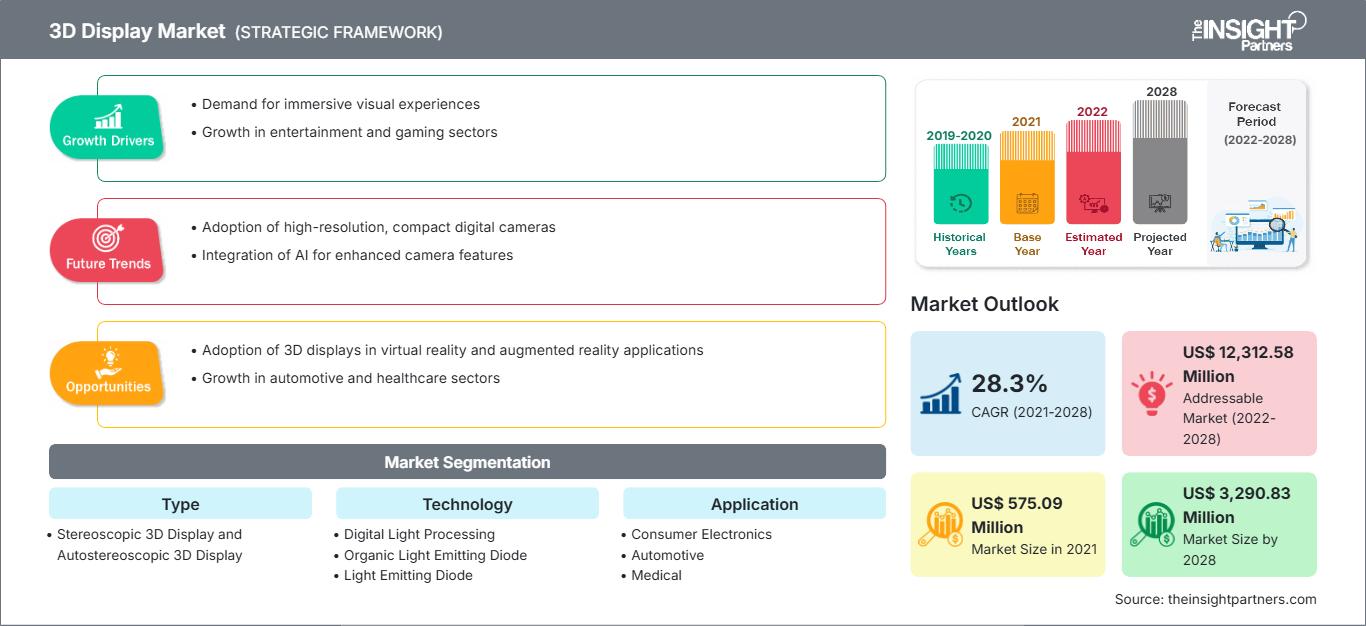

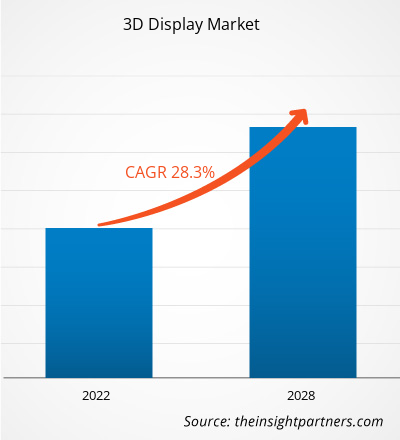

El mercado de pantallas 3D se valoró en US$ 575,09 millones en 2021 para alcanzar los US$ 3.290,83 millones en 2028; se estima que registrará una CAGR del 28,3% de 2021 a 2028.

La electrónica de consumo, la automoción, la medicina, el sector militar y de defensa, la industria, los medios de comunicación y el entretenimiento, y los videojuegos se encuentran entre los mercados potenciales para las pantallas 3D. Además, el crecimiento de las industrias del entretenimiento y los videojuegos ha tenido un impacto positivo en el mercado de las pantallas 3D, ya que el número de pantallas de cine ha aumentado significativamente; es decir, aproximadamente 125 000 en 2021 comenzaron a operar en una plataforma digital a nivel mundial. Asimismo, la creciente adopción de la realidad aumentada en diversas aplicaciones médicas para mejorar la visión de los cirujanos, reducir el tiempo de operación y la planificación preoperatoria está creando oportunidades para el mercado de las pantallas 3D. Por ejemplo, en mayo de 2020, Ocutrx Vision Technologies, LLC anunció el desarrollo de su nueva sala de visualización quirúrgica, "Ocutrx OR-Bot", equipada con un monitor 3D 8K para operar herramientas quirúrgicas. Sin embargo, las inversiones continuas, especialmente en soluciones de visualización 3D autoestereoscópica, y el creciente número de asociaciones entre los actores del mercado y los usuarios finales para desarrollar sistemas de visualización 3D holográficos y volumétricos avanzados para una amplia gama de aplicaciones se encuentran entre los factores que impulsan el crecimiento del mercado global de visualización 3D.

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de pantallas 3D: Perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Impacto de la pandemia de COVID-19 en el mercado de pantallas 3D

La crisis de la COVID-19 afectó a industrias de todo el mundo, y la economía global fue la más afectada en 2020, y es probable que esto continúe en 2021. El brote generó importantes disrupciones en industrias primarias como la automotriz, el comercio minorista y la electrónica de consumo. La fuerte caída en las industrias electrónica y manufacturera está impactando el crecimiento del mercado global de pantallas 3D. América del Norte es una de las regiones más favorables para la adopción y el crecimiento de nuevas tecnologías debido a las políticas gubernamentales de apoyo para impulsar la innovación, la presencia de una enorme base industrial y un alto poder adquisitivo, especialmente en países desarrollados como Estados Unidos y Canadá. América del Norte alberga un gran número de empresas manufactureras y tecnológicas, por lo que el impacto del brote de COVID-19 había sido bastante severo hasta mediados de 2021. La región espera una recuperación del mercado y una mejora económica con las campañas de vacunación contra la COVID-19.

Perspectivas del mercado: mercado de pantallas 3D

Un número creciente de asociaciones industriales impulsará el crecimiento del mercado

Las principales áreas de aplicación actuales de las pantallas 3D son el marketing y la publicidad. Se prevé que los sectores médico, automotriz y de defensa se encuentren entre las áreas con mayor potencial para las pantallas 3D. El número de posibles áreas de aplicación de las tecnologías de visualización 3D podría alcanzar cifras sin precedentes, dependiendo del crecimiento positivo y el desarrollo tecnológico del mercado.

Perspectivas basadas en tipos

Según el tipo, el mercado de pantallas 3D se segmenta en pantallas 3D estereoscópicas y pantallas 3D autoestereoscópicas. El segmento de pantallas 3D autoestereoscópicas tuvo una mayor participación de mercado en 2021.

Los actores que operan en el mercado de pantallas 3D se centran principalmente en el desarrollo de productos avanzados y eficientes.

- En abril de 2021, AUO lanzó una impresionante serie de pantallas ALED en Touch Taiwan 2021 con tecnología y aplicaciones micro LED líderes en el mundo en exhibición.

- En septiembre de 2021, la pantalla extensible de Samsung puede convertir contenido 2D en escenas 3D en movimiento.

Perspectivas regionales del mercado de pantallas 3D

Los analistas de The Insight Partners han explicado detalladamente las tendencias regionales y los factores que influyen en el mercado de pantallas 3D durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de pantallas 3D en Norteamérica, Europa, Asia Pacífico, Oriente Medio y África, y Sudamérica y Centroamérica.

Alcance del informe del mercado de pantallas 3D

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2021 | US$ 575,09 millones |

| Tamaño del mercado en 2028 | US$ 3.290,83 millones |

| CAGR global (2021-2028) | 28,3% |

| Datos históricos | 2019-2020 |

| Período de pronóstico | 2022-2028 |

| Segmentos cubiertos |

Por tipo

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de pantallas 3D: comprensión de su impacto en la dinámica empresarial

El mercado de pantallas 3D está creciendo rápidamente, impulsado por la creciente demanda del usuario final debido a factores como la evolución de las preferencias del consumidor, los avances tecnológicos y un mayor conocimiento de las ventajas del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades del consumidor y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

- Obtenga una descripción general de los principales actores clave del mercado de pantallas 3D

El mercado de pantallas 3D se segmenta por tipo, tecnología, aplicación y geografía. Según el tipo, el mercado se segmenta en pantallas 3D estereoscópicas y pantallas 3D autoestereoscópicas. En 2021, el segmento de pantallas 3D autoestereoscópicas lideró el mercado de pantallas 3D y representó la mayor participación de mercado. Según la tecnología, el mercado se clasifica en procesamiento digital de luz, diodo orgánico emisor de luz y diodo emisor de luz. En 2021, el segmento de procesamiento digital de luz lideró el mercado de pantallas 3D y representó la mayor participación de mercado. Según la aplicación, el mercado se segmenta en electrónica de consumo, automotriz, médica, publicidad, comercio minorista, militar y defensa, entre otros. En 2021, el segmento de electrónica de consumo lideró el mercado de pantallas 3D y representó la mayor participación de mercado. Geográficamente, el mercado está ampliamente segmentado en América del Norte, Europa, Asia Pacífico (APAC), Oriente Medio y África (MEA) y América del Sur (SAM). En 2021, América del Norte representó una participación significativa en el mercado mundial.

Algunos de los principales proveedores en el mercado global de pantallas 3D incluyen empresas como AU OPTRONICS CORP, Innolux Corporation, LG Electronics, Mitsubishi Electric Corporation, Panasonic Corporation, Samsung Group, Sharp Corporation, Looking Glass Factory Inc, Light Field Lab Inc, Leia Inc, Sony, Toshiba Corporation y Fujifilm Corporation.

Naveen es un experimentado profesional en investigación de mercados y consultoría con más de 9 años de experiencia en proyectos personalizados, sindicados y de consultoría. Actualmente se desempeña como Vicepresidente Asociado, donde ha gestionado con éxito a las partes interesadas en toda la cadena de valor del proyecto y ha redactado más de 100 informes de investigación y más de 30 proyectos de consultoría. Su trabajo abarca proyectos industriales y gubernamentales, contribuyendo significativamente al éxito de los clientes y a la toma de decisiones basada en datos.

Naveen es licenciado en Ingeniería Electrónica y Comunicaciones por la VTU (Karnataka) y tiene un MBA en Marketing y Operaciones por la Universidad de Manipal. Ha sido miembro activo del IEEE durante 9 años, participando en conferencias, simposios técnicos y realizando voluntariado tanto a nivel de sección como regional. Antes de su puesto actual, trabajó como Consultor Estratégico Asociado en IndustryARC y como Consultor de Servidores Industriales en Hewlett Packard (HP Global).

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias