Análisis y pronóstico del mercado de generadores de centros de datos por tamaño, participación, crecimiento y tendencias para 2028

Pronóstico del mercado de generadores para centros de datos hasta 2028: impacto de la COVID-19 y análisis global por tipo de producto (diésel, gas natural y otros), capacidad (menos de 1 MW, 1-2 MW y más de 2 MW) y nivel (niveles 1 y 2, 3 y 4).

- Estado : Publicada

- Código de informe : TIPRE00012410

- Categoría : Energía y potencia

- Número de páginas : 189

- Formatos de informe disponibles :

- Fecha de última actualización : June 19, 2024

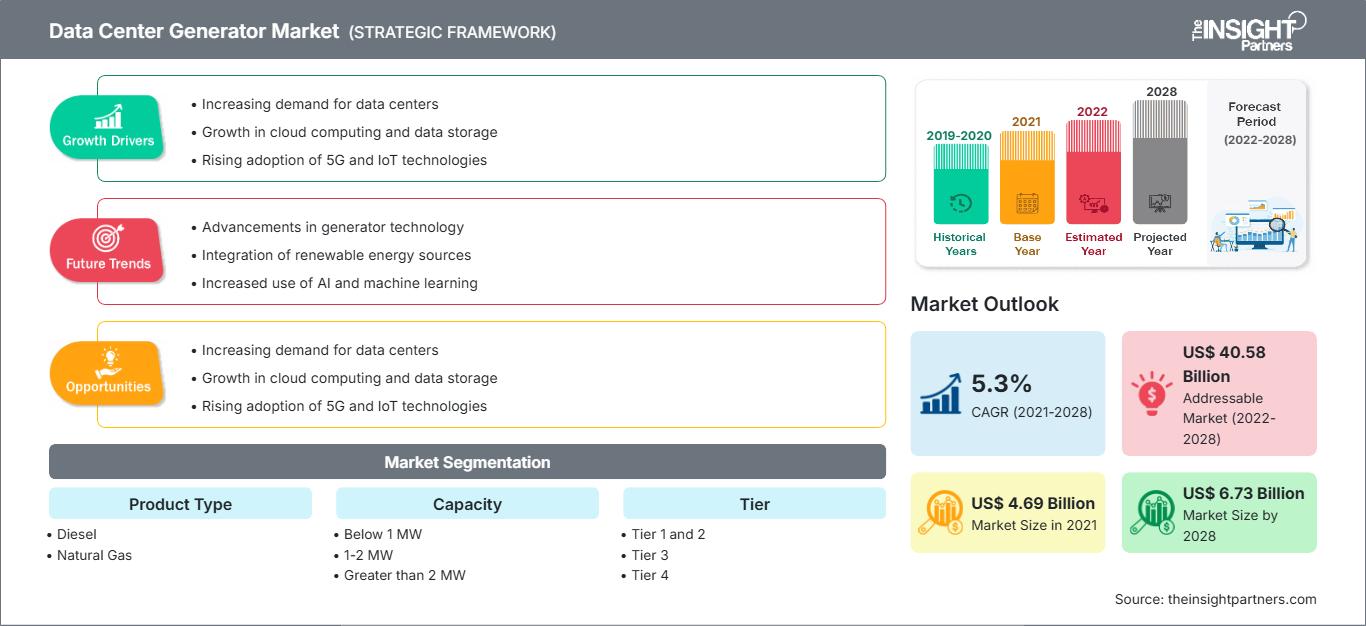

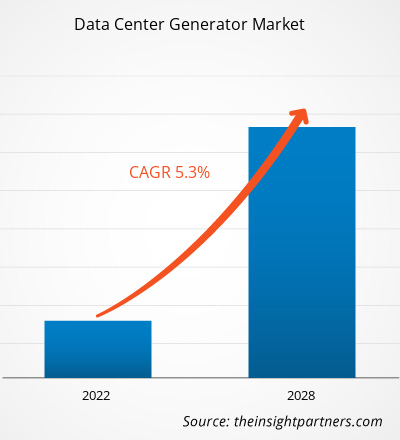

[Informe de investigación] El mercado de generadores para centros de datos se valoró en 4.693,00 millones de dólares estadounidenses en 2021 y se espera que alcance los 6.729,53 millones de dólares estadounidenses en 2028; se estima que registrará una tasa de crecimiento anual compuesta (TCAC) del 5,3% entre 2021 y 2028.

Los generadores sirven como fuente de alimentación de respaldo para los centros de datos durante un apagón. Un apagón total en un centro de datos puede requerir el reinicio del sistema, lo que conlleva tiempos de inactividad, dificultades de arranque y pérdida de datos. Por lo tanto, los centros de datos siempre cuentan con un suministro de energía de respaldo proporcionado por generadores para evitar este tipo de anomalías y fallos. Estas ventajas impulsan el crecimiento del mercado de generadores para centros de datos.

Estos generadores no requieren una conexión eléctrica previa para funcionar, lo cual representa un importante factor de dinamismo para el mercado. Además, los principales fabricantes producen generadores con capacidad personalizada para adaptarse a las cambiantes demandas de los clientes. Estos sistemas pueden aumentar o disminuir su capacidad según los requisitos energéticos del centro de datos. Esta adaptabilidad probablemente incrementará la demanda de generadores para centros de datos, impulsando así el crecimiento del mercado. Varios proveedores de servicios en la nube han aumentado su producción debido al incremento de la demanda de centros de datos en el borde de la red a nivel mundial. Google, por ejemplo, invirtió 3300 millones de dólares en 2019 para expandir su presencia de centros de datos en Europa. Asimismo, es probable que el mercado se beneficie del creciente desarrollo de instalaciones hiperescalables y del aumento en la implementación de sistemas de alimentación ininterrumpida (SAI) rotativos diésel (DRUPS).DRUPS).

Obtendrá personalización gratuita de cualquier informe, incluyendo partes de este informe, análisis a nivel de país y paquetes de datos de Excel. Además, podrá aprovechar excelentes ofertas y descuentos para empresas emergentes y universidades.

Mercado de generadores para centros de datos: Perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado que se describen en este informe.Esta muestra GRATUITA incluirá análisis de datos, que abarcarán desde tendencias de mercado hasta estimaciones y pronósticos.

Perspectivas del mercado de generadores de centros de datos

Aumento del número de centros de datos

En la era de los datos, ya existen alrededor de siete mil millones de dispositivos conectados a internet, y esa cifra sigue creciendo. Muchos de ellos generan enormes cantidades de datos, que deben registrarse, enrutarse, almacenarse, analizarse y recuperarse. Los fabricantes dependen del big data y el análisis de datos para mejorar la eficiencia, la productividad, la seguridad y la rentabilidad de sus operaciones a medida que el Internet de las Cosas (IoT) y la Industria 4.0 se consolidan. Por otro lado, la gestión interna de datos se está volviendo cada vez más compleja, lenta y costosa. Para ahorrar energía y costes de infraestructura, incluso grandes empresas como Cisco se plantean cerrar partes de sus propios centros de datos internos.

El aumento de la penetración de dispositivos conectados y el fácil acceso a internet, junto con la reducción del coste de los servicios de internet, están impulsando la demanda de almacenamiento de datos a nivel mundial. La necesidad de almacenamiento de datos también se está incrementando debido a la creciente demanda de análisis de macrodatos y servicios en la nube, como el contenido en línea que incluye películas, aplicaciones, vídeos y redes sociales. Por lo tanto, las empresas que utilizan servicios en la nube despliegan espacio de TI en sus centros de datos. Diversos sectores están explorando las ofertas de la nube y descubriendo las ventajas de los servicios de centros de datos para satisfacer sus necesidades relacionadas con la nube. Estos avances influyen directamente en el aumento del uso del Internet de las Cosas (IoT), lo que se traduce en la construcción de un gran número de centros de datos en todo el mundo. Por ejemplo, Colt ha anunciado el desarrollo de sus centros de datos hiperescalables en Europa y Asia-Pacífico, tras la venta de 12 centros de colocación edge en Europa. La corporación ha adquirido diez nuevos terrenos en Londres, Fráncfort, París y ubicaciones no reveladas en Japón, que le permitirán generar aproximadamente 100 MW de potencia de TI. Por lo tanto, el creciente número de centros de datos aumenta la necesidad de generadores para centros de datos que proporcionen un suministro eléctrico suficiente, lo que a su vez impulsa el crecimiento del mercado de generadores para centros de datos.

Información de mercado basada en el tipo de producto

En los últimos años, la demanda de generadores para centros de datos ha aumentado a nivel mundial. Las empresas ofrecen tres tipos: diésel, gas natural y bifuel. En enero de 2022, Cummins Power Generation anunció que había sido galardonada por la industria de centros de datos de China por sus soluciones de energía. Esta empresa fabrica generadores diésel para centros de datos. En enero de 2021, TRG Datacenters anunció la modernización de su centro de datos en Texas. La empresa planea instalar un sistema bifuel como respaldo de energía.

Perspectivas de mercado basadas en la capacidad

En cuanto a capacidad, el mercado de generadores para centros de datos se segmenta en menos de 1 MW, de 1 a 2 MW y más de 2 MW. La capacidad inferior a 1 MW es la más común. Las instalaciones con una capacidad superior a 10 MW utilizan generadores de más de 2 MW. Los generadores con una capacidad inferior a 1 MW se suelen emplear en centros de datos modulares. Se prevé que la adopción de generadores con una capacidad inferior a 1 MW impulse el despliegue de centros de datos. Los operadores de centros de datos a pequeña escala en economías en desarrollo los están adoptando por su menor coste. El auge de la fabricación de instalaciones hiperescalables en las economías emergentes reducirá la dependencia de generadores de baja capacidad en los próximos años.

Los participantes del mercado de generadores para centros de datos adoptan estrategias como fusiones, adquisiciones e iniciativas de mercado para mantener su posición. A continuación, se enumeran algunos avances de los principales actores del mercado de generadores para centros de datos:

- ABB LTD ha presentado una nueva tecnología de generadores de eje. Este nuevo generador ofrece flexibilidad y facilidad de instalación en numerosos buques, incluidos graneleros y portacontenedores. El generador de eje de imanes permanentes AMZ 1400 está optimizado para el control mediante convertidor y permite una mayor eficiencia que la inducción.

- Caterpillar lanzará un proyecto piloto con tecnología de celdas de combustible de hidrógeno para alimentación de respaldo en el centro de datos de Microsoft. Este proyecto permite a Caterpillar colaborar con líderes del sector para dar un gran paso hacia soluciones energéticas comercialmente viables que, además, ayudan a los clientes a lograr operaciones más sostenibles.

Perspectivas regionales del mercado de generadores de centros de datos

Los analistas de The Insight Partners han explicado en detalle las tendencias y los factores regionales que influyen en el mercado de generadores para centros de datos durante el período de previsión. Esta sección también analiza los segmentos y la geografía del mercado de generadores para centros de datos en Norteamérica, Europa, Asia Pacífico, Oriente Medio y África, y Sudamérica y Centroamérica.

Alcance del informe de mercado de generadores de centros de datos

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2021 | 4.690 millones de dólares estadounidenses |

| Tamaño del mercado para 2028 | 6.730 millones de dólares estadounidenses |

| Tasa de crecimiento anual compuesto global (2021 - 2028) | 5,3% |

| Datos históricos | 2019-2020 |

| período de previsión | 2022-2028 |

| Segmentos cubiertos |

Por tipo de producto

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de los actores del mercado de generadores de centros de datos: comprensión de su impacto en la dinámica empresarial

El mercado de generadores para centros de datos está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

- Obtenga una visión general de los principales actores del mercado de generadores para centros de datos.

El mercado global de generadores para centros de datos se segmenta según el tipo de producto, la capacidad y la categoría. Según el tipo de producto, se divide en generadores diésel, de gas natural y otros. En cuanto a la capacidad, se segmenta en menos de 1 MW, de 1 a 2 MW y más de 2 MW. Además, según la categoría, se divide en categorías 1 y 2, categoría 3 y categoría 4.

ABB, Atlas Copco AB, Caterpillar, Cummins Inc., DEUTZ AG, Generac Power Systems, Inc., HITEC Power Protection, Kirloskar, Kohler Co. y MITSUBISHI MOTORS CORPORATION son los principales actores del mercado de generadores para centros de datos considerados en este estudio. Además, se han analizado otros actores importantes del mercado para obtener una visión integral del tamaño del mercado global de generadores para centros de datos y su ecosistema.

Nivedita es una investigadora con más de 9 años de experiencia en Investigación de Mercados y Consultoría de Negocios. Actualmente se desempeña como Gerente de Proyectos en el área de TIC en The Insight Partners, y aporta una amplia experiencia en la gestión y ejecución de proyectos de investigación sindicados, personalizados, por suscripción y de consultoría en diversos sectores tecnológicos.

Con una trayectoria comprobada en la entrega de análisis basados en datos e información práctica, Nivedita ha sido una colaboradora clave en varios proyectos cruciales. Su trabajo abarca la ejecución integral de proyectos, desde la comprensión de los objetivos del cliente y el análisis de las tendencias del mercado hasta la formulación de recomendaciones estratégicas. Ha colaborado extensamente con empresas líderes en TIC, ayudándolas a identificar oportunidades de mercado y a adaptarse a los cambios del sector.

Nivedita posee un MBA en Administración de Empresas por IMS, Dehradun. Antes de unirse a The Insight Partners, adquirió una valiosa experiencia en MarketsandMarkets y Future Market Insights en Pune, donde ocupó diversos puestos de investigación y desarrolló una sólida base en análisis del sector y la interacción con el cliente.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias