Mercado de instrumentos de cirugía dental: mapeo competitivo y perspectivas estratégicas para 2031

Tamaño y pronóstico del mercado de instrumentos de cirugía dental (2021-2031), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por producto (instrumentos, consumibles), área terapéutica (odontología restauradora, ortodoncia, endodoncia, otras áreas terapéuticas), usuario final (hospitales y clínicas) y geografía.

- Estado : Datos publicados

- Código de informe : TIPRE00007975

- Categoría : Ciencias de la vida

- Número de páginas : 150

- Formatos de informe disponibles :

- Fecha de última actualización : May 16, 2024

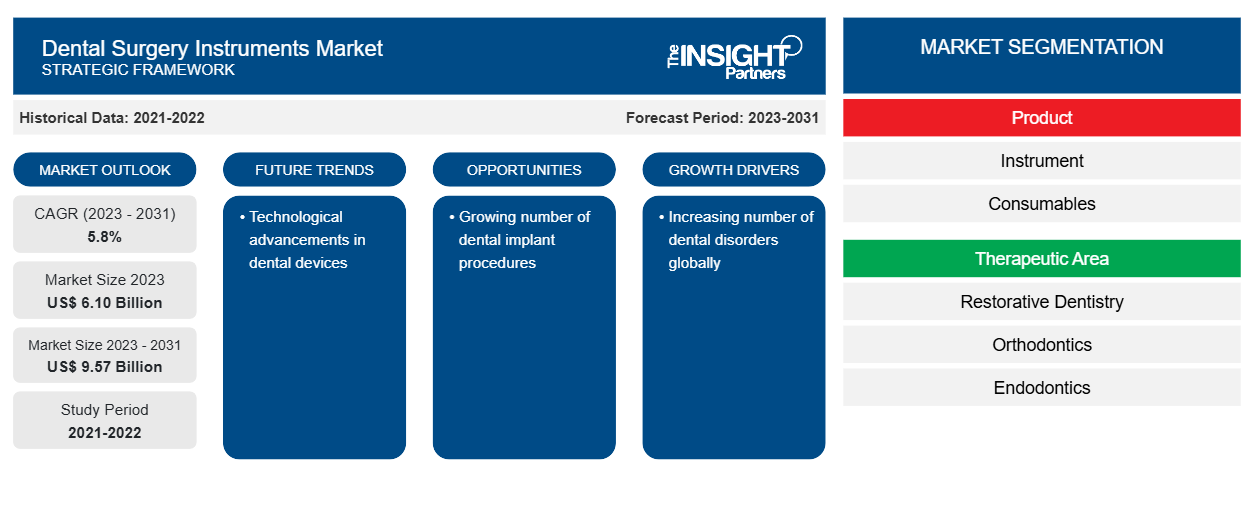

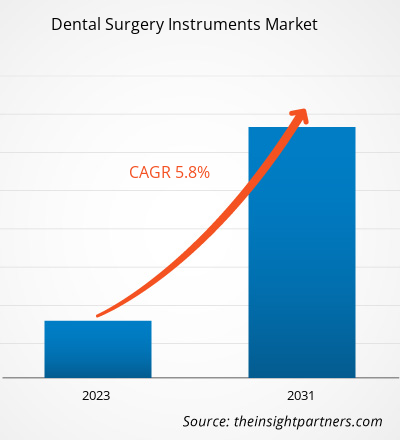

Se proyecta que el tamaño del mercado de instrumentos de cirugía dental alcance los 9.570 millones de dólares estadounidenses para 2031, frente a los 6.100 millones de dólares estadounidenses en 2023. Se espera que el mercado registre una CAGR del 5,8 % entre 2023 y 2031. Es probable que la creciente prevalencia de infecciones dentales, los avances tecnológicos en la industria dental y el creciente número de procedimientos dentales sigan siendo tendencias clave del mercado de instrumentos de cirugía dental.CAGR of 5.8% in 2023–2031. The increasing prevalence of dental infection, technological advancements in the dental industry, and the rising number of dental procedures are likely to remain key Dental Surgery Instruments market trends.

Análisis del mercado de instrumentos de cirugía dental

La creciente carga de enfermedades dentales como caries, enfermedad periodontal, cáncer oral, halitosis y caries dentales a nivel mundial está aumentando el crecimiento del mercado. Por ejemplo, las enfermedades bucales afectan aproximadamente a 3.500 millones de personas en todo el mundo. Las enfermedades bucales suponen una importante carga de salud tanto para los países desarrollados como para los países en desarrollo y afectan a las personas durante toda su vida, provocando dolor, malestar, desfiguración e incluso la muerte. Por lo tanto, se prevé que la enorme carga de enfermedades dentales aumente la demanda general de su tratamiento y cirugías, impulsando así el mercado de instrumentos quirúrgicos dentales durante el período de pronóstico.

Descripción general del mercado de instrumentos para cirugía dental

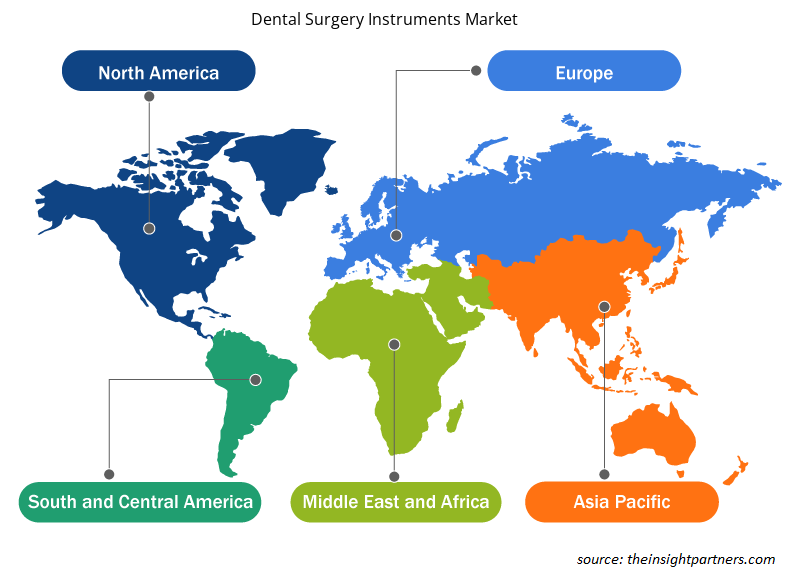

América del Norte es el mercado más grande para el crecimiento del mercado de instrumentos de cirugía dental, y Estados Unidos tiene la mayor participación de mercado, seguido de Canadá. Se prevé que factores como la creciente prevalencia de enfermedades dentales, las iniciativas gubernamentales para ayudar a las personas con el tratamiento dental y una mayor concienciación entre la población impulsen aún más el mercado general de instrumentos de cirugía dental de América del Norte. Por ejemplo, en 2021, según los datos recuperados del Centro para el Control de Enfermedades, a los 8 años, más de la mitad de los niños (52%) han tenido una caries en sus dientes primarios (de leche) en los EE. UU. De manera similar, según el Instituto Nacional de Investigación Dental y Craneofacial en 2022, la caries dental afecta al 90% de la población adulta de 20 a 64 años, y la enfermedad de las encías afecta a casi el 50% de los adultos de 45 a 64 años, que siguen siendo dos de las enfermedades bucales más prevalentes en los EE. UU. Por lo tanto, la creciente población adulta que sufre enfermedades bucales demandará tratamiento y cirugía dental, lo que a su vez está impulsando el mercado de instrumentos de cirugía dental de América del Norte.

Personalice este informe según sus necesidades

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de instrumentos para cirugía dental: perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Factores impulsores y oportunidades del mercado de instrumentos para cirugía dental

La creciente prevalencia de trastornos dentales demanda un sistema de instrumentos para cirugía dental que favorece el mercado

La creciente carga de enfermedades dentales y su creciente prevalencia están impulsando el crecimiento del mercado. Por ejemplo, según la Organización Mundial de la Salud (OMS), se estima que las enfermedades bucales afectan a casi 3.500 millones de personas en todo el mundo, y la enfermedad periodontal (de las encías) grave, que puede provocar la pérdida de dientes, también es muy común, ya que afecta a casi el 14% de la población mundial. Además, la iniciativa gubernamental que se está llevando a cabo es otro factor en el crecimiento del mercado. Países como España y su gobierno han emprendido iniciativas para que la atención dental sea accesible a una gran proporción de la población. También se están realizando inversiones para ampliar la cobertura dental. Por ejemplo, en febrero de 2021, el Gobierno de España asignó 49 millones de euros para ampliar la cobertura de la atención dental.

Avances tecnológicos en los instrumentos de cirugía dental: una oportunidad en el mercado de instrumentos de cirugía dental

Los fabricantes y profesionales dentales están utilizando la impresión 3D para diversas aplicaciones clínicas y propósitos de investigación. La fabricación aditiva de capas en la impresión 3D permite a los dentistas fabricar dispositivos médicos diseñados a medida, a pesar de las formas complejas, los sistemas porosos y los sistemas de asistencia internos, lo que no es posible con los dispositivos dentales tradicionales. La tecnología se está utilizando para fabricar dispositivos quirúrgicos desechables y reutilizables diseñados a medida. La tecnología también ayuda a los profesionales dentales a proporcionar numerosos implantes dentales personalizados , que consisten en alineadores transparentes, coronas, puentes y retenedores. Los escaneos 3D de la boca del paciente garantizan una alta precisión y personalización de los implantes dentales, mejorando su ajuste, comodidad y simplicidad del procedimiento quirúrgico. Se espera que la llegada de estas tecnologías impulse el mercado general de instrumentos de cirugía dental.customizability of dental implants, improving their match, comfort, and simplicity of surgical procedure. The advent of such technologies is expected to boost the overall dental surgery instrument market.

Informe de mercado de instrumentos de cirugía dental Análisis de segmentación

Los segmentos clave que contribuyeron a la derivación del análisis del mercado de instrumentos de cirugía dental son los servicios, los proveedores de servicios y los usuarios finales.

- Según el producto, el mercado de instrumentos para cirugía dental se segmenta en instrumentos y consumibles. Los instrumentos tuvieron una mayor participación de mercado en 2023. La mayor participación se puede atribuir a la creciente adopción de instrumentos para procedimientos quirúrgicos dentales.

- Por área terapéutica, el mercado está segmentado en odontología restauradora, ortodoncia, endodoncia y otras áreas terapéuticas. El segmento de odontología restauradora tuvo la mayor participación del mercado en 2023.

- Por usuario final, el mercado está segmentado en hospitales y clínicas. El segmento de clínicas tuvo la mayor participación de mercado en el año 2023. La creciente aceptación de instrumentos quirúrgicos avanzados y el número de clínicas dentales en países emergentes y desarrollados son los factores que aumentan la demanda de instrumentos de cirugía dental en las clínicas.

Análisis de la cuota de mercado de los instrumentos de cirugía dental por geografía

El alcance geográfico del informe del mercado de instrumentos de cirugía dental se divide principalmente en cinco regiones: América del Norte, Asia Pacífico, Europa, Medio Oriente y África, y América del Sur / América del Sur y Central.

América del Norte ha dominado el mercado de instrumentos de cirugía dental. El crecimiento del mercado se puede atribuir a la creciente incidencia mundial de enfermedades dentales, la creciente población geriátrica y la necesidad de instrumentos dentales para la odontología cosmética, que está impulsando el mercado de instrumentos de cirugía dental de América del Norte. Además, se prevé que la demanda de instrumentos de cirugía dental y su mayor adopción en los próximos años debido al consumo repetido de consumibles por parte de hospitales, odontólogos y clínicas dentales impulse aún más el mercado de instrumentos de cirugía dental en los países de América del Norte.

Perspectivas regionales del mercado de instrumentos para cirugía dental

Los analistas de Insight Partners explicaron en detalle las tendencias y los factores regionales que influyen en el mercado de instrumentos de cirugía dental durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de instrumentos de cirugía dental en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

- Obtenga datos regionales específicos para el mercado de instrumentos de cirugía dental

Alcance del informe de mercado de instrumentos de cirugía dental

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2023 | US$ 6.10 mil millones |

| Tamaño del mercado en 2031 | US$ 9,57 mil millones |

| CAGR global (2023 - 2031) | 5,8% |

| Datos históricos | 2021-2022 |

| Período de pronóstico | 2023-2031 |

| Segmentos cubiertos |

Por producto

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado: comprensión de su impacto en la dinámica empresarial

El mercado de instrumentos para cirugía dental está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían sus ofertas, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

La densidad de actores del mercado se refiere a la distribución de las empresas o firmas que operan dentro de un mercado o industria en particular. Indica cuántos competidores (actores del mercado) están presentes en un espacio de mercado determinado en relación con su tamaño o valor total de mercado.

Las principales empresas que operan en el mercado de instrumentos de cirugía dental son:

- Dentsply Sirona

- 3M

- Danaher

- Coltene Holdings AG

- Brasseler Estados Unidos

- Integra Ciencias de la Vida

Descargo de responsabilidad : Las empresas enumeradas anteriormente no están clasificadas en ningún orden particular.

- Obtenga una descripción general de los principales actores clave del mercado de instrumentos de cirugía dental

Noticias y desarrollos recientes del mercado de instrumentos para cirugía dental

El mercado de instrumentos de cirugía dental se evalúa mediante la recopilación de datos cualitativos y cuantitativos posteriores a la investigación primaria y secundaria, que incluye publicaciones corporativas importantes, datos de asociaciones y bases de datos. A continuación, se incluye una lista de los avances en el mercado de instrumentos de cirugía dental:

- J. Morita Corp. adquirió el negocio de la planta Nasu de Dentsply Sirona en Japón, que fabrica productos de ortodoncia y otros productos relacionados con la odontología. Esta adquisición aumentaría el crecimiento del mercado de instrumentos de cirugía dental en el próximo período. (Fuente: J Morita Corporation, comunicado de prensa/sitio web de la empresa/boletín informativo, abril de 2021)

- Henry Schein, Inc., el mayor proveedor mundial de soluciones de atención médica para odontólogos y médicos en consultorios, anunció que ha completado la adquisición de Condor Dental Research Company SA (Condor Dental), una empresa de distribución dental que presta servicios a odontólogos generales, especialistas y laboratorios en Suiza. (Fuente: J Morita Corporation, comunicado de prensa/sitio web de la empresa/boletín informativo, junio de 2022)

Informe de mercado sobre instrumentos de cirugía dental: cobertura y resultados

El informe “Tamaño y pronóstico del mercado de instrumentos de cirugía dental (2021-2031)” proporciona un análisis detallado del mercado que cubre las siguientes áreas:

- Tamaño del mercado y pronóstico a nivel global, regional y nacional para todos los segmentos clave del mercado cubiertos bajo el alcance

- Dinámica del mercado, como impulsores, restricciones y oportunidades clave

- Principales tendencias futuras

- Análisis detallado de las cinco fuerzas de Porter y PEST y FODA

- Análisis del mercado global y regional que cubre las tendencias clave del mercado, los principales actores, las regulaciones y los desarrollos recientes del mercado.

- Análisis del panorama de la industria y de la competencia que abarca la concentración del mercado, el análisis de mapas de calor, los actores destacados y los desarrollos recientes

- Perfiles detallados de empresas

Mrinal es una experimentada analista de investigación con más de 8 años de experiencia en inteligencia de mercado y consultoría en ciencias de la vida. Con una mentalidad estratégica y un firme compromiso con la excelencia, ha desarrollado una amplia experiencia en pronósticos farmacéuticos, evaluación de oportunidades de mercado y desarrollo de indicadores de referencia para la industria. Su trabajo se centra en brindar información práctica que permita a los clientes tomar decisiones estratégicas informadas.

La principal fortaleza de Mrinal reside en convertir conjuntos de datos cuantitativos complejos en inteligencia de negocios significativa. Su perspicacia analítica es fundamental para definir estrategias de salida al mercado (GTM) y descubrir oportunidades de crecimiento en los sectores farmacéutico y de dispositivos médicos. Como consultora de confianza, se centra constantemente en optimizar los procesos de flujo de trabajo y establecer las mejores prácticas, impulsando así la innovación y la eficiencia operativa para sus clientes.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias