Papas fritas congeladas Descripción general del mercado, crecimiento, tendencias, análisis, informe de investigación (2022-2030)

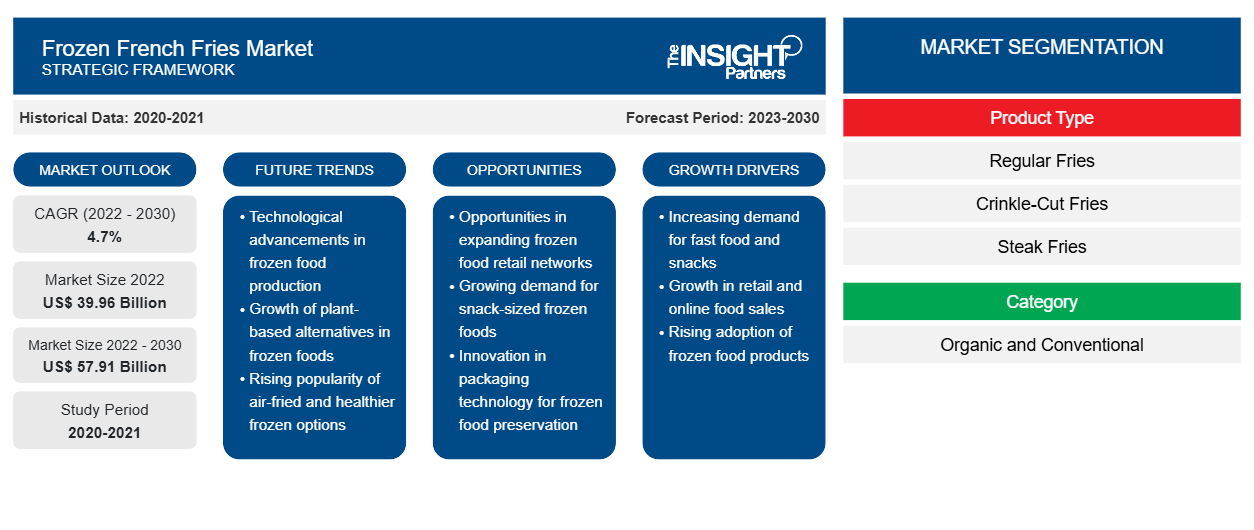

Datos históricos : 2020-2021 | Año base : 2022 | Período de pronóstico : 2023-2030Tamaño y pronósticos del mercado de papas fritas congeladas (2020-2030), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por tipo de producto (papas fritas regulares, onduladas, bistec y otras), categoría (orgánica y convencional) y usuario final (minorista y servicios de alimentación).

- Estado : Publicada

- Código de informe : TIPRE00030038

- Categoría : Alimentos y bebidas

- Número de páginas : 145

- Formatos de informe disponibles :

[Informe de investigación] Se espera que el mercado de papas fritas congeladas crezca de US$ 39.955,11 millones en 2022 a US$ 57.910,15 millones en 2030; se espera que registre una CAGR del 4,7% de 2022 a 2030.

Perspectivas del mercado y opinión de analistas:

Las patatas fritas congeladas se elaboran a partir de patatas y se sirven calientes. Las patatas fritas se pueden fabricar y servir en diversas formas, como gofres, tiras rizadas y finas, y se comen como un tentempié práctico. Se sirven con ketchup, salsa y otros. Las patatas fritas se pueden hornear o freír. Además, los condimentos y aromas frescos y distintivos de las patatas fritas las ayudan a destacarse de la competencia y atraer a los clientes que buscan experiencias culinarias inexploradas. Los perfiles de sabor de las patatas fritas se pueden mejorar experimentando con diversas hierbas, especias y mezclas de condimentos, ampliando la selección de alternativas disponibles para satisfacer una variedad más amplia de preferencias de los consumidores. El crecimiento del mercado mundial de patatas fritas congeladas se atribuye al creciente número de empresas que ofrecen servicios de entrega de alimentos en línea, incluidas Food Panda, Swiggy, Uber Eats y otras. Han hecho que pedir alimentos sea una tarea fácil y adecuada para los consumidores. Además, se prevé que el aumento de los lanzamientos de productos por parte de los principales participantes de la industria impulse el mercado de las patatas fritas congeladas durante el período de pronóstico.

Factores impulsores del crecimiento y desafíos:

La cadena de frío, que consiste en el preenfriado, el almacenamiento refrigerado y el transporte refrigerado, es uno de los pilares de la cadena de manipulación poscosecha. Se considera la columna vertebral de cualquier industria poscosecha (desarrollada o en desarrollo) y un conjunto esencial de tecnologías para reducir las pérdidas de alimentos. La logística de la cadena de frío ha demostrado ser fundamental para cualquier país que busque aumentar su participación en el mercado de alimentos congelados . La infraestructura de la cadena de frío ha aumentado significativamente en los últimos años. Por ejemplo, según el informe del Instituto Internacional de Refrigeración (IIR) y la Alianza Global de la Cadena de Frío (GCCA), la capacidad total de los almacenes refrigerados a nivel mundial aumentó a 719 millones de metros cúbicos en 2020, un 16,7% más que la capacidad reportada en 2018.

Además, la expansión de la capacidad de la cadena de frío en los países emergentes difiere de un país a otro. En la mayoría de los países, como Sudáfrica, México y Kenia, la cadena de frío se concentra en áreas urbanas y terminales de transporte, como aeropuertos, donde pueden estar ubicados los exportadores. Además, los principales proveedores de servicios de mercado están mejorando constantemente sus tecnologías para mantenerse por delante de la competencia y mantener la eficiencia, la integridad y la seguridad en todo el mundo. Por ejemplo, los proveedores han implementado la tecnología de Análisis de Peligros y Puntos Críticos de Control (HACCP) e Identificación por Radiofrecuencia (RFID) para mejorar la eficiencia con envíos más pequeños. Además, están ampliando sus flotas de vehículos refrigerados de múltiples compartimentos para brindar servicios adicionales a los consumidores. Por lo tanto, se espera que los avances en la infraestructura de la cadena de frío ofrezcan oportunidades lucrativas para los actores del mercado de papas fritas congeladas, impulsando aún más el crecimiento de este mercado.

Personalice este informe según sus necesidades

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de patatas fritas congeladas: perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Segmentación y alcance del informe:

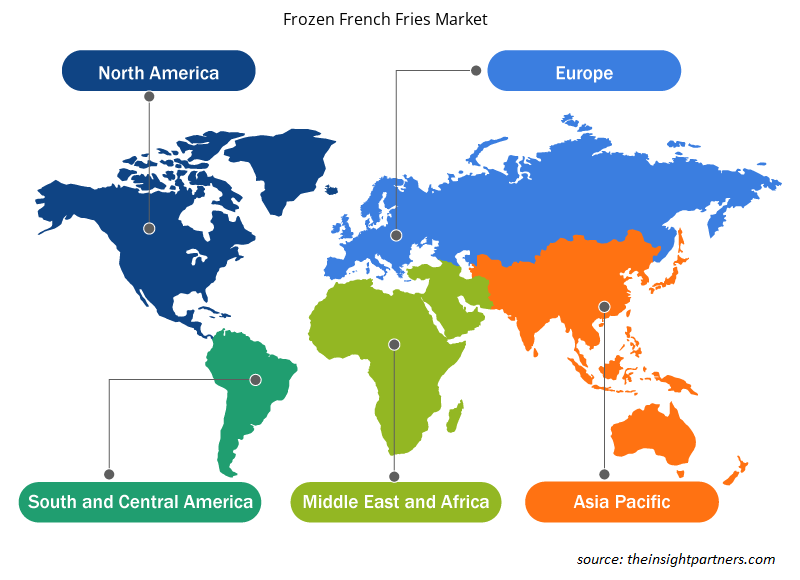

El “Mercado Global de Papas Fritas Congeladas” está segmentado en base al tipo de producto, categoría, usuario final y geografía. Según el tipo de producto, el mercado está segmentado en papas fritas regulares, papas fritas onduladas, papas fritas tipo bistec y otras. Según la categoría, el mercado está bifurcado en orgánico y convencional. Según el usuario final, el mercado de papas fritas congeladas está segmentado en venta minorista y servicio de alimentos. El mercado de papas fritas congeladas, según la geografía, está segmentado en América del Norte (Estados Unidos, Canadá y México), Europa (Alemania, Francia, Italia, el Reino Unido, Rusia y el resto de Europa), Asia Pacífico (Australia, China, Japón, India, Corea del Sur y el resto de Asia Pacífico), Oriente Medio y África (Sudáfrica, Arabia Saudita, los Emiratos Árabes Unidos y el resto de Oriente Medio y África), y América del Sur y Central (Brasil, Argentina y el resto de América del Sur y Central).

Análisis segmental:

Según el tipo de producto, el mercado de patatas fritas congeladas se segmenta en patatas fritas normales, patatas fritas onduladas, patatas fritas tipo bistec y otras. El segmento de patatas fritas normales tuvo la mayor participación en el mercado de patatas fritas congeladas en 2022 y se espera que registre una tasa de crecimiento significativa durante el período de pronóstico. Las patatas fritas normales en el mercado de patatas fritas congeladas son un acompañamiento popular en restaurantes de comida rápida, hamburgueserías y hogares. Las patatas fritas normales son más delgadas que las patatas fritas tipo bistec, generalmente se cortan en trozos de entre 1/8 y 1/4 de pulgada de grosor. A menudo se salan y se pueden servir con kétchup, vinagre, mayonesa, salsa de tomate u otras especialidades locales.

Análisis regional:

Según la geografía, el mercado de papas fritas congeladas se segmenta en cinco regiones clave: América del Norte, Europa, Asia Pacífico, América del Sur y Central, y Oriente Medio y África. El mercado mundial de papas fritas congeladas estuvo dominado por América del Norte y se estimó que rondaría los US$ 35.000 millones en 2022. Europa es el segundo contribuyente principal, con más del 25% de la participación del mercado. El mercado de papas fritas congeladas en América del Norte está segmentado en Estados Unidos, Canadá y México. El mercado de papas fritas congeladas de América del Norte está segmentado en Estados Unidos, Canadá y México. La región es uno de los principales mercados de papas fritas congeladas debido a la industria de procesamiento de alimentos bien establecida y las tendencias crecientes de consumo para llevar, cenar en el lugar y para llevar. Muchos fabricantes importantes de papas fritas congeladas, como HJ Heinz Company, JR Simplot Company y McCain Foods Limited, operan activamente en la región. Estas empresas han expandido su negocio en toda la región y tienen una participación de mercado significativa. Cuentan con una amplia red de distribución en la región, lo que les permite atender a muchos clientes. Por lo tanto, todos los factores mencionados anteriormente impulsan el crecimiento del mercado de papas fritas congeladas.

Desarrollos industriales y oportunidades futuras:

A continuación se enumeran varias iniciativas adoptadas por los actores clave que operan en el mercado de patatas fritas congeladas:

- En septiembre de 2020, Aviko BV adquirió una planta de patatas en Alemania del gigante de bienes de consumo Unilever. Esta planta procesa patatas para elaborar productos de marca como puré, albóndigas, ñoquis y snacks instantáneos.

- En octubre de 2022, Lamb Weston Holdings, Inc. anunció que había firmado un acuerdo para comprar las participaciones de capital restantes en su empresa conjunta europea Meijer Frozen Foods BV por US$ 763,58 millones.

- En julio de 2021, Lamb Weston modernizó su planta de papas fritas de Idaho con una inversión de US$ 415 millones. Esta línea de procesamiento permitirá a la planta de papas fritas de Idaho producir más de 350 millones de libras de papas fritas congeladas y otros productos de papa al año.

- En marzo de 2023, McCain anunció una inversión sustancial en Coaldale, duplicando el tamaño de sus instalaciones y producción en Coaldale, Alberta. La inversión reflejará el sólido crecimiento comercial de McCain.

Perspectivas regionales del mercado de patatas fritas congeladas

Los analistas de Insight Partners explicaron en detalle las tendencias y los factores regionales que influyen en el mercado de papas fritas congeladas durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de papas fritas congeladas en América del Norte, Europa, Asia Pacífico, Medio Oriente y África, y América del Sur y Central.

- Obtenga datos regionales específicos para el mercado de papas fritas congeladas

Alcance del informe de mercado de patatas fritas congeladas

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2022 | US$ 39,96 mil millones |

| Tamaño del mercado en 2030 | US$ 57,91 mil millones |

| CAGR global (2022-2030) | 4,7% |

| Datos históricos | 2020-2021 |

| Período de pronóstico | 2023-2030 |

| Segmentos cubiertos |

Por tipo de producto

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de papas fritas congeladas: comprensión de su impacto en la dinámica empresarial

El mercado de las papas fritas congeladas está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían sus ofertas, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

La densidad de actores del mercado se refiere a la distribución de las empresas o firmas que operan dentro de un mercado o industria en particular. Indica cuántos competidores (actores del mercado) están presentes en un espacio de mercado determinado en relación con su tamaño o valor total de mercado.

Las principales empresas que operan en el mercado de papas fritas congeladas son:

- Compañía de patatas de Bart

- Aviko BV

- Agristo NV.

- Compañía: Lamb Weston Holdings Inc.

- McCain

Descargo de responsabilidad : Las empresas enumeradas anteriormente no están clasificadas en ningún orden particular.

- Obtenga una descripción general de los principales actores clave del mercado de papas fritas congeladas

Impacto del COVID-19:

La pandemia de COVID-19 afectó a las economías e industrias de varios países. Los confinamientos, las prohibiciones de viajes y los cierres de empresas en los principales países de América del Norte, Europa, Asia Pacífico (APAC), América del Sur y Central (SAM) y Oriente Medio y África (MEA) afectaron negativamente al crecimiento de varias industrias, incluidas las de alimentos y bebidas. El cierre de las unidades de fabricación perturbó las cadenas de suministro globales, las actividades de fabricación, los cronogramas de entrega y las ventas de varios productos esenciales y no esenciales. Varias empresas anunciaron posibles retrasos en las entregas de productos y una caída en las ventas futuras de sus productos en 2020. Además, las prohibiciones impuestas por varios gobiernos en Europa, Asia y América del Norte a los viajes internacionales obligaron a las empresas a suspender temporalmente sus planes de colaboración y asociación.

Panorama competitivo y empresas clave:

Entre los actores destacados que operan en el mercado mundial de papas fritas congeladas se encuentran Bart's Potato Company, Aviko BV, Agristo NV., Lamb Weston Holdings Inc, McCain, Farm Frites International BV, Rairandev Golden Fries Pty Ltd, Himalaya Food International Ltd, JR Simplot Company y The Kraft Heinz Co. Estos fabricantes de papas fritas congeladas ofrecen opciones de snacks de vanguardia con formas innovadoras para brindar una experiencia superior a los consumidores.

- Análisis histórico (2 años), año base, pronóstico (7 años) con CAGR

- Análisis PEST y FODA

- Tamaño del mercado, valor/volumen: global, regional y nacional

- Industria y panorama competitivo

- Conjunto de datos de Excel

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias

Desbloquea descuentos exclusivos en informes

Consultar ahora

Obtenga una muestra gratuita para - Mercado de papas fritas congeladas

Obtenga una muestra gratuita para - Mercado de papas fritas congeladas