Strategie di mercato degli elettrodi di grafite, principali attori, opportunità di crescita, analisi e previsioni entro il 2027

Previsioni di mercato degli elettrodi di grafite fino al 2027 - Impatto del COVID-19 e analisi globale per tipo di prodotto (alta potenza, altissima potenza, potenza normale); applicazione (forno ad arco elettrico, forno a siviera, altri) e geografia

- Stato : Edito

- Codice del report : TIPRE00014019

- Categoria : Prodotti chimici e materiali

- Numero di pagine : 142

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : June 19, 2024

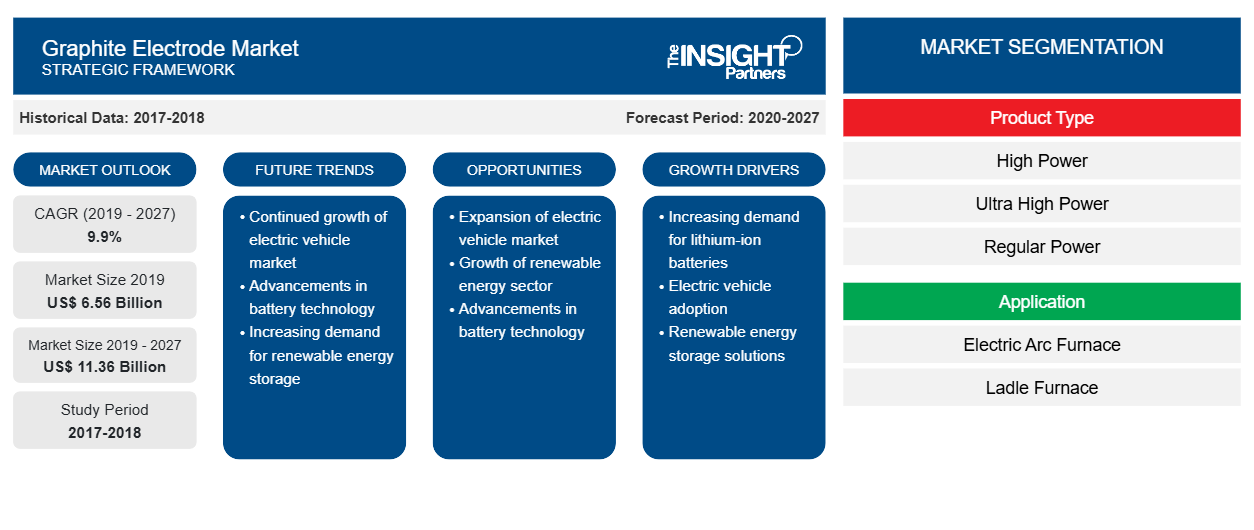

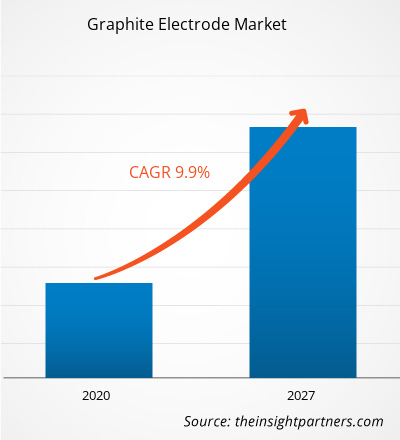

[Rapporto di ricerca] In termini di fatturato, il mercato degli elettrodi di grafite è stato valutato a 6.564,2 milioni di dollari nel 2019 e si prevede che raggiungerà 11.356,4 milioni di dollari entro il 2027 con un CAGR del 9,9% dal 2020 al 2027.

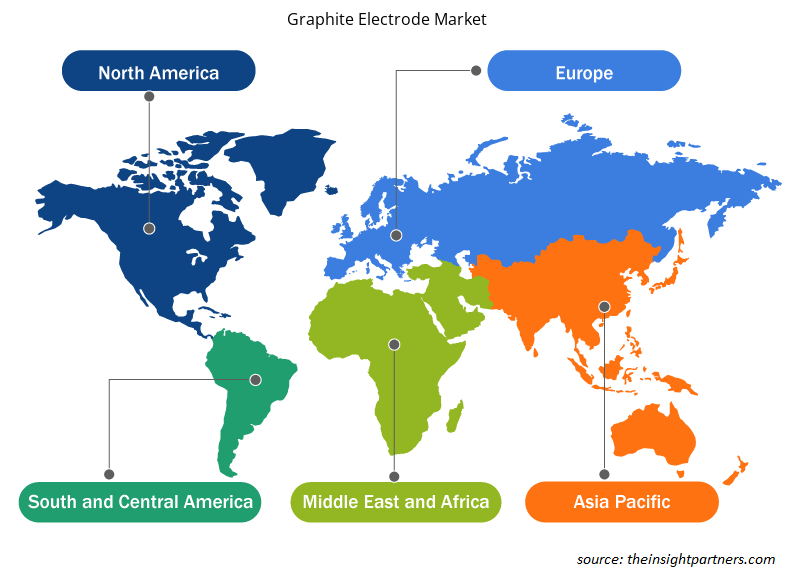

Il mercato globale degli elettrodi di grafite è dominato dalla regione Asia-Pacifico che rappresenta circa il 58% del mercato globale degli elettrodi di grafite complessivamente. L'elevata domanda di elettrodi di grafite da parte di questi paesi è attribuita al forte aumento della produzione di acciaio grezzo. Secondo la World Steel Association, nel 2018, Cina e Giappone hanno prodotto rispettivamente 928,3 e 104,3 milioni di tonnellate di acciaio grezzo. Nella regione APAC, i forni ad arco elettrico hanno una domanda significativa a causa dell'aumento dei rottami di acciaio e dell'aumento della fornitura di energia elettrica in Cina. Le crescenti strategie di mercato di varie aziende nella regione APAC stanno incoraggiando la crescita del mercato degli elettrodi di grafite nella regione. Ad esempio, Tokai Carbon Co., Ltd., un'azienda giapponese, ha acquisito l'attività di elettrodi di grafite di SGL GE Holding GmbH (SGL GE), al costo di 150 milioni di dollari USA.

I governi dei principali paesi europei hanno adottato varie iniziative per far progredire i loro settori manifatturiero, dell'elettronica e dei semiconduttori, tra gli altri. L'Europa ha notevolmente migliorato le sue soluzioni industriali attraverso le iniziative Industry 4.0. La Commissione europea si sta concentrando sull'aumento dei finanziamenti per la R&S per rafforzare la competitività del settore manifatturiero e di altri settori della regione nel mondo. La domanda di elettrodi di grafite è direttamente collegata alla produzione di acciaio nei forni ad arco elettrico e la regione è uno dei produttori di acciaio cruciali al mondo, con la Russia come produttore maggiore.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato degli elettrodi di grafite: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Impatto della pandemia di COVID-19 sul mercato degli elettrodi di grafite

Secondo l'ultimo rapporto sulla situazione dell'Organizzazione mondiale della sanità (OMS), Stati Uniti, India, Spagna, Italia, Francia, Germania, Regno Unito, Russia, Turchia, Brasile, Iran e Cina sono tra i paesi più colpiti dall'epidemia di COVID-19. L'epidemia è iniziata a Wuhan (Cina) nel dicembre 2019 e da allora si è diffusa rapidamente in tutto il mondo. La crisi del COVID-19 sta colpendo le industrie in tutto il mondo e si prevede che l'economia globale subirà il colpo peggiore nel 2020 e probabilmente nel 2021. L'epidemia ha creato notevoli interruzioni nell'industria siderurgica. Il forte calo del commercio internazionale sta influenzando negativamente la crescita dell'elettrodo di grafite. Le chiusure della produzione, le restrizioni sulla catena di fornitura, la gestione degli acquisti, la scarsità di manodopera e i blocchi delle frontiere per combattere e contenere l'epidemia hanno influenzato negativamente il settore delle costruzioni. Il rallentamento della produzione nel settore delle costruzioni sta influenzando direttamente l'adozione di vari prodotti in acciaio, influenzando così il mercato degli elettrodi di grafite.

Approfondimenti di mercato

La transizione nell'industria siderurgica cinese sostiene la crescita del mercato degli elettrodi di grafite

Nel 2016 e nel 2017, la scena dell'industria siderurgica cinese è stata plasmata dal rifiuto guidato dalla politica del potenziale IF mentre il governo si sforzava di iscrivere un eccesso di offerta nazionale. Secondo worldsteel.org, il consumo di rottami di acciaio nelle acciaierie EAF e BOF (basic oxygen furnace) ha toccato un record di oltre 200 milioni di tonnellate metriche all'anno. Nel frattempo, la capacità EAF della Cina ha rinunciato a un nuovo apice di 130 milioni di tonnellate metriche all'anno poiché le normative governative limitano la generazione da parte di acciaierie integrate in aree chiave e promuovono la loro vigorosa sostituzione con la capacità EAF. Ciò ha dato origine alla produzione di acciaio EAF, favorendo così la crescita del mercato degli elettrodi di grafite.

Informazioni basate sul tipo di prodotto

In termini di tipologia di prodotto, il segmento ad altissima potenza ha conquistato la quota maggiore del mercato globale degli elettrodi di grafite nel 2019. L'elettrodo di grafite ad altissima potenza viene utilizzato per il riciclaggio dell'acciaio nel settore dei forni ad arco elettrico (EAF). Il suo costituente principale è il coke ad aghi di alto valore, prodotto da petrolio o catrame di carbone. Gli elettrodi di grafite sono perfezionati con una forma cilindrica e realizzati con aree filettate a ciascuna estremità. In questo modo, gli elettrodi di grafite possono essere assemblati in una colonna di elettrodi utilizzando i nippli degli elettrodi. Per soddisfare il requisito di costi inferiori e maggiore efficienza lavorativa, i forni ad arco ad altissima potenza di grande capacità stanno diventando sempre più popolari. Pertanto, si prevede che gli elettrodi di grafite ad altissima potenza detengano la quota maggiore del mercato degli elettrodi di grafite. Inoltre, si prevede che il segmento assisterà alla crescita CAGR più elevata nel mercato degli elettrodi di grafite.

Approfondimenti basati sulle applicazioni

In base all'applicazione, il mercato degli elettrodi di grafite è segmentato in forno ad arco elettrico, forno a siviera e altri. Si stima che il segmento del forno ad arco elettrico crescerà al CAGR più elevato durante il periodo di previsione. L'elettrodo di grafite è un componente indispensabile della produzione di acciaio tramite il metodo del forno ad arco elettrico (EAF) e la purificazione dell'acciaio del forno a siviera. Gli elettrodi di grafite sono utilizzati anche per la produzione di metallo ferroso non acciaioso, ferrolega, metallo di silicio e fosforo giallo. L'elettrodo di grafite è un materiale di consumo indispensabile nella produzione di acciaio EAF, ma è necessario in quantità molto piccole; una tonnellata di produzione di acciaio necessita solo di ~1,7 kg di elettrodo di grafite. Il segmento detiene oltre l'80% della quota di mercato totale degli elettrodi di grafite.

Il mercato degli elettrodi di grafite è altamente consolidato, con solo un certo numero di attori che dominano il mercato degli elettrodi di grafite. Di seguito sono elencati alcuni degli sviluppi recenti nel mercato degli elettrodi di grafite:

2020: Tokai Carbon e Tokai COBEX hanno completato l'acquisizione di Carbone Savoie International SAS, un produttore di carbonio e grafite.

2020: Il consiglio di amministrazione di GrafTech International Ltd. ha approvato il riacquisto di un massimo di 100 milioni di $ di azioni ordinarie della società in acquisti sul mercato aperto.

2019: Showa Denko (SDK) ha completato l'acquisizione di tutte le azioni di SGL GE Holding GmbH, una società di produzione di elettrodi di grafite. Dopo l'acquisizione, il nome della società è cambiato in SHOWA DENKO CARBON Holding GmbH.

Approfondimenti regionali sul mercato degli elettrodi di grafite

Le tendenze regionali e i fattori che influenzano il mercato degli elettrodi di grafite durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del mercato degli elettrodi di grafite in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e America meridionale e centrale.

- Ottieni i dati specifici regionali per il mercato degli elettrodi di grafite

Ambito del rapporto di mercato degli elettrodi di grafite

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2019 | 6,56 miliardi di dollari USA |

| Dimensioni del mercato entro il 2027 | 11,36 miliardi di dollari USA |

| CAGR globale (2019 - 2027) | 9,9% |

| Dati storici | 2017-2018 |

| Periodo di previsione | 2020-2027 |

| Segmenti coperti |

Per tipo di prodotto

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli attori del mercato degli elettrodi di grafite: comprendere il suo impatto sulle dinamiche aziendali

Il mercato degli elettrodi di grafite sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato degli elettrodi di grafite sono:

- Gruppo EPM

- GRAFTECH INTERNAZIONALE LTD

- Grafite India Limited

- HEG limitata

- Società di Carbonio Kaifeng, Ltd.

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato degli elettrodi di grafite

Segmentazione del mercato

Mercato degli elettrodi di grafite – Per tipo di prodotto

- Alta potenza

- Potenza ultra elevata

- Potenza regolare

Mercato degli elettrodi di grafite – per applicazione

- Forno ad arco elettrico

- Forno a siviera

- Altri

Mercato degli elettrodi di grafite per regione

-

America del Nord

- NOI

- Canada

- Messico

-

Europa

- Francia

- Germania

- Italia

- Regno Unito

- Russia

- Resto d'Europa

-

Asia Pacifico (APAC)

- Cina

- India

- Corea del Sud

- Giappone

- Australia

- Resto dell'APAC

-

Medio Oriente e Africa (MEA)

- Sudafrica

- Arabia Saudita

- Emirati Arabi Uniti

- Resto del MEA

-

America del Sud (SAM)

- Brasile

- Argentina

- Resto del SAM

Le aziende profilate nel mercato degli elettrodi di grafite sono le seguenti:

- Gruppo EPM

- GrafTech International Ltd

- Grafite India Limited

- Società a responsabilità limitata

- Kaifeng Carbon Co., Ltd, Gruppo energetico e chimico Zhongping (KFCC)

- Nantong Yangzi Carbon Co., Ltd.

- Nippon Carbon Co Ltd.

- Sangraf Internazionale

- SHOWA DENKO KK

- Azienda: Tokai Carbon Co., Ltd.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative