自動車用電子機器市場の動向、シェア、需要予測(2034年まで)

自動車エレクトロニクス市場規模と予測(2021年~2034年)、世界および地域別シェア、トレンド、成長機会分析レポート 対象範囲:タイプ別(ECU/DCU、センサー、パワーエレクトロニクス、その他)、用途別(ボディ、シャシー、パワートレイン、インフォテインメント、ADAS/AD、その他)、車種別(乗用車、商用車)

- ステータス : 公開されたデータ

- レポートコード : TIPAT00002369

- カテゴリー : エレクトロニクスおよび半導体

- ページ数 : 150

- 利用可能なレポート形式 :

- 最終更新日 : July 17, 2026

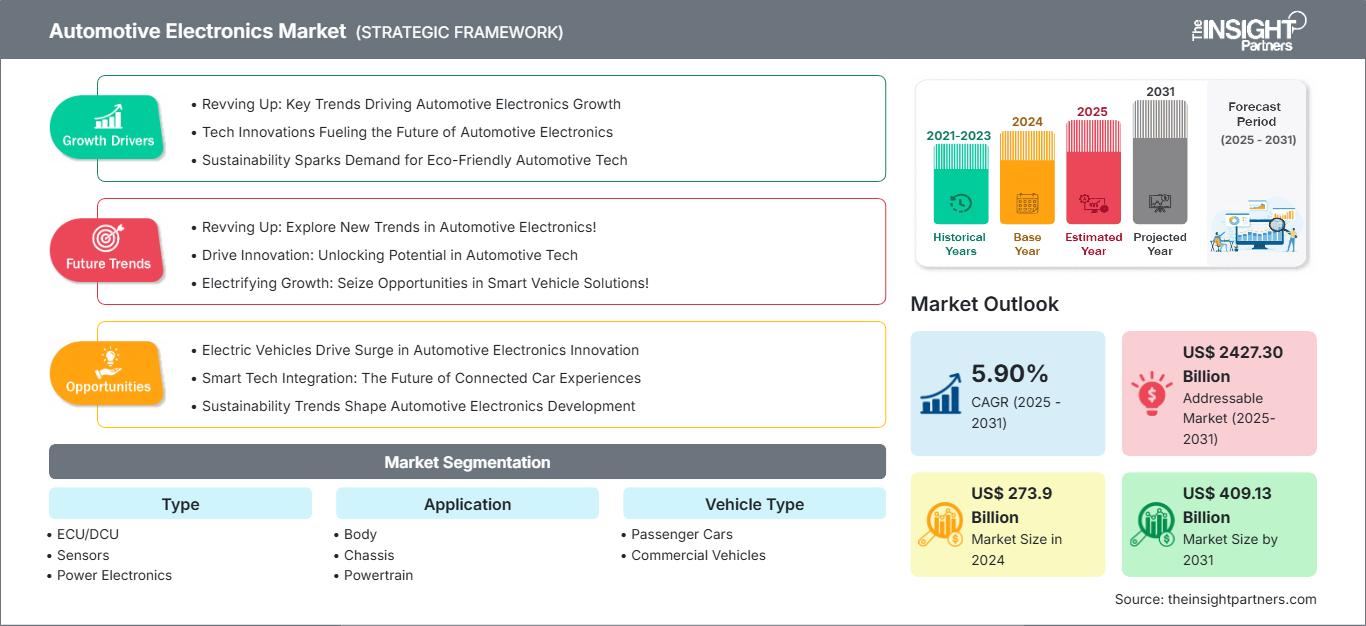

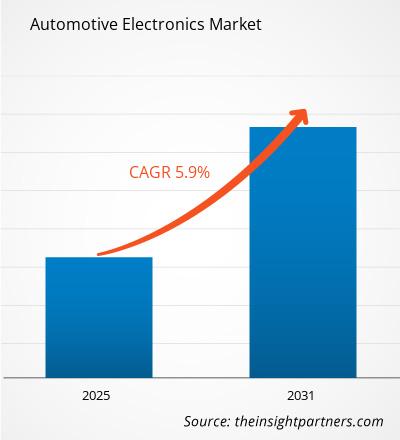

2025年の市場規模

3259億7000 万泊

基準年値

2034年の予測

6,641億4,000 万泊

2034年までに予測される

2026年~2034年の平均成長率(CAGR)

8.23 %

成長率

対象市場

4兆4481億1000 万兆

(2026年~2034年)

自動車用電子機器の市場規模は、2025年には3,259億7,000万万に達すると予想されており、2034年には6,641億4,000万に達すると予測されています。2026年から2034年の期間における年平均成長率(CAGR)は8 .23%です。主な成長率は、ECU、センサー、パワーエレクトロニクス、インフォテインメント、ADASおよびADシステム、ボディエレクトロニクス、シャシー制御、パワートレイン制御、そして乗用車と商用車の両方における電子機器の使用増加です。

北米は、ローカルソフトウェア駆動型プラットフォーム、電動パワートレイン、安全電子機器といった分野で、引き続き重要な拠点であり続けています。 北米市場は、2026年から2034年の予測期間において、年平均成長率(CAGR)7.4%~8.4%を記録すると予測されています。

自動車用電子機器市場の評価と洞察

- 北米は2025年に自動車エレクトロニクス市場の25%~29%のシェアを確保、EVプラットフォーム、ADASコンテンツ、および現地の半導体政策に取り組まれ、2026年から2034年の間に平均成長率(CAGR)7.4%~8.4%で成長すると予測されている。

- アメリカは2025年には北米の78%~83%を目安に、2026年から2034年にかけて年平均成長率(CAGR)7.5%~8.5%で成長すると予測されている。

- 欧州は2025年には23%~27%のシェアを留保、ドイツ、フランス、英国、イタリア、スペインが牽引役となり、2026年から2034年にかけて年平均成長率(CAGR)7.0%~8.0%で成長すると予測されている。

- アジア太平洋地域は2025年には38%~42%のシェアを留保、中国、日本、韓国、インド、オーストラリアに支えられ、2026年から2034年にかけて年平均成長率(CAGR)8.8%~9.8%で成長すると予測されている。

- 最大のアセトンであるECU/DCUは、2025年には34%~38%の市場シェアを確保、2026年から2034年までのCAGRは7.8%~8.8%の範囲になると予測されている。

- 高成長期であるADAS/ADは、2025年には15%~19%の市場シェアを確保、2026年から2034年までのCAGRは10.2%~11.2%の範囲になると予測されている。

- 詳細に分析された主要企業:デンソー株式会社、HGMオートモーティブエレクトロニクス、日立製作所、インフィニオン・テクノロジーズAG、マイクロチップ・テクノロジー社、NXPセミコンダクターズNV、ロバート・ボッシュGmbH、ソニー・インディアPvt. Ltd.、テキサス・インスツルメンツ社、ZFフリードリヒスハーフェンAG。

出典: The Insight Partnersによる独自の調査、政府研究所、企業の年次報告書、投資家向けプレゼンテーション、業界、データベース、専門家へのインタビューに基づいた分析。

車載エレクトロニクスは、スタンドアロンモジュールから、制御、センシング、通信、ソフトウェア実行が統合されたドメイン、ゾーン、集中型アプローチへと進化を遂げました。 現在の製造動向は、ECUの統合、センサーフュージョン、車載用パワーコンポーネント、そして長期サイクルでのコンポーネント認定などです。

今後数年間で最も急速な成長が見込まれるのは、電動化、運転支援、コネクテッドカーネットワークが重なり合う分野です。アジア太平洋地域の製造規模、欧州の排出ガス規制、北米の現地生産奨励プログラムが相まって、パワーエレクトロニクス、ADASコントローラー、インテリジェントコックピット、ネットワーク技術への投資が促進されています。車両1台あたりの電子部品搭載量の増加が市場を支えている一方で、サプライヤーは信頼性、ソフトウェアテスト、サイバーセキュリティ、コストといった課題への対応が求められています。

自動車エレクトロニクス市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2025年の市場規模 | 3259億7000万米ドル |

| 2034年までの市場規模 | 6,641億4,000万米ドル |

| 世界の年間平均成長率(2026年~2034年) | 8.23% |

| 履歴データ | 2021年~2024年 |

| 予測期間 | 2026年~2034年 |

自動車用電子機器市場分析

需要を牽引する要因としては、電動推進システム、デジタルコックピット、ADASセンサー、バッテリー管理、ボディコントロール、セキュアな車両接続などが挙げられます。自動車エレクトロニクス市場の成長は、分散型電子制御ユニットからドメインコントローラーへの移行と密接に関係しています。あらゆる自動車プログラムにおいて、機能安全、電磁両立性、耐熱性、サイバーセキュリティ、そして様々なグレードや地域における長寿命といった課題に対応できるエレクトロニクスが求められています。

このエコシステムは、半導体メーカー、センサーメーカー、ECU統合メーカー、パワーエレクトロニクスメーカー、ソフトウェアツールメーカー、ティア1モジュールメーカー、そして自動車メーカーで構成されています。供給ダイナミクスは、地域における高品質な部品、拡張性の高いリファレンスデザイン、そしてエンジニアリングサポートによって好影響を受けています。車両プラットフォームのライフサイクルが長いため、性能や小型化と同様に、供給体制も非常に重要です。

主要な競合企業には、幅広い製品ポートフォリオとOEM認定実績を持つ自動車関連サプライヤーが含まれます。具体的には、デンソー株式会社、ロバート・ボッシュ社、ZFフリードリヒスハーフェン社、インフィニオン・テクノロジーズ社、NXPセミコンダクターズ社、テキサス・インスツルメンツ社、マイクロチップ・テクノロジー社、日立製作所、ソニー・インディア社、HGMオートモーティブ・エレクトロニクス社などが挙げられ、これらの企業はECU、センサー、パワーコンポーネント、イメージングソリューション、制御ソフトウェア、およびシステム統合技術を用いて競合しています。

投資動向としては、SiCパワーモジュール、レーダーおよびビジョンセンシング、車載イーサネット、コックピットインテリジェンス、バッテリー管理、柔軟な電子制御ソリューションなどが挙げられます。市場評価におけるサプライヤーの評価では、サプライヤーの堅牢性、製造拠点、セキュリティ能力、ソフトウェアサポートなどが考慮されます。戦略的なポジショニングにおいては、ADAS/ADアプリケーションをサポートするための高性能コンピューティングと、その他の車載システム向けのコスト効率の高い電子機器との間でトレードオフが生じます。

● レポートのカスタマイズ

貴社の具体的なビジネス要件に合わせて、このレポートをカスタマイズしてください。

本レポートは、お客様の事業目標、事業範囲、ターゲット市場に合わせてカスタマイズ可能です。カスタマイズオプションには、顧客セグメントの絞り込み、地域別分析、競合分析、戦略的洞察などがあり、情報に基づいた意思決定を支援します。

このレポートをカスタマイズする →調整可能な項目

- ● セグメンテーション

- ● 地理

- ● 競合分析

- ● 言語設定

自動車エレクトロニクス市場:戦略的洞察

地域別分析

北米自動車エレクトロニクス市場

北米地域は2025年に市場シェアの25%~29%を占め、2026年から2034年にかけて7.4%~8.4%の成長が見込まれています。これは自動車エレクトロニクス市場における北米の市場シェアを示しており、車両ソフトウェア、アナログ回路、コネクテッドソリューション、先進安全システムにおいて米国が優位を占めていることを示しています。需要を牽引する要因としては、電気ピックアップトラック、商用フリートのテレマティクス、デジタルインストルメントクラスター、バッテリー管理システム、レベル2+の安全機能などが挙げられます。

現地の顧客は、コネクテッドカーにおける供給の安定性、エンジニアリングの専門知識、およびサイバーセキュリティに関するポリシーとの整合性を求めている。主要サプライヤーには、NXPセミコンダクターズ、テキサス・インスツルメンツ、マイクロチップ・テクノロジー、デンソー、ロバート・ボッシュなどがある。用途としては、レーダーセンシングや電力変換ソリューションなどが挙げられる。自動車メーカーは、各車両における電子機器の搭載量増加に伴い、長期的な供給状況の可視性に対する要求を高めている。

米国自動車エレクトロニクス市場

2025年には北米の需要の78%~83%を米国が占め、7.5%~8.5%の成長が見込まれています。用途のトレンドとしては、ADASプロセッサチップ、車載イーサネット、バッテリー管理、インフォテインメントコントローラ、電源管理ICなどが挙げられます。米国の半導体設計能力と車両ソフトウェア開発能力は、先進的な電子アーキテクチャに不可欠な要素となっています。

これらの企業は事業を多角化しており、テキサス・インスツルメンツやマイクロチップ・テクノロジーはアナログ半導体、MCU、接続チップを提供し、NXPセミコンダクターズはレーダーとネットワークのサポートを提供している。デンソー、ロバート・ボッシュ、ZFフリードリヒスハーフェンはシステム統合のサポートを提供している。自動車メーカーは、供給と機能安全性を確保するために、エレクトロニクス分野への関与を拡大している。

欧州自動車エレクトロニクス市場

欧州セグメントは2025年に23~27%の市場シェアを占め、7.0~8.0%の成長が見込まれています。ドイツセグメントは、高級車、EVパワーエレクトロニクス、安全装置、車載半導体設計といった分野で圧倒的なシェアを誇っています。フランスは電動化プラットフォームを提供し、英国は先進的な推進技術、コネクティビティ、自動車設計能力に注力しています。

イタリアとスペインのセグメントは、自動車製造、産業用電子機器、および欧州のOEMへの部品供給を通じて市場を支えています。インフィニオン・テクノロジーズ、ロバート・ボッシュ、ZFフリードリヒスハーフェン、NXPセミコンダクターズ、デンソーは、パワートレイン、シャシー、ボディエレクトロニクス、および安全関連のニーズに対応しています。この地域の環境および安全規制が市場を牽引するでしょう。

アジア太平洋地域の自動車エレクトロニクス市場

アジア太平洋地域は2025年も38~42%のシェアを維持し、8.8~9.8%の成長が見込まれる。中国はEV販売台数、国内エレクトロニクス戦略、インテリジェントコックピットの迅速な導入において優れている。日本と韓国はセンサー、ECU、ディスプレイ、パワーエレクトロニクスの専門知識を有し、インドとオーストラリアは車載エレクトロニクス需要の伸びを牽引する。

産業政策、バッテリー製造チェーン、そして乗用車の輸出志向型生産が引き続き市場を牽引している。デンソー、日立製作所、ソニー・インディア、インフィニオン・テクノロジーズ、NXPセミコンダクターズなどが競合企業として名を連ね、新たな地域企業も参入している。乗用車向けパワートレイン、ADAS/AD、ボディエレクトロニクス、インフォテインメントソリューションへの需要が最も高い。

中東・アフリカ自動車エレクトロニクス市場

中東・アフリカ地域は、UAEのコネクテッドモビリティ、高級車の輸入、スマートインフラ整備に牽引され、年平均成長率(CAGR)6.5%~7.5%の成長が見込まれる。サウジアラビアは自国の自動車生産能力と電気自動車開発に投資しており、南アフリカは引き続き自動車生産の主要拠点となっている。

中東・アフリカのその他の地域では、市場は商用車両、テレマティクス、車載エレクトロニクス、車両のアップグレードといった分野と密接に関連している。エネルギー関連国は、EV充電、車両の電動化、高度道路交通システム(ITS)の導入を検討しており、これにより電子機器の利用が拡大する見込みだ。

セグメンテーション分析

タイプ

2026年から2034年にかけて、このタイプの市場は7.9%~8.9%の成長が見込まれています。自動車用電子機器市場の範囲は、ECU/DCU、センサー、パワーエレクトロニクスに及び、需要は車両アーキテクチャの統合、電動化、リアルタイムセンシング、ソフトウェア制御機能によって形成されています。制御、センシング、電力変換が拡張可能なプラットフォームに統合されている分野で、最も高い成長が見込まれます。

- ECU/DCUは、集中制御、ドメインコンピューティング、ボディ管理、シャシー監視、パワートレイン調整といった機能が、信頼性の高い車載グレードの処理能力とソフトウェア統合に依存しているため、最大のシェアを占めている。

- センサーは、先進運転支援システム(ADAS)、車体快適性、シャシー制御、バッテリー監視、およびキャビンインテリジェンスを支えており、車両が自動的な意思決定のために、より豊富なリアルタイムデータを必要とするにつれて、安定した需要を生み出している。

- パワーエレクトロニクスは、ハイブリッド車や電気自動車のアーキテクチャにおいて、インバーター、車載充電器、DC-DCコンバーター、バッテリーシステム、熱管理などを通じて、戦略的に重要な役割を担うようになっている。

応用

アプリケーション市場は、2026年から2034年にかけて8.4%~9.4%の成長が見込まれています。需要は、車体、シャシー、パワートレイン、インフォテインメント、ADAS/ADシステムなど、幅広い分野に及んでいます。中でもADAS/ADは、レーダー、カメラ、ドメインコントローラー、ブレーキ監視システムが高級車からより幅広い乗用車や商用車へと普及するにつれ、最も急速に成長しています。

- 車体電子機器は、照明、窓、空調制御、シートモジュール、アクセスシステム、快適性機能などを通じて安定した需要を生み出し、コスト効率の高いコントローラーとセンサーを必要とする。

- シャーシ関連のアプリケーションでは、安定性制御、ステアリング、サスペンション、ブレーキインターフェース、センサーフュージョンなどに電子機器が使用され、より安全なハンドリングと高い車両ダイナミクス性能を実現しています。

- 内燃機関車、ハイブリッド車、電気自動車を問わず、エンジン制御、インバーター管理、バッテリー監視、車載充電、熱管理システムなどを通じて、パワートレインの需要が高まっている。

- インフォテインメントシステムは、接続性、ナビゲーション、ディスプレイ、オーディオ、車両データサービス、無線によるアップデートなどをサポートしており、コックピットエレクトロニクスは重要な価値創造の源泉となっている。

- カメラ、レーダー、ドメインコントローラー、ドライバーモニタリング、ブレーキ監視が安全機能および差別化機能の中核となるにつれ、ADAS/ADは戦略的に重要になってきている。

車両タイプ

車両タイプ別では、2026年から2034年にかけて7.7%~8.7%の成長が見込まれています。乗用車は、インフォテインメント、先進運転支援システム(ADAS)、電動化、快適システムなどの普及により、電子機器消費の大半を占めています。商用車は、車両テレマティクス、安全規制、エネルギー管理、予知保全、そしてますます高度化する物流業務によって、成長を加速させています。

- 乗用車は最大の需要基盤を牽引しており、これは量販モデルと高級モデルの両方に、先進運転支援システム(ADAS)、デジタルコックピット、バッテリー管理、ボディコントロール、コネクティビティ電子機器がますます搭載されるようになっているためである。

- 商用車は、運行効率を高めるために、車両運行事業者がテレマティクス、運転支援システム、電動パワートレイン、予知保全、安全電子機器などを採用するにつれて、戦略的重要性が高まっている。

機会の概要

|

応用 |

収益貢献 |

トレンドタグ |

導入段階 |

|

体 |

中くらい |

スマートな快適さ |

成熟した |

|

シャーシ |

中くらい |

ブレーキ制御 |

スケーリング |

|

パワートレイン |

高い |

EVインバーター |

スケーリング |

|

インフォテインメント |

高い |

コネクテッドコックピット |

スケーリング |

|

ADAS/AD |

高い |

センサーフュージョン |

スケーリング |

自動車用電子機器市場の成長要因と影響分析

電動化により車両1台あたりの電子機器の価値が上昇する

電気自動車やハイブリッド車は、トラクションインバータ、バッテリー管理システム、車載充電器、温度制御、DC-DCコンバータなど、すべて車載グレードの部品に依存するため、従来型モデルよりも大幅に多くの電子制御を必要とします。その影響は、パワートレイン、シャシー、安全電子機器全体に及び、サプライヤーは高電圧動作、機能安全、長期にわたる認証サイクルに対応しなければなりません。インフィニオン・テクノロジーズ、デンソー、日立製作所、テキサス・インスツルメンツは、電力およびアナログ需要の恩恵を受けており、自動車メーカーは複数年にわたるEVプラットフォーム向けの安定した供給を求めています。この要因により、ユニット需要と車両1台あたりの平均電子機器価値の両方が拡大しています。

ADASの普及拡大に伴い、センサーとコンピューティングの要件が拡大する

安全規制、消費者評価、そしてOEMの差別化により、運転支援機能はより多くの車種に搭載されるようになっています。カメラ、レーダー、超音波センサー、ブレーキコントローラー、ドメインプロセッサーには、リアルタイムでデータを確実に処理できるセンサー、ECU、メモリ、アナログインターフェースが必要です。NXP Semiconductors NV、Sony India Pvt. Ltd.、Microchip Technology Inc.、ZF Friedrichshafen AGは、センシング、制御、および安全要件を中心に事業を展開しています。市場への影響としては、設計の複雑化、ソフトウェア検証期間の長期化、機能安全およびサイバーセキュリティ要件を満たす電子機器への需要の高まりなどが挙げられます。

ソフトウェア定義車両がネットワークアーキテクチャを再構築する

自動車メーカーは、断片化された電子制御ユニットを、高帯域幅通信、集中型コンピューティング、セキュアゲートウェイ機能に依存するドメインおよびゾーンアーキテクチャに置き換えつつあります。この変化により、車載イーサネット、ドメインコントローラ、電源管理、組み込みセキュリティ、ソフトウェア互換エレクトロニクスに対する需要が高まっています。インフィニオン・テクノロジーズAGによるマーベルの車載イーサネット事業の買収は、サプライヤーがソフトウェア定義型車両ネットワークに向けてどのように再編を進めているかを示しています。その商業的影響はハードウェアにとどまらず、ベンダーはソフトウェアスタック、リファレンスデザイン、アップデートパス、長期的なプラットフォーム互換性をサポートする必要があります。

自動車用電子機器市場の将来動向

集中型コンピューティングプラットフォームが主流の車両に搭載される

自動車エレクトロニクス市場のトレンドは、インフォテインメント、ADAS/AD、ボディコントロール、コネクティビティといったワークロードを統合する集中型コンピューティングプラットフォームへとますますシフトしていくでしょう。コスト、安全性、熱に関する制約が解消されれば、主流の車両はスケーラブルなプロセッサと、様々な重要度に対応したソフトウェア環境を採用するようになります。このトレンドは、エレクトロニクス、開発ツール、セキュリティ機能、そしてエコシステムパートナーシップを兼ね備えたサプライヤーに有利に働きます。また、部品ごとの調達から、複数のモデル、ソフトウェアアップデート、地域ごとの機能バリエーションをサポートするプラットフォームロードマップに基づく調達へと移行していくでしょう。

センサーフュージョンが安全性の差別化における重要な要素となる

将来の車両安全システムは、レーダー、カメラ、超音波、車内センシングデータのより高度な融合に依存するようになるでしょう。この変化により、同期センサー、エッジ処理、高速ネットワーク、ソフトウェア検証環境への需要が高まります。NXP Semiconductors NVとSony India Pvt. Ltd.はレーダーおよびイメージング層に関連し、ZF Friedrichshafen AGとRobert Bosch GmbHはセンシングをブレーキおよびシャシー機能に接続します。OEM各社が性能、コスト、規制要件、消費者の受容性のバランスを取るにつれて、採用は徐々に進んでいくでしょう。

自動車用電子機器市場の機会

電気自動車および先進運転支援システム(ADAS)プラットフォーム向け長期供給契約

自動車メーカーは、特にEV用パワーエレクトロニクス、ADAS/ADコントローラー、安全性が重要なECUなど、プラットフォームリスクが高い分野では、より長期的な電子機器供給契約を結ぶ意欲を示しています。自動車用電子機器市場の予測では、専用の生産能力計画、車載パッケージング、ソフトウェア検証、および割り当ての可視性を向上させる共同開発契約への投資が推奨されています。サプライヤーは、設計サポート、セカンドソース戦略、ライフサイクルコミットメント、および透明性の高い認定ロードマップを提供することで差別化を図ることができます。検証済みの電子機器プラットフォームが、地域やモデルイヤーを問わず複数の車種に対応できる場合、最も魅力的な機会となります。

サイバーセキュリティ接続およびテレマティクス電子機器

コネクテッドカーには、機能安全性を損なうことなく、セキュアなゲートウェイ、テレマティクス制御ユニット、暗号化通信、リモート診断をサポートする電子機器が必要です。コネクテッドカーのデータフローに対する規制当局の監視強化に伴い、セキュアなハードウェアの信頼の基点、車載イーサネット、アップデート可能なアーキテクチャの価値が高まっています。NXPセミコンダクターズ、マイクロチップ・テクノロジー、テキサス・インスツルメンツ、ロバート・ボッシュは、セキュアな通信、電源、インターフェースのニーズに対応できます。電子機器、セキュリティ関連文書、ソフトウェアの有効化を組み合わせたサプライヤーは、乗用車や商用車におけるコネクティビティの標準化に伴い、大きな価値を獲得できるでしょう。

最近の動向

- 2026年6月:NXPセミコンダクターズNVは、車載レーダーシステムオンチップ「SAF8444」を発表し、センサー上でのL2/L2+ ADAS処理を主流の車両プラットフォームにもたらし、レーダーベースの安全システム展開におけるシステムコスト、負荷、設計の複雑さを軽減する。

- 2025年12月:デンソー株式会社は、統合型モビリティコンピューター向け次世代車載システムオンチップに関する共同開発契約をMediaTek Inc.と締結しました。この契約は、デンソーの車載システム設計とMediaTekの半導体設計・検証能力を組み合わせたものです。

- 2025年8月:インフィニオン・テクノロジーズAGは、マーベル・テクノロジー社の車載イーサネット事業の一歩を完了し、ソフトウェア定義型車両ポートフォリオを強化するとともに、マイクロコントローラー、プロセッサ、センサー向けの高帯域幅車載ネットワークにおける機能を拡張しました。

よくある質問

Naveenは、カスタム、シンジケート、コンサルティングの各プロジェクトにおいて9年以上の実績を持つ、経験豊富な市場調査およびコンサルティングのプロフェッショナルです。現在はアソシエイトバイスプレジデントを務め、プロジェクトバリューチェーン全体にわたるステークホルダー管理を成功させ、100件以上の調査レポートと30件以上のコンサルティング案件を執筆しています。産業および政府機関のプロジェクトに幅広く携わり、クライアントの成功とデータに基づく意思決定に大きく貢献しています。

Naveenは、カルナータカ州VTUで電子通信工学の学位を取得し、マニパル大学でマーケティング&オペレーションズのMBAを取得しています。IEEEの会員として9年間活動し、会議や技術シンポジウムへの参加、セクションレベルおよび地域レベルでのボランティア活動に積極的に取り組んでいます。現職以前は、IndustryARCでアソシエイト戦略コンサルタント、Hewlett Packard(HP Global)で産業用サーバーコンサルタントを務めていました。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応