Automotive Electronics Market Trends, Share & Demand by 2034

Coverage: By Type (ECU/DCU, Sensors, Power Electronics, and Others), By Application (Body, Chassis, Powertrain, Infotainment, ADAS/AD, Others), By Vehicle Type (Passenger Cars, and Commercial Vehicles)

- Status : Data Released

- Report Code : TIPAT00002369

- Category : Electronics and Semiconductor

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 17, 2026

2025 Market Size

US$ 325.97 Bn

Base year value

2034 Forecast

US$ 664.14 Bn

Projected by 2034

CAGR 2026-2034

8.23 %

Growth rate

Addressable Market

US$ 4,448.11 Bn

(2026-2034)

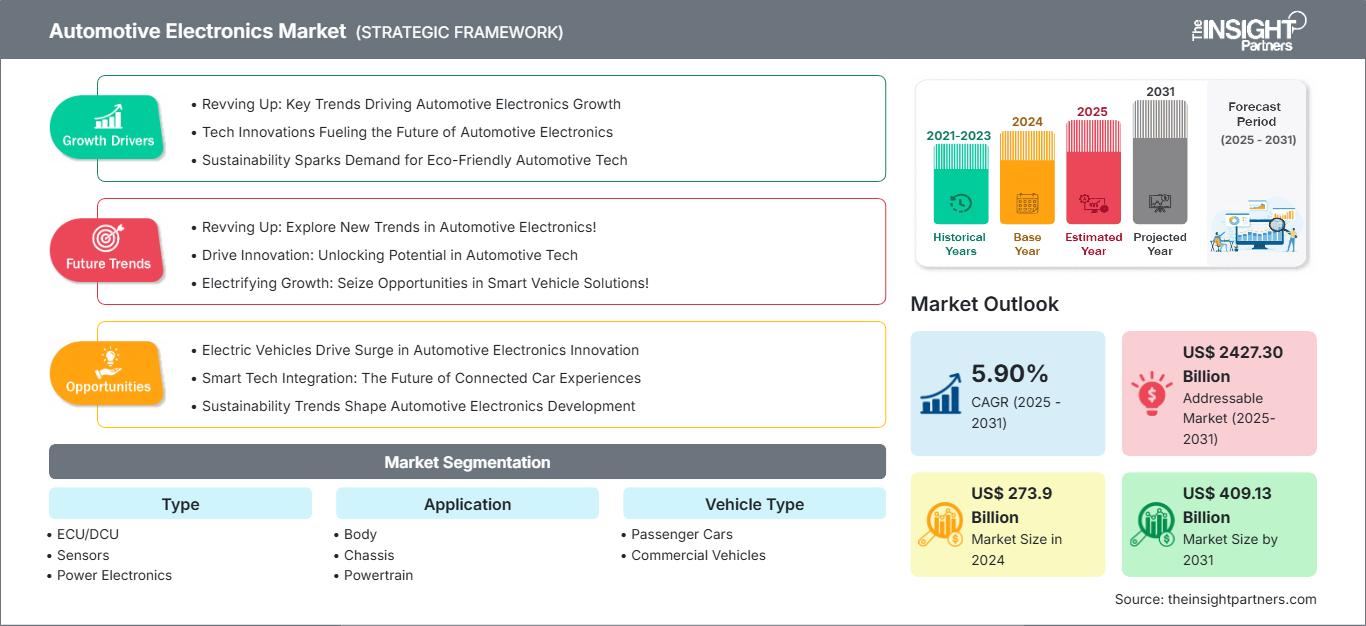

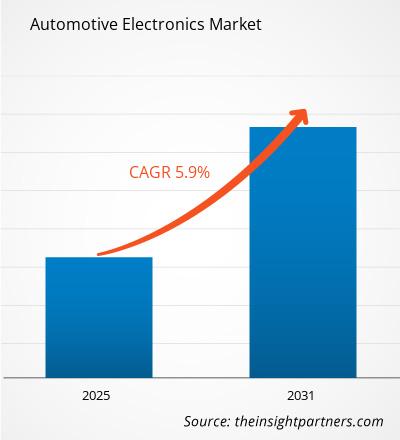

The Automotive Electronics Market size is expected to reach US$ 325.97 Billion in 2025 and is forecasted to reach US$ 664.14 Billion by 2034, expanding at a CAGR of 8.23% in the period 2026 to 2034. The key growth factors will be ECU, sensors, power electronics, infotainment, ADAS & AD systems, body electronics, chassis control, powertrain control, and increased usage of electronics in both passenger cars and commercial vehicles.

North America continues to remain an important demand center in the form of local software-driven platforms, electrified powertrains, and safety electronics. The market in North America is projected to register a CAGR in the range of 7.4% to 8.4% during the forecast period 2026 to 2034.

Automotive Electronics Market Assessment and Insights

- North America held 25%–29% Automotive Electronics Market share in 2025 and is expected to grow at a CAGR of 7.4%–8.4% between 2026–2034, driven by EV platforms, ADAS content, and local semiconductor policy.

- US represented 78%–83% of North America in 2025 and is projected to grow at a CAGR of 7.5%–8.5% between 2026–2034.

- Europe accounted for 23%–27% share in 2025 and is forecast to grow at a CAGR of 7.0%–8.0% between 2026–2034, led by Germany, France, the UK, Italy, and Spain.

- Asia Pacific held 38%–42% share in 2025 and is projected to grow at a CAGR of 8.8%–9.8% between 2026–2034, supported by China, Japan, South Korea, India, and Australia.

- Largest Segment ECU/DCU held a market share of 34%–38% in 2025, with CAGR range of 7.8%–8.8% between 2026–2034.

- High Growth Segment ADAS/AD held a market share of 15%–19% in 2025, with CAGR range of 10.2%–11.2% between 2026–2034.

- Key companies analyzed in detail: DENSO Corporation, HGM Automotive Electronics, Hitachi, Ltd., Infineon Technologies AG, Microchip Technology Inc., NXP Semiconductors N.V., Robert Bosch GmbH, Sony India Pvt. Ltd., Texas Instruments Incorporated, and ZF Friedrichshafen AG.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

Electronics in vehicles have evolved from stand-alone modules to domain, zonal, and centralized approaches where control, sensing, communications, and software execution are integrated. Manufacturing trends currently involve consolidation of ECUs, sensor fusion, automotive power components, and qualification of components in a long cycle. The market is influenced by EV platforms, safety norms, and software updates which necessitate a more coordinated approach between car makers, Tier 1 manufacturers, semiconductor companies, and software providers.

Growth opportunities in the coming years will be the fastest for applications where electrification, assisted driving, and connected vehicle networks are overlapping. The combination of the APAC manufacturing scale, European emission norms, and the North American localization incentive programs is leading to investments in power electronics, ADAS controllers, intelligent cockpits, and networking technologies. The market is supported by the rising electronic content per vehicle, while suppliers need to handle issues such as reliability, software testing, cybersecurity, and cost.

Automotive Electronics Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 325.97 Billion |

| Market Size by 2034 | US$ 664.14 Billion |

| Global CAGR (2026 - 2034) | 8.23% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Automotive Electronics Market Analysis

The drivers for demand include electrified propulsion system, digital cockpit, ADAS sensors, battery management, body control, and secure vehicle connectivity. The growth of the Automotive Electronics Market is directly connected with the change of distributed electronic control units to domain controllers. Every automotive program needs electronics that are capable of addressing issues related to functional safety, electromagnetic compatibility, thermal robustness, cybersecurity, and lifetime sustainment in various trims and geographies.

The ecosystem consists of semiconductor providers, sensor providers, ECU integration providers, power electronics providers, software tooling providers, Tier 1 module providers, and automakers. The supply dynamics are positively influenced by qualified components, scalable reference designs, and engineering support in the region. Due to the long life cycle of vehicle platforms, it is as critical as the performance and miniaturization.

Key competitors include automotive-oriented suppliers with wide product portfolios and OEM qualification experience. They include DENSO Corporation, Robert Bosch GmbH, ZF Friedrichshafen AG, Infineon Technologies AG, NXP Semiconductors N.V., Texas Instruments Incorporated, Microchip Technology Inc., Hitachi, Ltd., Sony India Pvt. Ltd., and HGM Automotive Electronics that compete using ECUs, sensors, power components, imaging solutions, control software, and integration.

Trends in investments include SiC power modules, radar and vision sensing, automotive Ethernet, cockpit intelligence, battery management, and flexible electronic control solutions. The evaluation of suppliers in market assessment considers supplier robustness, manufacturing geography, security competence, and software support. The strategic positioning involves a trade-off between high-performance compute to support ADAS/AD applications and cost-effective electronics for other automotive systems.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Automotive Electronics Market: Strategic Insights

Regional Insights

North America Automotive Electronics Market

The North America region accounted for 25%–29% market share in 2025 and will grow at 7.4%–8.4% from 2026 to 2034. This represents the North American market share of the Automotive Electronics Market, which shows the dominance of the United States in vehicle software, analog circuitry, connected solutions, and advanced safety systems. Drivers of demand include electric pickup trucks, telematics of commercial fleets, digital instrument clusters, battery management systems, and Level 2+ safety functionalities.

Local customers seek supply security, engineering expertise, and alignment with policies on cybersecurity in connected vehicles. Leading suppliers include NXP Semiconductors N.V., Texas Instruments Incorporated, Microchip Technology Inc., DENSO Corporation, and Robert Bosch GmbH. Applications include radar sensing and power conversion solutions. The requirement for longer-term allocation visibility from automakers is increasing due to rising electronics content in each vehicle.

U.S. Automotive Electronics Market Market

The U.S. accounted for 78%–83% of North America's demand in 2025 and is forecast to grow by 7.5%–8.5%. The application trends consist of ADAS processor chips, automotive Ethernet, battery management, infotainment controllers, and power management ICs. The semiconductor design capabilities and vehicle software development of the country make it an integral part of advanced electronic architectures.

The companies are widely diversified, including Texas Instruments Incorporated and Microchip Technology Inc., providing analog semiconductors, MCUs, and connectivity chips, whereas NXP Semiconductors N.V. provides support for radar and networking. DENSO Corporation, Robert Bosch GmbH, and ZF Friedrichshafen AG provide support for system integration. The car manufacturers are expanding their involvement in electronics to assure supply and functional safety.

Europe Automotive Electronics Market Market

The Europe segment had a market share of 23%-27% in 2025 and will grow by 7.0%-8.0%. The German segment dominates because of premium automobiles, EV power electronics, safety equipment, and automotive semiconductor design. France provides an electrification platform, while the UK focuses on advanced propulsion technology, connectivity, and automotive design capabilities.

The Italian and Spanish segments provide the market through vehicle manufacture, industrial electronics, and component supplies to OEMs in Europe. Infineon Technologies AG, Robert Bosch GmbH, ZF Friedrichshafen AG, NXP Semiconductors N.V., and DENSO Corporation cater to powertrain, chassis, body electronics, and safety needs. Environmental and safety regulations in the region will drive the market.

APAC Automotive Electronics Market Market

APAC is expected to maintain its position in 2025 with 38%-42% share, growing by 8.8%-9.8%. China excels in EV volumes, local electronics strategy, and quick adoption of intelligent cockpits. Japan and South Korea bring expertise in sensors, ECUs, displays, and power electronics, and India and Australia drive up vehicle electronics demand growth.

Industrial policy, battery manufacturing chains, and export-oriented production of passenger cars continue driving the market. DENSO Corporation, Hitachi, Ltd., Sony India Pvt. Ltd., Infineon Technologies AG, and NXP Semiconductors N.V. are the competitors alongside new regional players. Strongest demand is seen in powertrain, ADAS/AD, body electronics, and infotainment solutions for passenger cars.

Middle East & Africa Automotive Electronics Market Market

The Middle East & Africa segment will witness growth at a CAGR of 6.5% - 7.5%, driven by the UAE through connected mobility, premium car imports, and smart infrastructure. Saudi Arabia is making investments in its own automotive production capability and electric vehicle dreams, whereas South Africa continues to be the main source of automotive production.

For the rest of the MEA, the market is linked with the use of commercial fleets, telematics, body electronics, and vehicle upgrading. The energy countries are looking into EV charging, fleet electrification, and intelligent transportation system, thus boosting the usage of electronics content.

Segmentation Analysis

Type

Type is projected to grow at 7.9%–8.9% during 2026–2034. Automotive Electronics Market scope spans ECU/DCU, sensors, and power electronics, with demand shaped by vehicle architecture consolidation, electrification, real-time sensing, and software-controlled functions. Growth is strongest where control, sensing, and power conversion are integrated into scalable platforms.

- ECU/DCU represents the largest position because centralized control, domain computing, body management, chassis supervision, and powertrain coordination depend on reliable automotive-grade processing and software integration.

- Sensors support ADAS, body comfort, chassis control, battery monitoring, and cabin intelligence, creating resilient demand as vehicles require richer real-time data for automated decisions.

- Power Electronics gains strategic importance through inverters, onboard chargers, DC-DC converters, battery systems, and thermal management in hybrid and electric vehicle architectures.

Application

Application is forecast to grow at 8.4%–9.4% during 2026–2034. Demand is distributed across body, chassis, powertrain, infotainment, and ADAS/AD systems. ADAS/AD shows the fastest momentum as radar, camera, domain controllers, and braking supervision expand from premium vehicles into broader passenger and commercial platforms.

- Body electronics provide steady demand through lighting, windows, climate control, seat modules, access systems, and comfort features requiring cost-efficient controllers and sensors.

- Chassis applications use electronics for stability control, steering, suspension, braking interfaces, and sensor fusion, supporting safer handling and higher vehicle dynamics performance.

- Powertrain demand rises through engine control, inverter management, battery monitoring, onboard charging, and thermal systems across internal combustion, hybrid, and electric vehicles.

- Infotainment systems support connectivity, navigation, displays, audio, vehicle data services, and over-the-air updates, making cockpit electronics a major value center.

- ADAS/AD is strategically important as cameras, radar, domain controllers, driver monitoring, and braking supervision become core safety and differentiation features.

Vehicle Type

Vehicle Type is expected to grow at 7.7%–8.7% during 2026–2034. Passenger cars dominate electronics consumption due to infotainment, ADAS, electrification, and comfort systems. Commercial vehicles add momentum through fleet telematics, safety mandates, energy management, predictive maintenance, and increasingly connected logistics operations.

- Passenger Cars drive the largest demand base because mass-market and premium models increasingly include ADAS, digital cockpit, battery management, body control, and connectivity electronics.

- Commercial Vehicles show rising strategic relevance as fleet operators adopt telematics, driver assistance, electrified drivetrains, predictive maintenance, and safety electronics for operating efficiency.

Opportunity Snapshot

| Application | Revenue Contribution | Trend Tag | Adoption Stage |

| Body | Medium | Smart Comfort | Mature |

| Chassis | Medium | Brake Control | Scaling |

| Powertrain | High | EV Inverter | Scaling |

| Infotainment | High | Connected Cockpit | Scaling |

| ADAS/AD | High | Sensor Fusion | Scaling |

Automotive Electronics Market Growth Drivers and Impact Analysis

Electrification Raises Electronics Value Per Vehicle

Electric and hybrid vehicles require substantially more electronic control than conventional models because traction inverters, battery management systems, onboard chargers, thermal controls, and DC-DC converters all depend on automotive-grade components. The impact is visible across powertrain, chassis, and safety electronics, where suppliers must support high-voltage operation, functional safety, and long qualification cycles. Infineon Technologies AG, DENSO Corporation, Hitachi, Ltd., and Texas Instruments Incorporated benefit from power and analog demand, while automakers seek resilient supply for multi-year EV platforms. This driver expands both unit demand and average electronics value per vehicle.

ADAS Penetration Expands Sensor and Compute Requirements

Safety regulation, consumer ratings, and OEM differentiation are moving driver assistance functions into more vehicle categories. Cameras, radar, ultrasonic sensors, braking controllers, and domain processors require sensors, ECUs, memory, and analog interfaces that can process data reliably in real time. NXP Semiconductors N.V., Sony India Pvt. Ltd., Microchip Technology Inc., and ZF Friedrichshafen AG are positioned around sensing, control, and safety requirements. The market impact includes higher design complexity, longer software validation, and stronger demand for electronics meeting functional safety and cybersecurity requirements.

Software-Defined Vehicles Reshape Network Architecture

Automakers are replacing fragmented electronic control units with domain and zonal architectures that rely on high-bandwidth communication, centralized compute, and secure gateway functions. This shift increases demand for automotive Ethernet, domain controllers, power management, embedded security, and software-compatible electronics. Infineon Technologies AG’s acquisition of Marvell’s automotive Ethernet business shows how suppliers are repositioning for software-defined vehicle networks. The commercial impact extends beyond hardware, as vendors must support software stacks, reference designs, update pathways, and long-term platform compatibility.

Automotive Electronics Market Future Trends

Centralized Compute Platforms Move into Mainstream Vehicles

Automotive Electronics Market trends will increasingly center on centralized compute platforms that consolidate infotainment, ADAS/AD, body control, and connectivity workloads. Mainstream vehicles will adopt scalable processors and mixed-criticality software environments once cost, safety, and thermal constraints are resolved. This trend favors suppliers that combine electronics, development tools, security capability, and ecosystem partnerships. It also shifts purchasing from component-by-component sourcing toward platform roadmaps that support multiple models, software updates, and regional feature variations.

Sensor Fusion Becomes a Core Safety Differentiator

Future vehicle safety systems will rely on deeper fusion of radar, camera, ultrasonic, and in-cabin sensing data. The shift will increase demand for synchronized sensors, edge processing, high-speed networking, and software validation environments. NXP Semiconductors N.V. and Sony India Pvt. Ltd. are relevant to radar and imaging layers, while ZF Friedrichshafen AG and Robert Bosch GmbH connect sensing to braking and chassis functions. Adoption will advance gradually as OEMs balance performance, cost, regulatory requirements, and consumer acceptance.

Automotive Electronics Market Opportunities

Long-Term Supply Agreements for EV and ADAS Platforms

Automakers are willing to enter longer electronics supply arrangements where platform risk is high, especially for EV power electronics, ADAS/AD controllers, and safety-critical ECUs. Automotive Electronics Market Forecasts support investment in dedicated capacity planning, automotive packaging, software validation, and co-development agreements that improve allocation visibility. Suppliers can differentiate by offering design support, second-source strategies, lifecycle commitments, and transparent qualification roadmaps. The opportunity is most attractive where one validated electronics platform can serve multiple vehicle models across regions and model years.

Cybersecure Connectivity and Telematics Electronics

Connected vehicles require electronics that support secure gateways, telematics control units, encrypted communication, and remote diagnostics without compromising functional safety. Regulatory scrutiny of connected vehicle data flows increases the value of secure hardware roots of trust, automotive Ethernet, and update-capable architectures. NXP Semiconductors N.V., Microchip Technology Inc., Texas Instruments Incorporated, and Robert Bosch GmbH can address secure communication, power, and interface needs. Suppliers that combine electronics, security documentation, and software enablement can capture value as connectivity becomes standard in passenger and commercial vehicles.

Recent Developments

- June 2026: NXP Semiconductors N.V. announced the SAF8444 automotive radar system-on-chip, bringing on-sensor L2/L2+ ADAS processing to mainstream vehicle platforms and reducing system cost, thermal load, and design complexity for radar-based safety deployments.

- December 2025: DENSO Corporation signed a joint development agreement with MediaTek Inc. for next-generation automotive system-on-chips intended for integrated mobility computers, combining DENSO’s automotive system design with MediaTek’s semiconductor design and verification capability.

- August 2025: Infineon Technologies AG completed the acquisition of Marvell Technology, Inc.’s automotive Ethernet business, strengthening its software-defined vehicle portfolio and expanding capabilities in high-bandwidth in-vehicle networking for microcontrollers, processors, and sensors.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends