ヨーロッパのデータセンター建設市場 - 2030年の成長予測、統計および事実

ヨーロッパのデータセンター建設市場規模と予測 (2020 ~ 2030 年)、地域シェア、傾向、成長機会分析レポートの対象範囲: 建設の種類別 (電気建設、一般建設、機械建設)。階層標準 (階層 3、階層 4、階層 1 および階層 2)。業種 (IT および電気通信、BFSI、メディアおよびエンターテイメント、小売、製造、政府、運輸、その他)

- ステータス : 出版

- レポートコード : TIPTE100000384

- カテゴリー : テクノロジー、メディア、通信

- ページ数 : 132

- 利用可能なレポート形式 :

- 最終更新日 : November 17, 2025

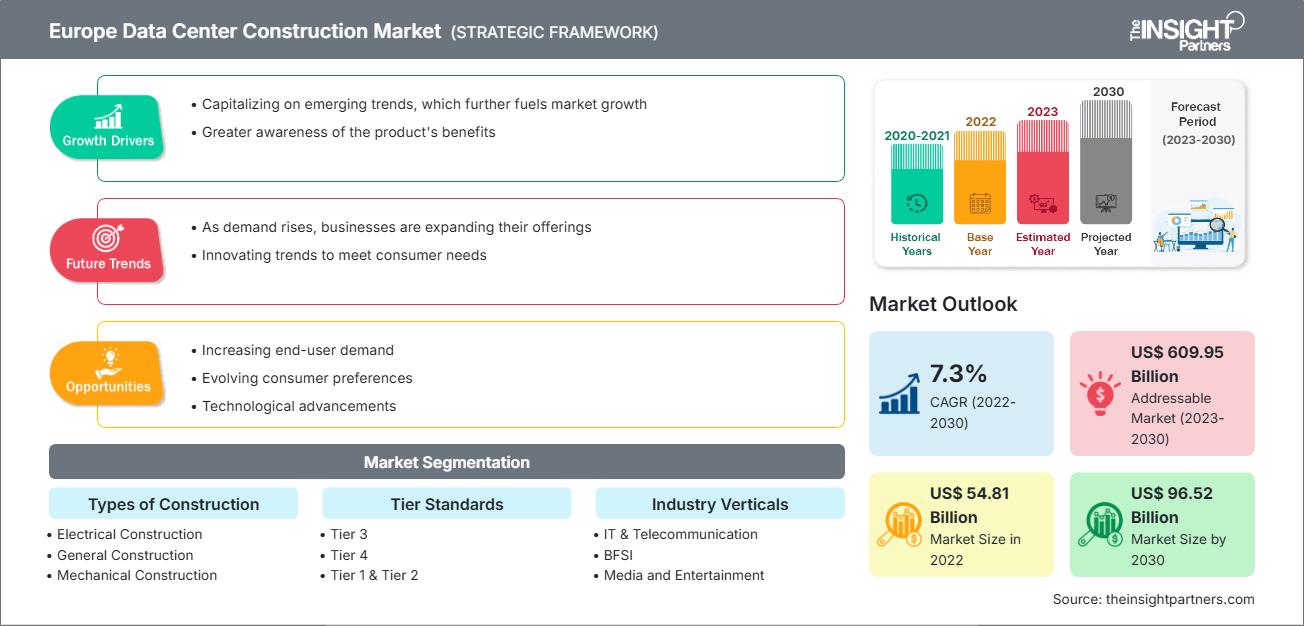

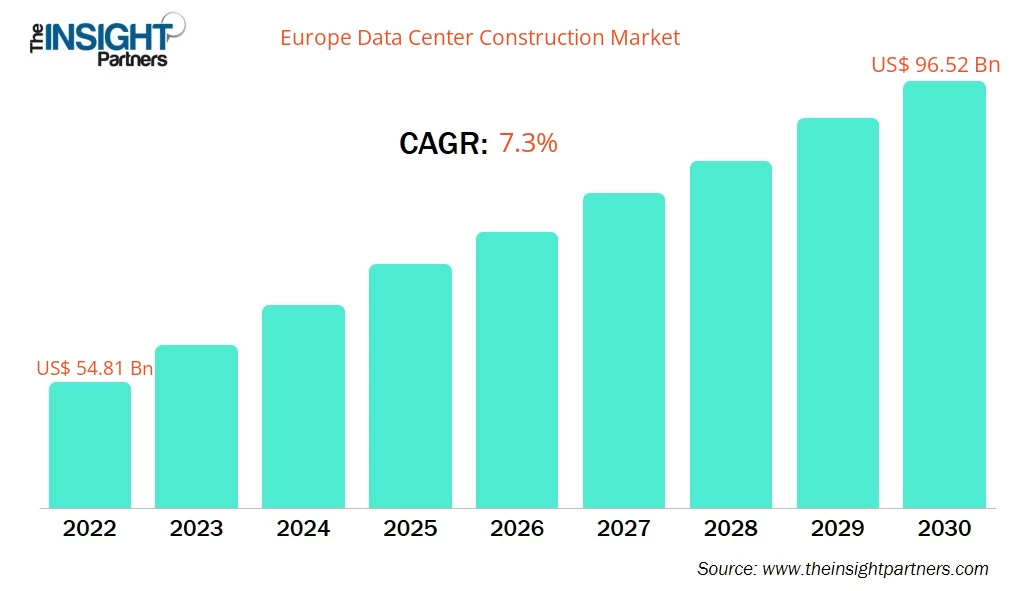

ヨーロッパのデータセンター建設市場規模は、2022年に548.1億米ドルと評価され、2030年までに965.2億米ドルに達すると予想されており、2022年から2030年にかけて7.3%のCAGRを記録すると予測されています。

アナリストの視点:

データセンター建設とは、データの保存、処理、管理のための様々なIT運用と機器を収容・運用する施設を物理的に構築することです。欧州データセンター建設市場レポートは、市場を牽引する主要な要因と主要プレーヤーの開発状況に重点を置いています。

データセンター建設市場の概要:

データセンター建設とは、特定の要件と基準に準拠したデータセンター施設の設計と建設を指します。データセンター建設では、現在および将来のサーバーや機器を収容するのに十分なスペースを備えたフロアプランの作成が最優先されます。これにより、施設は増大するデータストレージと処理の需要に効果的に対応できます。データセンターは、地震、洪水、暴風雨などの自然災害に耐えられるように設計する必要があります。建設作業には、防火システムの導入や消火のための十分な水供給の確保など、予防策の実施と影響の軽減が含まれます。データセンター建設には、配線、冷却システム、電源、セキュリティ対策などのインフラコンポーネントの綿密な計画と設計が必要です。効率的で安全な運用を確保するために、建築基準法と業界基準が考慮されます。建設プロセスは通常、評価、計画、設計、実際の建設という複数の段階で構成されます。各段階では、ビジネスニーズ、施設要件、規制遵守を慎重に検討する必要があります。データセンターは、規模、容量、目的が多岐にわたります。それぞれに固有の特性と機能を持つ、さまざまなタイプと階層があります。データセンターの設計と建設は、その用途と、求められる冗長性と信頼性のレベルによって異なります。データセンターの建設は、建築、電気工学、機械工学、ITインフラといった分野の専門知識を必要とする複雑かつ重要なプロセスです。その目的は、データの保管と処理業務のための安全で信頼性が高く、効率的な環境を構築することです。ヨーロッパのデータセンター建設市場の予測は、過去の傾向、調査、企業の動向、ホワイトペーパーなど、様々なデータソースと分析手法に基づいています。

グリーン データ センターの使用が増えることで、今後数年間でデータ センター建設市場に新たなトレンドが生まれることが期待されます。

欧州データセンター建設市場は、建設形態、階層設計、および業種に基づいてセグメント化されています。建設形態に基づいて、欧州データセンター建設市場は、一般建設、電気設計、機械設計に分類されます。階層設計に基づいて、欧州データセンター建設市場は、Tier 1、Tier 2、Tier 3、Tier 4に分類されます。業種に基づいて、欧州データセンター建設市場は、IT・通信、BFSI、政府機関、製造業、小売業、運輸業、メディア・エンターテインメント、その他に分類されます。

Rittal GmbH & Co KG、Schneider Electric SE、DPR Construction Inc、INFINITI IT Ltd、blu-3 (UK) Ltd、Datalec Precision Installations Ltd、Coromatic AB Sweden、Winthrop Technologies Ltd、Mercury Engineering Ltd、STO Building Group Inc.は、本データセンター建設市場調査で紹介された主要企業の一部です。さらに、エコシステムの全体像を把握するため、本調査ではその他の主要企業についても調査・分析を行いました。

このレポートの一部、国レベルの分析、Excelデータパックなど、あらゆるレポートを無料でカスタマイズできます。また、スタートアップや大学向けのお得なオファーや割引もご利用いただけます。

欧州データセンター建設市場:戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

データセンター建設市場の推進要因:

IoTサービスの急速な拡大が欧州データセンター建設市場の成長を牽引

IoT(モノのインターネット)サービスの急速な拡大は、データセンター建設市場の主要な牽引役です。近年、電球、携帯電話、ウェブカメラなどのIoTデバイスの急増により、IoTはデータセンターを変革してきました。IoTデバイスの数は、2025年までに416億~754億4000万台に増加すると予想されています。IoTデバイスの数が増えれば増えるほど、データを適切に保管、処理、分析するためにデータセンターへの依存度が高まります。さらに、IoTを通じてインターネットに接続するデバイスが増えるにつれて、膨大な量のデータが生成されます。これには、スマートホーム、ウェアラブル、産業機器、コネクテッドカーなどのセンサーが含まれます。これらのデバイスによって生成されるデータの種類は、位置データ、環境データ、使用状況データ、さらにはリアルタイムのビデオストリームなど、ますます多様化かつ複雑になっています。

さらに、IoTの導入により、データセンターを取り巻く環境は進化しています。分析とプロセスは、企業のデジタルトランスフォーメーションにおいて不可欠な要素です。分析とプロセスは、データセンターが運用面で活動を拡大するための手段となります。データセンター特有のデジタル化プロセスには、運用におけるIoTの導入、キャパシティビルディング、事業開発、インフラ整備、システム活用などが含まれます。全体として、IoTサービスの拡大は、データセンター建設市場を大きく牽引しています。より多くのデバイスが接続され、より多くのデータが生成されるにつれて、効率的で拡張性の高いデータセンター・インフラストラクチャの必要性はますます高まっていくでしょう。

データセンター建設市場のセグメント分析:

欧州データセンター建設市場分析は、建設の種類、ティア基準、業界区分という3つのセグメントを考慮して実施されました。建設の種類に基づいて、データセンター建設市場は電気工事、一般工事、機械工事に分類されます。電気工事セグメントは、欧州データセンター建設市場の46.71%を占めています。データセンターには、ユーティリティフィード、スイッチギア、発電機、UPS、PDUなど、ユーティリティフィードからサーバーラックへの電力伝送を支援する複数の電気機器が含まれます。データセンターインフラに到達する電気供給は、変圧器を使用して使用可能な電圧レベルに変換する必要があります。さらに、ユーティリティグリッドはデータセンターへの主要な電力供給源です。同時に、スイッチギアは変圧器またはユーティリティからデータセンターフロアへの電力を安全に供給するのに役立ちます。さらに、発電機と無停電電源装置は、それぞれ長期および一時的なバックアップ電源を提供します。配電ユニットは、ラックやスタンドアロンシステムへの電力伝送を支援します。

データセンター建設市場の地域分析:

欧州のデータセンター建設市場は、ドイツ、フランス、スウェーデン、英国、その他欧州諸国に分類されます。欧州のデータセンター建設市場は、欧州経済の好調、クラウドコンピューティング需要の高まり、デジタル技術への依存度の高まりなどの要因により、成長を遂げています。この市場には、電気インフラ、機械インフラ、一般インフラ、ソリューション、サービス、専門サービスなど、様々な種類のインフラとサービスが含まれます。複数の企業が欧州のデータセンター建設市場に積極的に参入しています。例えば、2023年10月、フランスに拠点を置くデータセンター運営会社Data4は、スペインのサン・アグスティン・デ・グアダリクスに新キャンパスを開発するため、ヒル・インターナショナルのサービスを導入しました。MAD2と呼ばれるこのプロジェクトは、6.5ヘクタールの敷地に4つのデータセンターを建設し、合計80MWの容量を誇ります。Data4は、これらの新施設が顧客の成長に対応するために、効率的で柔軟なモデルを活用することを強調しています。さらに、国際的に認知されたコロケーションサービスプロバイダーであるTELEHOUSEは、2023年10月、フランスのパリ・マニにあるTH3に2番目のデータセンターを建設すると発表しました。このデータセンターは、12,000平方メートルの広大なITフロアスペースと18MWの電力容量を提供します。同社によるこのようなインフラ拡張の決定は、既存の欧州施設のホスティングおよび接続設備を増強することで、欧州および各国のデジタル独立性を高め、ひいては世界のインターネットトラフィックをこの地域に呼び込むという戦略目標と一致しています。こうした展開は、欧州全体のデータセンター建設市場の成長を後押しすると期待されています。データ処理需要の増加や技術革新の進展といった要因が、ドイツのデータセンター建設市場シェアの拡大を促進しています。ドイツのデータセンター建設市場規模は、2030年までに177億7,000万米ドルに達すると予想されています。市場の主要プレーヤーは、増大する需要に対応するために、買収やデータセンター容量の拡大に投資しています。例えば、2023年1月、CyrusOneはドイツのフランクフルトにあるオフィスビルを買収し、データセンターキャンパスに転換する計画を発表しました。このオフィスビルは、投資グループのCorumによって9,500万ユーロ(1億230万米ドル)で売却されました。さらに、ドイツにおける法規制の導入は、データセンター運営の規制と最適化に対する同国の取り組みを浮き彫りにしています。ドイツは、ヨーロッパで初めてデータセンターに関する本格的な法規制を導入した国です。この規制は、エネルギー効率、環境への影響、セキュリティなど、データセンター運営のさまざまな側面に対処することを目的としています。さらに、データセンター業界の有力企業であるNorthCは、は、ドイツのフランクフルトに最先端のデータセンター施設を開発する計画を発表しました。これは同社にとってドイツ市場への初進出となります。5MWの容量を予定するフランクフルトの新施設は、ドイツにおけるデータセンターサービスの需要増加に対応します。

データセンター建設市場の主要プレーヤー分析:

データセンター建設市場レポートで紹介されている著名な企業には、Rittal GmbH & Co KG、Schneider Electric SE、DPR Construction Inc、INFINITI IT Ltd、blu-3 (UK) Ltd、Datalec Precision Installations Ltd、Coromatic AB Sweden、Winthrop Technologies Ltd、Mercury Engineering Ltd、および STO Building Group Inc などがあります。

最近の動向:

データセンター建設市場では、合併や買収といった無機的戦略と有機的戦略が企業に広く採用されています。データセンター建設市場における最近の主要な動向をいくつかご紹介します。

- 2023年2月、マーキュリーは英国ロンドン近郊に建設中のグローバル・テクニカル・リアルティ(GTR)のGB Oneデータセンター・キャンパスにおいて、元請け業者として事業を展開することを発表しました。グレーター・ロンドンのデータセンター集積地の一つ、スラウ・トレーディング・エステートに位置するこの40.5MWの施設は、完成すればこの地域で最大規模の施設となります。持続可能性を念頭に設計されたこの施設は、マーキュリーのチームがGB OneのLEED(Leadership in Energy and Environmental Design)認証取得に向けて取り組んでいます。

- 2023年2月、安全な電力供給とデータ通信のためのミッションクリティカルなインフラストラクチャの大手サプライヤーであるコロマティックは、ストックホルム南部のコナプトの新しいデータセンターのミッションクリティカルな機器の設計、構築、納入を委託されました。

レポートの範囲

欧州データセンター建設市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2022年の市場規模 | 548億1000万米ドル |

| 2030年までの市場規模 | 965.2億米ドル |

| CAGR(2022年~2030年) | 7.3% |

| 履歴データ | 2020-2021 |

| 予測期間 | 2023~2030年 |

| 対象セグメント |

建設の種類別

|

| 対象地域と国 |

ヨーロッパ

|

| 市場リーダーと主要企業の概要 |

|

欧州データセンター建設市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

欧州データセンター建設市場は、消費者嗜好の変化、技術の進歩、製品メリットへの認知度向上といった要因によるエンドユーザー需要の高まりに牽引され、急速に成長しています。需要の高まりに伴い、企業は提供内容の拡充、消費者ニーズへの対応のための革新、そして新たなトレンドの活用を進めており、これが市場の成長をさらに加速させています。

- ヨーロッパのデータセンター建設市場の主要な主要プレーヤーの概要を入手

アンキタは、テクノロジー、メディア、ICT、エレクトロニクス・半導体の各分野で8年以上の経験を持つ、ダイナミックな市場調査およびコンサルティングのプロフェッショナルです。Microsoft、Oracle、NEC、SAP、KPMG、Expeditors Internationalといったグローバルクライアントに対し、100件以上のコンサルティングおよび調査案件を主導・遂行してきました。彼女のコアコンピテンシーは、市場評価、データ分析、予測、戦略策定、競合情報、レポート作成です。

アンキタは、販売前の提案書作成やクライアントとの協議から、販売後の実用的なインサイトの提供まで、プロジェクトサイクル全体を巧みに管理することに長けています。彼女は、部門横断的なチームの管理、複雑な調査モジュールの構築、そしてクライアント固有のビジネス目標に合わせたソリューションの調整に長けています。優れたコミュニケーション能力、リーダーシップ、そしてプレゼンテーション能力により、急速に変化する市場環境において、常に価値主導の成果を生み出しています。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応