データセンター冷却市場 - 2031年までの世界の市場規模、動向、収益分析

データセンター冷却市場の規模と予測(2021年 - 2031年)、世界および地域別のシェア、トレンド、成長機会分析レポートの対象範囲:タイプ別(空冷および液冷)、コンポーネント別(空調システム、チラー、空調ユニット、冷却塔、熱交換器、加湿器、その他)、冷却タイプ別(部屋ベース冷却、列ベース冷却、ラックベース冷却)、データセンタータイプ別(ハイパースケールデータセンター、コロケーションデータセンター、ホールセールデータセンター、エンタープライズデータセンター)、業界別(ITおよび通信、BFSI、ヘルスケア、製造、政府および防衛、メディアおよびエンターテイメント、小売、エネルギー、その他)、および地域別(北米、ヨーロッパ、アジア太平洋、中東およびアフリカ、南米および中米)

- ステータス : 出版

- レポートコード : TIPTE100000136

- カテゴリー : テクノロジー、メディア、通信

- ページ数 : 251

- 利用可能なレポート形式 :

- 最終更新日 : January 30, 2026

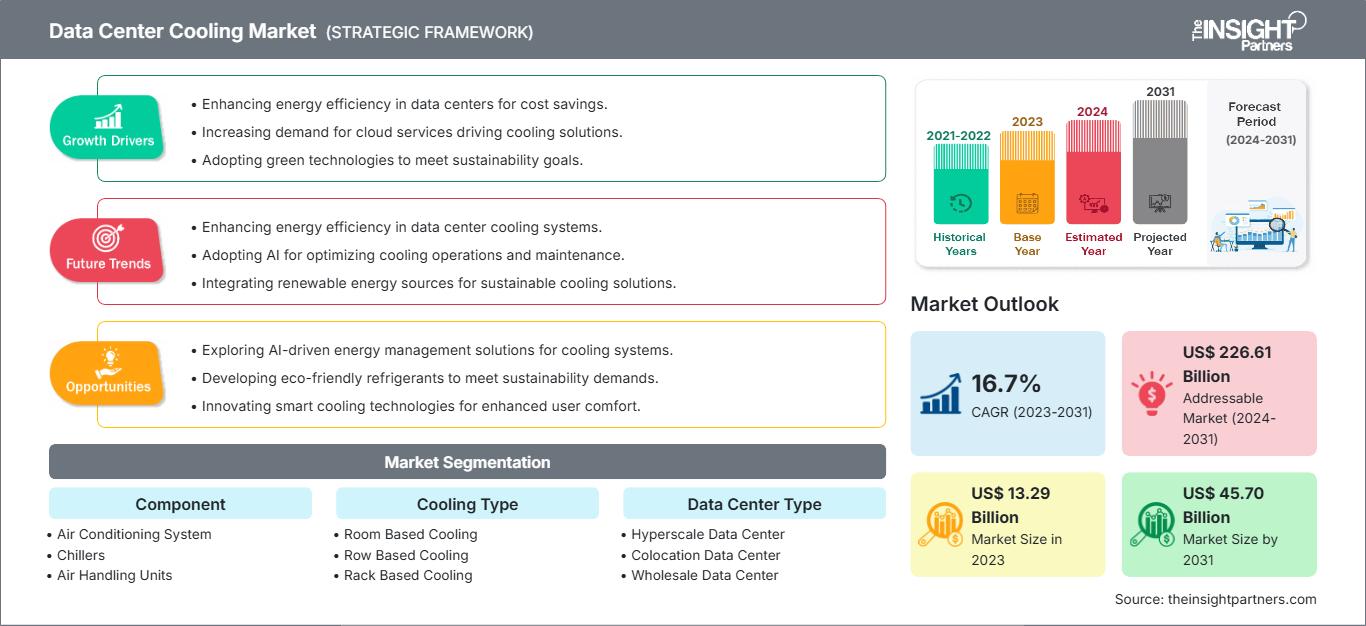

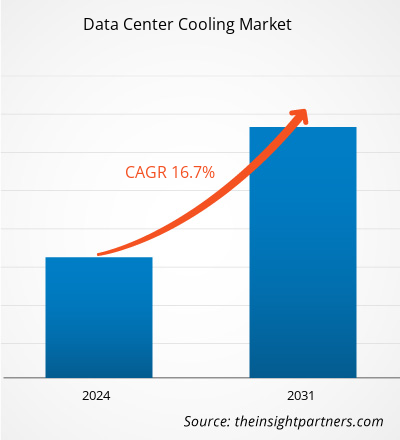

データセンター冷却市場規模は、2024年の154億3,102万米ドルから、2031年には457億531万米ドルに達すると予測されています。市場は2025年から2031年の間に16.9%のCAGRを記録すると予想されています。

データセンター冷却市場分析

データセンター冷却ソリューションは、データセンター内の標準温度を維持するために不可欠です。市場は、膨大なデータ生成量、クラウド導入の増加、そして高密度ワークロードの普及によって活性化しています。事業者は、厳格なエネルギー効率と持続可能性の基準を満たしながら、熱密度の増大という課題に直面しています。そのため、市場は従来の空冷だけでなく、高度な空気制御、液冷、フリークーリング技術など、幅広いソリューションに注目しています。インテリジェントな監視とAI駆動型制御システムにより、大規模なハイパースケールキャンパスから小規模なエッジ施設まで、あらゆる施設の冷却リソースの予測保守とリアルタイム最適化が可能になります。

データセンター冷却市場の概要

デジタルインフラストラクチャを構成するITハードウェアは、信頼性、パフォーマンス、そして長寿命を維持するために、常に冷却する必要があります。従来のコンピュータルームエアコン(CRAC)や冷水システムに加え、高度なチップ直接冷却技術や液浸冷却技術など、幅広いソリューションが利用可能です。

データセンター冷却市場のトレンドは、より高い精度、効率、そして柔軟性へと移行しています。現代の冷却方法は、最大の冷却効果を発揮するホットアイルとコールドアイルのコンテインメントといったコンテインメント構造に重点を置いています。外気や水を利用して冷却するエコノマイザーの使用が急速に普及し、機械圧縮にかかるエネルギー消費を削減しています。

データセンターの電力密度が高まるにつれ、空冷と液冷を慎重に組み合わせるハイブリッド冷却モデルの人気が高まっています。この包括的な手法により、事業者は特定の熱負荷と用途に最適な冷却技術を判断できます。これにより、企業の環境・社会・ガバナンス(ESG)への取り組みを支援しながら、設備投資(CapEx)と運用コスト(OpEx)の両方を最適化することができます。

要件に合わせてレポートをカスタマイズ

無料カスタマイズデータセンター冷却市場:戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

データセンター冷却市場の推進要因と機会

市場の推進要因:

- データ密度とコンピューティング密度の急激な増加:クラウドサービス、AI/MLワークロード、そして5Gを活用したアプリケーションの急速な拡大により、サーバーラック内の熱密度が増加しています。このような熱密度の上昇には、効率的な冷却装置が必要です。

- 厳格なエネルギー効率と持続可能性に関する規制:世界的なエネルギー価格の上昇が続いています。CO2削減目標や電力使用効率(PUE)などの効率基準により、事業者は運用コストの削減にもつながる高度な冷却技術への投資を迫られています。

- ハイパースケールおよびエッジ インフラストラクチャの拡張: 大規模なハイパースケール データ センター プロジェクトにより、集中型の大容量冷却プラントの需要が高まる一方、エッジ コンピューティングの分散性により、分散型の耐久性の高い冷却ユニットの必要性が生まれます。

市場機会:

- 高度な液体冷却と浸漬冷却の採用: 冷却を必要とする高密度 AI サーバーと GPU の需要の増加は、直接冷却、チップ冷却、完全浸漬冷却などの液体冷却技術の開発と使用の大きな機会であり、優れた熱転送効率を提供するだけでなく、熱の再利用の可能性も秘めています。

- スマート冷却管理のためのAIとIoTの統合:冷却インフラをデータセンター・インフラ管理(DCIM)プラットフォーム、IoTセンサー、AIアルゴリズムなどと統合することで、データセンター事業者は予測分析、動的負荷分散、自律最適化といった機能を活用できるようになります。これにより、ソリューションプロバイダーやサービスプロバイダーは新たな収益源を創出できます。

- 旧式設備の改修と近代化: 長期間稼働しているデータセンターの大規模なインストールベースが世界中に存在し、そのため、旧式の冷却システムを最新の効率的なソリューションにアップグレードする大きな可能性があり、これが改修プロジェクトやサービス契約の強力なアフターマーケットを促進することになります。

データセンター冷却市場レポートのセグメンテーション分析

データセンター冷却市場は、その運用、成長の可能性、そして現在のトレンドをより明確に理解するために、明確なカテゴリーに分類されています。以下は、ほとんどの業界レポートで使用されている標準的なセグメンテーション手法です。

冷却タイプ別:

- ルームベース冷却:CRACやCRAHユニットなどの従来のペリメーターシステムは、データホール全体を冷却します。ルームベース冷却は、主に中程度で均一な熱負荷のある大企業や小規模施設で使用され、そのシンプルさと信頼性が高く評価されています。

- 列ベース冷却:列内冷却ユニットは、サーバーラック間に配置され、集中的に効率的に熱を除去します。中密度から高密度の環境では、精度向上と空気の混合抑制が求められるため、人気が高まっています。

- ラックベースの冷却:各ラックに直接冷却機構が組み込まれているため、超高密度アプリケーションにおいて最高レベルの精度を実現します。ラックベースの冷却は、混在環境における特定のHPCまたはAIクラスターに不可欠です。

データセンターの種類別:

- ハイパースケールデータセンター

- コロケーションデータセンター

- ホールセールデータセンター

- エンタープライズデータセンター

業界別:

- ITおよび通信

- BFSI

- 健康管理

- 製造業

- 政府と防衛

- メディアとエンターテイメント

- 小売り

- エネルギー

- その他

地理別:

- 北米

- ヨーロッパ

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

アジア太平洋地域のデータセンター冷却市場は、最も急速な成長が見込まれています。

データセンター冷却市場の地域別分析

The Insight Partnersのアナリストは、予測期間全体を通してデータセンター冷却市場に影響を与える地域的な傾向と要因を詳細に解説しています。このセクションでは、北米、ヨーロッパ、アジア太平洋、中東・アフリカ、中南米におけるデータセンター冷却市場のセグメントと地域についても解説します。

データセンター冷却市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2024年の市場規模 | 154億3,102万米ドル |

| 2031年までの市場規模 | 457億531万米ドル |

| 世界のCAGR(2025年~2031年) | 16.9% |

| 履歴データ | 2021-2023 |

| 予測期間 | 2025~2031年 |

| 対象セグメント |

タイプ別

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業の概要 |

|

データセンター冷却市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

データセンター冷却市場は、消費者の嗜好の変化、技術の進歩、製品メリットへの認知度の高まりといった要因によるエンドユーザー需要の増加に牽引され、急速に成長しています。需要の増加に伴い、企業は製品ラインナップの拡充、消費者ニーズへの対応のための革新、そして新たなトレンドの活用を進めており、これが市場の成長をさらに加速させています。

- データセンター冷却市場のトップキープレーヤーの概要を入手

データセンター冷却市場シェア分析(地域別)

アジア太平洋地域は最も急速な成長を遂げています。ラテンアメリカ、中東、アフリカの新興市場は、データセンター冷却プロバイダーにとって多くの未開拓の機会を提供しています。

データセンター冷却市場は、地域によって成長率が異なります。以下は、地域別の市場シェアとトレンドの概要です。

1. 北米

- 北米は成熟した主要市場であり、その成長は主にハイパースケールビジネスの拡大、AIインフラ投資、そしてエンタープライズITの近代化によって牽引されています。この地域におけるエネルギー効率と持続可能性への取り組みは、液冷やフリークーリングといった最先端の冷却方式の継続的な導入を牽引する重要な要因となっています。

2. ヨーロッパ

- 欧州市場は、厳格な環境規制、高いエネルギーコスト、そして野心的な持続可能性目標を特徴としています。そのため、北欧などの適した気候におけるフリークーリングや、高密度アプリケーション向けの高度な液冷システムの導入など、効率的な冷却装置に対する需要が高まっています。

3. アジア太平洋

- アジア太平洋地域は最も急速に成長している市場であり、その拡大は急速なデジタルトランスフォーメーション、大規模なハイパースケールデータセンターの建設、そして中国、インド、東南アジアにおける政府の取り組みによるものです。この地域では、大規模導入向けの費用対効果の高い空冷から、AIハブ向けの高度な液冷まで、幅広い冷却ソリューションが提供されています。

4. 南米と中央アメリカ

- 中南米市場は、クラウド導入の増加、地域データ主権のトレンド、そしてデジタルインフラへの投資により、勢いを増しています。ブラジルやチリといった国々は、性能、コスト、そして地域の気候条件への耐性の最適なバランスを実現する冷却ソリューションを提供できる大きな可能性を秘めています。

5. 中東およびアフリカ

- 中東およびアフリカの市場成長は、特にUAEやサウジアラビアなどの湾岸協力会議(GCC)諸国におけるデジタルインフラへの投資によって牽引されています。この地域では極端な気温上昇により効率的な機械冷却が不可欠となり、過酷な環境向けに設計された高性能でエネルギー効率が最適化された空調システムの需要が高まっています。

データセンター冷却市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

高い市場密度と競争

市場は非常に競争が激しく、Asetek, Inc.、Rittal GmbH & Co KG、Stulz SpA、Carrier Global Corpなどが市場を席巻する主要プレーヤーです。さらに、地域メーカーやニッチメーカーも、特定の業界や用途に特化したソリューションを提供しています。

この高いレベルの競争により、企業は次のようなものを提供して他社に差をつけようとします。

- 効率、インテリジェンス (AI/ML 統合)、新しい冷却技術の継続的なイノベーション。

- 設計、展開、継続的な管理および最適化サービスをカバーする包括的なエンドツーエンドのソリューション。

- 地球温暖化係数 (GWP) が低い冷媒、高い自由冷却能力、および熱再利用の可能性があるソリューションを開発します。

機会と戦略的動き

- 戦略的提携の形成

- サービスとソフトウェア層に焦点を当てる

- 持続可能性への取り組みをリードする

調査の過程で分析した他の企業:

- 株式会社日立製作所

- ノーテックエアソリューションズ

- エアデールインターナショナルエアコンディショニング株式会社

- ファーウェイテクノロジーズ株式会社

- ジョンソンコントロールズ

- グリーン・レボリューション・クーリング株式会社(GRC)

- クールITシステムズ株式会社

- サブマーテクノロジーズSL

- nVent Electric plc

免責事項:上記の企業は、特定の順序でランク付けされているわけではありません。

データセンター冷却市場のニュースと最近の動向

- シュナイダーエレクトリック、新たなデータセンターソリューションを発表:エネルギー管理と自動化におけるデジタルトランスフォーメーションのリーダーであるシュナイダーエレクトリックは、2025年11月、次世代AIクラスターアーキテクチャの厳しい要求に応えるために特別に設計された新たなデータセンターソリューションを発表しました。EcoStruxure™データセンターソリューションポートフォリオを進化させ、シュナイダーエレクトリックは、液体冷却、高出力バスウェイ、高密度NetShelterラックのためのインフラストラクチャを統合した、プレファブリケーション型モジュラーEcoStruxure Podデータセンターソリューションを発表しました。

- OVHcloud、次世代AI搭載冷却システムを発表:2025年10月、OVHcloudはデータセンター向けの新たな冷却アーキテクチャを発表しました。OVHcloudスマートデータセンターは、最新の工業デザインとAI機能を組み合わせ、電力と水の消費量を削減し、データセンターが周囲の環境にインテリジェントに対応できるようにします。この新技術により、OVHcloudは水の消費量を最大30%、冷却電力の消費量を最大50%削減できます。

データセンター冷却市場レポートの対象範囲と成果物

「データセンター冷却市場の規模と予測(2021〜2031年)」レポートでは、以下の分野をカバーする市場の詳細な分析を提供しています。

- データセンター冷却市場の規模と予測、スコープに含まれるすべての主要市場セグメントの世界、地域、国レベルでの予測

- データセンター冷却市場の動向、および推進要因、制約、主要な機会などの市場動向

- 詳細なPEST分析とSWOT分析

- 主要な市場動向、世界および地域の枠組み、主要プレーヤー、規制、最近の市場動向を網羅したデータセンター冷却市場分析

- データセンター冷却市場の市場集中、ヒートマップ分析、主要プレーヤー、最近の動向を網羅した業界の展望と競争分析

- 詳細な企業プロフィール

アンキタは、テクノロジー、メディア、ICT、エレクトロニクス・半導体の各分野で8年以上の経験を持つ、ダイナミックな市場調査およびコンサルティングのプロフェッショナルです。Microsoft、Oracle、NEC、SAP、KPMG、Expeditors Internationalといったグローバルクライアントに対し、100件以上のコンサルティングおよび調査案件を主導・遂行してきました。彼女のコアコンピテンシーは、市場評価、データ分析、予測、戦略策定、競合情報、レポート作成です。

アンキタは、販売前の提案書作成やクライアントとの協議から、販売後の実用的なインサイトの提供まで、プロジェクトサイクル全体を巧みに管理することに長けています。彼女は、部門横断的なチームの管理、複雑な調査モジュールの構築、そしてクライアント固有のビジネス目標に合わせたソリューションの調整に長けています。優れたコミュニケーション能力、リーダーシップ、そしてプレゼンテーション能力により、急速に変化する市場環境において、常に価値主導の成果を生み出しています。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応