5G Chipset Market Size, Share & Trends by 2034

Coverage: By Type (Modem, RFIC); Process Node (Less Than 10 nm, Between 10-28 nm, Above 28 nm); Frequency (Sub-6 GHz, 24-29 GHz, Above 39 GHz); End User (IT & Telecom, Manufacturing, Media & Entertainment, Healthcare, Energy & Utilities, Others); and Geography

- Status : Data Released

- Report Code : TIPEL00002370

- Category : Electronics and Semiconductor

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 10, 2026

2025 Market Size

US$ 59.98 Bn

Base year value

2034 Forecast

US$ 307.85 Bn

Projected by 2034

CAGR 2026-2034

19.93 %

Growth rate

Addressable Market

US$ 1,491.65 Bn

(2026-2034)

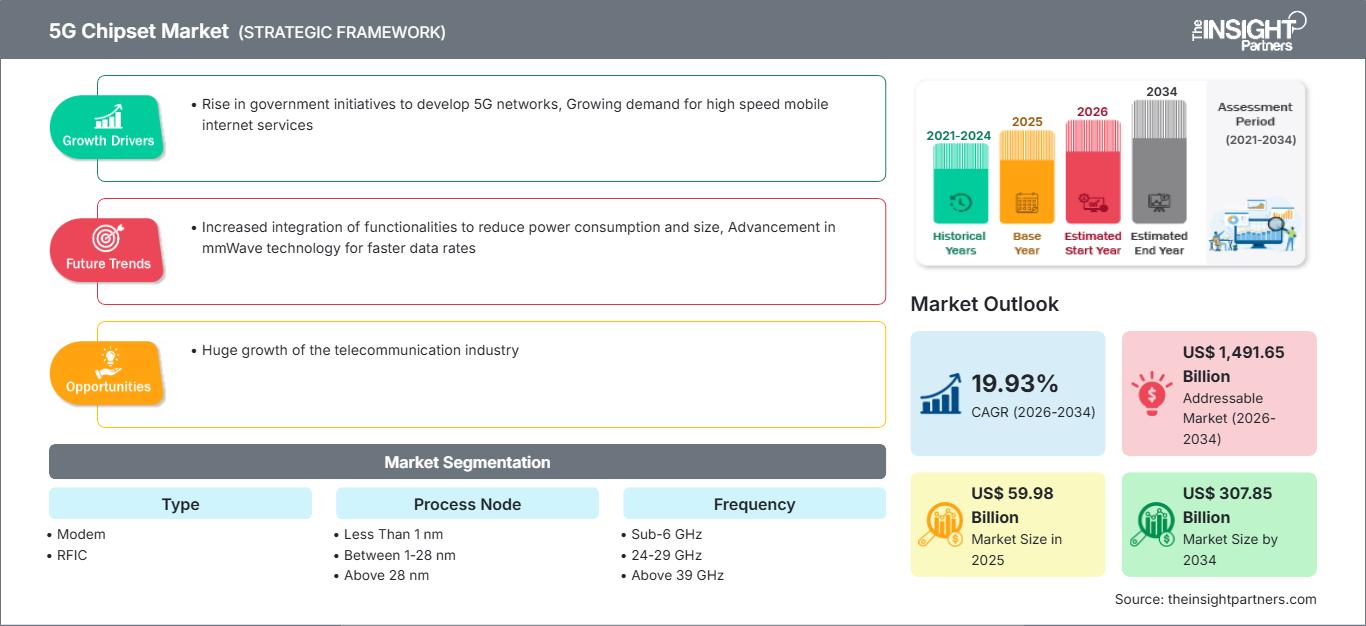

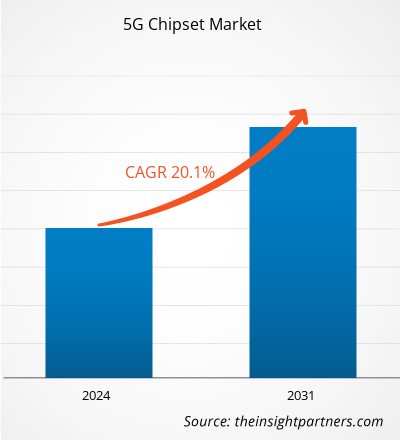

The 5G Chipset Market was valued at US$ 59.98 Billion in 2025 and is projected to reach US$ 307.85 Billion by 2034, expanding at a CAGR of 19.93% during 2026–2034. The market will be characterized by increasing need for modem and RFIC solutions for smartphones, fixed wireless access, private networks, industrial IoT, healthcare, media systems, energy networks, and telecommunication devices.

North America will grow at a CAGR of 18.5% to 19.5% from 2026 to 2034, driven by the uptake of premium smartphones, fixed wireless access, private 5G, connected cloud-based factories, and testing of 5G Advanced technology. According to Ericsson, North America was able to penetrate its market with 5G subscriptions at 79% in 2025.

5G Chipset Market Assessment and Insights

- North America held 25%–29% share in 2025 and is expected to grow at a 18.5%–19.5% CAGR between 2026–2034 as operators expand FWA, standalone 5G, and enterprise connectivity.

- The US represented 80%–86% of North America in 2025 and is projected to grow at a 18.8%–19.4% CAGR, led by premium devices and private networks.

- Europe accounted for 19%–23% share in 2025 and is expected to grow at a 17.5%–18.8% CAGR, with Germany, the UK, France, Italy, and Spain leading demand.

- Asia Pacific held 41%–46% share in 2025 and is projected to grow at a 20%–21% CAGR, led by China, South Korea, Japan, India, and Taiwan.

- Largest Segment: Modem captured 63%–68% market share in 2025 and is expected to grow at a 19%–20% CAGR due to handset, CPE, and IoT demand.

- High Growth Segment: RFIC held 32%–37% market share in 2025 and is projected to grow at a 20%–21.5% CAGR as multi-band device complexity rises.

- Key companies analyzed in detail: Broadcom Inc.; Huawei Technologies Co., Ltd.; Infineon Technologies AG; MediaTek Inc.; Nokia Corporation; Qualcomm Incorporated; Intel Corporation; UNISOC Technologies Co., Ltd.; Samsung Electronics Co., Ltd.; Qorvo, Inc.; Marvell Technology, Inc.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

The 5G Chipset Market has progressed from the focus on the provision of modems to handsets into an ecosystem of connectivity semiconductors. Today's production depends on the use of advanced nodes for the processing of modems, mature nodes for radio-frequency and power, chip-making, and design validation. The market size will be affected by 5G Advanced, satellite, artificial intelligence, and integrated modem-RF solutions.

Future demand will include the expansion of new markets because of the affordability of 5G handsets in new geography, adoption of private 5G networks by industries, and availability of mid-band and mmWave spectrum through regulations. GSA reported 26 operators in 15 countries investing in 5G Advanced in 2025, while Ericsson forecast 6.4 billion 5G subscriptions by 2031, reinforcing the long-term 5G Chipset Market growth pathway.

5G Chipset Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 59.98 Billion |

| Market Size by 2034 | US$ 307.85 Billion |

| Global CAGR (2026 - 2034) | 19.93% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

5G Chipset Market Analysis

Demand is supported by increasing demand for mobile data, standalone 5G migration, fixed wireless access, industry IoT, and increasing semiconductor content per connected endpoint. As shown in the market analysis, modem-RF capability influences battery life, uplink capability, latency, spectrum flexibility, and device certification, which makes chipset choice a strategic choice for original equipment manufacturers and network equipment providers.

The value chain consists of fabless design houses, foundries, OSAT companies, RF component companies, device OEMs, telecom equipment suppliers, module manufacturers, operators, and enterprise integrators. Supply conditions are still affected by advanced node capacity, RF front-end components, export regulations, and validation periods. This implies that the 5G Chipset Market scope covers consumer electronics, infrastructure, automotive, energy, healthcare, manufacturing, and media applications.

Competition is concentrated but multidimensional. Qualcomm Incorporated and MediaTek Inc. lead across commercial modem platforms, Samsung Electronics Co., Ltd. and Huawei Technologies Co., Ltd. support integrated device ecosystems, while Broadcom Inc., Qorvo, Inc., Infineon Technologies AG, Intel Corporation, Marvell Technology, Inc., Nokia Corporation, and UNISOC Technologies Co., Ltd. influence RF, infrastructure, edge, and value-tier demand.

Trends in investment involve 5G Advanced technology, AI-enabled modems, 3GPP Release 18 compatibility, non-terrestrial networking, RF integration, and robust platforms. Trends in strategic positioning involve moving beyond mere high downlink speeds to value propositions involving operator validation, low power consumption, robust uplink capabilities, software-upgradability, wideband spectrum availability, and speed to market for devices.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

5G Chipset Market: Strategic Insights

Regional Insights

North America 5G Chipset Market

North America held 25%–29% share in 2025 and is projected to grow at a 18.5%–19.5% CAGR through 2034. Demand is supported by operator mid-band investment, fixed wireless access, premium smartphones, private enterprise networks, and AI-ready edge devices. Ericsson reported North America had 79% 5G subscription penetration in 2025, strengthening replacement demand for advanced modem-RF systems.

The strongest regional adoption is seen in smartphones, broadband gateways, industrial gateways, connected cars, healthcare devices, and media streaming devices. Qualcomm Incorporated, Broadcom Inc., Intel Corporation, Qorvo, Inc., Marvell Technology, Inc., Nokia Corporation, Samsung Electronics Co., Ltd., and MediaTek Inc. provide assistance in designing, RF testing, infrastructure validation, and ecosystem validation. The region favors suppliers that combine performance leadership with carrier certification and security readiness, reflecting evolving 5G Chipset Market Trends.

U.S. 5G Chipset Market

The US represented 80%–86% of North America in 2025 and is expected to expand at a 18.8%–19.4% CAGR during 2026–2034. Demand is centered on high-end smartphones, 5G CPE, enterprise routers, connected cars, health monitoring, live streaming applications, military communications, and industrial automation gateways that need secure and high-bandwidth-low-latency connectivity.

Corporate participation is widespread in modern technology, RF front-end devices, cloud computing systems, edge computing chips, and telecommunications equipment. Some of the corporations supporting the application trends in broadband connectivity, intelligent manufacturing, power grids, and telemedicine include Qualcomm Incorporated, Broadcom Inc., Intel Corporation, Qorvo, Inc., Marvell Technology, Inc., Samsung Electronics Co., Ltd., MediaTek Inc., Nokia Corporation, and Infineon Technologies AG.

Europe 5G Chipset Market

Europe accounted for 19%–23% share in 2025 and is projected to grow at a 17.5%–18.8% CAGR. In the United Kingdom, modernized operators, connectivity in media, digitization in healthcare, and enterprise pilots will be beneficial. The demand for chipsets capable of delivering sub-6 GHz speeds, security of enterprise networks, and energy-efficient broadband devices is high.

Germany is the lead country due to automotive engineering, intelligent factories, machinery manufacture, robotics, and private 5G campus facilities. Reliable low-latency chipsets that enable machines to communicate, predict failures, and perform automated quality checks are required by industrial companies. Infineon Technologies AG, Nokia Corporation, Qualcomm Incorporated, Broadcom Inc., and Samsung Electronics Co., Ltd. are key players.

France, Italy, and Spain contribute via public infrastructure development, telecom developments, modernization of manufacturing sector, smart cities, utilities, and content delivery services. France is strong in enterprises and public network solutions, while Italy is strong in industrial modernization, and Spain in broadband and venue solutions. European success will be determined by spectrum policies, investment of operators in capital spending, and tangible benefits from private 5G network operations, thus boosting 5G Chipset Market Size.

APAC 5G Chipset Market

APAC held 41%–46% share in 2025 and is projected to grow at a 20%–21% CAGR. China is the leading country, supported by smartphone manufacturing, telecom scale, industrial digitization, and semiconductor localization. South Korea and Japan add premium device, robotics, automotive, and consumer electronics demand.

India is becoming a major expansion market as affordable 5G smartphones, fixed wireless access, and local manufacturing incentives scale. Australia contributes through mining, utilities, remote broadband, and enterprise connectivity. Samsung Electronics Co., Ltd., Huawei Technologies Co., Ltd., MediaTek Inc., UNISOC Technologies Co., Ltd., Qualcomm Incorporated, and Nokia Corporation influence regional demand.

The drivers of policy development involve spectrum growth, electronics manufacturing incentives, smart industry initiatives, and national digital infrastructure. Volume production is influenced by the number of devices in APAC, whereas the advanced economies dictate the premium modem, RFIC, and 5G Advanced adoption.

Middle East & Africa 5G Chipset Market

Middle East & Africa is expected to grow at a 21%–22.5% CAGR during 2026–2034. The UAE is the leading country due to advanced telecom networks, smart cities, premium devices, and enterprise digitization. Saudi Arabia expands through energy, logistics, infrastructure, and industrial diversification programs.

Rugged CPE, gateways, remote asset management, and secure private networking are among the needs of the energy and infrastructure users. There is selective use of mobile broadband, mining, health, education, ports, and public infrastructure services in South Africa and Rest of MEA.

Affordability, spectrum availability, and availability of devices continue to pose challenges. The deployment of fixed wireless access is beneficial in areas where rolling out fiber is expensive, while 5G technology is useful for utility companies and industries with dispersed assets.

Segmentation Analysis

Type

The Type segment is expected to grow at a 19%–20.5% CAGR during 2026–2034. Demand is led by integrated modem-RF platforms, but RFIC complexity is rising as devices support more spectrum bands, higher uplink performance, and compact antenna designs across handsets, gateways, industrial modules, and connected equipment.

- Modem platforms lead adoption because they manage 5G connectivity, carrier aggregation, protocol compatibility, latency, and device certification across smartphones, CPE, vehicles, industrial gateways, and satellite-ready devices.

- RFIC demand is strategically important as devices require efficient signal conversion, filtering coordination, power amplification support, and multi-band operation across sub-6 GHz and mmWave frequencies.

Process Node

The Process Node segment is projected to grow at a 18.8%–20.2% CAGR during 2026–2034. Advanced nodes support high-performance modem processing and AI features, while mature nodes remain critical for RF, power management, and cost-sensitive components. This mix makes process strategy central to performance, margins, and supply resilience.

- Less Than 1 nm remains a forward-looking category tied to future ultra-dense semiconductor architectures that could support 6G-ready modem intelligence and highly integrated RF processing.

- Between 1-28 nm represents the strategic core for commercial 5G chipsets, balancing performance, power efficiency, integration density, and scalability across premium and mid-range devices.

- Above 28 nm remains relevant for mature RF, power, and supporting connectivity components where cost control, reliability, and adequate performance outweigh leading-edge density.

Frequency

The Frequency segment is expected to grow at a 18.7%–20.8% CAGR during 2026–2034. Sub-6 GHz remains the practical coverage layer, while mmWave bands support high-capacity urban, venue, and FWA use cases. Chipset vendors must balance antenna complexity, thermal efficiency, and spectrum support.

- Sub-6 GHz dominates practical deployment because it balances coverage, capacity, indoor performance, and device compatibility for smartphones, fixed wireless access, and enterprise connectivity.

- 24-29 GHz supports high-capacity mmWave services in dense urban areas, venues, and FWA deployments where short-range throughput and spectrum depth justify advanced RF designs.

- Above 39 GHz remains specialized, supporting ultra-high-capacity trials, dense network zones, and future applications where beamforming precision and device ecosystem maturity improve.

End User

The End User segment is projected to grow at a 19.1%–20.6% CAGR during 2026–2034. IT and telecom remain the largest demand base, while manufacturing, healthcare, media, and energy applications expand the 5G Chipset Market trends beyond consumer devices into mission-critical connectivity, edge computing, and industrial automation.

- IT & Telecom leads because operators, cloud providers, network vendors, and device ecosystems depend on 5G chipsets for broadband access, smartphones, network equipment, and enterprise services.

- Manufacturing adoption rises through private 5G, robotics, machine vision, predictive maintenance, and connected production assets requiring reliable low-latency communication inside industrial environments.

- Media & Entertainment uses 5G chipsets for immersive content, live streaming, mobile gaming, connected venues, and high-throughput consumer devices requiring stable broadband performance.

- Healthcare demand grows through remote monitoring, connected medical devices, hospital networks, telehealth equipment, and real-time data transmission where reliability, security, and mobility are critical.

- Energy & Utilities adoption is supported by smart grids, field monitoring, connected substations, remote asset inspection, and industrial communications across distributed infrastructure networks.

Opportunity Snapshot

| End User | Revenue Contribution | Trend Tag | Adoption Stage |

| IT & Telecom | High | FWA Expansion | Mature |

| Manufacturing | Medium | Private 5G | Scaling |

| Media & Entertainment | Medium | Immersive Media | Scaling |

| Healthcare | Low | Remote Care | Emerging |

| Energy & Utilities | Medium | Grid Connectivity | Scaling |

5G Chipset Market Growth Drivers and Impact Analysis

5G Advanced Migration Raises Modem-RF Requirements

Migration toward 5G Advanced is increasing chipset requirements across smartphones, CPE, industrial gateways, vehicles, and enterprise devices. 3GPP Release 18 adds enhancements for AI, energy efficiency, XR, non-terrestrial networks, industrial needs, and network slicing. GSA reported that 5G Advanced investment was still early in 2025, creating replacement potential as networks and devices mature. The market impact is clear: buyers are shifting from basic 5G compatibility toward validated uplink performance, power efficiency, spectrum flexibility, and software upgradeability. Vendors with integrated modem-RF systems, AI-assisted tuning, and Release 18 roadmaps can capture premium design wins, strengthening their market Share while extending platform lifecycles.

Fixed Wireless Access Expands Beyond Handsets

Fixed wireless access is widening chipset demand beyond smartphones by creating high-volume requirements for routers, outdoor CPE, gateways, and integrated broadband devices. Ericsson reported that 71% of FWA providers offered FWA over 5G in 2026, while global FWA connections are forecast to rise from 185 million in 2025 to 350 million by 2031. This changes market economics because CPE devices require sustained throughput, thermal efficiency, RF stability, security, and operator certification, supporting continued 5G Chipset Market Growth. Chipset vendors that deliver cost-effective, power-efficient platforms for broadband access can benefit from telecom operators seeking faster coverage expansion without universal fiber deployment.

Industrial Connectivity Increases Semiconductor Content

Industrial digitization is increasing semiconductor content in factories, utilities, ports, mines, hospitals, and logistics networks. Private 5G, robotics, machine vision, smart meters, remote monitoring, and connected substations require chipsets with secure authentication, predictable latency, and long lifecycle support. The IEA has emphasized digitalization in energy systems, while WHO-linked healthcare digitization priorities reinforce reliable connectivity needs in medical environments. Market impact is broader demand diversity and lower dependence on handset cycles. Suppliers that combine low power, rugged reliability, industrial software support, and flexible spectrum compatibility can convert pilots into repeatable enterprise deployments, reinforcing the positive 5G Chipset Market Forecast.

5G Chipset Market Future Trends

AI-Native Modem-RF Optimization

The optimization of modems RF will be done using native AI for adaptation to congested, mobile, thermal, antenna, and application traffic conditions. The Qualcomm X85 platform focuses on on-device AI for optimized 5G Advanced operation, while the Mediatek M90 roadmap focuses on AI-enabled modem operations and satellite support. The trend will move the focus of competition from maximum speed claims to intelligent connectivity experience that enhances battery life, uplink quality, latency, and handover capability. Premium smartphones will adopt these capabilities first, but CPE, connected vehicles, industrial gateways, XR devices, and private-network endpoints will increasingly require adaptive connectivity to maintain service quality in complex radio environments, helping leading suppliers strengthen their 5G Chipset Market Share.

Terrestrial and Satellite Connectivity Convergence

Terrestrial and satellite connectivity are converging as modem platforms add non-terrestrial network support for emergency messaging, remote monitoring, maritime communication, mining, energy operations, and rural coverage. 3GPP Release 18 further integrates satellite access into the 5G system, making chipset readiness more relevant for resilient communications. Future adoption will depend on standards maturity, operator partnerships, satellite economics, device power efficiency, and certification, aligning with emerging 5G Chipset Market Trends. The strongest use cases will emerge where terrestrial networks are unavailable or unreliable, enabling devices to maintain minimum connectivity for safety, logistics, infrastructure monitoring, and field operations beyond urban coverage zones.

5G Chipset Market Opportunities

Industrial Private 5G and Edge Platforms

Industrial private 5G offers a high-value opportunity because factories, ports, mines, utilities, and logistics hubs need secure wireless systems for robotics, video analytics, predictive maintenance, connected tools, and autonomous equipment. Investment should focus on industrial modules, rugged CPE, gateways, edge devices, and reference designs optimized for long lifecycle deployments. Nokia Corporation, Intel Corporation, Qualcomm Incorporated, Infineon Technologies AG, Broadcom Inc., Marvell Technology, Inc., and Samsung Electronics Co., Ltd. can participate through infrastructure, processors, RF components, and connectivity platforms. Vendors that align with system integrators and application providers can move enterprises from pilots to scaled deployments.

Affordable 5G Devices in Emerging Economies

Affordable 5G devices create a large opportunity as India, Southeast Asia, Africa, Latin America, and parts of the Middle East move from 4G-heavy installed bases toward mass 5G adoption. The opportunity includes smartphones, routers, education devices, retail terminals, healthcare equipment, and enterprise connectivity products, supporting sustained 5G Chipset Market Size expansion. Action should prioritize mid-range modem platforms, simplified RF designs, power-efficient integration, and partnerships with local manufacturers. MediaTek Inc., UNISOC Technologies Co., Ltd., Qualcomm Incorporated, Samsung Electronics Co., Ltd., Huawei Technologies Co., Ltd., and Broadcom Inc. can address different price tiers as operators seek stronger returns on spectrum investment.

Recent Developments

- In July 2025: HPE completes USD 14 billion Juniper Networks acquisition (July 2025): Hewlett Packard Enterprise (HPE) completed its acquisition of Juniper Networks, strengthening its position in AI-driven networking, hybrid cloud, and enterprise infrastructure. The deal combines HPE’s networking portfolio with Juniper’s AI-native networking technology, including Mist AI capabilities, and aims to help HPE compete more strongly in the growing AI infrastructure market. The acquisition is expected to expand HPE’s networking business and support next-generation AI-powered networks.

- In December 2025: MediaTek launches Dimensity 7100 for mid-range 5G smartphones: MediaTek introduced the new Dimensity 7100 5G chipset, designed for affordable and mid-range smartphones with improved performance and power efficiency. Built on a 6nm process, it features an octa-core CPU with Arm Cortex-A78 cores, Mali-G610 GPU, support for LPDDR5 RAM, UFS 3.1 storage, and up to 200MP cameras. The chip offers better gaming, AI imaging, HDR display support, Wi-Fi 6, Bluetooth 5.4, and a 5G modem with speeds up to 3.3Gbps. MediaTek highlights efficiency improvements, including lower power consumption in apps, multimedia, and modem usage.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends