Diabetes Care Devices Market Dynamics and Trends by 2028

Diabetes Care Devices Market Forecast to 2028 - Analysis By Type (Glucose Monitoring Devices and Insulin Delivery Devices) and End User (Homecare and Hospitals & Clinics)

- Status : Published

- Report Code : TIPRE00003753

- Category : Life Sciences

- No. of Pages : 190

- Available Report Formats :

- Last update date : June 13, 2024

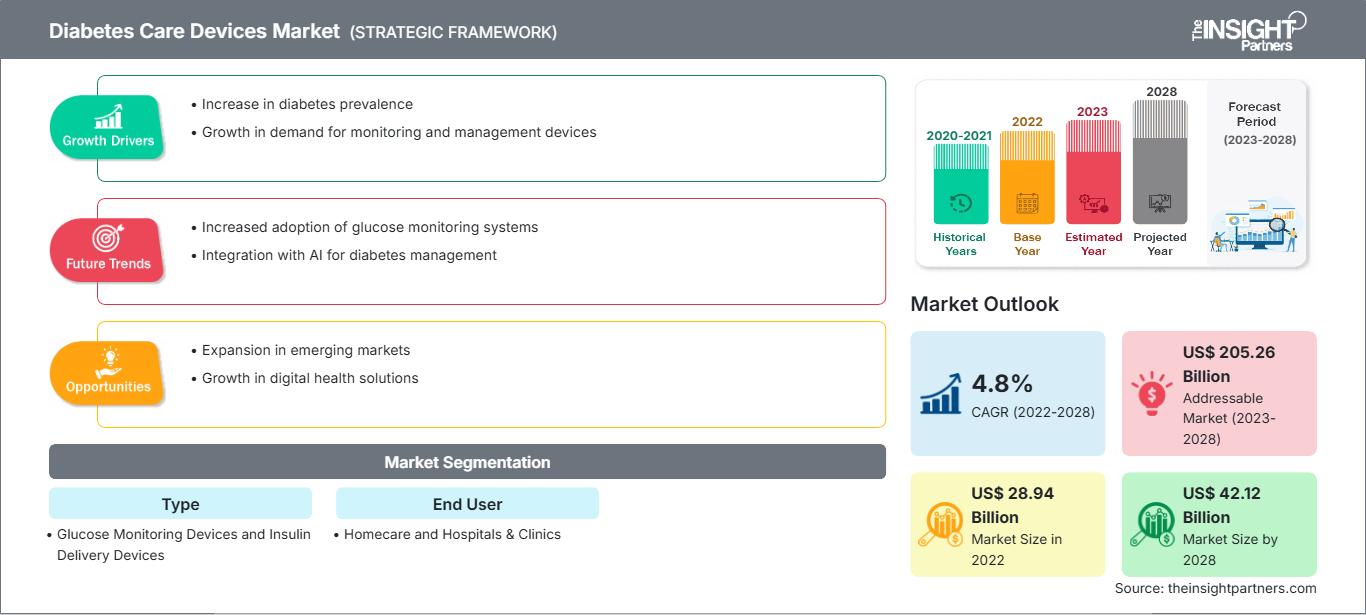

2022 Market Size

US$ 28.94 Bn

Base year value

2028 Forecast

US$ 42.12 Bn

Projected by 2028

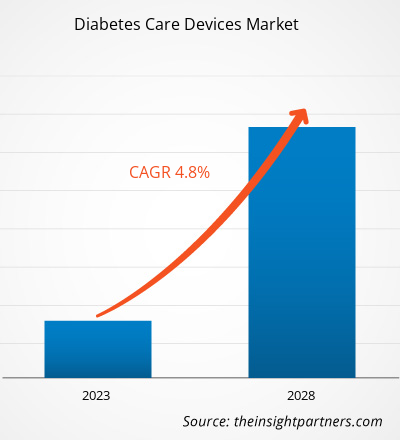

CAGR 2023-2028

4.8 %

Growth rate

Addressable Market

US$ 205.26 Bn

(2023-2028)

[Research Report] The diabetes care devices market is expected to grow from US$ 28,942.1 million in 2022 to US$ 42,119.3 million by 2028; it is estimated to grow at a CAGR of 4.8% from 2022 to 2028.

Market Insights and Analyst View:

The diabetes care devices are the medical devices are used to monitor the glucose levels in the blood of the diabetes patients. The monitoring devices are known as continuous glucose monitoring devices or glucometers. The other diabetes care devices are used to deliver insulin in the body, these devices are used by the diabetes patients who are unable to produce insulin by their own. The insulin delivery devices include insulin pumps, insulin pens, insulin syringes and others. Increase in technological advancements, rise in the incidences of obesity, increasing adoption of insulin delivery devices and rising prevalence of diabetes are driving the growth of the diabetes care devices market. Key manufacturers are focusing on technological innovations and development of advanced products to gain substantial share of the market. For instance, in April 2023, Medtronic plc received U.S. Food and Drug Administration (FDA) approval for its MiniMed 780G system. This system features the lowest glucose target setting (as low as 100 mg/dL) in any automated insulin pump on the market and one that more closely reflects the average glucose of person not living with diabetes.

Market Research Highlights

- North America dominated the market with 38.5% share in 2021.

- Asia Pacific is poised to grow at a CAGR of 5.2% over the forecast period.

- United States market is projected to grow at a CAGR of 5.1% over the forecast period.

- By Type, the Glucose Monitoring Devices segment accounted for the largest market share of 54.5% in 2021.

- By Glucose Monitoring Devices Type, the Test Strips segment is anticipated to witness the fastest growth, registering a CAGR of 5.5% over the forecast period

- By Insulin Delivery Devices Type, the Pen segment accounted for the largest market share of 33.7% in 2021.

- By End User, the Homecare segment is anticipated to witness the fastest growth, registering a CAGR of 5% over the forecast period

- The report profiles key industry players such as B Braun SE, BD, Terumo Corp, Medtronic Plc, F. Hoffmann-La Roche Ltd, Novo Nordisk AS, Eli Lilly and Co, Insulet Corp, Tandem Diabetes Care Inc, Dexcom Inc, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Diabetes Care Devices Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Growth Drivers and Opportunities:

Diabetes is a deadly chronic disease with no specialized cure. It is primarily caused by the body’s inability to produce or effectively use the hormone insulin. This inability prevents the body from adequately regulating blood glucose levels. There are two forms of diabetes—diabetes type-I or diabetes insipidus and diabetes type-2 or diabetes mellitus. The incidences of diabetes are steadily increasing globally. Type 2 diabetes is the most prevalent type of diabetes and has increased with cultural and societal changes. In high-income countries, ~91% of adults have type 2 diabetes. In 2021, as per the International Diabetes Federation (IDF), diabetes will affect ~537 million persons aged 20-79. Similarly, the total number of diabetics is expected to surge to 643 million by 2030 and 783 million by 2045.

Prevalence of Diabetes Worldwide among People aged 20-79 Years, 2021 vs 2030 vs 2045 (In Millions)

|

Region |

2021 |

2030 |

2045 |

|

North America & Caribbean |

51 |

57 |

63 |

|

South & Central America |

32 |

40 |

49 |

|

Africa |

24 |

33 |

55 |

|

Europe |

61 |

67 |

69 |

|

Middle East & North Africa |

73 |

95 |

136 |

|

South-East Asia |

90 |

113 |

152 |

|

Western Pacific |

206 |

238 |

260 |

Source: International Diabetes Federation (2022)

Diabetes can lead to several complications in various body parts and raise the overall risk of premature death. Heart attack, stroke, kidney failure, leg amputation, vision loss, and nerve damage are a few major complications associated with diabetes. Hence, patients suffering from this disease require frequent monitoring and external administration of insulin. The growing prevalence of diabetes is fuelling the growth of the diabetes care devices market worldwide during the forecast period.

Report Segmentation and Scope:

The “Global Diabetes Care Devices Market” is segmented based on product, end user, and geography. Based on product, the diabetes care devices market is segmented into glucose monitoring devices and insulin delivery devices. Based on end user, the diabetes care devices market is segmented into homecare and hospitals & clinics. The diabetes care devices market based on geography is segmented into North America (US, Canada, and Mexico), Europe (Germany, France, Italy, UK, Russia, and Rest of Europe), Asia Pacific (Australia, China, Japan, India, South Korea, and Rest of Asia Pacific), Middle East & Africa (South Africa, Saudi Arabia, UAE, and Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and Rest of South & Central America)

Segmental Analysis:

The global diabetes care devices market, based on product is segmented into glucose monitoring devices and insulin delivery devices. In 2022, the glucose monitoring devices segment hold the largest share of the market, by product. Moreover, the glucose monitoring devices segment of diabetes care devices market is also expected to witness growth in its demand at a fastest CAGR of 5.0% during 2022 to 2028. The glucose monitoring devices market consists of components such as glucometers, lancets, testing strips and other glucose monitoring devices. In 2022 testing strips segment hold the largest market share among the glucose monitoring devices segments. The glucose monitoring devices or glucose meters are medical devices are used to determine the approximate levels or the concentration of glucose in the blood of the patients living with diabetes. The concentration of the glucose level can be measured by various means such as through testing strips, lancets, and others.

The global diabetes care devices market, end user was segmented into home care and hospitals & clinics. In 2022, the homecare segment holds the largest share of the market, by end user. In addition, the segment is also expected to grow at the fastest rate during the coming years owing to the rise in the prevalence of the diabetes and it makes patients independent to manage and monitor their diabetes. The hospital is a multifaceted organization and an institute that provides health to people through complication however, the specialized treatments are offered with scientific equipment. The team of trained staff educated in the problems of modern medical science assists in providing better treatments. They are all coordinated together for the common goal of restoring and maintain good health. Hospitals serves a significant role by providing extensive range of medical services to the patient population suffering from wide variety of diseases.

Regional Analysis:

Based on geography, the diabetes care devices market is divided into five key regions: North America, Europe, Asia Pacific, South & Central America, and Middle East & Africa. In 2020, US held the largest share of the North America diabetes care devices market. The growth of the diabetes care devices market is estimated to have a larger share in the United States. In US diabetes care is among the most common and expensive chronic diseases. The highest rate of diabetes is commonly seen in the elder populations. However, the rise in the prevalence of the diabetes continues across the US and other than the elder population it is seen among the overweight and obese population. In 2021, according to the International Diabetes Federation (IDF), diabetes would affect approximately 32.2 million persons aged 20 to 79 across the US. Similarly, the total number of diabetics is expected to surge to 34.7 million by 2030 and 36.2 million by 2045. In the country the huge investments are being done however the country lags the other developed countries in terms of life expectancy, infant mortality and other related diseases. Nevertheless, the country has is performing well for the diabetes care and it ranks 4th among the other 11 leading developed countries. Although the rising prevalence of the diabetes is enforcing to enhance the care systems towards the diabetes.

The Asia Pacific diabetes care devices market is analyzed on the basis of the five major countries such as China, Japan, India, Australia, South Korea, and rest of Asia Pacific. However, Asia Pacific is estimated to register the highest CAGR during the forecast period. The diabetes care devices market in the region is largely held by countries such as China, Japan, and India. The growth of the market is majorly contributed by China, and the growth is attributed by the maximum production of diabetes care products and the availability of the product through the widest e-commerce chain. The prevalence of diabetes is significantly higher in China, the incidences for type 2 diabetes has rapidly increased in the country in the last few decades. The type 2 diabetes has become a leading problem in the country as it is more commonly found in the lower age group people. The leading causes that are contributing to the growth of the type 2 diabetes are genetic and environmental factors.

The rise in the prevalence of the diabetes is the important factors that is likely to drive the growth of the market. The world's most populous country has the highest number of diabetics compared to any other country globally – about 116 million in 2019. By 2045, this number is anticipated to reach 147 million. Additionally, as approximately 95% of patients with diabetes in China have type 2 diabetes, the rapid increase in the prevalence of diabetes in China may be attributed to the increasing rates of overweight and obesity and the reduction in physical activity, which is driven by economic development, lifestyle changes, and diet.

Industry Developments and Future Opportunities:

Various initiatives taken by key players operating in the global diabetes care devices market are listed below:

- In April 2023, Medtronic plc received U.S. Food and Drug Administration (FDA) approval of its MiniMed 780G system with the Guardian 4 sensor requiring no fingersticks while in SmartGuard technology.

- In April 2022, BD (Becton, Dickinson and Company) a leading global medical technology company, announced that it has completed its spinoff of Embecta Corp. (embecta), which holds BD's former Diabetes Care business and is now one of the largest pure-play diabetes management companies in the world.

- In March 2022, Medtronic plc, a global leader in healthcare technology, announced reimbursement for continuous glucose monitoring (CGM), a key diabetes technology has been expanded or initiated in several countries throughout North and South America. CGM systems provide critical information on glucose levels to help simplify the management of diabetes. Automated insulin pump system reimbursement has progressed in Europe as well.

- In January 2022, Drug firm Novo Nordisk India launched a first of its kind diabetes treatment medication in the country. The company introduced the world's first and only oral semaglutide, a game-changer in diabetes management.

- In March 2022, Terumo Corporation, a global leader in medical technology, and Glooko, a global leader in data management, remote patient monitoring and mobile apps for people with chronic conditions, have announced a technology integration to deliver new diabetes data sharing solutions together globally. This new integration will enable people with diabetes to transfer recorded data from MEDISAFE WITHTM insulin patch pump into the Glooko platform, thus helping them to visualize insulin dosage, food, and activities in graphs more easily and to realize personalized remote patient monitoring and patient care more effectively.

Diabetes Care Devices Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 28.94 Billion |

| Market Size by 2028 | US$ 42.12 Billion |

| Global CAGR (2022 - 2028) | 4.8% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Diabetes Care Devices Market Players Density: Understanding Its Impact on Business Dynamics

The Diabetes Care Devices Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Covid-19 Impact:

The COVID-19 pandemic affected economies and industries in various countries across the globe. Lockdowns, travel restrictions, and business shutdowns in North America, Europe, Asia Pacific (APAC), South & Central America (SAM), and the Middle East & Africa (MEA) hampered the growth of several industries, including the healthcare industry. As a result, health care systems are overburdened, and the delivery of medical care to all patients has become a challenge in the region. In addition, medical device industry is also facing negative impact of this pandemic. As the COVID-19 pandemic continues to unfold, medical device companies are finding difficulties in managing their operations. Many companies offering diabetes care devices have their business operations in the United States and business are adversely being affected by the effects of a widespread outbreak of COVID-19. This has disrupted and restricted company’s ability to distribute products, as well as temporary closures of company’s facilities. However, gradually hospitals have started resuming elective procedures as the COVID-19 recovery rate is increasing the demand for medical equipment like diabetes care is expected to increase.

Competitive Landscape and Key Companies:

Some of the prominent players operating in the global diabetes care devices market include BD; Novo Nordisk A/S; Medtronic; B. Braun Melsungen AG; Tandem Diabetes Care Inc.; Insulet Corporation; Eli Lilly and Company; Dexcom, Inc.; Terumo Corporation; F. Hoffmann-LA Roche LTD among others. These diabetes device companies focus on new product launches and geographical expansions to meet the growing consumer demand worldwide and increase their product range in specialty portfolios. They have a widespread global presence, which provides them to serve a large set of customers and subsequently increases their market share. The report offers trend analysis of the diabetes care device market emphasizing on various parameters such as technological advancements, market dynamics, and competitive landscape analysis of leading market players across the globe.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends