Glucose Monitoring Devices Market Size and Competitive Analysis by 2030

Coverage: By Type (Continuous Glucose Monitoring Devices, Self-Glucose Monitoring Devices), Application (Type 1 Diabetes and Type 2 Diabetes), Testing Type (Fingertip Testing and Alternate Site Testing), End User (Healthcare Settings and Self/Homecare), and Geography

- Status : Published

- Report Code : TIPRE00004116

- Category : Life Sciences

- No. of Pages : 205

- Available Report Formats :

- Last update date : July 25, 2024

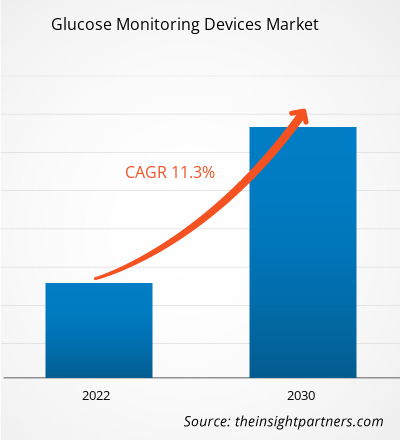

2022 Market Size

US$ 16,803.63 Mn

Base year value

2030 Forecast

US$ 39,530.75 Mn

Projected by 2030

CAGR 2022-2030

11.3 %

Growth rate

Addressable Market

US$ 224,237.21 Mn

(2022-2030)

The glucose monitoring devices market size is expected to grow from US$ 16,803.63 million in 2022 to US$ 39,530.75 million by 2030; it is estimated to register a CAGR of 11.3% from 2022 to 2030. Rapid Technological advancements in glucose monitoring devices will likely remain a key trend in the market.

Glucose Monitoring Devices Market Analysis

The primary factors propelling the market development are the growing geriatric population, rising incidence of diabetes, rising global prevalence of obesity, and the increasing number of product innovations. Moreover, products with cutting-edge technology provide better results when treating diabetes. Globally, the prevalence of diabetes is rising, which drives up demand for more advanced products. Thus, every year, new products are being developed as a result of research studies carried out by researchers.

Due to improvements in glucose monitoring technology, smaller blood volumes are needed for better accuracy. Additionally, glucose monitoring devices and blood glucose meters have better data transfer capability. Technological developments in blood glucose monitoring have increased accuracy, decreased blood volume requirements, and data transfer between glucose monitoring devices and blood glucose meters. For instance, Abbott unveiled a new wearable in June 2022 that uses a single sensor to monitor ketone and glucose levels continuously.

Glucose Monitoring Devices Market Overview

Sedentary lifestyles, poor diets, and obesity are the leading causes of obesity and diabetes cases. According to research published in the Journal of the American Heart Association, 30–53% of newly diagnosed cases of diabetes in the US each year are related to obesity. Obesity's effects raise the expense of medical care for prescription medications, inpatient care, and outpatient care. In the US, obesity-related medical expenses come to approximately US$ 260.6 billion a year. Thus, it is anticipated that there will be a greater need for glucose monitoring equipment in the upcoming years.

Market Assessment and Insights

- North America dominated the market with 35.6% share in 2022.

- Asia Pacific is poised to grow at a CAGR of 12.1% over the forecast period.

- United States market is projected to grow at a CAGR of 11.9% over the forecast period.

- By Type, the Self-Glucose Monitoring (SGM) Devices segment accounted for the largest market share of 58.4% in 2022.

- By Continous Glucose Monitoring (CGM) Devices, the Sensors segment is anticipated to witness the fastest growth, registering a CAGR of 12.4% over the forecast period

- By Self-Glucose Monitoring (SGM) Devices, the Testing Strips segment accounted for the largest market share of 53.6% in 2022.

- By Application, the Type 1 Diabetes segment is anticipated to witness the fastest growth, registering a CAGR of 11.7% over the forecast period

- By Testing Sites, the Fingertip Testing segment accounted for the largest market share of 68.9% in 2022.

- By End User, the Healthcare Settings segment is anticipated to witness the fastest growth, registering a CAGR of 12% over the forecast period

- The report profiles key industry players such as Abbott Laboratories, B Braun SE, Terumo Corp, Medtronic Plc, F. Hoffmann-La Roche Ltd, GE HealthCare Technologies Inc, Nipro Corp, Ypsomed Holding AG, LifeScan Inc, Ascensia Diabetes Care Holdings AG, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Glucose Monitoring Devices Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Glucose Monitoring Devices Market Drivers and Opportunities

An increase in the Prevalence of Diabetes Favors Market Growth

Diabetes is a chronic illness that poses a severe risk to life. The primary cause of it is the body's incapacity to make or use the hormone insulin. This incapacity hinders the body's ability to control blood glucose levels appropriately. Diabetes comes in two varieties: diabetes type ll, commonly referred to as diabetes insipidus, and diabetes type l. Globally, both the incidence and prevalence of diabetes are continuously rising. The most common type of diabetes, type 2, has grown in frequency in tandem with societal and cultural shifts. Up to 91% of adults with type 2 diabetes have the illness in high-income nations. By 2045, there will likely be 738 million diabetics worldwide, up from an estimated 537 million in 2021, as per the International Diabetes Federation (IDF). Patients who have diabetes require frequent monitoring and external administration of insulin. The rising prevalence of diabetes globally is driving the growth of the glucose monitoring devices market.

Significant Opportunities in Developing Regions

The governments of the Asia-Pacific region are concentrating on developing the medical tourism industry to increase revenue flow. By signing two strategic Memorandums of Understanding with well-known medical tourism and healthcare facilitators, Passage Asia and Ezy Healthcare, in May 2023, the Malaysia Healthcare Travel Council (MHTC) increased its global footprint and improved its seamless healthcare experience. A significant step forward in MHTC's mission to offer the most remarkable healthcare travel experience and expand into the Oceania region has been reached with these collaborations.

Additionally, in response to the pandemic, Abbott debuted a do-it-yourself version of its continuous glucose monitoring device in India in November 2020. For US$ 66.61, the reader is a one-time expense for the user, whereas the sensor may require replacement every three months for US$ 60.55. The sensor maps the sugar levels against factors like diet, exercise, and other factors over three months. It provides continuous readings for 14 days. The expanding Indian market presents prospects for foreign enterprises to enhance their earnings because of the nation's improving healthcare infrastructure.

Glucose Monitoring Devices Market Report Segmentation Analysis

Key segments that contributed to the derivation of the glucose monitoring devices market analysis are type, application, and end user.

- Based on type, the glucose monitoring devices market is divided into continuous glucose monitoring devices, self-glucose monitoring devices. The self-glucose monitoring devices segment held the most significant market share in 2022.

- By application, the market is categorized into type 1 diabetes and type 2 diabetes. The type 2 diabetes segment held the largest share of the market in 2022.

- Based on testing type, the glucose monitoring devices market is divided into fingertip testing, alternate site testing. The fingertip testing segment held the most significant market share in 2022.

- By end user, the market is segmented into healthcare settings and self/homecare. The self/homecare segment held the largest share of the market in 2022.

Glucose Monitoring Devices Market Share Analysis by Geography

The geographic scope of the glucose monitoring devices market report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The US, Canada, and Mexico comprise the three segments of the North American market for glucose monitoring devices. This region's market is growing because of the rising prevalence of diabetes and an aging population, which are the main factors driving the market's growth. Furthermore, technological advancements in monitoring devices further enhance the overall market growth. In the US alone, over 37 million children and adults have diabetes, according to a report by the American Diabetes Association. An estimated US$ 16,752 is spent on diagnosed diabetes each year in the US, of which US$ 9,601 is directly related to the disease.

Additionally, the United States spends a lot of money on hospital inpatient care (30% of total medical costs), prescription drugs to treat diabetes complications (30%), anti-diabetic drugs and diabetes supplies (15%), and doctor visits (13%). Thus, diabetes is so common in the US and costs so much to treat that the US population is adopting glucose monitoring devices faster, driving the market's growth.

Glucose Monitoring Devices Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 16,803.63 Million |

| Market Size by 2030 | US$ 39,530.75 Million |

| Global CAGR (2022 - 2030) | 11.3% |

| Historical Data | 2020-2021 |

| Forecast period | 2022-2030 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Glucose Monitoring Devices Market Players Density: Understanding Its Impact on Business Dynamics

The Glucose Monitoring Devices Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Glucose Monitoring Devices Market News and Recent Developments

The glucose monitoring devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the developments in the glucose monitoring devices market are listed below:

- Beurer India Pvt. Ltd, manufacturer of electric healthtech devices, has announced the launch of a blood glucose monitor device retailing for ₹1,200, which will be available in the market by September 2024. (Source: Beurer India Pvt. Ltd, News Latter, May 2024)

- Dexcom, a real-time continuous glucose monitoring (CGM) device manufacturer for people with diabetes, has launched its latest CGM system, Dexcom ONE+ in Ireland. Dexcom ONE+ uses Dexcom’s best-in-class and most accurate sensor design. (Source: Dexcom, News Latter, March 2024)

Glucose Monitoring Devices Market Report Coverage and Deliverables

The “Glucose Monitoring Devices Market Size and Forecast (2020–2030)” report provides a detailed analysis of the market covering below areas:

- Glucose monitoring devices market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Glucose monitoring devices market trends as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- Glucose monitoring devices market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments.

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the glucose monitoring devices market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends