Digital Diagnostics Market Size, Growth & Trends by 2034

Digital Diagnostics Market Size and Forecasts (2021–2034), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage : by Product (Hardware, Software and Services); Diagnosis Type (Cardiology, Oncology, Neurology, Radiology, Pathology); End User (Hospitals and Clinics, Clinical Laboratories); and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00040732

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 08, 2026

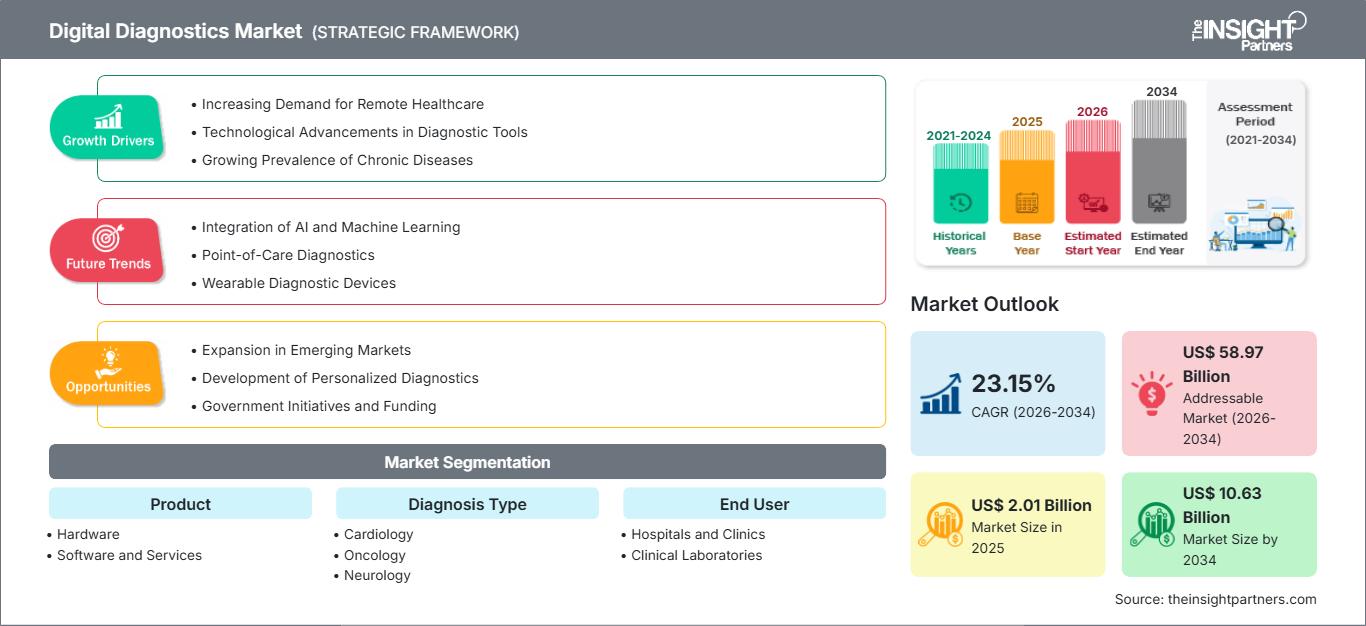

2025 Market Size

US$ 2.01 Bn

Base year value

2034 Forecast

US$ 10.63 Bn

Projected by 2034

CAGR 2026-2034

23.15 %

Growth rate

Addressable Market

US$ 58.97 Bn

(2026-2034)

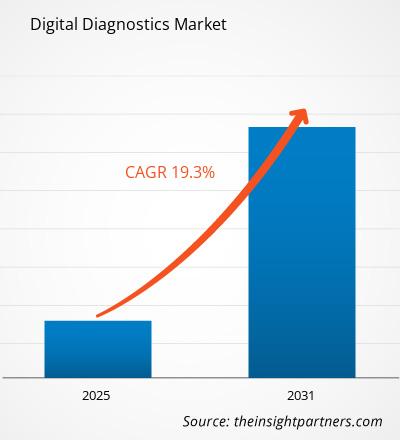

The Digital Diagnostics Market continues to gain strategic importance across modern healthcare systems as providers increasingly rely on data-driven diagnostic workflows, connected medical devices, and artificial intelligence-enabled clinical decision support. The market is estimated at approximately US$ 2.01 billion in 2025 and is projected to reach nearly US$ 10.63 billion by 2034, reflecting a robust growth trajectory at a CAGR of around 23.15% during 2026–2034. Rising demand for faster diagnosis, remote monitoring, and precision medicine is accelerating adoption across care settings.

North America remains a key revenue-generating region within the Digital Diagnostics Market, supported by a mature healthcare infrastructure and widespread digital health investments. The regional market is anticipated to advance at an estimated 22.4% CAGR through the forecast period. Increasing deployment of AI-assisted imaging platforms, growing chronic disease prevalence, and favorable reimbursement pathways for digital health technologies continue to strengthen regional demand across hospitals, laboratories, and specialty care networks.

Digital Diagnostics Market Assessment and Insights

- North America: North America accounted for 37–40% of the digital diagnostics market share in 2025 and is anticipated to expand at a CAGR of 21.8–22.6% during 2026–2034. Strong adoption of AI-powered diagnostics, integrated healthcare networks, and advanced clinical imaging platforms continues to support regional market leadership.

- U.S.: The U.S. represented 78–82% of the North American digital diagnostics market size in 2025 and is projected to register a CAGR of 22.0–22.8% during 2026–2034, driven by expanding digital pathology adoption, precision medicine initiatives, and large-scale healthcare digitization investments.

- Europe: Europe held 27–30% of the digital diagnostics market share in 2025 and is expected to grow at a CAGR of 21.0–22.0% during 2026–2034. Germany, the United Kingdom, and France remain leading markets, supported by expanding digital healthcare ecosystems and increasing deployment of AI-assisted diagnostic technologies.

- Asia Pacific: Asia Pacific accounted for 23–26% of the digital diagnostics market share in 2025 and is forecast to expand at a CAGR of 25.0–26.5% during 2026–2034. China, Japan, India, and South Korea continue to lead regional demand, driven by healthcare modernization initiatives, digital health policies, and growing investments in AI-enabled healthcare infrastructure.

- Largest Segment: Software and Services represented the largest digital diagnostics market segment and is expected to record a CAGR of 24.0–25.0% during 2026–2034, reflecting rising demand for AI algorithms, cloud-based analytics, and interoperable diagnostic platforms.

- Largest Segment: Diagnosis Type – Radiology represented the largest diagnosis segment and is expected to record a CAGR of 22.5–23.5% during 2026–2034, supported by increasing imaging volumes and wider adoption of AI-assisted image interpretation.

- High Growth Segment: Diagnosis Type – Pathology is projected to grow at a CAGR of 25.5–27.0% during 2026–2034, driven by accelerating adoption of digital pathology for biomarker discovery and precision oncology workflows.

- High Growth Segment: End User – Clinical Laboratories is projected to grow at a CAGR of 24.5–25.5% during 2026–2034, supported by increasing laboratory automation and the expansion of centralized digital diagnostic networks that improve operational efficiency and scalability.

- Key companies analyzed in detail: Abbott Laboratories; Roche Diagnostics International AG; Siemens Healthineers AG; Philips Healthcare; Medtronic plc; GE HealthCare Technologies Inc.; Thermo Fisher Scientific Inc.; Oracle Health (formerly Cerner Corporation); Becton, Dickinson and Company; Hologic, Inc.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

The digital diagnostics market report has transitioned from isolated software applications to integrated healthcare ecosystems connecting imaging systems, pathology platforms, laboratory information systems, wearable devices, and electronic health records. Advancements in computing power, cloud infrastructure, and machine learning have enabled healthcare organizations to improve diagnostic accuracy while reducing operational inefficiencies across clinical workflows.

Over the coming decade, market expansion will be influenced by increasing healthcare digitization, workforce shortages in diagnostic specialties, and demand for decentralized care delivery. Industry participants are focusing on interoperable solutions capable of integrating diverse clinical datasets, enabling healthcare providers to generate actionable insights and accelerate treatment decisions across multiple disease areas.

Digital Diagnostics Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 2.01 Billion |

| Market Size by 2034 | US$ 10.63 Billion |

| Global CAGR (2026 - 2034) | 23.15% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Digital Diagnostics Market Analysis

Healthcare providers increasingly face pressure to improve diagnostic turnaround times while managing growing patient volumes. Digital diagnostics addresses these challenges through automation, AI-assisted interpretation, and connected diagnostic ecosystems. Demand is particularly strong in oncology, cardiology, radiology, and pathology, where large volumes of clinical data require rapid and accurate analysis.

The value chain encompasses device manufacturers, software developers, cloud service providers, healthcare institutions, diagnostic laboratories, and data analytics specialists. Greater collaboration among these stakeholders is creating comprehensive platforms that combine image acquisition, analysis, reporting, and clinical decision support within unified environments.

Competition within the Digital Diagnostics Market is characterized by a blend of established healthcare technology companies and emerging digital health innovators. Organizations including Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, Philips Healthcare, Medtronic, GE Healthcare, Thermo Fisher Scientific, Cerner Corporation, Becton Dickinson, and Hologic continue to expand digital capabilities through partnerships, acquisitions, and software innovation.

Investment activity remains concentrated around AI-powered diagnostics, cloud-native healthcare applications, and precision medicine platforms. Strategic priorities increasingly include interoperability, cybersecurity, regulatory compliance, and scalable deployment models. Vendors capable of delivering integrated solutions that improve clinical outcomes while demonstrating economic value are expected to strengthen their competitive positions throughout the forecast period.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Digital Diagnostics Market: Strategic Insights

Regional Insights

North America Digital Diagnostics Market

North America accounts for the largest share of the Digital Diagnostics Market and is expected to register a CAGR of approximately 22.4% during the forecast period. Strong adoption of electronic health records, advanced diagnostic imaging systems, and AI-enabled healthcare solutions supports continued market expansion. Healthcare providers are increasingly integrating digital diagnostics into routine clinical workflows to improve patient outcomes and operational efficiency.

Strengths of this region include high levels of healthcare expenditure, technological innovation, and positive regulatory changes that enable digital health implementation. Growth in this region is further boosted by high rates of chronic disease, rising numbers of diagnostic tests, and increased funding for precision medicine initiatives across hospitals and laboratory networks.

U.S. Digital Diagnostics Market

The United States is considered the largest digital diagnostics market player in North America, with a share of about 72–76% of regional market revenues. The U.S. market is expected to grow at a CAGR of about 22.8% through 2034, driven by the widespread adoption of AI-powered diagnostics, imaging solutions, and connected healthcare infrastructure.

Key players in the industry carry out significant operations across different parts of the country, advancing oncology diagnostics, radiology automation, digital pathology, and remote patient monitoring. The growing use of predictive analytics, cloud-based diagnostics solutions, and clinical decision support systems has increased the demand among hospitals, academic medical centers, and clinical laboratories.

Europe Digital Diagnostics Market

Europe contributes an estimated 24–28% share of the global Digital Diagnostics Market and is projected to advance at a CAGR near 21.6% through the forecast period. Regional growth is supported by healthcare modernization initiatives, increasing deployment of digital pathology systems, and expanding use of AI-assisted diagnostic applications. Germany remains the leading national market due to its strong healthcare infrastructure and technology adoption.

The UK continues to make great strides in deploying digital healthcare projects, including improvements in diagnostic effectiveness and accessibility. Increasing investment in innovations such as virtual healthcare services, imaging systems, and AI-enabled solutions is driving market growth in the public and private healthcare sectors.

Germany remains a leader in Europe because of the active introduction of advanced imaging solutions, laboratory automation systems, and precision medicine projects. The use of integrated diagnostic systems by healthcare facilities to streamline clinical processes and rationalize resource use is becoming more common.

France, Italy, and Spain exhibit steady growth in the digital healthcare and diagnostics industry, driven by the increasing importance of these sectors within the broader healthcare sector.

APAC Digital Diagnostics Market

Asia Pacific is expected to be the fastest-growing regional digital diagnostics market, with a projected CAGR of approximately 25.8%. The region currently represents roughly 21–25% of global revenue and benefits from large patient populations, rising healthcare expenditures, and increasing adoption of digital health technologies. China remains the largest market within the region.

China has made considerable investments in digital healthcare services, AI innovations, and healthcare technology infrastructure. The government's interference in the development of healthcare and technology is contributing significantly to market growth.

Japan leverages its highly advanced healthcare system and its aging population dynamics to adopt digital diagnostic solutions. South Korea has a strong digital infrastructure and growing investments in the AI healthcare sector. There are increasing applications of telemedicine and diagnostic software in India, while Australia continues its digital healthcare implementation initiatives.

Middle East & Africa Digital Diagnostics Market

The Middle East & Africa Digital Diagnostics Market is projected to expand at a CAGR approaching 20.7% through 2034. Regional adoption is supported by healthcare infrastructure modernization, increasing diagnostic capacity, and growing interest in technology-enabled healthcare delivery. Saudi Arabia currently leads the regional market.

Saudi Arabia continues to invest in the digitalization of the healthcare industry in line with efforts towards economic diversification. Advanced hospitals, smart healthcare infrastructure, and digital transformation are leading to the adoption of digital diagnostic technology.

The UAE has emerged as an innovative market for digital healthcare products, but South Africa remains significant due to developments in laboratory facilities and rising demand for diagnostic services. Digital diagnostic instruments are increasingly used in MEA countries due to improved infrastructure and increased investment in the healthcare sector.

Segmentation Analysis

Product

- Hardware: Includes imaging devices, connected diagnostic instruments, sensors, and data acquisition systems that generate clinical information for digital interpretation, supporting real-time diagnostics and improved healthcare workflow efficiency.

- Software and Services: Represents the leading segment due to growing adoption of AI algorithms, analytics platforms, cloud-based diagnostics, workflow management tools, interoperability solutions, implementation services, and ongoing technical support.

Diagnosis Type

- Cardiology: Digital diagnostics support cardiac imaging interpretation, arrhythmia detection, remote monitoring, and predictive analytics, enabling clinicians to identify cardiovascular conditions earlier and improve treatment planning.

- Oncology: Advanced digital pathology, molecular diagnostics, AI-assisted imaging, and biomarker analysis support precision medicine initiatives and increasingly personalized cancer management strategies.

- Neurology: Utilizes imaging analytics, neurodiagnostic software, and AI-driven pattern recognition to improve detection and monitoring of neurological disorders, including neurodegenerative diseases and stroke.

- Radiology: Strong demand stems from AI-enhanced image interpretation, workflow optimization, and automated reporting capabilities that help address radiologist workload challenges and improve diagnostic consistency.

- Pathology: Digital slide scanning, image analysis software, and remote pathology review capabilities are transforming laboratory workflows and enabling collaborative diagnostic decision-making.

End User

- Hospitals and Clinics: Largest end-user category due to extensive diagnostic testing requirements, integrated healthcare infrastructure, and growing investments in digital transformation initiatives across care delivery settings.

- Clinical Laboratories: Increasingly adopt digital diagnostics to improve throughput, automate analytical processes, enhance quality control, and support complex testing requirements across multiple disease areas.

Opportunity Snapshot

| End User | Revenue Contribution | Trend Tag | Adoption Stage |

| Hospitals and Clinics | High | AI Workflow | Mature |

| Clinical Laboratories | Medium | Lab Automation | Scaling |

Digital Diagnostics Market Growth Drivers and Impact Analysis

Growing Adoption of Artificial Intelligence in Clinical Diagnostics

The use of artificial intelligence in diagnostic processes is on the rise due to its benefits in speed, precision, and uniformity. Artificial intelligence can process large amounts of data in less time than manual analysis, which is especially useful in fields with a shortage of professionals, such as radiology and pathology. The implementation of AI technology is seen as an important step towards enhancing clinical decision-making and minimizing inconsistencies. In addition to improving efficiency, more sophisticated algorithms can identify disease patterns that are not easily detected by conventional methods. With increasing regulation and growing confidence among health facilities in AI, demand for digital diagnostic platforms continues to accelerate globally.

Expansion of Remote Healthcare and Connected Care Models

The provision of healthcare services is increasingly moving outside clinical settings. Remote patient monitoring systems, wearables, telemedicine platforms, and cloud-based diagnostic systems are generating large volumes of health data that need to be analyzed digitally. Digital diagnostics are crucial for enabling continuous patient monitoring and clinical interventions. The ability to provide decentralized healthcare services will prove extremely useful for managing chronic illnesses, rural healthcare, and elderly populations. Digital diagnostic tools that analyze real-time patient data are becoming an integral part of healthcare facilities as healthcare systems seek to scale patient monitoring and preventive healthcare practices.

Rising Demand for Precision Medicine and Personalized Care

The trend in the healthcare industry is shifting towards individualized treatments based on patients' clinical profiles. Precision medicine needs a high-level diagnostic system capable of analyzing complex biological, imaging, and clinical datasets. Digital diagnostics technology enables this transformation by integrating multiple sources of information into clinically relevant information. In fields such as oncology, neurology, and cardiology, these technological advancements have greatly benefited patients. Better diagnostics enable better targeted treatments and improved patient management. As healthcare providers seek evidence-based approaches to personalized care, investment in digital diagnostic technologies is expected to remain a major driver of market growth.

Digital Diagnostics Market Future Trends

Convergence of Multimodal Diagnostic Data Platforms

Future diagnostic systems will increasingly reflect digital diagnostics market trends by integrating imaging, pathology, genomics, laboratory, and population health management data through unified platforms. This approach enables physicians to access comprehensive diagnostic information from a single interface instead of multiple systems. With developments in interoperability standards and cloud computing technology, this kind of system has become feasible to implement. Organizations that can integrate various types of clinical data easily will be able to reap competitive advantages from this trend. The trend is expected to improve diagnostic confidence, streamline clinical workflows, and support increasingly sophisticated precision medicine applications across healthcare systems.

Growth of Cloud-Native Diagnostic Ecosystems

Cloud computing is revolutionizing the way diagnostic information is processed, analyzed, and distributed. Cloud-native systems are becoming a preferred choice for healthcare companies for scalability, remote access, and continuous software updates. Among the fields benefiting from cloud-based deployment are digital pathology, radiology, and laboratory diagnostics. Future developments in the market can be seen in secure information exchange, enhanced analytics, and global accessibility. In the future, a cloud-native diagnostic ecosystem could become the cornerstone of digital healthcare infrastructure.

Digital Diagnostics Market Opportunities

Expansion of Digital Diagnostics in Emerging Healthcare Systems

Digital diagnostic services present significant opportunities across developing economies as healthcare expansion and digitalization initiatives accelerate. Many healthcare organizations are seeking cost-effective ways to strengthen diagnostic capabilities despite workforce shortages. Advanced automation, remote interpretation, and artificial intelligence can address these challenges, reinforcing the digital diagnostics market forecast. Investments in innovative, affordable solutions tailored to developing regions are expected to deliver strong returns, while organizations establishing early partnerships with healthcare providers will secure lasting competitive advantages.

Development of Integrated Diagnostic and Therapeutic Pathways

The combination of diagnostics and treatment planning is a significant area of opportunity across many diseases. There is an ever-growing need for solutions that link diagnostic results to evidence-based treatment plans. Digital diagnostic tools can be used to achieve this aim through clinical analytics, predictive models, and treatment decision support. Such a combination can lead to better care coordination, a quicker start to treatment, and better patient outcomes. Vendors that successfully connect diagnostic intelligence with broader healthcare management workflows are likely to benefit from expanding demand for value-based healthcare solutions.

Recent Developments

- December 2025: Roche Diagnostics announced the U.S. launch of the next-generation cobas 6800/8800 systems and upgraded software, enhancing laboratory throughput, workflow flexibility, sample prioritization, and molecular testing efficiency. The development addresses operational challenges such as staffing shortages and increasing test complexity while improving resource utilization across clinical laboratories.

- November 2025: Siemens Healthineers unveiled its new strategic phase focused on healthcare AI, disease-specific innovation, and enhanced diagnostic capabilities. The company highlighted expanded investments in imaging, precision therapy, and diagnostics while emphasizing artificial intelligence as a key accelerator for future clinical impact and operational efficiency.

- May 2025: Roche received FDA approval for the VENTANA MET (SP44) RxDx Assay, the first companion diagnostic approved to identify eligible non-squamous non-small cell lung cancer patients for a targeted therapy. The approval strengthens precision oncology diagnostics and supports more personalized treatment decisions.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends