Europe Knee Implants Market Analysis and Forecast by Size, Share, Growth, Trends 2031

Europe Knee Implants Market Size and Forecast (2021 - 2031), Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type Of Procedures (Total Knee Replacement, Partial Knee Replacement, and Revision Knee Replacement), Implant Type (Fixed Bearing Prosthesis and Mobile Bearing Prosthesis), Material (Cemented and Non-Cemented), and End User (Hospitals, Orthopedic Clinics, Others, and Ambulatory Surgical Centers)

Historic Data: 2021-2023 | Base Year: 2024 | Forecast Period: 2025-2031- Status : Published

- Report Code : TIPRE00043403

- Category : Life Sciences

- No. of Pages : 198

- Available Report Formats :

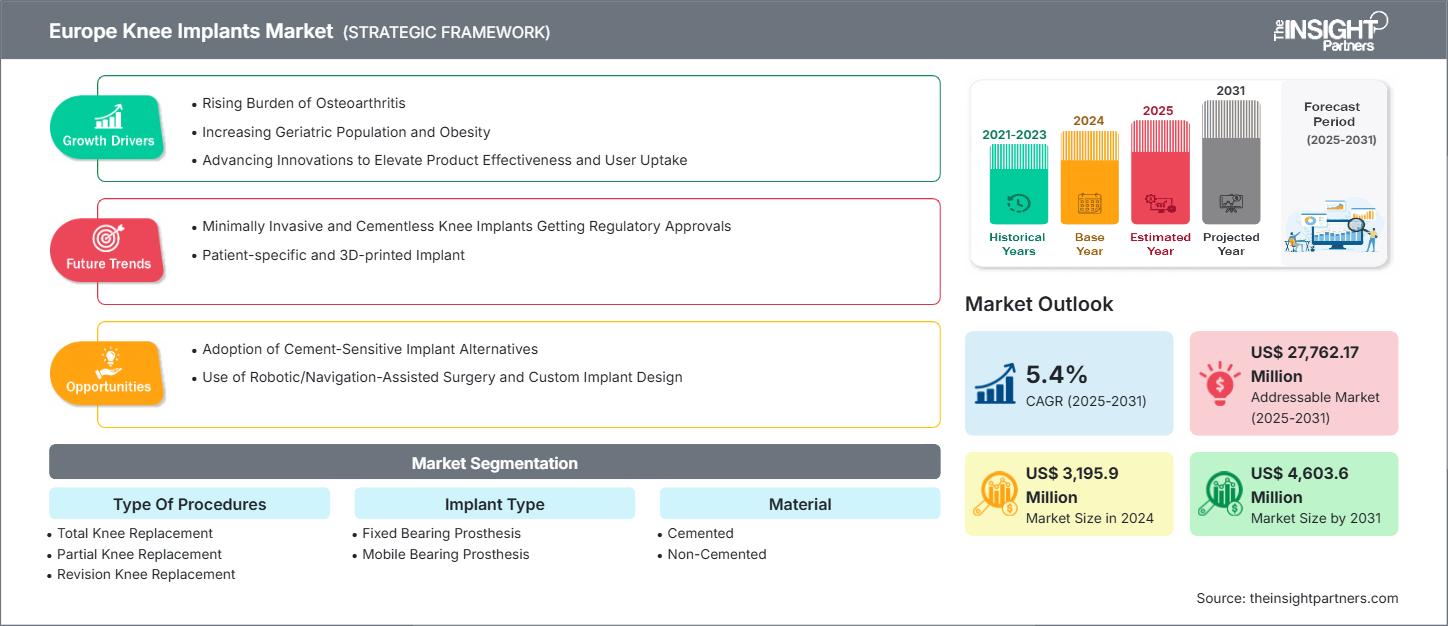

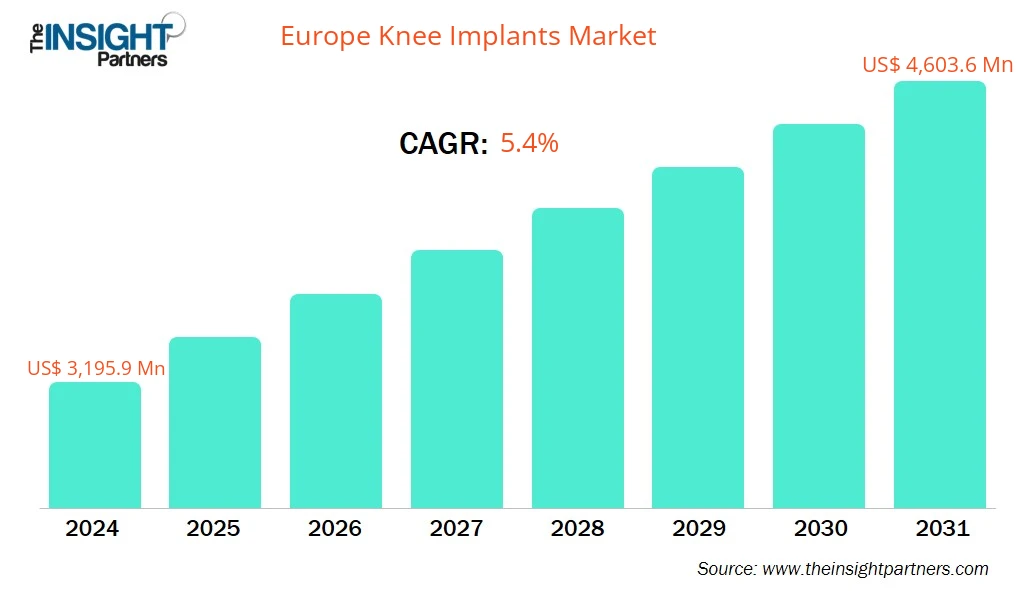

The Europe Knee Implants Market size is expected to reach US$ 4,603.6 Million by 2031 from US$ 3,195.9 Million in 2024. The market is estimated to record a CAGR of 5.4% from 2025 to 2031.

Executive Summary and Europe Knee Implants Market Analysis:

Europe has a rising prevalence of osteoarthritis and aging populations, higher procedure volumes, policy shifts toward outpatient surgery, and technological innovation. According to a report by ReportLinker, in 2023, Germany performed ~194,550 total knee replacement procedures (inpatient), with France (~134,410), the UK (~106,630), Italy (~91,190), Spain (~72,840), and Poland (~37,160) also reporting substantial volumes, reflecting strong procedural demand across key regional markets. Year on year, Poland and Spain saw ~14.5% and ~10.2% increases in inpatient knee replacements, respectively, in 2023. Alongside that, there is a shift toward "day surgery" or outpatient total knee replacements. In 2023, Denmark led with ~23.97 procedures per 100,000 persons, marking ~16.7% YoY increase, while Finland saw ~55.1% rise in this metric.

Osteoarthritis affects tens of millions across Europe. Western Europe had ~57 million people with OA as of 2019, a rise of ~54% over the past 30 years, tied to obesity and aging trends. Although more recent prevalence figures for 2022-2024 are scant in the public registry sources, the increasing procedural data (2023) strongly suggests a continuously rising demand. In terms of product /technological development, Europe has been a key market for platforms like Zimmer Biomet's Oxford cementless partial knee, which has been sold widely in Europe for many years (~60% European market share as cited by the company) before its US approval in late 2024. A high disease burden, increased surgeries (especially outpatient/day surgeries), aging demographics, and the availability and use of newer implant technologies are collectively driving market growth.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONEurope Knee Implants Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Europe Knee Implants Market Segmentation Analysis:

- By Type of Procedures, the Europe Knee Implants Market is segmented into Total Knee Replacement, Partial Knee Replacement, and Revision Knee Replacement. The Total Knee Replacement segment dominated the market in 2024.

- By Implant Type, the Europe Knee Implants Market is segmented into Fixed Bearing Prosthesis and Mobile Bearing Prosthesis. The Fixed Bearing Prosthesis segment dominated the market in 2024.

- By Material, the Europe Knee Implants Market is segmented into Cemented and Non-Cemented. The Cemented segment dominated the market in 2024.

- By End User, the Europe Knee Implants Market is segmented into Hospitals, Orthopedic Clinics, Others, and Ambulatory Surgical Centers. The Hospitals segment dominated the market in 2024.

Europe Knee Implants Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 3,195.9 Million |

| Market Size by 2031 | US$ 4,603.6 Million |

| CAGR (2025 - 2031) | 5.4% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Type Of Procedures

|

| Regions and Countries Covered |

Europe

|

| Market leaders and key company profiles |

|

Europe Knee Implants Market Players Density: Understanding Its Impact on Business Dynamics

The Europe Knee Implants Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Europe Knee Implants Market Outlook

Demographic change and the rising prevalence of obesity together contribute to increased incidence and early onset of knee degeneration. In the UK, the NJR 2024 Report showed that patients undergoing primary knee replacement had a mean age of 69.3 years, with 55% female, and an average BMI of 30.8 in 2023. The female predominance and the high average BMI reflect known risk factors. Older age adds further burden from declining cartilage repair and lower resilience to joint injury. Such a demographic would either require or opt for knee arthroplasty. As high BMI and older age are also associated with increased risk of complications and revisions, manufacturers need to produce implants with better longevity, more forgiving fixation, and designs suited for higher loads. Thus, demographic trends and obesity lead to a higher demand from patients requiring surgery as well as greater technical requirements.

Europe Knee Implants Market Country Insights

By country, the Europe Knee Implants Market is segmented into Germany, France, the United Kingdom, Italy, Spain, and the Rest of Europe. Germany held the largest share in 2024.

The Germany knee implants market is experiencing robust growth driven by its aging population and high prevalence of osteoarthritis, a primary cause of joint deterioration. According to a 2023 study published in Osteoarthritis and Cartilage Open based on data from the InGef health research database, the annual prevalence of knee osteoarthritis in Germany steadily increased, underscoring a consistent and growing patient pool for surgical intervention. A report from the German Federal Statistical Office (Destatis) also indicates a consistent rise in the number of primary knee arthroplasty procedures performed, highlighting the sustained demand for these implants.

Furthermore, the market expansion is bolstered by the rapid adoption of advanced surgical technologies. German hospitals and clinics are increasingly investing in robot-assisted surgical systems, which enhance precision and can lead to better patient outcomes and faster recovery times. For instance, the Helios Klinikum in Munich has adopted robotic arm-assisted surgical systems, such as the Mako, which enables a more bone-sparing and precise procedure. This focus on technological innovation is also evident in new product developments, with German companies such as Merete GmbH and Euromed Implants manufacturing high-quality, innovative prostheses. These factors, combined with a well-established and accessible healthcare system, are collectively driving the strong performance of the German knee implants market.

Europe Knee Implants Market Company Profiles

Some of the key players operating in the market include MicroPort Scientific Corp, Medtronic Plc, Stryker Corp, Zimmer Biomet Holdings Inc, Smith & Nephew Plc, Conmed Corp, Exactech Inc, B. Braun Melsungen AG, Enovis Corp, and Medacta Group SA.

These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

Europe Knee Implants Market Research Methodology

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research

The research process begins with comprehensive secondary research, utilizing internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

- Company websites, annual reports, financial statements, broker analyses, and investor presentations

- Industry trade journals and other relevant publications

- Government documents, statistical databases, and market reports

- News articles, press releases, and webcasts specific to companies operating in the market

Note:

All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.Primary Research

The Insight Partners conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis and gain valuable insights. These research interviews are designed to:

- Validate and refine findings from secondary research

- Enhance the expertise and market understanding of the analysis team

- Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

- Industry stakeholders: Vice Presidents, Business Development Managers, Market Intelligence Managers, and National Sales Managers

- External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Unlock Exclusive Report Discounts

Enquire Now

Get Free Sample For

Get Free Sample For