Gynecological Devices Market Dynamics and Trends by 2031

Coverage: By Product (Surgical Devices, Hand Instruments, and Diagnostic Imaging System); End User (Hospitals, Diagnostic Centers, Clinics, and Others), and Geography

- Status : Data Released

- Report Code : TIPHE100001241

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : February 15, 2025

2023 Market Size

US$ 9.30 Bn

Base year value

2031 Forecast

US$ 17.70 Bn

Projected by 2031

CAGR 2024-2031

7.97 %

Growth rate

Addressable Market

US$ 106.69 Bn

(2024-2031)

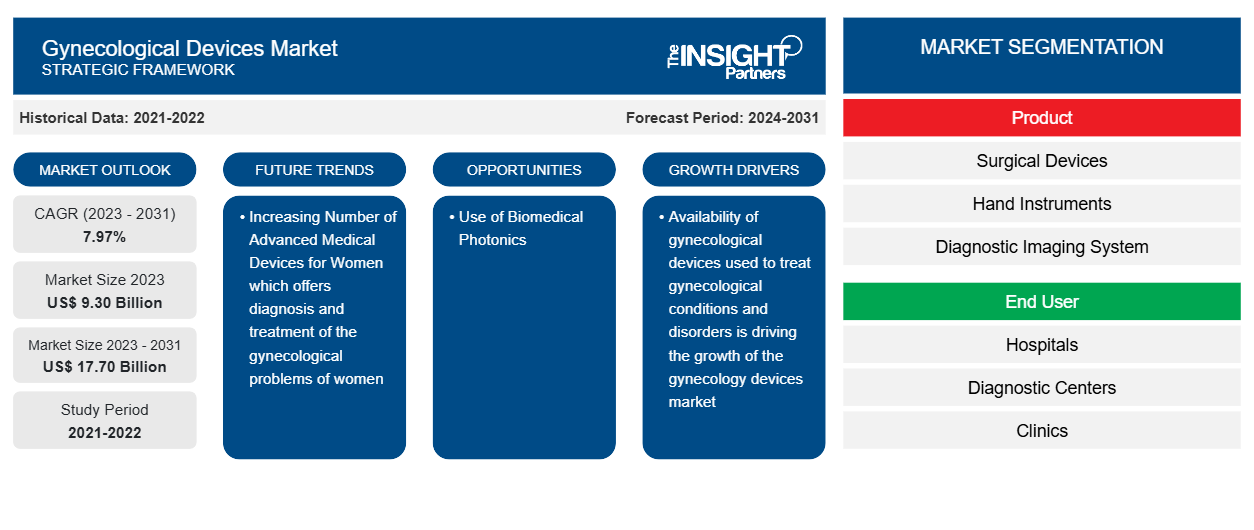

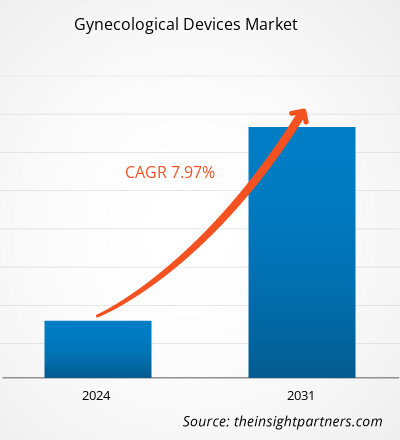

The gynecological devices market size is projected to reach US$ 17.70 billion by 2031 from US$ 9.30 billion in 2023. The market is expected to register a CAGR of 7.97% during 2023–2031. The utilization of artificial intelligence in gynecology is likely to remain a key trend in the market.

Gynecological Devices Market Analysis

Key factors driving the growth of the market are increasing gynecological disorders and growing public awareness. Furthermore, rising awareness of simulation education has created growth opportunities for the gynecological devices market over the upcoming forecast period. Demand for gynecological devices is being driven by a rise in gynecological illnesses, including ovarian cancer, cervical cancer, uterine cancer, vaginal cancer, and vulvar cancer. According to the American Cancer Society's 2022 update, women are often diagnosed with endometrial cancer at the age of 60, however, diagnoses before the age of 45 are uncommon.

Gynecological Devices Market Overview

Gynecological diseases comprise various diseases, including uterine cancer, cervical cancer, polycystic ovary syndrome, and ovarian cancer. A total of 334,382 deaths among individuals 25 years of age and older with gynecologic cancer were recorded between 2010 and 2022, according to data released by the NCBI in 2024. For instance, endometrium cancer is the most common cancer of the female reproductive organs in the US, and uterine cancer is the sixth most common cancer in women in the country. According to the American Cancer Society's projections, there will be around 67,880 new cases of uterine cancer identified in the US in 2024. Roughly 13,250 women will lose their lives to uterine cancer. Further, the availability of gynecological devices used to treat gynecological conditions and disorders is driving the growth of the gynecology devices market.

Market Research Highlights

- Global market for Gynecological Devices was valued at US$ 9.30 Billion in 2023

- Annual market size is expected to reach US$ 17.70 Billion by 2031

- Total addressable market (TAM) during 2024-2031 is projected to reach approximately US$ 106.69 Billion

- Market is anticipated to register a CAGR of 7.97% during the forecast period

- The United States represents a key market, supported by Availability of gynecological devices used to treat gynecological conditions and disorders is driving the growth of the gynecology devices market, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Use of Biomedical Photonics are expected to influence market dynamics and addressable market

- Report profiles industry participants, including CooperSurgical Inc, Hologic, Inc., Medtronic, Stryker, Boston Scientific Corporation, KARL STORZ SE & Co. KG, General Electric Company, Olympus Corporation, Richard Wolf GmbH, Ethicon, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Gynecological Devices Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Gynecological Devices Market Drivers and Opportunities

Increasing Number of Advanced Medical Devices for Women

The healthcare industry is offering various technologically advanced products for the diagnosis and treatment of the gynecological problems of women. The advancement in the healthcare industry, specifically in the medical devices industry, has encouraged players to provide their customers with the best equipment, devices, and systems. Manufacturers of medical devices have devised innovative gynecological devices with better efficacy and reduced the patient’s discomfort by offering quick recovery. Moreover, the evolution of endometrial ablation devices for the treatment of menorrhagia and the usage of endoscopes in gynecological surgeries are a few of the prime developments in the gynecology devices market in the last few years. For instance, Olympus launched the Guardenia Contained Extraction System in September 2022. The newest addition to Advanced Surgical Concepts (ASC) Ltd. of Bray, Ireland's arsenal of confined tissue extraction products for gynecological surgeries, is called Guardenia. The system, designed to confine and isolate tissue during or before surgical removal and extracorporeal manual morcellation, is only distributed in the United States by Olympus America Inc.

Use of Biomedical Photonics

The developments in the medical devices industry have motivated existing players and upcoming players to introduce their novel products to the market. For instance, the use of biomedical photonics for gynecological surgeries has various scopes for the gynecology market players to develop and introduce products for biomedical photonics. Biomedical photonics is specially designed for uterine transplantation and is used for a permanent uterine factor of fertility. The study for this technique was conducted using minimally invasive optical spectroscopy (MSI), which was done on rabbits and sheep. Further, the study proved MSI to be promising for human use in the future. Therefore, the research and development in this field will offer various opportunities for the gynecology device market players in the coming future.

Gynecological Devices Market Report Segmentation Analysis

Key segments that contributed to the derivation of the gynecological devices market analysis are product and end user.

- Based on product, the gynecological devices market is segmented into surgical devices, hand instruments, and diagnostic imaging systems. The adult patient simulator segment held a larger market share in 2023.

- Based on end user, the gynecological devices market is segmented by hospitals, diagnostic centers, clinics, and others. The academic institutes segment held a larger market share in 2023.

Gynecological Devices Market Share Analysis by Geography

The geographic scope of the gynecological devices market report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

In North America, the US is the largest market for gynecological devices. Owing to the rising incidence of cancer linked to gynecology, the prevalence of device makers in the region, and technological developments, the North American market for gynecological devices is the largest in the world. The American Cancer Society estimates that 65,950 new cases of uterine corpus cancer were detected in the US in 2022. Cervical cancer is the most common malignancy among American women and is a significant cause for concern. In the US, 14,100 cases of cervical cancer are predicted by 2022. Moreover, 8,100 Canadian women are anticipated to receive a uterine cancer diagnosis in 2022, according to the Canadian Cancer Society's 2022 update. Therefore, there is a greater need for gynecological gadgets nationwide as a result of the rising prevalence of cancer.

Gynecological Devices Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2023 | US$ 9.30 Billion |

| Market Size by 2031 | US$ 17.70 Billion |

| Global CAGR (2023 - 2031) | 7.97% |

| Historical Data | 2021-2022 |

| Forecast period | 2024-2031 |

| Segments Covered |

By Product

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Gynecological Devices Market Players Density: Understanding Its Impact on Business Dynamics

The Gynecological Devices Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Gynecological Devices Market News and Recent Developments

The Gynecological Devices Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the developments in the gynecological devices market are listed below:

- Innovia Medical Expands Gynecology Range in the U.S. with the Launch of the DTR Medical LLETZlearn Training Simulator. (Source: Innovia Medical, Company Website, August 2023)

- UroViu Corp has launched the new Hystero-V, a single-use hysteroscope compatible with UroViu’s Always Ready endoscopy platform. The 12-Fr, semi-rigid Hystero-V features a hydrophilic coating enabling gentle insertion and superior visualization for highly effective intrauterine examinations. The single-use hysteroscope eliminates the need for reprocessing the equipment, and the ease-of-use, portability, and time-saving aspects of the Hystero-V mean more efficient and comfortable procedures for doctors and patients. (Source: UroViu Corp, Company Website, June 2022)

Gynecological Devices Market Report Coverage and Deliverables

The “Gynecological Devices Market Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering below areas:

- Gynecological devices market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Gynecological devices market trends as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- Gynecological devices market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments.

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the gynecological devices market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends