mHealth Market Size, Share, Growth, Scope & Trend Analysis 2028

mHealth Market Forecast to 2028 - Analysis By Service (Remote Monitoring, Diagnosis, Treatment, Health Support, Fitness & Wellness, and Other Services), Devices (Insulin Pump, BP Monitor, Glucose Monitor, Personal Pulse Oximeter, and Other Devices), and End User (Mobile Operators, Devices Vendors, Health Providers, and Others), and Geography

- Status : Published

- Report Code : TIPHE100000821

- Category : Technology, Media and Telecommunications

- No. of Pages : 157

- Available Report Formats :

- Last update date : June 12, 2024

2021 Market Size

US$ 70.83 Bn

Base year value

2028 Forecast

US$ 410.39 Bn

Projected by 2028

CAGR 2022-2028

28.5 %

Growth rate

Addressable Market

US$ 1,528.20 Bn

(2022-2028)

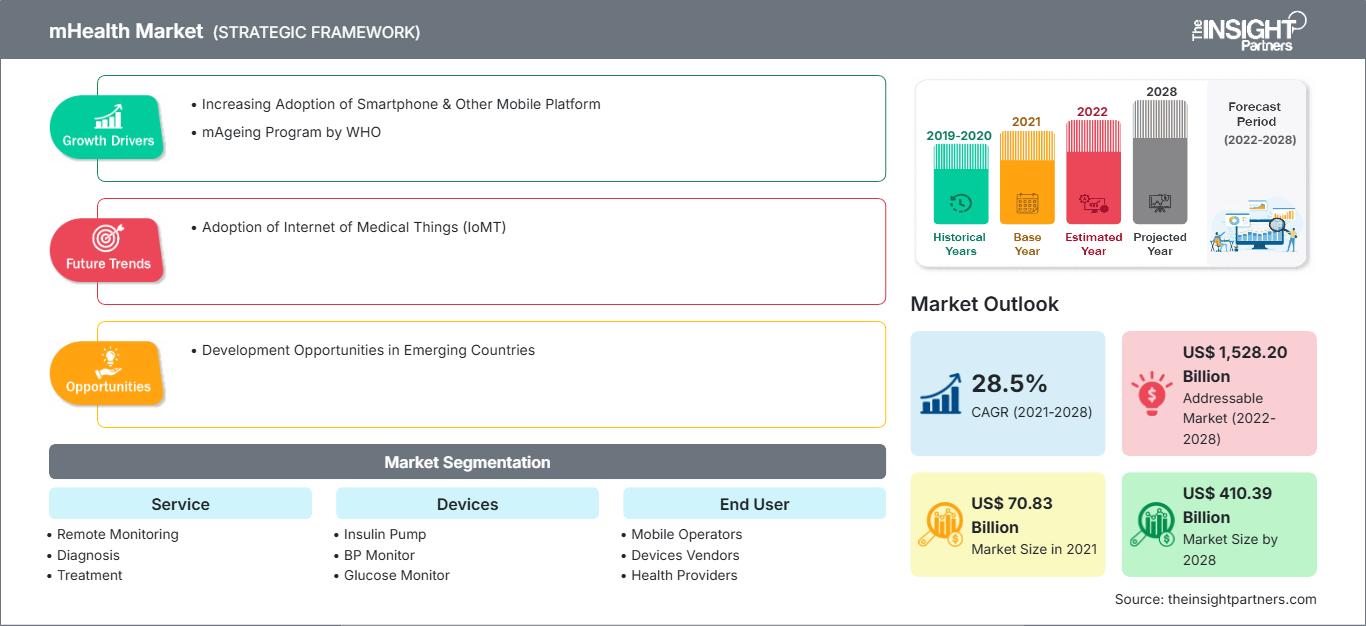

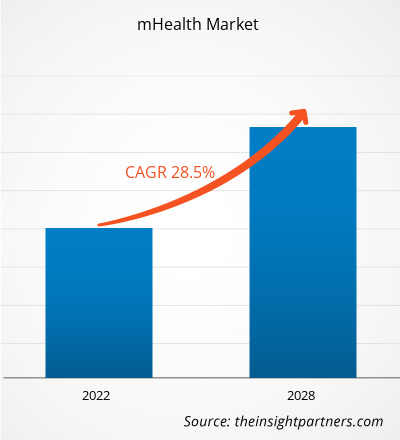

[Research Report] The mHealth market is expected to grow from US$ 70.83 billion in 2021 to US$ 410.39 billion by 2028; it is estimated to grow at a CAGR of 28.5% during 2021-2028.

Analyst Viewpoint:

There is growing demand for health consumers owing to convenience. Wearable devices and other mobile technology allow users to continuously track and manage health data without approaching healthcare providers. Health can also bridge gaps in treatment care by allowing patients to communicate with physicians or healthcare teams through smart technology. Increasing adoption of smartphones & other mobile platforms and the mAgeing program by the World Health Organization (WHO) are the most impacting factors responsible for the mhealth market growth. However, stringent regulations and policies refrain the mhealth market from growing to its full potential. Further, development opportunities in emerging countries provide lucrative opportunities for the mhealth mhealth market to grow to its full potential during the forecast period 2021-2028.

Market Dynamics

Increasing Adoption of Smartphone & Other Mobile Platforms

Smartphones are knowing as significantly auspicious tools that helps to change the health-related behaviors and to manage chronic conditions. The smartphones also contribute to make healthcare practices more easy and manageable by, collecting health data or healthcare information and offer services to the patients. The mhealth technology is a tool that supports treatments, disease surveillance and chronic disease management. Due to the easy access and vast variety of applications, the large number of people can use these mobile health apps. Moreover, mobile health or mhealth apps providing new opportunities such as product launches and new technology to manage chronic conditions and to change health-related behaviors. Currently, the health & wellness app available through the iOS platform has doubled in the past two years. For example, the number of mobile apps has increased to meet the demand and opportunity presented by the smartphone proliferation of the mobile market. Moreover, mhealth apps can be divided into two main categories: those facilitating overall wellness, such as exercise and diet, and others specifically focus on disease management through the implementation of treatment protocols, such as medication reminders. Therefore, consumer mhealth apps targeting wellness comprise two-thirds of the mhealth app space. Rising utility of smartphones ultimately drives the mhealth market growth during the forecast period.

Market Research Highlights

- Global market for mHealth was valued at US$ 70.83 Billion in 2021

- Annual market size is expected to reach US$ 410.39 Billion by 2028

- Total addressable market (TAM) during 2022-2028 is projected to reach approximately US$ 1,528.20 Billion

- Market is anticipated to register a CAGR of 28.5% during the forecast period

- The United States represents a key market, supported by Increasing Adoption of Smartphone & Other Mobile Platform, mAgeing Program by WHO, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Development Opportunities in Emerging Countries are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Allscripts Healthcare LLC, Koninklijke Philips N.V., Medtronic, Boston Scientific Corp., athenaheath Inc., Honeywell Life Care Solutions, Cisco Systems Inc., Omron Corp., Masimo, AgaMatrix Inc., while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

mHealth Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Future Trends

Adoption of Internet of Medical Things (IoMT)

Connected devices are shaping the modern world, opening up space for greater mobility and agility, increasing efficiency and productivity, and allowing to receive and process various types of data for valuable insights. A survey conducted in 2020 by the Pew Research Center states that 21% of Americans (about 70 million people) claim to have embraced wearable tech. Hence, IoT trend eventually has paved its way to healthcare where it is known as IoMT (Internet of Medical Things).

Gradually, mhealth apps and IoMT devices like wearables are going hand in hand, providing meaningful grounds for each other. For instance, Apple watches, when introduced in 2015, were mainly used for fitness tracking, while today, Apple’s “Movement Disorder API” allows monitoring symptoms and gathering new insights into Parkinson’s disease. Nearly all IoMT devices require integration with an mhealth app, and the latter provides the app with useful data that ensures better health management.

Report Segmentation and Scope

The “Global mhealth Market” is segmented based on service, devices, and end user, and geography. Based on service, the mhealth market is segmented into in remote monitoring services, diagnosis services, treatment services, health support services, fitness & wellness services. Based on devices, the mhealth market is segmented into insulin pump, bp monitor, glucose monitor, personal pulse oximeter, and others. By end user, the mhealth market is segmented as mobile operators, device vendors, health providers, and others. The mhealth market based on geography is segmented into North America (US, Canada, and Mexico), Europe (Germany, France, Italy, Spain, and Rest of Europe), Asia Pacific (Australia, China, Japan, India, South Korea, and Rest of Asia Pacific), Middle East & Africa (South Africa, Saudi Arabia, UAE, and Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and Rest of South & Central America)

Segmental Analysis:

Based on service, the mhealth market is segmented into remote monitoring services, diagnosis services, treatment services, health support services, fitness & wellness services. The remote monitoring services segment held a larger share of the mhealth market in 2022 and knockout the others segment accounting least market share. The digital age, with digital sensors, the Internet of Things (IoT), and big data tools, has opened new opportunities for improving the delivery of health care services, with remote monitoring systems playing a crucial role and improving access to patients. The versatility of these systems has been demonstrated during the current COVID-19 pandemic. Health remote monitoring systems (HRMS) present various advantages such as the reduction in patient load at hospitals and health centers. Patients that would most benefit from HRMS are those with chronic diseases, older adults, and patients that experience less severe symptoms recovering from SARS-CoV-2 viral infection.

Based on devices, the mhealth market is segmented as insulin pump, bp monitor, glucose monitor, personal pulse oximeter, and others. The insulin pump segment is anticipated to hold the largest share of the market in 2022. Moreover, the same segment is estimated to register the highest CAGR of 28.8% during the forecast period. Diabetes is a metabolic disorder that refers to the condition created by the body's inability to regulate glucose levels. It has been labelled the 'silent epidemic' for its insidious and chronic nature. The medical profession has postulated that patients could benefit from a system providing continuous glucose readings. Worldwide, the number of people with diabetes is increasing and about 90% of patients have type 2 diabetes mellitus; about one fifth of people with type 2 diabetes are on insulin treatment. The global burden of type 2 diabetes has prompted increasing efforts to develop mobile technologies for self-monitoring of blood glucose among patients with diabetes. A wide variety of home glucometers are available that are portable, inexpensive, reliable and sensitive, and which use smaller amounts of blood than in the past.

Regional Analysis:

Based on geography, the mhealth market is divided into five key regions: North America, Europe, Asia Pacific, South & Central America, and Middle East & Africa. In 2022, North America held the largest share of the mhealth market, and Asia Pacific is estimated to register the highest CAGR during the forecast period. The North America mHealth market has been segmented into the US, Canada, and Mexico. All the three countries in the region are witnessing a sequential change in the mHealth market. North America has largest market share of the mHealth market, by geography.

The increasing aging populations and rising health care costs helps to grow the demand for mHealth services in the region. In particular, the US provides strong examples of technological developments and emerging opportunities in the market. Most of the mHealth apps in the US are regulated by FDA, that perform patient specific analysis and/or patient specific diagnosis or treatment recommendations in an effort to ensure that any application that could cause misinformation leading to a health risks, are moderated. The increasing use of smart phones and the prevalence of mobile technology use both clinical and lifestyle applications, helps to propel the growth the market. Moreover, the use of smart technologies helps to educate and improve the health behaviors in the region.

Asia Pacific (APAC) is the fastest-growing regional market for mHealth; and China, India, Japan, South Korea, Australia, and Rest of APAC are the major contributors to the market in this region. Asia Pacific is likely to account for over 23.26% market share of the global MHealth market in 2021 owing to the growing investments from international players in China and India, improving government support in countries, expanding base of CRO services, and advancing healthcare infrastructure. Therefore, the region holds huge potential for the MHealth market players to grow during the forecast period.

Among Asia Pacific region, China holds largest share for mhealth market. China is country with huge population and have flourished healthcare infrastructure, with rapid growth in communication. The level of social and economic developments differs between coastal area and rural areas. In the coastal areas, health resources are relatively well developed and easily available as compared to rural areas of the west. Patients in rural areas often experience more difficulties due to lack of medical care and drugs. The development of mhealth in China is relatively new.

Healthcare represents a major challenge for many countries as rising health care costs, aging populations, access disparities and chronic illnesses threaten traditional health care systems. China provide strong examples of technological developments and emerging opportunities in mobile health, or mHealth. In order to best leverage these advances, China and the United States must change operations and policy practice in order to facilitate the growth of the mHealth sector and ultimately capture the benefits of mobile technology in healthcare, these scholars assert. In both China and the United States, the cost of medical care is growing rapidly. In China rural residents primarily use mobile phones to access the Internet. According to the survey of China Network Information Center (CNNIC) in June 2013, 78.9 percent of Internet users in China’s rural areas rely on mobile phones. The gap in medical services between urban areas and rural areas is apparent in China as well. China has many people who suffer from cardiovascular issues as well as hypertension and diabetes. According to the Chronic and Non-communicable Disease Prevention and Control Center of Chinese Center for Disease and Prevention, around 33% of adults received diagnoses of hypertension and approximately 9.5% were told they had diabetes. Moreover, according to the China Health Statistics Yearbook, urban areas have more medical personnel and sick beds than rural areas. According to The State Council Information Office of the People’s Republic of China, doctors diagnose 260 million people with chronic illnesses every year. Chronic diseases account for 85 percent of the deaths in China every year. In turn, the number of people afflicted with hypertension and diabetes has increased in recent years placing pressure on the health care system and the government to respond to the crisis.

Industry Developments and Future Opportunities:

Various initiatives taken by key players operating in the global mhealth market are listed below:

- In February 2022, Highmark Health announced launching of “Dubbed Well360 Diabetes Management”, a virtual care program for adults with type 2 diabetes that includes personalized care management, remote patient monitoring, and telehealth.

- In January 2022, MVP Health Care, a non-profit payer with members in New York and Vermont, announced launching of a virtual primary and specialty care solution for Medicaid members.

- In February 2020, DexCom signed a commercialization agreement with Insulet Corporation, a medical device company. Under this agreement, the companies aimed to combine current and future Dexcom continuous glucose monitoring systems (CGM) with Insulet’s trusted tubeless insulin delivery Pod into the Omnipod Horizon System for automated insulin delivery.

- In February 2020, Johnson and Johnson announced it is partnering with Apple for a new mHealth study. The study would determine whether the Apple Watch and an accompanying app can help reduce the risk of stroke in older Americans. The Heartline Study is open to more than 40 million seniors enrolled in Medicare. The aim is to determine whether the ECG sensor and app on the Apple Watch can accurately detect the presence of atrial fibrillation, a key indicator of stroke susceptibility.

- In January 2020, Sanofi signed an agreement with BIOCORP, a French company specialized in the development and manufacturing of medical devices and smart drug delivery systems. The agreement was signed for BIOCORP’s smart sensor Mallya. The smart sensor will record the dosage when a person uses a SoloStar pen to administer insulin. This information would be combined with blood glucose levels recorded by Sanofi’s digital monitoring platform, which currently includes the MyStar DoseCoach blood glucose meter and the My Dose Coach smartphone app.

mHealth Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2021 | US$ 70.83 Billion |

| Market Size by 2028 | US$ 410.39 Billion |

| Global CAGR (2021 - 2028) | 28.5% |

| Historical Data | 2019-2020 |

| Forecast period | 2022-2028 |

| Segments Covered |

By Service

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

mHealth Market Players Density: Understanding Its Impact on Business Dynamics

The mHealth Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Competitive Landscape and Key Companies:

Some of the prominent players operating in the global mhealth market include AT&T, Apple Inc., Samsung Electronics Co. Ltd., Google Inc., Qualcomm Technologies Inc., Cisco Systems Inc., Medtronic PLC, Koninklijke Philips N.V., Allscripts Healthcare Solutions, and Boston Scientific Corp. These companies focus on new product launches and geographical expansions to meet the growing consumer demand worldwide and increase their product range in specialty portfolios. They have a widespread global presence, which provides them to serve a large set of customers and subsequently increases their market share.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends