Middle East & Africa Anti-Obesity Drugs Market Overview, Growth, Trends, Analysis, Research Report (2025-2031)

Middle East & Africa Anti-Obesity Drugs Market Size and Forecast (2021 - 2031), Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Prescription Drugs and OTC Drugs), Mechanism of Action (Centrally Acting Drugs, Peripherally Acting Drugs, and Others), Drug Class (GLP-1 Agonist, Lipase Inhibitors, MC4R agonist, and Others), GLP-1 Agonist [Semaglutide, Liraglutide, and Tirzepatide (Zepbound)], Application (Appetite Suppression, Inhibition of Fat Absorption or Digestive Enzymes, Metabolic Enhancement, and Combination), Route of Administration (Oral and Parenteral), and Distribution Channel (Hospital Pharmacies, Online Channel, and Retail Pharmacies)

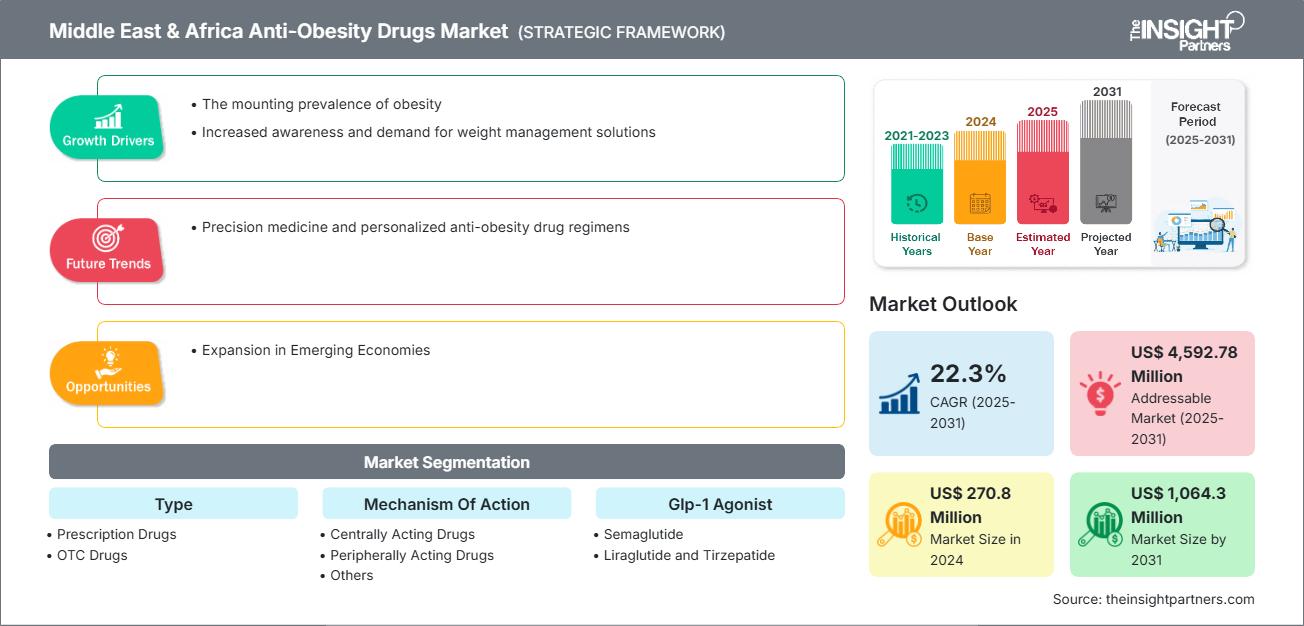

Historic Data: 2021-2023 | Base Year: 2024 | Forecast Period: 2025-2031- Report Code : TIPRE00041496

- Category : Life Sciences

- No. of Pages : 218

- Available Report Formats :

The Middle East & Africa Anti-Obesity Drugs Market size is expected to reach US$ 1,064.3 Million by 2031 from US$ 270.8 Million in 2024. The market is estimated to record a CAGR of 22.3% from 2025 to 2031.

Executive Summary and Middle East & Africa Anti-Obesity Drugs Market Analysis:

The anti-obesity drugs market in the Middle East & Africa is segmented into the UAE, Saudi Arabia, South Africa, and the Rest of Middle East & Africa. Increasing suburbanization and changing lifestyles have led to increased consumption of high-calorie, processed foods and a decline in physical activity, contributing to higher obesity rates. Additionally, growing awareness of obesity-related health risks-such as diabetes, cardiovascular disease, and certain cancers-has increased demand for medical interventions. Governments and health organizations in the region are launching public health campaigns and initiatives to combat obesity, further supporting market expansion. Improved access to healthcare, rising disposable incomes, and increasing investment in healthcare infrastructure also play significant roles. Furthermore, the region has seen a growing presence of pharmaceutical companies offering innovative anti-obesity treatments, including GLP-1 receptor agonists. As cultural perceptions shift and medical tourism gains popularity, especially in countries like the UAE and South Africa, the anti-obesity drug market is poised for continued growth across the Middle East & Africa.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONMiddle East & Africa Anti-Obesity Drugs Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Middle East & Africa Anti-Obesity Drugs Market Segmentation Analysis:

- By Type, the Middle East & Africa Anti-Obesity Drugs Market is segmented into Prescription Drugs and OTC Drugs. Prescription Drugs held the largest share of the market in 2024.

- By Mechanism of Action, the Middle East & Africa Anti-Obesity Drugs Market is segmented into Centrally Acting Drugs, Peripherally Acting Drugs, and Others. Centrally Acting Drugs held the largest share of the market in 2024.

- By Drug Class, the Middle East & Africa Anti-Obesity Drugs Market is segmented into GLP-1 Agonist, Lipase Inhibitors, MC4R agonist, and Others. GLP-1 Agonist held the largest share of the market in 2024.

- By GLP-1 agonist, the Middle East & Africa Anti-Obesity Drugs Market is segmented into Semaglutide, Liraglutide, and Tirzepatide (Zepbound). Semaglutide held the largest share of the market in 2024.

- By Application, the Middle East & Africa Anti-Obesity Drugs Market is segmented into Appetite Suppression, Inhibition of Fat Absorption or Digestive Enzymes, Metabolic Enhancement, and Combination. Appetite Suppression held the largest share of the market in 2024.

- By Route of Administration, the Middle East & Africa Anti-Obesity Drugs Market is segmented into Oral and Parenteral. Oral held the largest share of the market in 2024.

- By Distribution Channel, the Middle East & Africa Anti-Obesity Drugs Market is segmented into Hospital Pharmacies, Online Channel, and Retail Pharmacies. Hospital Pharmacies held the largest share of the market in 2024.

Middle East & Africa Anti-Obesity Drugs Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 270.8 Million |

| Market Size by 2031 | US$ 1,064.3 Million |

| CAGR (2025 - 2031) | 22.3% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

Middle East and Africa

|

| Market leaders and key company profiles |

|

Middle East & Africa Anti-Obesity Drugs Market Players Density: Understanding Its Impact on Business Dynamics

The Middle East & Africa Anti-Obesity Drugs Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Middle East & Africa Anti-Obesity Drugs Market Outlook

Genetic, environmental, and lifestyle factors influence obesity. Recent advances have shown that individuals respond differently to anti-obesity medications due to variations in their genetic makeup, metabolic rate, gut microbiota, and existing comorbidities. As a result, a drug that is effective for one patient may yield limited results or cause intolerable side effects for another. In obesity treatment, precision medicine utilizes pharmacogenomic testing and comprehensive patient profiling to select the most suitable drug or combination of drugs. Companies are developing diagnostic tools that analyze genetic markers related to obesity and drug metabolism. These tools assist clinicians in predicting which patients are likely to benefit from GLP-1 receptor agonists, centrally acting agents, or emerging therapies that employ novel mechanisms of action. The expanding pipeline of anti-obesity drugs -some targeting different pathways and mechanisms-enables clinicians to align therapies with individual patient profiles. Suppose a patient does not respond adequately to a GLP-1 agonist. In that case, a physician may opt to switch to or combine it with another agent that targets a different pathway, such as a dual or triple agonist. This approach mirrors the individualized treatment strategies already established in diabetes and oncology.

Pharmacogenomic companies such as Acosta and Phenomix provide tests that support personalized obesity treatment, and this trend is expected to accelerate as more data become available and additional drugs enter the market. Ultimately, this shift toward individualized regimens will make anti-obesity pharmacotherapy more effective, cost-efficient, and widely accepted by patients and healthcare providers. In the United Arab Emirates (UAE), in March 2025, VIVUS LLC launched QSYMIA® (phentermine and topiramate extended-release capsules). This marked the first approval of this obesity treatment in the Middle East. This approval allows healthcare providers to offer QSYMIA to adults and children aged 12 and older. It directly addresses the rising obesity rates in the region. By 2035, the UAE is expected to have over 7.5 million people living with obesity, which highlights a growing public health challenge. VIVUS, together with PharmaAccess and distributor Alphamed Drug Store, aims to give healthcare providers more treatment options to fight this issue, supporting the UAE's plan to tackle obesity. This move reflects the ongoing trend of personalized medicine and tailored anti-obesity regimens in the Middle East. In conclusion, precision medicine is transforming the anti-obesity drugs market by allowing clinicians to tailor therapies based on genetic and metabolic profiles. This trend promises improved efficacy, fewer side effects, and better long-term outcomes, positioning personalized regimens as a cornerstone of future obesity management.

Middle East & Africa Anti-Obesity Drugs Market Country Insights

By country, the Middle East & Africa Anti-Obesity Drugs Market is segmented into Saudi Arabia, South Africa, the United Arab Emirates, and the Rest of Middle East & Africa. Saudi Arabia held the largest share in 2024.

The rate of increase of overweight and obese populations in Saudi Arabia has been particularly concerning, with figures nearly doubling over the last five decades. Like in many other Gulf Cooperation Council (GCC) countries, rapid economic growth and urbanization have led to significant lifestyle shifts, marked by reduced physical activity and greater intake of highly processed foods and beverages. Per the article -Overweight and obesity-A growing challenge in Saudi Arabia, published in December 2022, over half of the Saudi population was classified as overweight, and more than 20% had obesity. The economic burden of obesity treatment and management in the country is estimated at US$ 6.4 billion, highlighting the urgent need for effective medical interventions.

In response to the health and social implications of obesity, the country's government has implemented an extensive range of policies under its Vision 2030 plan, focusing on creating a healthier population and improve quality of life.

Additionally, companies' efforts to make anti-obesity drugs available in the nation help enhance their market presence. In April 2025, Novo Nordisk, a leading global healthcare company, signed a Memorandum of Understanding (MoU) with Lifera, a biopharmaceutical firm owned by Saudi sovereign wealth fund PIF-to localize the manufacturing of semaglutide-based GLP-1 treatments within the Kingdom. This MoU represents a major step forward in enhancing Saudi Arabia's healthcare infrastructure and pharmaceutical production capabilities. Semaglutide GLP-1 treatments are the world's leading therapeutics for weight management. As part of the agreement, Novo Nordisk aims to launch Wegovy in Saudi Arabia in 2025, making it available to patients with obesity across both public and private healthcare sectors. The increasing adoption of GLP-1 receptor agonists and supportive government initiatives underscore the country's commitment to addressing obesity and its associated health risks. In conclusion, Saudi Arabia's anti-obesity drugs market is rapidly expanding, driven by the above factors.

Middle East & Africa Anti-Obesity Drugs Market Company Profiles

Some of the key players operating in the market include GSK Plc, F. Hoffmann-La Roche Ltd, Teva Pharmaceutical Industries Ltd, Novo Nordisk AS, Eli Lilly and Co, Sun Pharmaceutical Industries Ltd, VIVUS LLC, Currax Pharmaceuticals LLC., AdvaCare Pharma USA LLC, and Rhythm Pharmaceuticals Inc.

These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

Middle East & Africa Anti-Obesity Drugs Market Research Methodology

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research

The research process begins with comprehensive secondary research, utilizing internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

- Company websites, annual reports, financial statements, broker analyses, and investor presentations

- Industry trade journals and other relevant publications

- Government documents, statistical databases, and market reports

- News articles, press releases, and webcasts specific to companies operating in the market

Note:

All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.Primary Research

The Insight Partners conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis and gain valuable insights. These research interviews are designed to:

- Validate and refine findings from secondary research

- Enhance the expertise and market understanding of the analysis team

- Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

- Industry stakeholders: Vice Presidents, Business Development Managers, Market Intelligence Managers, and National Sales Managers

- External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Get Free Sample For

Get Free Sample For