Robotic Assisted Surgery Systems Market Size, Growth & Demand by 2034

Coverage: By Product Type (Systems, Consumables and Accessories, and Software and Services), Application (Gynecological Surgery, Cardiovascular Procedure, Neurosurgery, Orthopedic Surgery, Laparoscopy, Urology, and Other Applications), End User (Hospitals, Ambulatory Surgery Centers, and Other End Users), and Geography (North America, Europe, Asia Pacific, South & Central America, and Middle East & Africa)

- Status : Data Released

- Report Code : TIPRE00004753

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : April 01, 2026

2025 Market Size

US$ 2.09 Bn

Base year value

2034 Forecast

US$ 5.87 Bn

Projected by 2034

CAGR 2026-2034

12.16 %

Growth rate

Addressable Market

US$ 34.87 Bn

(2026-2034)

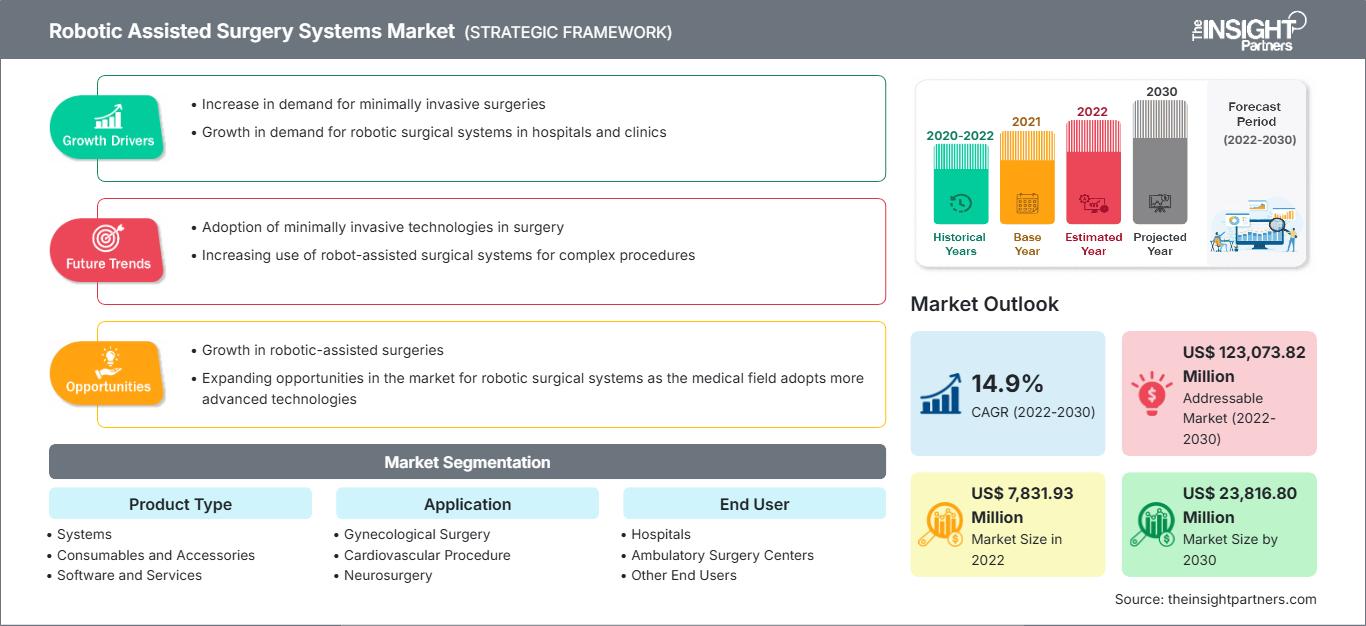

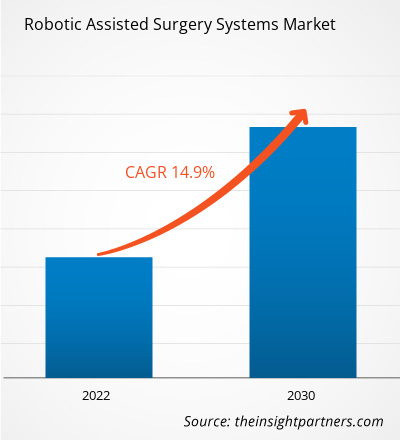

The global Robot-Assisted Surgery Systems Market size is projected to reach US$ 5.87 billion by 2034 from US$ 2.09 billion in 2025. The market is anticipated to register a CAGR of 12.16% during the forecast period 2026–2034.

Key market dynamics include an accelerating global demand for minimally invasive procedures, significant advancements in high-definition 3D visualization, and the integration of artificial intelligence for real-time intraoperative guidance. Additionally, the market is expected to benefit from an aging global population prone to chronic conditions, increasing hospital investments in digital surgery ecosystems, and the expansion of robotic applications into specialized fields such as neurosurgery and orthopedic joint replacement.

Robot Assisted Surgical Systems Market Analysis

The robot-assisted surgical systems market analysis shows a trend toward modular and portable platforms as healthcare providers seek to lower the high entry costs traditionally associated with fixed-tower systems. The market is moving into high-volume centers utilizing multi-port flagship platforms and high-growth segments adopting specialized robots for specific anatomical regions like the spine and knee. Strategic opportunities are emerging in the development of telesurgery and remote proctoring, where low-latency connectivity allows expert surgeons to assist in procedures across different geographic locations. The analysis also notes that market expansion depends on recurring revenue models, with sales of proprietary consumables and instruments often outpacing the growth of one-time system installations. Competitive differentiation now stands out depending on digital ecosystems that offer post-operative data analytics and cloud-based video storage for surgeon training and performance benchmarking.

Robot Assisted Surgical Systems Market Overview

Robot-assisted surgical systems have advanced from niche experimental tools to mainstream medical standards. The robot-assisted surgical systems include multi-port systems, single-port platforms for ultra-minimally invasive access, and handheld robotic assistance for orthopedics. Both established MedTech giants and agile startups compete in this market, using technologies such as haptic feedback, machine learning, and augmented reality. Growing demand for convenient outpatient options among health-conscious patients in North America and Europe has increased the popularity of robotic systems as a solution for faster recovery and reduced hospital stays. North America leads in revenue due to its established surgical infrastructure and favorable reimbursement, while Asia-Pacific is advancing in system innovation and hospital adoption. The US market is the most developed, driven by health-focused demographics and the broad availability of specialized robotic training programs. Competition among brands is fueling greater system variety and the inclusion of advanced features like AI-guided navigation and smart sensors.

Market Research Highlights

- Global market for Robotic Assisted Surgery Systems was valued at US$ 2.09 Billion in 2025

- Annual market size is expected to reach US$ 5.87 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 34.87 Billion

- Market is anticipated to register a CAGR of 12.16% during the forecast period

- The United States represents a key market, supported by Increase in demand for minimally invasive surgeries, Growth in demand for robotic surgical systems in hospitals and clinics, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Growth in robotic-assisted surgeries, Expanding opportunities in the market for robotic surgical systems as the medical field adopts more advanced technologies are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Intuitive Surgical Inc., Stryker Corporation, Johnson & Johnson Inc., SRI International Inc., Accuray Incorporated, Renishaw PLC, Medtronic PLC, Brainlab, Smith & Nephew PLC, Globus Medical, Zimmer Biomet, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Robotic Assisted Surgery Systems Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Robot Assisted Surgical Systems Market Drivers and Opportunities

Market Drivers:

- Superior Precision and Minimal Invasiveness: Robotic systems provide surgeons with enhanced dexterity and smaller fat-to-incision ratios, which makes recovery easier for patients with complex surgical needs. This clinical benefit, along with growing interest in reduced hospital stays, is driving its popularity.

- Premiumization of Surgical Suites: The expansion of specialized surgical departments and high-end operating rooms has sustained high demand for robotic inputs. As hospitals trade up to digital surgical experiences, advanced robotic platforms continue to see stable volume gains.

- Rapid Expansion of Digital and E-commerce Channels: Online platforms and B2B digital procurement have removed traditional geographic barriers for niche medical technology. This is particularly evident in the rapid adoption of specialized software and shelf-stable surgical consumables in regions like Asia-Pacific and North America.

Market Opportunities:

- Expansion into Orthopedics and Neurosurgery: Beyond general surgery, robotic platforms offer significant opportunities in high-precision joint replacements and delicate cranial procedures for athletes and the elderly.

- Growth in Emerging APAC Corridors: Forming strategic partnerships between Western-based suppliers and Asian distributors may facilitate access to high-margin market segments in China and India, where demand for premium, high-tech healthcare is increasing.

- Diversification into Specialty Certifications: There is a growing opportunity for manufacturers to target specific medical needs through certifications such as FDA 510(k) clearances and CE Marks for new indications, as seen in recent successful retail expansions in the North American market.

Robot Assisted Surgical Systems Market Report Segmentation Analysis

The robot-assisted surgical systems market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Product Type:

- Systems: A massive segment that aligns with global hospital infrastructure trends. It is increasingly preferred by high-volume medical centers that prioritize clinical excellence and cutting-edge technology.

- Consumables and Accessories: The dominant volume driver, particularly within the surgical and orthopedic, due to established supply chains and the need for regular replacement of proprietary tools.

- Software and Services: The fastest-rising channel, especially for cloud-based data analytics and D2C training modules, enabling long-term operational efficiency.

By Application:

- Gynecological Surgery: Remains a primary channel for robotic adoption, benefiting from the expansion of minimally invasive hysterectomy and myomectomy procedures.

- Urology: One of the most mature segments, particularly for prostatectomy, where robotic assistance offers a clear competitive advantage in patient outcomes.

- Laparoscopy: A fast-growing category that includes various general surgery procedures such as hernia repair and colorectal surgery.

- Orthopedic Surgery: Offers a growing range of robotic-arm-assisted bone preparation and joint replacement solutions in urban markets.

- Cardiovascular Procedure: A specialized but high-value segment focusing on cardiac valve repairs and coronary artery bypass.

- Neurosurgery: Focused on stereotactic navigation and high-precision cranial interventions.

- Other Applications: Includes emerging fields like dental robotics and pediatric surgery.

By End User:

- Hospitals: Remain the primary end user for large-scale systems, benefiting from the ability to handle high patient volumes and complex cases.

- Ambulatory Surgery Centers: The fastest-growing end user, benefiting from the shift toward outpatient procedures and the demand for compact, cost-efficient robotic units.

- Other End Users: Includes academic research institutes and specialty surgical clinics.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Robotic Assisted Surgery Systems Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 2.09 Billion |

| Market Size by 2034 | US$ 5.87 Billion |

| Global CAGR (2026 - 2034) | 12.16% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Product Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Robotic Assisted Surgery Systems Market Players Density: Understanding Its Impact on Business Dynamics

The Robotic Assisted Surgery Systems Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Robot Assisted Surgical Systems Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for premium surgical system manufacturers and specialized MedTech providers to expand.

The robot-assisted surgical systems market is undergoing a significant transformation, moving from a niche, high-cost luxury to a global standard in precision healthcare. Growth is driven by the rising prevalence of chronic diseases, a surge in demand for minimally invasive alternatives, and the expansion of ambulatory surgical care. Below is a summary of market share and trends by region:

North America

- Market Share: Holds the largest share globally, anchored by a highly advanced healthcare infrastructure and favorable reimbursement policies.

- Key Drivers:

- Rising consumer preference for high-precision, AI-integrated surgical profiles found in modern robotic platforms

- Mainstreaming of specialty robotic surgery in high-end hospital chains and academic medical centers

- Increased adoption of single-port (SP) systems for urological and gynecological procedures to minimize patient trauma

- Trends: Scaling of robotic programs in Ambulatory Surgery Centers (ASCs) and the successful adoption of advanced imaging certifications to appeal to safety-focused demographics.

Europe

- Market Share: Represents a substantial segment, driven by deep-seated surgical ecosystems in Germany, France, and the UK.

- Key Drivers:

- High domestic demand for complex surgeries such as robotic-assisted radical prostatectomy and mitral valve repair

- Established processing infrastructure and strict regulatory frameworks for medical device safety

- Robust government support for healthcare digitalization and the implementation of national cancer plans

- Trends: A strategic shift toward prioritizing cost-effective modular robots and a focus on open-platform systems to meet the demands of eco-conscious and budget-constrained European health systems.

Asia-Pacific

- Market Share: The fastest-growing region, with Japan and China acting as the primary drivers for the entire continent, particularly for domestic system innovation.

- Key Drivers:

- Massive patient base seeking premium, high-tech surgical options for cancer and orthopedic care

- Government-supported medical initiatives focused on high-value smart manufacturing

- Rapid urbanization and rising disposable incomes are leading to a preference for westernized luxury medical treatments

- Trends: Heavy reliance on tele-mentoring platforms and B2B contracts for high-end robotic components used in the burgeoning domestic MedTech industries of China and India.

South and Central America

- Market Share: Emerging market with a growing robotics industry in countries like Brazil and Chile.

- Key Drivers:

- Increasing awareness of the clinical superiority of robotic assistance for reduced blood loss and shorter hospital stays

- Modernization of private hospital networks into commercial-grade surgical hubs to attract medical tourism

- Rising interest in minimally invasive protocols among middle-to-high income segments

- Trends: Growth of boutique surgical centers and the introduction of robotic-assisted spine and joint replacement programs to differentiate from the traditional manual market.

Middle East and Africa

- Market Share: Developing market with deep clinical roots in tertiary care, transitioning toward formalized commercial robotic production.

- Key Drivers:

- Strategic investments in Smart Healthcare infrastructure to improve regional health security and reduce reliance on overseas treatment

- High demand for precision-guided surgery in arid or remote climates where specialist access is limited

- Government initiatives to establish Centers of Excellence for robotic training

- Trends: Implementation of modern 5G-enabled telesurgery and refrigeration technologies for sterile instrument transport, coupled with a focus on high-nutrient data analytics for the pediatric segment.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Intuitive Surgical, Inc., Medtronic plc, and Stryker Corporation. Regional experts and niche players like CMR Surgical and Zimmer Biomet, alongside innovators like Asensus Surgical, Inc. and Smith & Nephew, also contribute to a diverse and rapidly expanding market landscape. This competitive environment pushes vendors to differentiate through:

- Premiumization and functional branding position robotic systems as a superior clinical alternative to traditional surgery by emphasizing higher precision and better patient outcomes for health-conscious consumers.

- System diversification now includes more than just large towers. Companies offer portable carts, handheld units, and cloud-integrated software packages.

- Supply chain control ensures quality, transparency, and meets ethical clean-label standards from the manufacturing of robotic arms to local hospital processing.

- New processing technologies, like AI-driven boundary detection and membrane-thin visualization, help create high-quality surgical environments worldwide.

Opportunities and Strategic Moves

- Partner with high-end hospital channels and e-commerce platforms to tap into the surging demand for outpatient-friendly and artisanal-level surgical precision in Asia-Pacific and North American markets.

- Incorporate sustainable manufacturing practices and energy-efficient certifications to appeal to environmentally conscious millennials and Gen Z surgeons seeking ethical medical alternatives.

Major Companies operating in the Robot Assisted Surgical Systems Market are:

- Intuitive Surgical Inc.

- Stryker Corporation

- Johnson & Johnson Inc.

- SRI International Inc.

- Accuray Incorporated

- Renishaw PLC

- Medtronic PLC

- Brainlab

- Smith & Nephew PLC

- Globus Medical

- Zimmer Biomet

Disclaimer: The companies listed above are not ranked in any particular order.

Robot Assisted Surgical Systems Market News and Recent Developments

- In February 2026, Stryker announced the limited market release of Mako RPS (Robotic Power System) for Total Knee, an intuitive handheld robotic system that combines Stryker’s proven robotics and power tool legacies and represents Mako’s expansion into a new robotics platform. Mako now includes Mako SmartRobotics™ – Stryker’s multi-specialty, robotic-arm assisted platform featuring Mako 4 – and Mako Handheld Robotics with Mako RPS, which is designed to reach a new market segment.

- In January 2026, Johnson & Johnson announced that the company had submitted the OTTAVA™ Robotic Surgical System to the U.S. Food and Drug Administration (FDA) in an application for De Novo classification. Leveraging data from the Investigational Device Exemption (IDE) study, the company has applied for marketing authorization in multiple procedures in general surgery within the upper abdomen.

Robot Assisted Surgical Systems Market Report Coverage and Deliverables

The Robot-Assisted Surgical Systems Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Robot-Assisted Surgical Systems Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Robot-Assisted Surgical Systems Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Robot-Assisted Surgical Systems Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Robot-Assisted Surgical Systems Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends