Seam Welding Machine Market Key Players and Forecast by 2031

Coverage: By Mode (Intermittent Seam Welding and Continuous Seam Welding), Operation (Manual, Semi-Automatic, and Automatic), and Industry (Construction, Automotive, Oil and Gas, Manufacturing, and Others) and Geography

- Status : Data Released

- Report Code : TIPRE00018751

- Category : Manufacturing and Construction

- No. of Pages : 150

- Available Report Formats :

- Last update date : February 15, 2025

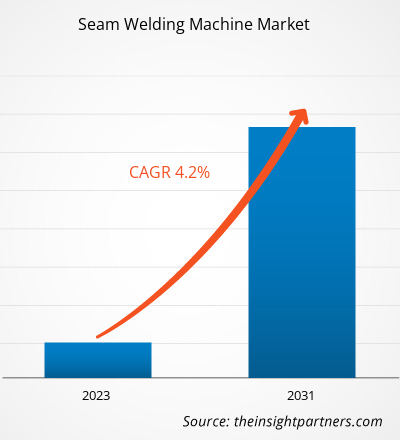

2023 Market Size

US$ 1,187.75 Mn

Base year value

2031 Forecast

US$ 1,649.31 Mn

Projected by 2031

CAGR 2023-2031

4.2 %

Growth rate

Addressable Market

US$ 11,485.44 Mn

(2023-2031)

Seam welding machine market size is projected to reach US$ 1,649.31 million by 2031 from US$ 1,187.75 million in 2023. The market is expected to register a CAGR of 4.2% in 2023–2031. Seam welding machines consist of one or two motor-driven wheels that create a series of over-lapping spot welds on the steel sheet components for achieving air and liquid-proof sealing on the welded components. The seamless current passes through these roller sheets, and the welded components are pressed in between them. Growing demand for seam welding machines across different industries, including automotive, industrial fabrications, construction energy, and power, among others, drives the market growth during the forecast period.

Seam Welding Machine Market Analysis

The seam welding machines market is dominated by Asia Pacific countries such as India, China, South Korea, Japan, and many others. This is owing to increasing demand from the automotive manufacturing facilities across the Asia Pacific countries drives the market growth. India's auto components manufacturing imports reached US$ 20.3 billion in 2023, with a significant share of 30% from China. Indian government is boosting the domestic manufacturing of electric vehicles is driving the seam welding machine market growth.

Market Research Highlights

- Global market for Seam Welding Machine was valued at US$ 1,187.75 Million in 2023

- Annual market size is expected to reach US$ 1,649.31 Million by 2031

- Total addressable market (TAM) during 2023-2031 is projected to reach approximately US$ 11,485.44 Million

- Market is anticipated to register a CAGR of 4.2% during the forecast period

- The United States represents a key market, supported by Growing Demand for Seam Welding Machines in the Automotive Sector is Boosting the Seam Welding Machine Market, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Rising Energy and Power Sector Across the Globe are Expected to Create Ample Opportunities for Market Growth are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Emerson Electric Co., Dahching Electric Industrial, FranzanKoike Aronson, Inc., Leister Technologies, CruxweldMiller, Weldmaster, Schnelldorfer Maschinenbau, Spiro International, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Seam Welding Machine Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Seam Welding Machine Market Overview

Seam Welding Machine Market Drivers and Opportunities

Growing Demand for Seam Welding Machines in the Automotive Sector is Boosting the Seam Welding Machine Market

Automotive production increased by 11.5% in 2022 compared to 2023, amounting to about 92 million units globally. The increase in production primarily drives the demand for advanced machines such as robotic welding seamless welding machines for automotive panels manufacturing by the leading automotive OEMs. Such rapid growth of automotive vehicle production across the advanced economies globally has driven the seam welding machine market growth in the automotive sector. Further, rising electric vehicle production with the emergence of hybrid electric vehicles is gaining popularity in the seam welding machine market.

Rising Energy and Power Sector Across the Globe are Expected to Create Ample Opportunities for Market Growth

Increasing demand for the fabrication of solar panel stands, and industrial boilers in the energy and power sector is expected to create ample opportunity for the seam welding machine market growth during the forecast period. For instance, in January 2024, Mortenson and Terra-Gen launched the largest solar panel and energy storage project named Edwards & Sanborn Solar in the US. Mortenson is the procurement, engineering, and construction service contractor for this project in the US. Increasing such projects across the globe is expected to create ample opportunity for the global seam welding machine market growth during the forecast period.

Seam Welding Machine Market Report Segmentation Analysis

Key segments that contributed to the derivation of the seam welding machine market analysis are mode, operation, and industry.

- Based on mode, the market is segmented into intermittent seam welding and continuous seam welding. Among these, continuous seam welding has the largest share owing to the increasing demand across automotive production across the globe.

- Based on operation, the seam welding machine market is categorized into manual, semi-automatic, and automatic.

- Based on industry, the market is segmented into construction, automotive, oil and gas, manufacturing, and others. Among these, the automotive industry has the largest share in 2023, this is owing to increasing automotive production across the globe.

Seam Welding Machine Market Share Analysis by Geography

The geographic scope of the Seam Welding Machine market report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South America/South & Central America.

Based on geography, the seam welding machine market is primarily segmented into North America, Europe, Asia Pacific (APAC), the Middle East & Africa (MEA), and South America (SAM). Asia Pacific is expected to account for the largest market share in 2023, and it is likely to retain its dominance during the forecast period. Further, the seam welding machine market in this region is expected to witness the highest CAGR during the forecast period. This is owing to increasing automotive production in the Asia Pacific countries such as China, Japan and India. For instance, in 2023, the Indian automotive manufacturers planned to invest more than US$ 7 billion by 2028 to strengthen its local automotive components production, such as electric motors, car panels, chassis and many others. Also, in March 2024, Autoneum planned to expand its production in Asia Pacific countries such as China and India. The company planned to open two new plants in Pune across Western India and in Changchun in Jilin, China. Increasing such investment in the automotive sector across the Asia Pacific countries has created massive demand for the seam welding machine market growth.

Europe is expected to hold the second-largest share of the seam welding machine market in 2023. In contrast, Germany is expected to be the dominant contributor to the regional seam welding machine market. Europe is home to top automakers, including Mercedes, Volkswagen, Skoda, BMW, and Audi. According to the Policy Department for Economic, Scientific, and Quality of Life Policies, the COVID-19 pandemic indirectly impacted over 1.1 million jobs due to the shutdown of automotive factories from March to May 2020.

Moreover, vehicle sales plummeted across Europe in 2020, while original equipment manufacturers (OEMs) announced further delays in the reopening of their assembly plants. In addition to a drop in demand for passenger cars and LCVs, disruptions in raw material supply chains due to limitations on cross-border movements led to delays in the supply of equipment, such as welding machines. However, the COVID-19 pandemic and its repercussions encouraged manufacturing companies to digitize and automate their operations, which allowed them to revive their operations in late 2020. Such revival efforts by manufacturing companies are creating future growth opportunities for seam welding machine providers in Europe.

Seam Welding Machine Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2023 | US$ 1,187.75 million |

| Market Size by 2031 | US$ 1,649.31 million |

| Global CAGR (2023 - 2031) | 4.2% |

| Historical Data | 2021-2022 |

| Forecast period | 2023-2031 |

| Segments Covered |

By Mode

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Seam Welding Machine Market Players Density: Understanding Its Impact on Business Dynamics

The Seam Welding Machine Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Seam Welding Machine Market News and Recent Developments

The Seam Welding Machine market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. The following is a list of developments in the market for innovations, business expansion, and strategies:

- In 2022, Stealth, a global manufacturing expert in performance gear, launched a first-to-market, patented seam welding technology that removes the need for stitching. The technology results in warmer, tougher, and entirely durable seams for longer-lasting products that protect adventurers from the harshest elements. (Source: Eurofins, Press Release)

- In 2022, Miller Electric launched a single-wire automated Hercules high-deposition MIG welding system. The Hercules welding system enhances the welding capacity without additional cost requirements related to the welding cells. This is a seamless welding machine with high deposition rates and enhances productivity by up to 30%. (Source: SGS, Newsletter)

Seam Welding Machine Market Report Coverage and Deliverables

The “Seam Welding Machine Market Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering the following areas:

- Seam Welding Machine Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Market dynamics such as drivers, restraints, and key opportunities

- Seam Welding Machine Market Trends

- Detailed PEST Analysis and SWOT analysis

- Seam Welding Machine Market Analysis covering key market trends, Global and regional framework, major players, regulations, and recent market developments.

- Seam Welding MachineMarket Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments.

- Detailed Company Profiles

- Emerson Electric Co.

- Dahching Electric Industrial

- Franzan

- Koike Aronson, Inc.

- Leister Technologies

- Cruxweld

- Miller Weldmaster

- Schnelldorfer Maschinenbau

- Spiro International

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends