US Electronic Health Record (EHR) Market Growth Drivers and Forecast by 2030

Historic Data: 2020-2021 | Base Year: 2022 | Forecast Period: 2023-2030US Electronic Health Record (EHR) Market Size and Forecasts (2020 - 2030), Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Installation Type (Cloud-Based and On-Premise), Type (Acute Electronic Health Record Market, Ambulatory Electronic Health Record Market, and Post-Acute Electronic Health Record Market), Application (Clinical Records, Administrative Task and Billing, Physician Support, and Patient Portal), and End User (Hospitals and Clinics, Ambulatory Surgical Centers, and Physicians Office/Specialty Care Centers))

- Report Date : Nov 2023

- Report Code : TIPRE00031430

- Category : Technology, Media and Telecommunications

- Status : Published

- Available Report Formats :

- No. of Pages : 114

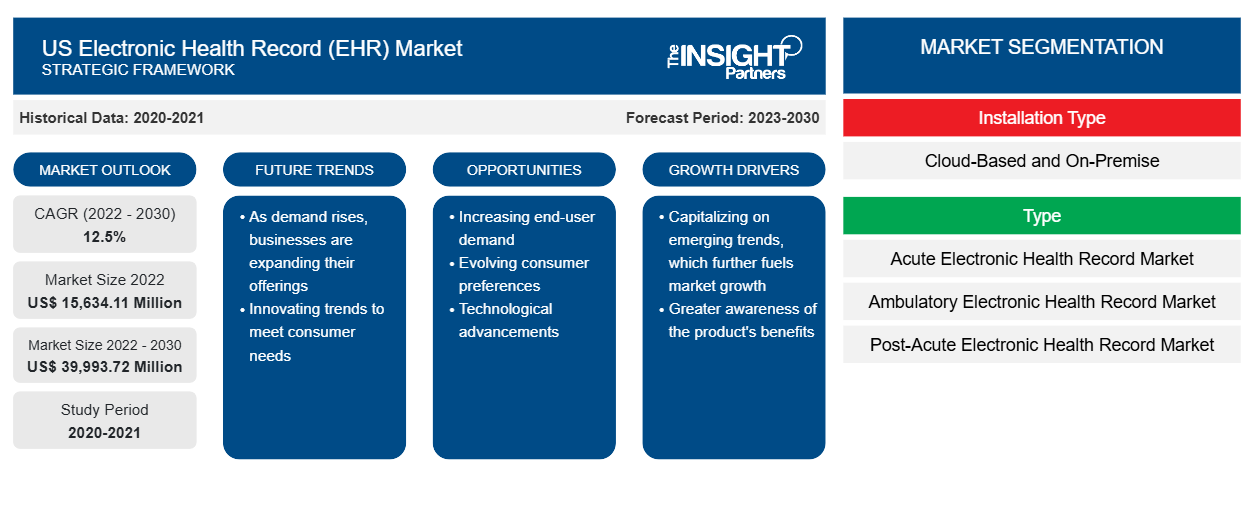

The US electronic health record market size is projected to grow from US$ 15,634.11 million in 2022 to US$ 39,993.72 million by 2030; the market is estimated to record a CAGR of 12.5% during 2022–2030.

Market Insights and Analyst View:

An electronic health record is an electronic version of a patient's medical history that is maintained by the provider over time and may include all of the key administrative and clinical data, including demographics, progress notes, problems, medications, vital signs, past medical history, immunizations, laboratory data, and radiology reports, under a particular provider. The electronic health record automates access to information and has the potential to streamline the clinician's workflow. The electronic health record can also support other care-related activities directly or indirectly through various interfaces, including evidence-based decision support, quality management, and outcomes reporting. Increasing adoption of electronic health records, rising incentives by the federal government, and growing incidences of medication errors are driving the market growth.

Growth Drivers:

Increasing Adoption of Electronic Health Records

Electronic Health Records are becoming increasingly popular with the growing digitization of the healthcare industry. As per The New England Journal of Medicine, as soon as the Health Information Technology for Economic and Clinical Health (HITECH) Act became law in 2009, the federal government dedicated US$ 300 million to help healthcare facilities adopt a nationwide health information exchange system. The Centers for Medicare and Medicaid Services (CMS) also offered more than US$ 35,000 million in incentive payments for electronic health record adoption. According to the Office of the National Coordinator for Health Information Technology (ONC), as of 2021, about 4 in 5 office-based physicians (78%) and almost all non-federal acute care hospitals (96%) adopted a certified electronic health record. This marked considerable 10-year progress when 28% of hospitals and 34% of physicians had adopted an electronic health record since 2011. As per Definitive Healthcare data from 2020, more than 89% of all hospitals had employed inpatient or ambulatory EHR systems.

Further, in May 2020, the US federal government proposed the Federal Health IT Strategic Plan 2020–2025 to mandate the use of electronic health record by healthcare providers. With the facts and statistics stated above, it is evident that the adoption rate of the electronic health record is expected to continue to improve during the forecast period.

Rising Incentives by the Federal Government

The government has invested billions in training health information technology workers and founding regional extension centers to provide technical advice. In 2009, as part of the Health Information Technology for Economic and Clinical Health (HITECH) Act, the federal government reserved US$ 27 billion for an incentive program that inspires hospitals and providers to implement electronic health record systems that would enable the health data historically confiscated in paper files to be shared among providers and use to improve the healthcare quality.

The Medicare Electronic Health Record Incentive Program is governed by the Centers for Medicare & Medicaid Services (CMS). In the US, the Medicare and Medicaid EHR Incentive Programs offer incentives to hospitals, physicians, and other healthcare facilities for meaningful use of certified EHR technology. A qualified professional or hospital can get a maximum incentive amount of up to US$ 63,750 through the Medicaid EHR Incentive Program and up to US$ 44,000 through the Medicare EHR Incentive Program. This incentive program succeeded in inspiring many healthcare facilities to adopt EHR systems.

Customize This Report To Suit Your Requirement

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

US Electronic Health Record (EHR) Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

US Electronic Health Record (EHR) Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Report Segmentation and Scope:

The “US electronic health record market” is segmented on the basis of installation type, type, application, and end user. Based on installation type, the market is segmented into cloud-based and on-premise. In terms of type, the US Electronic health record market is divided into acute electronic health record, ambulatory electronic health record, and post-acute electronic health record. By application, the market is segmented into clinical records, administrative task and billing, physician support, and patient portal. Based on end user, the market is segmented into hospitals and clinics, physician’s office/specialty care centers, and ambulatory surgical centers.

- This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Segmental Analysis:

The US electronic health record market, by installation type, is bifurcated into cloud-based and on-premise. The cloud-based segment held a larger share of the market in 2022 and is anticipated to register a higher CAGR of 12.7% during 2022–2030. A cloud-based electronic health record allows patient health files to be stored in the cloud rather than saving them on internal servers of the healthcare facility. The collected data is organized and maintained in actionable and shareable formats to allow effective communication between healthcare providers, third-party payers, and patients. Cloud-based electronic health records are popular among physicians and healthcare providers operating on a smaller scale as these systems can be installed without any requirement for in-house servers and offer a wide range of customizations and improvements as per their needs.

Cloud-based solutions are cost-effective as cloud computing decreases the cost of managing and maintaining IT systems. Cloud-based electronic health record offers flexibility and enables the user to access the data remotely.

Additionally, developments by market leaders in this segment are likely to improve the market growth. For instance, in July 2020, Cerner launched CommunityWorks Foundations, a cloud-based electronic health record platform, to reduce the cost of traditional electronic health record systems in rural and critical access hospitals. Similarly, in December 2020, Amazon's cloud division introduced a new tool, Amazon HealthLake, for healthcare organizations to search and analyze data.

US Electronic Health Record Market, by Installation Type– 2022 and 2030

- This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Based on type, the US Electronic health record market is segmented into acute electronic health record, ambulatory electronic health record, and post-acute electronic health record. The acute electronic health record segment held the largest market share in 2022, and the post-acute electronic health record segment is anticipated to register the highest CAGR of 10.3% during 2022–2030. Post-acute care facilities consist of rehabilitation centers, home health agencies, and long-term care hospitals. Rehabilitation centers offer education, medically supervised exercise, and support to patients suffering from neurological, cardiovascular, musculoskeletal, orthopedic, and other medical conditions. To provide high-quality services, rehab centers must maximize efficiencies in their administrative tasks, including data maintenance and billing. Most of the modern and advanced rehabilitation centers have turned to electronic systems to reduce the time-consuming paperwork. Electronic health record providers offer electronic health record software, especially for rehab centers. For instance, Orion offers the AccuCare system, an electronic health record and billing solution that is uniquely designed for the addiction rehabilitation field, thereby providing a combination of clinical, financial, management, and research functions that help professionals achieve more.

Home health services can range from nursing care to specialized medical services, such as laboratory tests. A physician may periodically visit patients at home to diagnose and treat medical conditions. Home healthcare software streamlines home healthcare agency management, patient care management, and therapy & rehabilitative service coordination.

Similarly, long-term care hospitals require electronic health record to focus on smooth and safe transitions of care for patients and residents. Meditech offers electronic health record solutions for Long Term Care - Hospitals & Health Systems and helps in delivering high-quality care, enhancing clinical outcomes, reducing medication errors, and optimizing reimbursement.

Based on application, the US electronic health record market is segmented into clinical records, administrative task and billing, physician support, and patient portal. The clinical records segment held the largest market share in 2022 and is anticipated to register the highest CAGR of 10.9% during 2022–2030. A clinical document contains information related to the care and services provided to the patient. It increases the importance of electronic health record by allowing electronic capture of clinical reports, patient assessments, and progress reports. A clinical document may include physician, nurse, and other clinician notes, relevant dates and times associated with the document, performers of the care described, flow sheets (vital signs, input and output, and problem lists), perioperative notes, discharge summaries, transcription document management, medical records abstracts. A clinical document is intended for better communication with the providers. It helps physicians demonstrate accountability and may ensure quality care is provided to the patient. A clinical document needs to be patient-centered, accurate, complete, concise, and prompt to serve these purposes.

Based on end user, the US Electronic health record market is segmented into hospitals and clinics, physician’s office/specialty care centers, and ambulatory surgical centers. The hospitals and clinics segment held the largest share of the market in 2022 and is expected to register the highest CAGR of 12.8% in the market during 2022–2030. Hospitals and clinics are primary contact points for patients to get their diagnosis done and opt for treatment options and alternatives. Available infrastructure in hospitals and clinics is capable of providing high-quality care for any disease condition as they have access to advanced medical devices. The hospitals and clinics segment is projected to hold a considerable share as a majority of patients in emerging nations and developed countries prefer visiting hospitals for health-related problems.

Country Analysis:

The US is the largest market for electronic health records in North America. The market is majorly driven by the transformation of digital healthcare, the increasing number of chronic diseases, and support from the federal government to implement electronic health record in order to improve the quality of care. Other factors, such as the introduction of advanced software technologies in healthcare, a higher number of hospitals, and the implementation of strategic government policies also aid in promoting the US electronic health record market expansion. Additionally, the need for automated systems due to the increasing patient population and crunch of healthcare resources are projected to fuel the adoption of electronic health record systems in the US. Emphasis on error reduction in hospital administrative work, which causes considerable mortalities, is also prominently anticipated to drive the growth of the market during the forecast period. For instance, as per a study published in the Journal of Patient Safety, an estimated 400,000 patient casualties are caused due to administrative errors in the US each year.

The presence of major market players in the country, along with their developments, is likely to favor the growth of the market. In September 2023, the Georgian Bay Information Network (GBIN), a partnership of six Ontario healthcare organizations, advanced its use of Oracle Health’s electronic health records by adding new capabilities for advanced clinical services, optimized medication administration, and oncology specialty support under its recently launched multi-year project called eNautilus. These additions are expected to help caregivers improve patient safety, enhance collaboration between caregivers across facilities, and reduce the administrative burden on clinicians across the GBIN’s combined 15 hospitals.

In April 2023, Microsoft Corp. and Epic expanded their established strategic collaboration to develop and integrate generative AI into healthcare by merging the scale and power of Azure OpenAI Service with Epic's industry-leading electronic health record software. The collaboration expands the long-standing partnership, which includes allowing organizations to run Epic environments on the Microsoft Azure cloud platform. This co-innovation is focused on delivering an inclusive array of generative AI-powered solutions integrated with Epic's electronic health record to increase productivity, improve patient care, and improve the financial integrity of health systems.

Industry Developments and Future Opportunities:

Various initiatives taken by key players operating in the US electronic health record market are listed below:

- In November 2023, eClinicalWorks LLC launched AI assistant tools that easily translate medical documents into its patients’ native language within the electronic health record.

- In September 2023, Oracle announced significant additions to its healthcare solutions, including new cloud-based electronic health record capabilities, generative AI services, public Application Programming Interfaces (APIs), and back-office enhancements designed for the healthcare industry.

- In May 2022, Greenway Health launched Greenway Secure Cloud, a cost-effective, fully bundled, cloud-based electronic health record and practice management solution. This product increases the security of patient health information and practice records, eliminates the need to manage software upgrades, and provides scalable, all-inclusive pricing to clients. It helps protect against cybersecurity threats by safely managing provider data in a maximum-security center and regularly and consistently patching security concerns in the ever-changing landscape of ransomware and malware attacks. Greenway Secure Cloud also offers data uptime of 99.9 % per year with timely automated updates to certify compliance in a regulatory environment that can be challenging for practices to navigate on their own.

Competitive Landscape and Key Companies:

Oracle Corp, AltexSoft Inc, Veradigm Inc, Greenway Health LLC, eClinicalWorks LLC, Infor-Med Inc, Microwize Technology Inc, Athenahealth Inc, ChipSoft BV, CureMD.com Inc, AdvancedMD Inc, and PracticeSuite Inc are the prominent US electronic health record market companies. These companies focus on new technologies, existing products’ advancements, and geographic expansions to meet the growing consumer demand worldwide.

US Electronic Health Record (EHR) Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 15,634.11 Million |

| Market Size by 2030 | US$ 39,993.72 Million |

| Global CAGR (2022 - 2030) | 12.5% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Installation Type

|

| Regions and Countries Covered | United State

|

| Market leaders and key company profiles |

Frequently Asked Questions

What are the driving factors for the US Electronic Health Record Market?

The growth of the market is attributed to an increasing adoption of electronic health records, and rising incentives by the federal government are the key driving factors behind the market development. However, the concerns regarding data privacy are hampering the market growth.

Which segment is dominating the US Electronic Health Record Market?

The US electronic health record market is analyzed on installation type, type, application, and end user. Based on installation type, the market is segmented into cloud-based and on-premise. In terms of type, the US Electronic health record market is divided into acute electronic health record, ambulatory electronic health record, and post-acute electronic health record. By application, the market is segmented into clinical records, administrative task and billing, physician support, and patient portal. Based on end user, the market is segmented into hospitals and clinics, physician’s office/specialty care centers, and ambulatory surgical centers. The cloud-based segment by installation type held a larger share of the market in 2022 and is anticipated to register a higher CAGR during 2022–2030

What is the Electronic Health Record Market?

An electronic health record is an electronic version of a patient's medical history that is maintained by the provider over time and may include all of the key administrative and clinical data, including demographics, progress notes, problems, medications, vital signs, past medical history, immunizations, laboratory data, and radiology reports, under a particular provider. The electronic health record automates access to information and has the potential to streamline the clinician's workflow.

Market Research & Consulting

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

- Parking Meter Apps Market

- eSIM Market

- Advanced Distributed Management System Market

- Online Exam Proctoring Market

- Electronic Data Interchange Market

- Barcode Software Market

- Maritime Analytics Market

- Cloud Manufacturing Execution System (MES) Market

- Robotic Process Automation Market

- Digital Signature Market

Testimonials

I wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.The Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.We worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, Market ResearchThe research report delivered details on drivers and restraints, trends, and opportunities, along with strategic activities in the market. Previously, we were struggling to get reliable information.

Manager Medical Devices ManufacturingReason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Yes! We provide a free sample of the report, which includes Report Scope (Table of Contents), report structure, and selected insights to help you assess the value of the full report. Please click on the "Download Sample" button or contact us to receive your copy.

Absolutely — analyst assistance is part of the package. You can connect with our analyst post-purchase to clarify report insights, methodology or discuss how the findings apply to your business needs.

Once your order is successfully placed, you will receive a confirmation email along with your invoice.

• For published reports: You’ll receive access to the report within 4–6 working hours via a secured email sent to your email.

• For upcoming reports: Your order will be recorded as a pre-booking. Our team will share the estimated release date and keep you informed of any updates. As soon as the report is published, it will be delivered to your registered email.

We offer customization options to align the report with your specific objectives. Whether you need deeper insights into a particular region, industry segment, competitor analysis, or data cut, our research team can tailor the report accordingly. Please share your requirements with us, and we’ll be happy to provide a customized proposal or scope.

The report is available in either PDF format or as an Excel dataset, depending on the license you choose.

The PDF version provides the full analysis and visuals in a ready-to-read format. The Excel dataset includes all underlying data tables for easy manipulation and further analysis.

Please review the license options at checkout or contact us to confirm which formats are included with your purchase.

Our payment process is fully secure and PCI-DSS compliant.

We use trusted and encrypted payment gateways to ensure that all transactions are protected with industry-standard SSL encryption. Your payment details are never stored on our servers and are handled securely by certified third-party processors.

You can make your purchase with confidence, knowing your personal and financial information is safe with us.

Yes, we do offer special pricing for bulk purchases.

If you're interested in purchasing multiple reports, we’re happy to provide a customized bundle offer or volume-based discount tailored to your needs. Please contact our sales team with the list of reports you’re considering, and we’ll share a personalized quote.

Yes, absolutely.

Our team is available to help you make an informed decision. Whether you have questions about the report’s scope, methodology, customization options, or which license suits you best, we’re here to assist. Please reach out to us at sales@theinsightpartners.com, and one of our representatives will get in touch promptly.

Yes, a billing invoice will be automatically generated and sent to your registered email upon successful completion of your purchase.

If you need the invoice in a specific format or require additional details (such as company name, GST, or VAT information), feel free to contact us, and we’ll be happy to assist.

Yes, certainly.

If you encounter any difficulties accessing or receiving your report, our support team is ready to assist you. Simply reach out to us via email or live chat with your order information, and we’ll ensure the issue is resolved quickly so you can access your report without interruption.

The List of Companies -

- Oracle Corp

- AltexSoft Inc

- Veradigm Inc

- Greenway Health LLC

- eClinicalWorks LLC

- Infor-Med Inc

- Microwize Technology Inc

- Athenahealth Inc

- ChipSoft BV

- CureMD.com Inc

- AdvancedMD Inc

- PracticeSuite

Get Free Sample For

Get Free Sample For