Photoresist Process Chemicals Market Share, Size & Demand by 2034

Photoresist Process Chemicals Market Size and Forecast (2021 - 2034), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product Type (Solvents, Binders, Sensitizer, and Others) and Application (Microelectronics, Printed Circuit Boards, and Others)

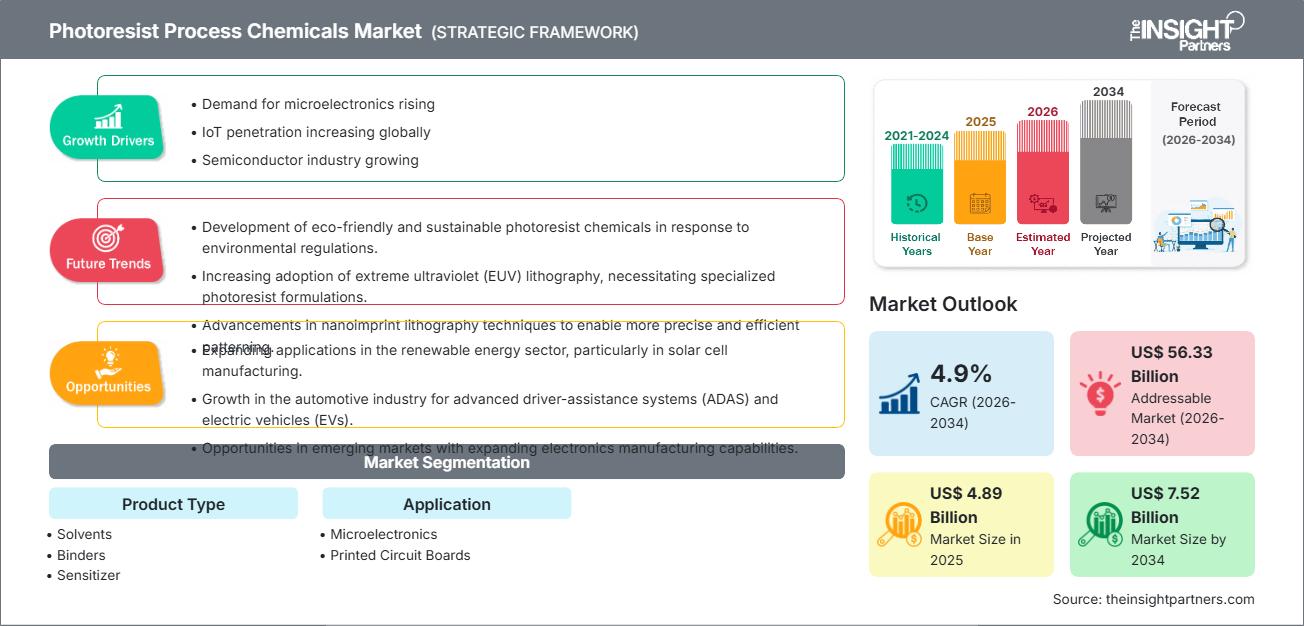

Historic Data: 2021-2024 | Base Year: 2025 | Forecast Period: 2026-2034- Report Date : Apr 2026

- Report Code : TIPRE00021610

- Category : Chemicals and Materials

- Status : Upcoming

- Available Report Formats :

- No. of Pages : 150

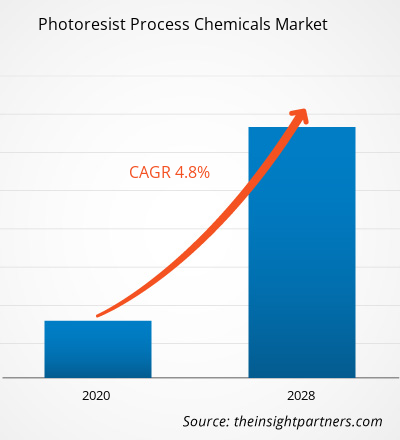

The global photoresist process chemicals market size is projected to reach US$ 7.52 billion by 2034 from US$ 4.89 billion in 2025. The market is anticipated to register a CAGR of 4.9% during the forecast period 2026–2034. Key market dynamics include a heightening global focus on ultra-pure specialty chemicals, rising industry awareness regarding the necessity of advanced node scaling for AI chips, and a significant shift toward Extreme Ultraviolet (EUV) lithography materials. Additionally, the market is expected to benefit from the growing popularity of 5G-enabled infrastructure, expansion in semiconductor fabrication plants (fabs) across emerging economies, and the increasing inclusion of high-purity solvents and sensitizers in high-value electronics segments like automotive radar and sophisticated consumer hardware.

Photoresist Process Chemicals Market Analysis

The photoresist process chemicals market analysis shows a shift toward high-purity chemical grades as semiconductor manufacturers prioritize yield rates and sub-7nm process stability. Procurement trends indicate the market is splitting into traditional i-line and g-line chemicals for legacy PCB sectors and high-growth EUV and ArF-exclusive markets in East Asia and North America. Strategic opportunities are emerging in specialty binders and sensitizers, where superior etch resistance and thermal stability compared to standard chemical alternatives offer a clear competitive advantage in advanced node fabrication. The analysis also notes that market expansion depends on the vertical integration of chemical supply chains to prevent disruptions and the efficiency of purification technologies for electronic-grade solvents. Competitive differentiation now stands out depending on R&D branding that highlights localized manufacturing, "zero-defect" quality control, and the ability to track the purity of raw materials from source to cleanroom. This approach helps top-tier chemical vendors secure long-term contracts in a market with high barriers to entry.

Photoresist Process Chemicals Market Overview

Photoresist process chemicals are shifting from a regional specialty chemical sector to a global strategic commodity. While historically focused on standard microelectronics, photoresist process chemicals are expanding into value-added segments like high-density interconnects (HDI), advanced packaging, and 3D NAND flash memory chemicals. Both established chemical giants and specialized lithography material providers are part of this market, making use of sophisticated polymer binders and sensitizers found in modern resist systems. More performance-conscious tech companies in North America and Asia-Pacific are looking for materials that can handle shrinking feature sizes, which has helped EUV-compatible chemicals gain popularity as a "next-generation" choice. Asia-Pacific remains the main production hub, but North America is witnessing a resurgence in domestic manufacturing through government-backed initiatives. For instance, the market in the US and North America is experiencing a significant transformation driven by the CHIPS Act and the rapid expansion of domestic semiconductor fabs. Increased investments in advanced logic and memory production are fueling demand for high-purity solvents and specialized sensitizers, positioning the region as a critical hub for high-performance lithography chemical innovation and supply chain security.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONPhotoresist Process Chemicals Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Photoresist Process Chemicals Market Drivers and Opportunities

Market Drivers:

- Expansion of Semiconductor Fabrication Capacity: The global surge in fab construction to meet chip shortages and national security needs is driving massive demand for process chemicals. This expansion, coupled with the move toward self-sufficiency in electronic materials, is a primary growth engine.

- Adoption of Advanced Lithography (EUV): The transition to sub-5nm nodes requires entirely new chemical formulations for photoresists. As manufacturers trade up to these advanced processes, the volume and value of EUV-specific process chemicals continue to see stable gains.

- Growth in High-Density Interconnect (HDI) PCBs: The proliferation of 5G devices and AI servers has increased the complexity of printed circuit boards. This is particularly evident in the rapid adoption of high-performance binders and developers in regions like Asia-Pacific.

Market Opportunities:

- Expansion into Advanced Packaging Materials: Beyond the lithography step, photoresist chemicals offer significant opportunities in Redistribution Layers (RDL) and through-silicon via (TSV) processes for 2.5D and 3D packaging.

- Localization of Chemical Supply Chains: Forming strategic partnerships between chemical suppliers and local fab operators may facilitate access to high-margin market segments in the US and Europe, where demand for reliable, local sourcing is increasing.

- Diversification into Eco-friendly Solvents: There is a growing opportunity for producers to target "green fab" initiatives through the development of low-toxicity, recyclable process chemicals, as seen in recent sustainable R&D breakthroughs.

Photoresist Process Chemicals Market Report Segmentation Analysis

The Photoresist Process Chemicals Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Product Type:

- Solvents: The dominant volume driver, essential for photoresist dilution and wafer cleaning, benefiting from the global increase in silicon wafer starts.

- Binders: A critical component for pattern integrity and adhesion. It is increasingly preferred for its thermal stability in high-temperature etching environments.

- Sensitizers: A fast-growing high-value segment that enables the chemical reaction during light exposure, particularly vital for high-sensitivity EUV resists.

By Application:

- Microelectronics: Remains the primary channel, encompassing CPUs, GPUs, and memory chips, benefiting from the global AI and data center boom.

- Printed Circuit Boards: A select but growing range of process chemicals used in high-density boards for automotive and aerospace applications.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Photoresist Process Chemicals Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 4.89 Billion |

| Market Size by 2034 | US$ 7.52 Billion |

| Global CAGR (2026 - 2034) | 4.9% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Product Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Photoresist Process Chemicals Market Players Density: Understanding Its Impact on Business Dynamics

The Photoresist Process Chemicals Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Photoresist Process Chemicals Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years due to the concentration of major foundries. Emerging markets in Europe and North America also have many untapped opportunities as they seek to rebuild their domestic semiconductor ecosystems.

1. North America

- Market Share: A highly innovative segment driven by high-end logic design and the aggressive "reshoring" of semiconductor manufacturing.

- Key Drivers:

- Rising federal investment in domestic chip production through the CHIPS Act, resulting in several mega-fabs entering the commissioning phase in 2026.

- Mainstreaming of advanced AI chip fabrication, which requires a higher density of specialty lithography chemicals per unit.

- Increased focus on R&D for next-generation High-NA EUV materials led by companies like Intel and DuPont.

- Trends: Strategic partnerships and joint development agreements (JDAs) between design firms and chemical manufacturers to co-develop resists for specific, proprietary chip architectures.

2. Europe

- Market Share: Holds a significant share in the high-tech equipment and chemical supply ecosystem, anchored by lithography leader ASML and specialty chemical giants like Merck KGaA.

- Key Drivers:

- High demand for automotive-grade semiconductors and power ICs in Germany and France to support the regional EV transition.

- Established processing infrastructure and the world's strictest purity and environmental regulations.

- Robust government support for the "European Chips Act" to double Europe’s global manufacturing share by 2030.

- Trends: A strategic shift toward ultra-high-purity "green" chemicals and the validation of sustainable, bio-based solvents to meet strict EU chemical safety standards.

3. Asia-Pacific

- Market Share: The largest and fastest-growing region with Taiwan, South Korea, and Japan acting as the primary engines for the global semiconductor industry.

- Key Drivers:

- The region serves as the primary hub for TSMC and Samsung, which collectively command the majority of global advanced photoresist demand.

- Government-supported fab expansions and the creation of "chemical industrial parks" in South Korea and Japan to secure upstream material supply.

- Rapid urbanization and the rise of digital infrastructure in India and SE Asia, increasing demand for mature-node semiconductors.

- Trends: Heavy reliance on long-term B2B contracts for customized resist systems tailored to 3nm and 2nm production lines, alongside massive capacity ramp-ups in China for G-line/I-line resists.

4. South and Central America

- Market Share: An emerging, niche segment primarily focused on assembly, testing, and back-end processing rather than front-end wafer fabrication.

- Key Drivers:

- Gradual expansion of the regional electronics supply chain in Brazil and Argentina to serve the North American automotive and consumer electronics markets.

- Increasing adoption of Internet of Things (IoT) devices driving a steady demand for Printed Circuit Board (PCB) lithography chemicals.

- Growth in electric vehicle (EV) adoption in South America, boosting demand for power electronics and associated chemicals.

- Trends: Growth in local semiconductor assembly and testing (OSAT) activities, creating a secondary market for thick-film resists used in advanced packaging.

5. Middle East and Africa

- Market Share: A developing market characterized by early-stage investments in high-tech manufacturing and national economic diversification initiatives.

- Key Drivers:

- Strategic government-led industrial development programs in Saudi Arabia and the UAE (e.g., Vision 2030) targeting local semiconductor-related facility build-outs.

- High demand for specialized chemicals for optoelectronics and photonic devices used in regional energy and industrial sectors.

- Partnerships with global semiconductor companies to transfer technology and localize production.

- Trends: Implementation of modern milking and refrigeration technologies, or in this context, localized "Smart Factory" chemical blending hubs, to support emerging niche manufacturing nodes and reduce import reliance.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Tokyo Ohka Kogyo Co., Ltd., Tokuyama Corporation, and Dupont. Regional experts and niche players like Allresist Gmbh and Microchemicals Gmbh, alongside diversified giants like Sumitomo Chemical, also contribute to a diverse and rapidly expanding market landscape. This competitive environment pushes vendors to differentiate through:

- Purity and Precision: Positioning chemicals as "electronic grade" with part-per-trillion (ppt) impurity levels to ensure high yields for health-conscious fab managers.

- Technological Innovation: Companies offer more than just basic chemicals; they provide "lithography stacks" that include primers, resists, and developers designed to work in sync.

- Integrated Supply Management: Producers manage the entire supply chain, from specialized polymer synthesis to clean-room packaging, ensuring quality and transparency.

Opportunities and Strategic Moves

- Expansion into Advanced Packaging: Capitalize on the rising adoption of 2.5D and 3D IC packaging by developing specialized thick-film resists and removers that can handle the high aspect ratios and complex interconnect layouts of modern chiplets.

- ESG and Green Chemistry: Invest in "PFAS-free" and low-solvent formulations to get ahead of tightening global environmental regulations, which are increasingly targeting the fluorinated compounds historically used in high-performance photoresists.

Major Companies operating in the Photoresist Process Chemicals Market are:

- Tokyo Ohka Kogyo Co., Ltd.

- Tokuyama Corporation

- Dupont

- Integrated Micro Materials

- Allresist Gmbh

- Microchemicals Gmbh

- Dischem Inc

- ENF TECHNOLOGY CO., LTD.

- Sumitomo Chemical Co., Ltd

Disclaimer: The companies listed above are not ranked in any particular order.

Photoresist Process Chemicals Market News and Recent Developments

- In January 2025, Lam Research’s Aether® dry photoresist technology was adopted by a leading memory manufacturer for advanced DRAM production, enhancing EUV lithography precision, yield, and cost efficiency. It supports faster, low-defect semiconductor patterning and sustainable manufacturing. This represents a move toward next-generation, high-performance, and environmentally optimized photoresist process chemicals.

- In May 2025, Asahi Kasei launched the TA Series of Sunfort™ dry film photoresist, designed for advanced semiconductor packaging used in AI servers. The product delivers ultra-high resolution and enhances production efficiency and yield in back-end processes. This represents a move toward more precise, cost-effective, and workflow-optimized photoresist solutions for next-generation semiconductor devices.

Photoresist Process Chemicals Market Report Coverage and Deliverables

The "Photoresist Process Chemicals Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Photoresist Process Chemicals Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Photoresist Process Chemicals Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Photoresist Process Chemicals Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Photoresist Process Chemicals Market.

- Detailed company profiles

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Get Free Sample For

Get Free Sample For