澳大利亚和新西兰床旁诊断超声市场基于(关键地区、市场参与者、规模和份额)- 到 2030 年的预测

澳大利亚和新西兰护理点诊断超声市场规模和预测(2020 - 2030)、区域份额、趋势和增长机会分析报告范围:按技术(2D、3D/4D 等)、便携性(手推车和紧凑型/手持式)、应用(普通影像、外科、心脏病学等)和最终用户(急诊科、重症监护室、手术室、IVF 诊所、物理治疗中心、运动医学、全科医生、呼吸中心、麻醉、和普通病房)

- 状态 : 已发布

- 报告代码 : TIPRE00033417

- 类别 : 生命科学

- 页数 : 137

- 可用报告格式 :

- 最后更新日期 : January 18, 2024

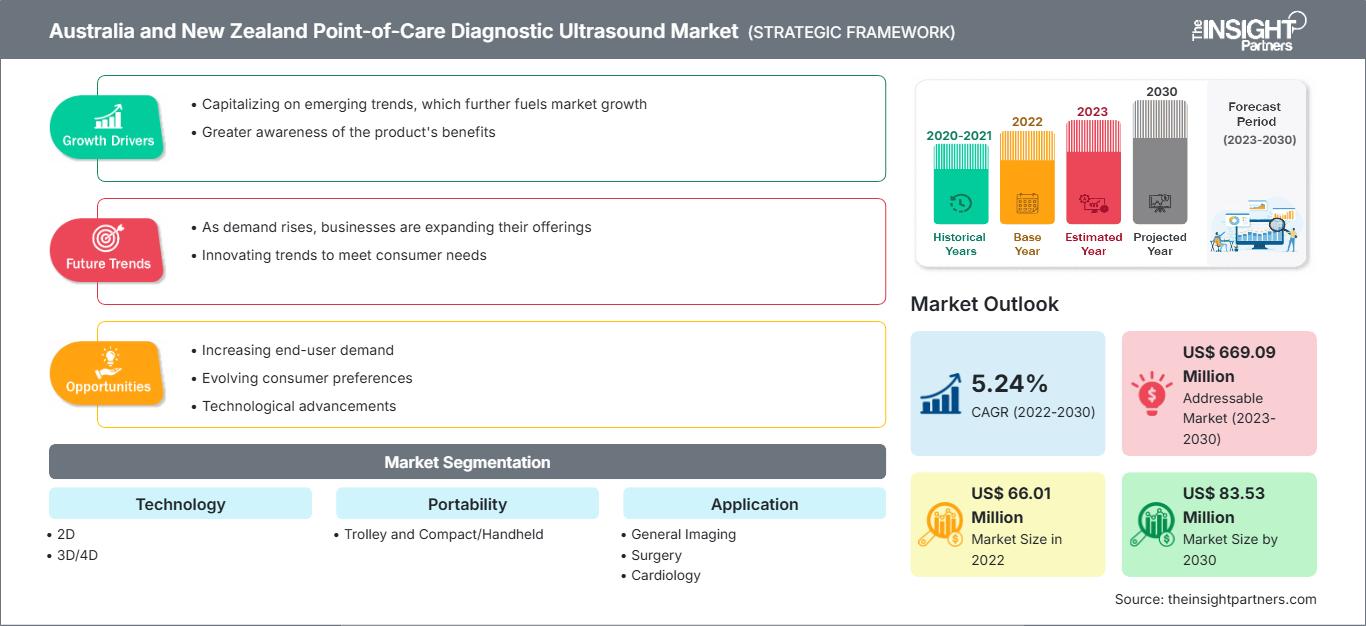

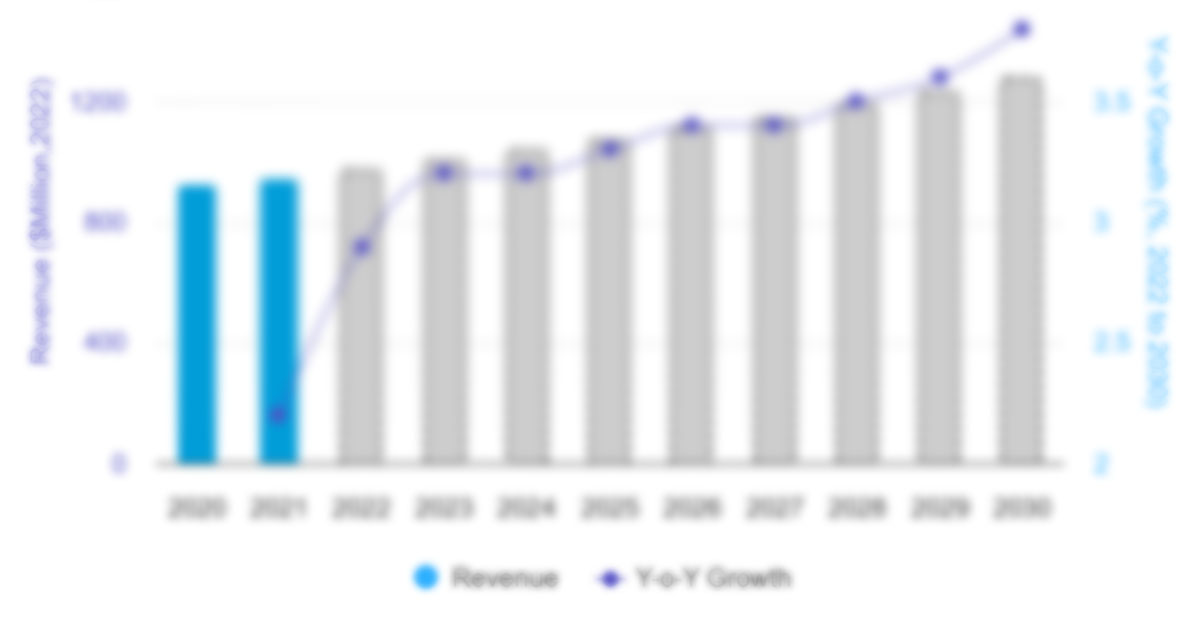

预计澳大利亚和新西兰即时诊断超声市场规模将从 2022 年的 6601 万美元增长到 2030 年的 8353 万美元;预计 2022 年至 2030 年的复合年增长率为 5.24%。

分析师观点

床旁超声(POCUS)在澳大利亚和新西兰的急诊科应用日益广泛,如今已被视为急诊医师的一项基本技能。技术进步有望减轻澳大利亚偏远地区医疗服务可及性问题带来的负面影响。未来技术很可能进一步发展,更多用户将有机会使用小型、手持式和便携式超声设备。

与以往相比,澳大利亚医疗机构目前可使用的床旁超声(POCUS)设备种类更加丰富。位于澳大利亚昆士兰州的凯恩斯医院引进了最先进的迈瑞TEX20高端POC超声设备,帮助急诊医生应对资源匮乏、患者群体多样化以及缺乏后续护理等挑战。择期手术和急诊数量的不断增长,使得人们更加需要利用POC超声进行更安全、更准确、更实时的疾病诊断。然而,熟练技术人员的短缺可能会影响2022年至2030年澳大利亚和新西兰床旁诊断超声市场的预测。

市场洞察

慢性病发病率的不断上升,以及因各种健康问题(例如急性腹痛、泌尿系统疾病和剧烈胸痛)需要紧急救治的患者人数的增加,推动了床旁超声(POCUS)设备的需求激增。POCUS 能够简化患者护理流程,提高医疗程序的有效性,减少并发症,并节省宝贵时间。POCUS 在诊断肺部疾病方面的准确性与实验室指标相当,甚至更高。因此,这些疾病发病率的上升以及需要紧急救治的患者人数的增加,预计将成为澳大利亚和新西兰床旁诊断超声市场预测的主要驱动因素之一。

床旁超声(POCUS)作为一种快速诊断工具,已被广泛应用于多个学科,尤其是在急诊医学领域。POCUS 使急诊科的医师助理(PA)或执业护士(NP)能够立即获取、解读超声图像并将其应用于临床诊疗。在急诊科,借助这些设备可以开展多种临床应用,例如快速超声检查(FAST)、聚焦超声心动图、肺部超声、引流以及其他一些操作。POCUS 已被用于辅助诊断多种疾病,包括急性阑尾炎、气道阻塞、腹主动脉瘤以及创伤评估等。因此,对于急诊科而言,配备 POCUS 至关重要,它可以提高急诊科的效率,使其能够有效应对各种紧急情况。POCUS 的快速便捷使其成为在正式放射学检查可能延误诊断的情况下的一种潜在选择。因此,床旁诊断超声在急诊护理中的应用日益广泛,从而推动了澳大利亚和新西兰床旁诊断超声市场在预测期内的增长。

未来趋势

超声设备正逐渐融合机器人技术、云计算、5G网络、人工智能(AI)和远程技术。随着时间的推移,超声系统已发展成为具备强大成像和通信能力的先进终端平台。此外,为了满足众多临床专科和科室日益增长的需求和规范,专用超声设备的需求也越来越大。远程床旁超声(POCUS)是一种利用现代计算机、网络连接和多媒体技术,通过数字化重建POCUS图像,从而远程采集、存储、传输、分析和处理图像的技术。通过高精度同步,可以实现通过文本、音频、视频和其他多通道连接进行的远程实时诊断和介入治疗。预计POCUS领域的这些技术将推动澳大利亚和新西兰床旁诊断超声市场规模的增长。

近年来,随着5G技术的发展,机器人操作和远程超声会诊对实时性、远距离、高分辨率、高带宽和低延迟的要求已得到满足,使得高质量床旁超声(POCUS)图像的传输和共享成为可能,使其成为宝贵的医疗资源。这为远程POCUS技术的广泛应用打开了大门。因此,预计未来澳大利亚和新西兰床旁诊断超声市场的增长将主要得益于床旁超声自动化程度的不断提高。

根据您的需求定制此报告

获取免费定制服务澳大利亚和新西兰即时诊断超声市场:战略洞察

-

获取本报告的主要市场趋势。这份免费样品将包含数据分析,内容涵盖市场趋势、估算和预测等。

报告细分和范围

澳大利亚和新西兰床旁诊断超声市场按技术、便携性、应用和最终用户进行细分。按技术划分,市场分为二维、三维/四维和其他类型。按便携性划分,市场分为推车式和便携式/手持式。按应用划分,澳大利亚和新西兰床旁诊断超声市场分为普通影像、心脏病学、外科手术和其他领域。按最终用户划分,市场分为急诊、重症监护/危重症监护、手术室、试管婴儿诊所、理疗中心、运动医学、全科医生、呼吸中心、麻醉科和普通病房。

- 这份免费样品将包含数据分析,内容涵盖市场趋势、估算和预测等。

基于技术的洞察

根据技术,澳大利亚和新西兰的床旁诊断超声市场可分为二维、三维/四维和其他类型。2022年,二维超声在澳大利亚和新西兰的床旁诊断超声市场占据最大份额。预计从2022年到2030年,三维/四维超声的复合年增长率将最高。在超声成像中,B型模式是在超声屏幕上生成二维(2D)灰阶图像,是最常用的模式,通常被称为二维模式。二维超声系统在市场上很容易买到,而且价格实惠。二维超声使用高频非电离声波,这些声波在一个平面上发射和接收。通常,二维超声用于诊断孕妇胎儿的健康状况。它生成黑白图像,显示胎儿的骨骼结构,并使内部器官清晰可见。床旁超声(POCUS)生成的二维图像使医护人员能够实时观察器官、血管和其他结构,从而辅助诊断和指导手术。与其他技术相比,二维超声更易于使用、更省时省力且更经济。此外,其卓越的图像质量和快速的检查结果也使其在诊断中心得到广泛应用。

基于可移植性的见解

根据便携性,澳大利亚和新西兰的床旁诊断超声市场可分为推车式和便携式/手持式两大类。2022年,推车式超声在澳大利亚和新西兰的床旁诊断超声市场份额更大,预计在2022年至2030年期间将保持最高的复合年增长率。推车式超声是一种便携式超声设备,常用于医疗机构的诊断成像。它使医护人员能够在不中断患者治疗的情况下,方便地在床旁对卧床患者进行诊断。推车式诊断超声便于在医院和诊断中心内移动。这些设备适用于监测胎儿和患者。

该系统经济高效,且不占用额外空间,因此深受小型诊所和医生的青睐。该系统的多功能性、人性化的操作特性、影像诊断技术的日益普及,以及在急诊和急救环境中推车式超声设备的广泛应用,都推动了澳大利亚和新西兰床旁诊断超声市场的增长。

基于应用的洞察

从应用领域来看,澳大利亚和新西兰的床旁诊断超声市场可分为普通影像、心脏病学、外科手术和其他领域。2022年,心脏病学领域占据了澳大利亚和新西兰床旁诊断超声市场最大的份额。预计在2022年至2030年期间,普通影像领域将实现最高的复合年增长率。床旁超声(POC)是指医护人员在患者床旁或临床环境中使用便携式超声设备进行检查。在普通影像领域,床旁超声可提供实时可视化图像,并有助于诊断各种疾病。它具有便捷性和便携性,适用于各种医疗环境。其紧凑便携的特性使医护人员能够在患者床旁进行影像检查,从而更轻松地实时评估不同的解剖结构和器官系统。此外,床旁超声经济高效,能够提升患者护理水平,加快诊断速度,并提高普通影像领域医疗评估的效率和准确性。它是一种快速便捷的初步评估工具,可指导后续的诊断和治疗决策。

基于最终用户的洞察

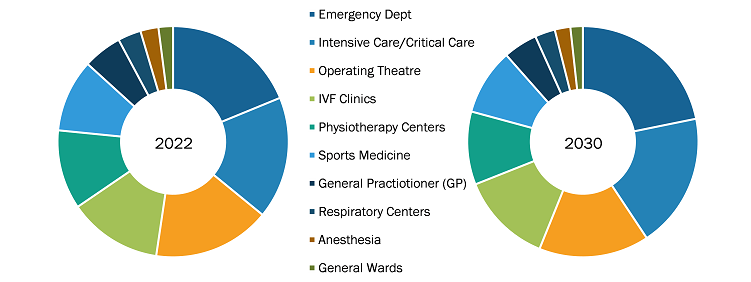

根据最终用户,澳大利亚和新西兰的床旁诊断超声市场可细分为急诊科、重症监护/危重症监护室、手术室、试管婴儿诊所、理疗中心、运动医学科、全科医生诊所、呼吸中心、麻醉科和普通病房。2022年,急诊科在澳大利亚和新西兰的床旁诊断超声市场中占据最大份额,预计在预测期内将保持最高的复合年增长率。

澳大利亚和新西兰即时诊断超声市场(按最终用户划分)——2022 年和 2030 年

- 这份免费样品将包含数据分析,内容涵盖市场趋势、估算和预测等。

国家分析

传统上,超声检查主要由超声医师、放射科专科医师和心脏病专家负责。随着床旁超声的引入,这种情况发生了改变,如今床旁超声已被应用于多个专科,用于诊断和手术指导。澳大利亚乡村医生将产科超声检查视为其床旁超声实践的重要组成部分。由于训练有素的超声医师长期短缺,与都市和偏远地区的孕妇相比,澳大利亚乡村和偏远地区的孕妇更难及时获得超声检查服务。

根据澳大利亚健康与福利研究所2021年的癌症数据,癌症是该国主要的疾病和死亡原因之一。2021年,澳大利亚约有15.1万例新增癌症病例,平均每天413例。同年,约有4.9万人死于癌症,平均每天135人死亡。此外,预计到2023年,结直肠癌将成为该国第四大常见癌症,当年报告病例约1.54万例。床旁超声(POCUS)已被证明是诊断胃肠道癌症的准确技术。因此,上述因素将推动澳大利亚和新西兰床旁超声诊断市场在预测期内的增长。

该报告重点介绍了澳大利亚和新西兰即时诊断超声市场的主要参与者,包括GE医疗、Butterfly Network, Inc.、富士胶片、Esoate SpA、Hologic, Inc.、Echonous Inc.、皇家飞利浦、深圳迈瑞生物医疗电子股份有限公司和Clarius Mobile Health Corp.。这些公司致力于推出新产品和拓展地域市场,以满足全球日益增长的消费者需求,并丰富其专业产品组合。它们拥有广泛的全球布局,能够服务众多客户,从而提升市场份额。

行业发展与未来机遇

:

- 2021年1月,Hologic公司推出全新SuperSonic MACH 20超声系统,进一步拓展了其超声产品组合。Hologic公司提供三种不同技术的超声系统,确保更多医疗机构能够获得定制化的超声解决方案,满足其独特的成像需求。这些系统旨在提高效率和诊断准确性,具备高质量图像和创新成像模式,并提供直观的用户体验。

- 2020年7月,富士胶片索诺施公司推出了新型Sonosite PX超声系统。Sonosite PX是Sonosite POCUS的下一代产品,拥有Sonosite系统有史以来最先进的图像清晰度、一系列提高工作流程效率的功能以及灵活的外形尺寸。

- 2020年3月,EchoNous公司宣布其KOSMOS平台获得FDA批准。该平台由一个独特的8盎司(约227克)超声设备组成,将基于超声的工具与深度学习相结合,用于对心脏、肺部和腹部进行临床评估。它是医学领域首个应用机器学习数学框架来模拟人类学习和决策过程的工具。

澳大利亚和新西兰床旁诊断超声报告范围

| 报告属性 | 细节 |

|---|---|

| 2022年市场规模 | 6601万美元 |

| 到2030年市场规模 | 8353万美元 |

| 复合年增长率(2022-2030 年) | 5.24% |

| 史料 | 2020-2021 |

| 预测期 | 2023-2030 |

| 涵盖的领域 |

通过技术

|

| 覆盖地区和国家 |

澳大利亚和新西兰

|

| 市场领导者和主要公司简介 |

|

Mrinal 是一位经验丰富的研究分析师,在生命科学市场情报和咨询领域拥有超过 8 年的经验。凭借战略思维和对卓越的不懈追求,她在医药预测、市场机遇评估和行业基准制定方面积累了深厚的专业知识。她的工作致力于提供切实可行的洞察,帮助客户做出明智的战略决策。

Mrinal 的核心优势在于将复杂的定量数据集转化为有意义的商业智能。她敏锐的分析能力有助于制定市场进入 (GTM) 战略,并发掘制药和医疗器械行业的增长机会。作为一名值得信赖的顾问,她始终致力于简化工作流程并建立最佳实践,从而为客户推动创新并提高运营效率。

- 全面的市场规模与预测分析

- 详细的细分市场分析

- 深入的市场动态评估

- 区域及国家级洞察

- 竞争格局与企业对标分析

- 战略性商业情报

客户评价

Insight Partners 的 SCADA 系统市场报告内容全面,对当前趋势和未来预测提供了宝贵的见解。该团队始终高度专业、响应迅速且乐于助人。我们非常满意,强烈推荐他们的服务。

兰·凯德姆 伙伴, Reali Technologies LTD我请求一份关于特定软件市场的报告,团队在几天内就完成了。报告信息非常相关,而且呈现得非常出色。之后,我请求对报告进行一些修改和补充。团队再次迅速响应,不到一周我就收到了最终报告。

让-埃尔韦·詹恩 主席, 未来分析公司我们与 Insight Partners 合作进行了一项重要的市场研究和预测。他们清晰地洞察了机遇和风险,帮助我们制定了计划。他们的研究简单易用,数据可靠,帮助我们做出了明智而自信的决策。我们强烈推荐他们。

皮尤什·纳格帕尔 高级副总裁, 远光全球Insight Partners 凭借其深厚的行业专业知识,提供了富有洞察力、结构合理的市场研究。他们的团队始终专业且响应迅速。用户友好的网站让访问行业报告变得顺畅无阻。我们强烈推荐他们可靠、高质量的研究服务。

安达幸彦 首席执行官, 深蓝有限责任公司这是我第一次从The Insight Partners购买市场报告。起初我有些犹豫,但访问了他们的网站后,我更放心地冒险购买市场报告。我对报告的质量和客户服务非常满意。我对最初的报告有一些疑问和意见,但在与他们的分析师通过电子邮件沟通了几次后,我相信这份报告可以作为我们战略规划流程的参考。非常感谢您抽出宝贵的时间,让这次体验如此愉快。我一定会向其他人推荐你们的服务,当我们需要更多市场数据时,你们将是我的首选。

约翰·铃木 总裁兼首席执行官、董事会董事, BK科技感谢您在处理我关于尼日利亚传染病体外诊断市场信息请求的过程中所展现的支持和专业精神。感谢您的耐心、指导,以及您愿意提供的折扣,最终促成了这笔交易。我期待未来与 Insight Partners 继续合作,这一切都要归功于您与我初次接触后留下的良好印象。

奇吉奥克博士 ONYIA 董事总经理, PineCrest 医疗保健有限公司购买理由

- 明智的决策

- 了解市场动态

- 竞争分析

- 客户洞察

- 市场预测

- 风险规避

- 战略规划

- 投资论证

- 识别新兴市场

- 优化营销策略

- 提升运营效率

- 顺应监管趋势