智能传感器市场规模、需求及增长预测(至2034年)

智能传感器市场规模及预测(2021-2034 年)、全球及区域份额、趋势及增长机会分析报告涵盖范围:按技术(MEMS、CMOS 及其他)、类型(温湿度传感器、压力传感器、运动传感器及其他)和终端用户行业(消费电子、汽车、医疗保健、制造、零售及其他)划分

- 状态 : 数据发布

- 报告代码 : TIPRE00010129

- 类别 : 电子和半导体

- 页数 : 150

- 可用报告格式 :

- 最后更新日期 : March 17, 2026

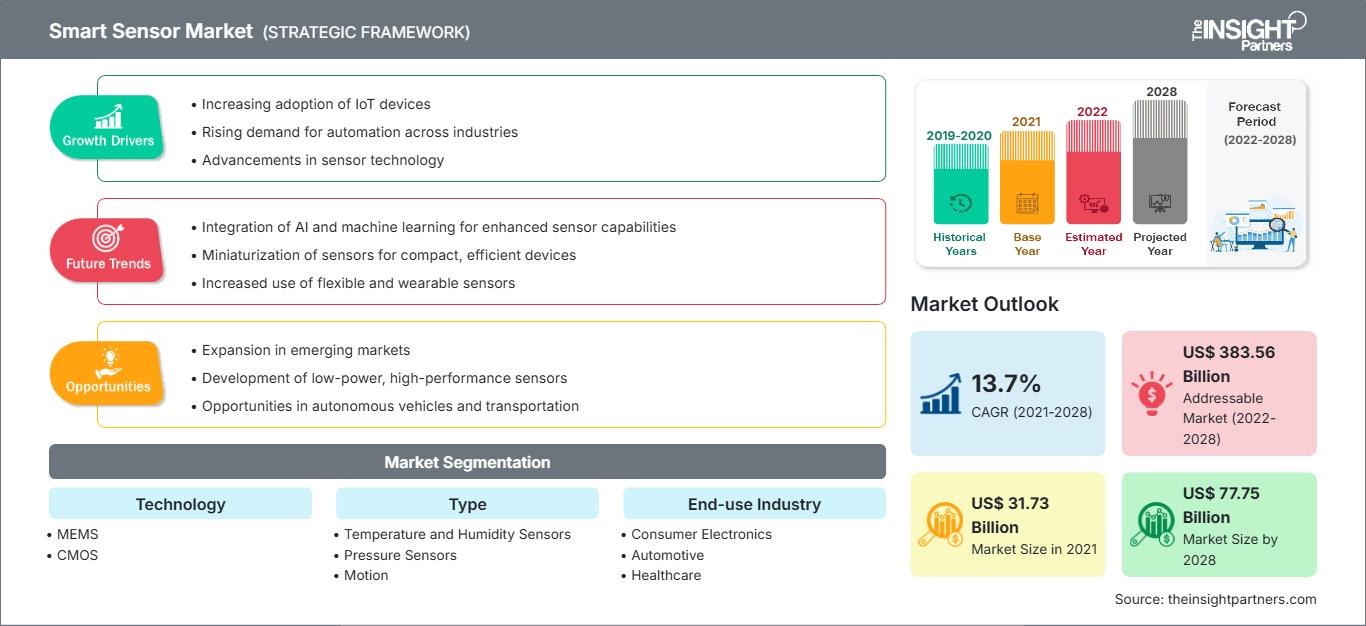

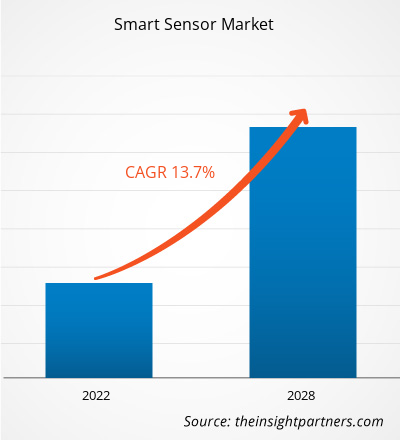

全球智能传感器市场规模预计将从2025年的527.5亿美元增长至2034年的1482.2亿美元。预计在2026年至2034年的预测期内,该市场将以12.66%的复合年增长率增长。

关键市场动态包括物联网的快速普及、工业4.0推动的工业自动化需求增长,以及人工智能和机器学习在边缘端的融合。此外,5G技术的全球推广、自动驾驶汽车和电动汽车的日益普及,以及智慧城市计划在各大城市中心的扩展,预计也将推动市场发展。

智能传感器市场分析

智能传感器市场分析揭示了从被动式硬件到能够自主决策的预测型系统的根本性转变。市场报告重点关注物理人工智能的兴起,这类传感器不仅能够收集数据,还能实时解读物理环境,从而支持机器人技术和数字医疗。采购策略日益注重提升SWaP-C(尺寸、重量、功耗和成本)性能,以满足扩展现实(XR)硬件和可穿戴医疗设备的微型化需求。氢能经济领域涌现出战略机遇,新能源基础设施的泄漏检测和安全保障需要专用传感器。分析还指出,尽管市场前景乐观,但由于缺乏标准化以及大规模工业物联网部署所需的高额初始投资,市场扩张受到一定限制。

智能传感器市场概览

智能传感器已成为现代数字孪生生态系统的基石,使物理资产的虚拟副本能够以高保真度运行。智能传感器强调多模态集成,单个芯片即可集成压力、温度和运动传感功能,从而减少芯片面积和能耗。无论是老牌半导体企业还是创新型初创公司,都在利用硅光子学和印刷电子技术,为智能包装和大面积环境监测开发柔性传感器。北美地区对远程患者监护的需求不断增长,以及亚太地区的快速城市化进程,使得智能传感器成为公共卫生和城市效率提升的关键工具。在美国,绿色建筑应用也呈现激增趋势,传感器能够优化暖通空调系统,以满足全球严格的可持续发展要求,并减少城市能源浪费。

根据您的需求定制此报告

获取免费定制服务智能传感器市场:战略洞察

-

获取本报告的主要市场趋势。这份免费样品将包含数据分析,内容涵盖市场趋势、估算和预测等。

智能传感器市场驱动因素和机遇

市场驱动因素:

- 物联网和工业 4.0 的扩展:智能工厂和互联环境中持续监控的必要性是传感器部署的主要驱动力。

- 更严格的汽车安全法规:全球对高级驾驶辅助系统和乘员监控的强制性要求,推动了对雷达、激光雷达和图像传感器的旺盛需求。

- 小型化和能效方面的进步:半导体制造技术的创新使得智能传感器体积更小、成本更低,从而能够应用于大众消费电子产品。

市场机遇:

- 边缘人工智能集成:开发具有片上机器学习功能的传感器为机器人和自主无人机提供了巨大的机遇。

- 智能能源和可持续发展领域的增长:对环境目标的日益关注为智能电网中的传感器、泄漏检测和节能建筑管理创造了机会。

- 拓展新兴医疗保健领域:传感器制造商与医疗设备供应商之间的战略合作可以促进进入高利润的远程病人监护市场。

智能传感器市场报告细分分析

智能传感器市场份额按不同细分市场进行分析,以便更清晰地了解其结构、增长潜力和新兴趋势。以下是行业报告中常用的标准细分方法:

按技术分类:

- MEMS:作为主流技术领域,因其尺寸小巧、成本低廉、可靠性高,被广泛应用于汽车和消费电子领域。

- CMOS:一个快速增长的领域,对于智能手机和安防系统中的图像传感和高速数据处理尤为重要。

- 其他:包括光学光谱学、纳米机电系统和量子传感等新兴技术,用于专门的工业和科学用途。

按类型:

- 温度和湿度传感器:对气候控制、冷链物流和工业过程监控至关重要。

- 压力传感器:最大的收入来源,对汽车安全系统、航空航天和医疗呼吸机至关重要。

- 运动传感器:由于可穿戴设备、游戏机和手势控制界面的普及,运动传感器正在迅速发展。

- 其他:涵盖各种传感器,包括用于各种垂直应用的图像传感器、流量传感器、气体传感器和生物传感器。

按最终用途行业划分:

- 消费电子产品:仍然是销量的主要驱动力,受益于智能手机和家庭自动化设备的不断更新换代。

- 汽车行业:增长最快的细分市场,这主要得益于汽车电气化和自动驾驶技术的进步。

- 医疗保健:专注于可穿戴健康监测器和先进诊断设备等高价值应用。

- 制造业:以工业 4.0 计划、预测性维护和机器人自动化为中心。

- 零售业:利用传感器进行库存管理、智能货架和增强客户分析。

- 其他应用领域:包括航空航天和国防、智能农业和楼宇自动化。

按地理位置:

- 北美

- 欧洲

- 亚太

- 南美洲和中美洲

- 中东和非洲

智能传感器市场报告范围

| 报告属性 | 细节 |

|---|---|

| 2025年市场规模 | 527.5亿美元 |

| 到2034年市场规模 | 1482.2亿美元 |

| 全球复合年增长率(2026-2034 年) | 12.66% |

| 史料 | 2021-2024 |

| 预测期 | 2026-2034 |

| 涵盖的领域 |

通过技术

|

| 覆盖地区和国家 |

北美

|

| 市场领导者和主要公司简介 |

|

智能传感器市场参与者密度:了解其对业务动态的影响

智能传感器市场正快速增长,这主要得益于终端用户需求的不断增长,而终端用户需求的增长又源于消费者偏好的转变、技术的进步以及消费者对产品优势认知的提高。随着需求的增长,企业不断拓展产品和服务,持续创新以满足消费者需求,并把握新兴趋势,这些都进一步推动了市场增长。

智能传感器市场份额地域分析

预计未来几年亚太地区将实现最快增长。南美和中美洲、中东和非洲等新兴市场在工业自动化和智慧城市基础设施方面也蕴藏着许多尚未开发的机遇。

智能传感器市场正经历着显著的全球扩张,从专用工业组件向无处不在的智能系统转型。北美凭借先进的研发能力和数字健康融合,仍然是高价值收入的主要来源;而亚太地区则占据了销量主导地位,是大众市场传感器生产的主要引擎。以下是各地区市场份额和趋势的概述:

1. 北美洲

- 市场份额:凭借成熟的技术生态系统和高额国防开支,占据领先的收入地位。

-

关键驱动因素:

- 高端临床级传感器在远程医疗和远程病人监护领域得到广泛应用。

- 对智能国防和航空航天应用领域进行了大量投资,特别是对自主无人机和导航系统。

- 成熟的智能家居市场,集成暖通空调和安防传感功能已成为标配。

- 趋势:大力转向网络安全强化型传感器以保护关键基础设施,以及人工智能集成可穿戴设备迅速普及。

2. 欧洲

- 市场份额:占据稳固的市场份额,主要得益于德国、法国和英国等汽车和工业中心地带。

-

关键驱动因素:

- 严格的欧洲新车安全评鉴协会(Euro NCAP)安全标准和排放规定正在推动先进的激光雷达和气体传感器的应用。

- 工业 4.0 在制造业中得到高度应用,预测性维护传感器对于提高运营效率至关重要。

- 政府主导的绿色建筑计划需要智能入住和环境传感器。

- 趋势:战略重点是可持续发展即服务,传感器在循环经济和能源中性城市发展中发挥着至关重要的作用。

3. 亚太地区

- 市场份额:增长最快的地区和全球生产中心。

-

关键驱动因素:

- 中国、日本和韩国庞大的消费电子产品制造基地,推动了对MEMS和CMOS传感器的需求。

- 在印度和东南亚开展大规模智慧城市项目,整合城市传感器,用于交通、垃圾和水资源管理。

- 汽车电气化进程迅速,该地区生产的电动汽车 (EV) 传感器产品占全球一半以上。

- 趋势:高度依赖 5G 赋能的智能农业和 B2B 合同,用于全球半导体供应链中的高精度组件。

4. 南美洲和中美洲

- 市场份额:新兴市场,巴西和阿根廷的制造业规模不断扩大。

-

关键驱动因素:

- 利用土壤湿度和养分跟踪智能传感器实现农业实践现代化。

- 汽车组装行业的扩张,创造了对安全传感器的本地化需求。

- 趋势:数字化矿业计划不断发展,利用坚固耐用的智能传感器来提高采矿业的安全性和资产跟踪能力。

5. 中东和非洲

- 市场份额:一个在能源领域根基深厚的新兴市场,正在向正规化的商业物联网转型。

-

关键驱动因素:

- 石油和天然气行业对用于泄漏检测和炼油厂自动化的专用气体和压力传感器有着很高的需求。

- 对智能基础设施进行战略投资,以支持像NEOM这样的未来城市项目。

- 趋势:实施现代海水淡化监测和制冷技术,以提高当地粮食安全和水资源利用效率。

市场密度高,竞争激烈

由于罗伯特·博世、意法半导体和德州仪器等老牌领先企业的存在,市场竞争日益激烈。亚德诺半导体和英飞凌科技等区域专家和细分市场参与者也为多元化且快速扩张的市场格局做出了贡献。这种竞争环境促使供应商通过以下方式实现差异化:

- 高端化和功能性品牌定位通过强调集成处理和连接性,将智能传感器定位为优于传统替代方案。

- 产品多元化如今已不仅仅包括数据收集,企业还提供多传感器模块和软件定义传感平台。

- 垂直整合,即生产商管理从晶圆制造到最终用户软件集成的整个供应链,可确保质量和透明度。

- 先进的MEMS封装和3D堆叠等新型加工技术有助于为下一代智能设备制造高质量的传感器。

机遇与战略举措

- 边缘人工智能战略合作伙伴关系:与人工智能芯片制造商和 NPU(神经处理单元)提供商建立合作关系,将机器学习直接嵌入传感器硬件中,以实现实时预测分析。

- 拓展氢能经济:瞄准氢燃料加注和燃料电池汽车基础设施中对专用泄漏检测和安全传感器的激增需求。

智能传感器市场的主要企业包括:

- Analog Devices公司

- 英飞凌科技公司

- 意法半导体

- TE Connectivity

- 微芯片技术公司

- 恩智浦半导体

- 西门子股份公司

- ABB有限公司

- 罗伯特·博世有限公司

- 霍尼韦尔国际公司

免责声明:以上列出的公司不分先后顺序。

智能传感器市场新闻及最新发展

- 2026年2月,英飞凌科技股份公司(Infineon Technologies AG)将通过收购欧司朗集团(ams OSRAM Group)的非光学模拟/混合信号传感器产品组合,拓展其传感器业务。双方已就此次收购达成一致,收购价格为5.7亿欧元,且不涉及债务和现金。通过这项投资,英飞凌将凭借互补的产品组合,巩固其在汽车和工业传感器领域的领先地位,并拓展其在医疗应用领域的产品范围。

- 2025年11月,意法半导体发布了ISM6HG256X,这是一款小巧的三合一运动传感器,专为数据密集型工业物联网应用而设计,进一步推动了边缘人工智能的发展。这款智能、高精度的惯性测量单元(IMU)传感器巧妙地将低重力(±16g)和高重力(±256g)加速度的同步检测与高性能、高稳定性的陀螺仪集成于一个紧凑的封装内,确保从细微的运动或振动到剧烈的冲击,都能准确检测,避免任何关键事件的发生。

智能传感器市场报告涵盖范围及成果

《智能传感器市场规模及预测(2021-2034)》报告对以下领域进行了详细的市场分析:

- 智能传感器市场规模及预测,涵盖全球、区域和国家层面的所有关键细分市场。

- 智能传感器市场趋势,以及驱动因素、制约因素和关键机遇等市场动态

- 详细的PEST和SWOT分析

- 智能传感器市场分析,涵盖关键市场趋势、全球和区域框架、主要参与者、法规以及近期市场发展动态。

- 智能传感器市场的行业格局和竞争分析,包括市场集中度、热力图分析、主要参与者和最新发展。

- 公司详细概况

Naveen 是一位经验丰富的市场研究和咨询专业人士,在定制项目、联合项目和咨询项目方面拥有超过 9 年的专业经验。他目前担任副总裁,成功管理了项目价值链中的利益相关者,撰写了 100 多份研究报告和 30 多项咨询项目。他的工作涵盖工业和政府项目,为客户的成功和数据驱动的决策做出了重要贡献。

Naveen 拥有卡纳塔克邦 VTU 的电子与通信工程学位,以及马尼帕尔大学的市场营销与运营 MBA 学位。他已担任 IEEE 会员 9 年,积极参与各种会议、技术研讨会,并在分部和地区层面担任志愿者。在此之前,他曾担任 IndustryARC 的助理战略顾问和惠普(惠普全球)的工业服务器顾问。

- 全面的市场规模与预测分析

- 详细的细分市场分析

- 深入的市场动态评估

- 区域及国家级洞察

- 竞争格局与企业对标分析

- 战略性商业情报

客户评价

Insight Partners 的 SCADA 系统市场报告内容全面,对当前趋势和未来预测提供了宝贵的见解。该团队始终高度专业、响应迅速且乐于助人。我们非常满意,强烈推荐他们的服务。

兰·凯德姆 伙伴, Reali Technologies LTD我请求一份关于特定软件市场的报告,团队在几天内就完成了。报告信息非常相关,而且呈现得非常出色。之后,我请求对报告进行一些修改和补充。团队再次迅速响应,不到一周我就收到了最终报告。

让-埃尔韦·詹恩 主席, 未来分析公司我们与 Insight Partners 合作进行了一项重要的市场研究和预测。他们清晰地洞察了机遇和风险,帮助我们制定了计划。他们的研究简单易用,数据可靠,帮助我们做出了明智而自信的决策。我们强烈推荐他们。

皮尤什·纳格帕尔 高级副总裁, 远光全球Insight Partners 凭借其深厚的行业专业知识,提供了富有洞察力、结构合理的市场研究。他们的团队始终专业且响应迅速。用户友好的网站让访问行业报告变得顺畅无阻。我们强烈推荐他们可靠、高质量的研究服务。

安达幸彦 首席执行官, 深蓝有限责任公司这是我第一次从The Insight Partners购买市场报告。起初我有些犹豫,但访问了他们的网站后,我更放心地冒险购买市场报告。我对报告的质量和客户服务非常满意。我对最初的报告有一些疑问和意见,但在与他们的分析师通过电子邮件沟通了几次后,我相信这份报告可以作为我们战略规划流程的参考。非常感谢您抽出宝贵的时间,让这次体验如此愉快。我一定会向其他人推荐你们的服务,当我们需要更多市场数据时,你们将是我的首选。

约翰·铃木 总裁兼首席执行官、董事会董事, BK科技感谢您在处理我关于尼日利亚传染病体外诊断市场信息请求的过程中所展现的支持和专业精神。感谢您的耐心、指导,以及您愿意提供的折扣,最终促成了这笔交易。我期待未来与 Insight Partners 继续合作,这一切都要归功于您与我初次接触后留下的良好印象。

奇吉奥克博士 ONYIA 董事总经理, PineCrest 医疗保健有限公司购买理由

- 明智的决策

- 了解市场动态

- 竞争分析

- 客户洞察

- 市场预测

- 风险规避

- 战略规划

- 投资论证

- 识别新兴市场

- 优化营销策略

- 提升运营效率

- 顺应监管趋势