Marktnachfrage, Marktanteil und Prognose für Arthroskopiegeräte bis 2034

Marktgröße und Prognose für Arthroskopiegeräte (2021–2034), globaler und regionaler Marktanteil, Trends und Wachstumspotenzialanalyse. Berichtsabdeckung: Nach Produkt (Arthroskope, arthroskopische Implantate, Flüssigkeitsmanagementsysteme, Radiofrequenzsysteme (RF), motorbetriebene Shaver-Systeme, Visualisierungssysteme, sonstige arthroskopische Ausrüstung); Anwendung/Arthroskopieart (Kniearthroskopie, Hüftarthroskopie, Schulter- und Ellenbogenarthroskopie, Wirbelsäulenarthroskopie, Fuß- und Sprunggelenksarthroskopie/kleine Gelenke und Sonstige); und Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00020213

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : January 23, 2026

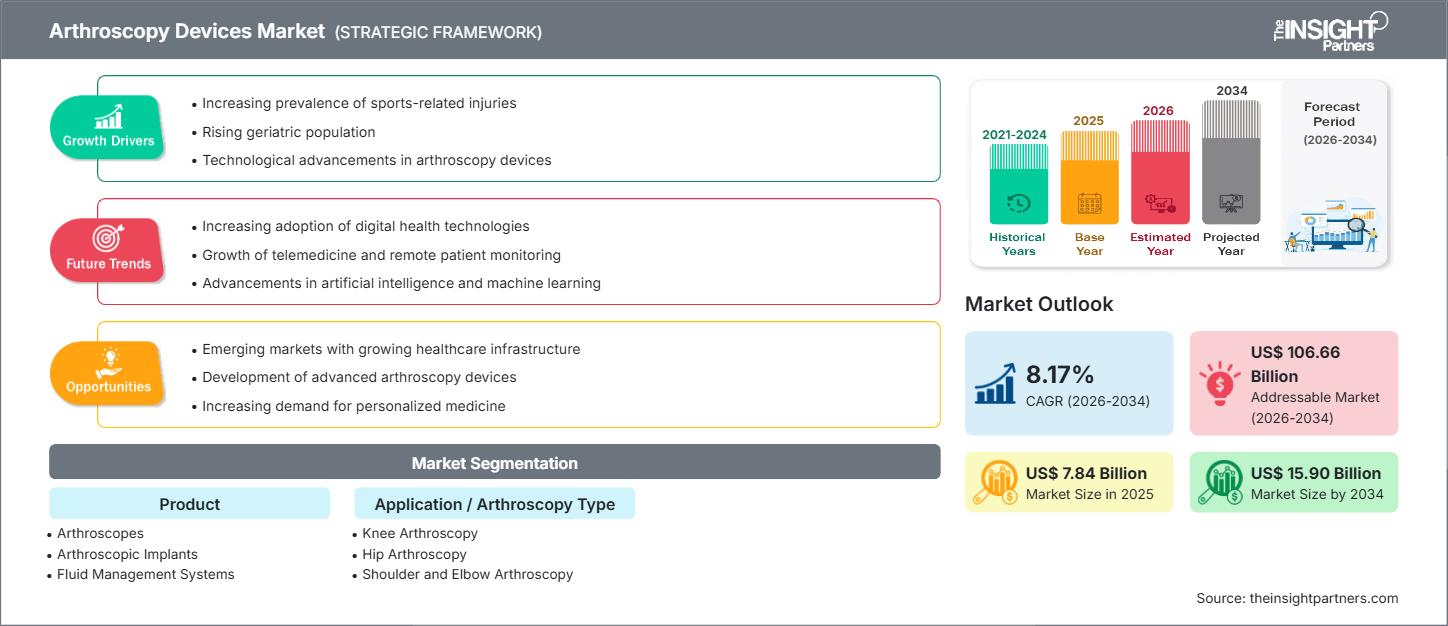

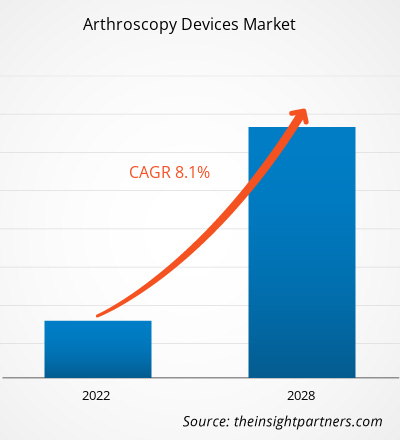

Der Markt für Arthroskopiegeräte hatte im Jahr 2025 einen Wert von 7,84 Milliarden US-Dollar und wird voraussichtlich bis 2034 auf 15,90 Milliarden US-Dollar anwachsen, was einem durchschnittlichen jährlichen Wachstum von 8,17 % von 2026 bis 2034 entspricht.

Marktanalyse für Arthroskopiegeräte

Das Wachstum des Marktes für Arthroskopiegeräte wird durch die zunehmende Verbreitung von Erkrankungen des Bewegungsapparates, die steigende Inzidenz sportbedingter Gelenkverletzungen und die wachsende Präferenz für minimalinvasive chirurgische Eingriffe angetrieben.

Fortschritte in der chirurgischen Technologie, wie verbesserte arthroskopische Visualisierungssysteme, motorisierte Instrumente, Radiofrequenzsysteme und biokompatible Implantate, verbessern die Ergebnisse der Eingriffe, verkürzen die Erholungszeiten und fördern die weltweite Verbreitung arthroskopischer Verfahren.

Darüber hinaus sprechen der Ausbau der orthopädischen Infrastruktur, steigende Gesundheitsausgaben und das Wachstum der älteren Bevölkerung (die anfälliger für Gelenkerkrankungen ist) für eine langfristige Nachfrage nach Arthroskopiegeräten.

Marktübersicht für Arthroskopiegeräte

Arthroskopiegeräte bezeichnen eine breite Palette medizinischer Instrumente und Systeme, die zur Durchführung arthroskopischer Eingriffe eingesetzt werden – minimalinvasive Operationen zur Diagnose und Behandlung von Gelenkerkrankungen. Zu diesen Geräten gehören Arthroskope, Visualisierungssysteme, Flüssigkeitsmanagementsysteme, Radiofrequenzsysteme (RF-Systeme), motorbetriebene Shaver-Systeme, arthroskopische Implantate, Bohrer und Fixierungssysteme sowie weiteres zugehöriges Zubehör.

Mithilfe dieser Instrumente können orthopädische Chirurgen das Innere von Gelenken visualisieren, Reparatureingriffe durchführen (z. B. Bandreparatur, Knorpelwiederherstellung, Meniskusreparatur), die Bewässerung und den Flüssigkeitsfluss steuern und Stabilisierungselemente implantieren, und all dies bei minimalem Gewebetrauma und schnellerer Genesung.

Arthroskopiegeräte spielen eine entscheidende Rolle bei einer Vielzahl von Gelenken, darunter Knie, Hüfte, Schulter, Wirbelsäule, Fuß/Sprunggelenk und kleinere Gelenke, und helfen Ärzten, in Krankenhäusern, ambulanten Operationszentren, orthopädischen Kliniken und Spezialzentren eine effektive und weniger invasive Versorgung zu gewährleisten.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für Arthroskopiegeräte: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese kostenlose Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen für Arthroskopiegeräte

Markttreiber:

- Zunehmende Häufigkeit von Erkrankungen des Bewegungsapparates und Gelenkverletzungen: Die steigende Zahl von Fällen von Arthrose, Bänderrissen, Meniskusschäden und sportbedingten Verletzungen treibt die Nachfrage nach arthroskopischen Eingriffen und entsprechenden Geräten an.

- Präferenz für minimalinvasive Chirurgie (MIS): Chirurgen und Patienten bevorzugen zunehmend die Arthroskopie gegenüber offenen Gelenkoperationen aufgrund von Vorteilen wie kleineren Einschnitten, geringerem Risiko, schnellerer Genesung und kürzerem Krankenhausaufenthalt.

- Technologische Fortschritte bei arthroskopischen Geräten: Innovationen wie hochauflösende Visualisierungssysteme, motorisierte Shaver, fortschrittliches Flüssigkeitsmanagement, bioresorbierbare und metallische Implantate sowie HF-Systeme verbessern die chirurgische Präzision, die Patientenergebnisse und erweitern das Spektrum der behandelbaren Gelenkerkrankungen.

- Wachsende orthopädische Infrastruktur und Investitionen im Gesundheitswesen: Der Ausbau von Krankenhäusern, ambulanten Operationszentren und orthopädischen Fachkliniken, insbesondere in Schwellenländern, erhöht die Zugänglichkeit zu arthroskopischen Eingriffen.

Gelegenheiten:

- Expansion in Schwellenländern: Regionen wie der asiatisch-pazifische Raum (einschließlich Länder wie Indien und China) weisen ein starkes Wachstumspotenzial auf, bedingt durch steigende Investitionen im Gesundheitswesen, ein wachsendes Bewusstsein für minimalinvasive Verfahren, zunehmende Sportverletzungen bei jüngeren Bevölkerungsgruppen und eine wachsende ältere Bevölkerung, die anfällig für Gelenkerkrankungen ist.

- Produktinnovation und Differenzierung: Die Entwicklung von Implantaten der nächsten Generation, verbesserten Visualisierungssystemen, tragbaren Flüssigkeitsmanagementgeräten und fortschrittlichen HF-/motorisierten Werkzeugen ermöglicht es Geräteherstellern, Mehrwertlösungen anzubieten und potenziell einen größeren Marktanteil zu gewinnen.

- Wachstum ambulanter Operationszentren (ASCs) und minimalinvasiver ambulanter Eingriffe: Mit der weltweiten Expansion von ASCs dürfte auch die Nachfrage nach Arthroskopiegeräten, die für den ambulanten Bereich optimiert sind (kompakte, effiziente, kostengünstigere Systeme), steigen.

- Steigende Nachfrage nach Gelenkreparatur und Rehabilitation aufgrund der alternden Bevölkerung: Der weltweite Anstieg der Zahl älterer Menschen, die anfällig für Arthrose und degenerative Gelenkerkrankungen sind, steigert die langfristige Nachfrage nach arthroskopischen Geräten und Eingriffen.

Markt für Arthroskopiegeräte, Segmentierungsanalyse

Der Markt wird üblicherweise anhand mehrerer Dimensionen segmentiert, wie folgt:

Nach Produkt:

- Arthroskope

- Arthroskopische Implantate

- Fluidmanagementsysteme

- Hochfrequenzsysteme (HF)

- Elektrische Rasiersysteme

- Visualisierungssysteme

- Weitere arthroskopische Geräte

Nach Anwendungsgebiet / Arthroskopieart:

- Kniearthroskopie

- Hüftarthroskopie

- Schulter- und Ellenbogenarthroskopie

- Wirbelsäulenarthroskopie

- Fuß- und Sprunggelenksarthroskopie / Kleine Gelenke und andere

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Naher Osten und Afrika

- Süd- und Mittelamerika / Lateinamerika

Markt für Arthroskopiegeräte – Regionale Einblicke

Die regionalen Trends und Einflussfaktoren auf den Markt für Arthroskopiegeräte im gesamten Prognosezeitraum wurden von den Analysten von The Insight Partners eingehend erläutert. Dieser Abschnitt behandelt außerdem die Marktsegmente und die geografische Verteilung des Marktes für Arthroskopiegeräte in Nordamerika, Europa, Asien-Pazifik, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika.

Berichtsumfang zum Markt für Arthroskopiegeräte

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 7,84 Milliarden US-Dollar |

| Marktgröße bis 2034 | 15,90 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 8,17 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nebenprodukt

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte der Akteure im Bereich Arthroskopiegeräte: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Arthroskopiegeräte wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile der Produkte. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen für die Bedürfnisse der Verbraucher und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

- Verschaffen Sie sich einen Überblick über die wichtigsten Akteure auf dem Markt für Arthroskopiegeräte.

Marktanteilsanalyse für Arthroskopiegeräte nach Regionen

- Nordamerika hält derzeit einen führenden Anteil am Markt für Arthroskopiegeräte, was durch eine fortschrittliche Gesundheitsinfrastruktur, eine hohe Inanspruchnahme minimalinvasiver orthopädischer Eingriffe, eine große ältere und sportaktive Bevölkerung sowie günstige Erstattungspolitiken begünstigt wird.

- Europa bleibt aufgrund der zunehmenden Häufigkeit von Arthrose und degenerativen Gelenkerkrankungen, gut etablierter Gesundheitssysteme und der steigenden Nachfrage nach minimalinvasiver Gelenkreparatur ein Schlüsselmarkt.

- Im asiatisch-pazifischen Raum wird im Prognosezeitraum voraussichtlich das schnellste Wachstum erwartet, getrieben durch den Ausbau der orthopädischen Infrastruktur, steigende verfügbare Einkommen, ein zunehmendes Bewusstsein für minimalinvasive Eingriffe, das Wachstum des Medizintourismus und eine wachsende Zahl von Gelenkverletzungen sowohl bei älteren als auch bei jüngeren sportaktiven Bevölkerungsgruppen.

- Der Nahe Osten und Afrika sowie Lateinamerika stellen aufstrebende Märkte dar, in denen der zunehmende Zugang zur Gesundheitsversorgung, Investitionen in die medizinische Infrastruktur und die steigende Nachfrage nach erschwinglichen Gelenkreparaturverfahren erhebliche Chancen für eine Ausweitung der Anwendung von Arthroskopiegeräten bieten.

Markt für Arthroskopiegeräte, Wettbewerbsumfeld und Hauptakteure

Der globale Markt für Arthroskopiegeräte ist durch eine Mischung aus etablierten multinationalen Medizintechnikherstellern und spezialisierten Anbietern orthopädischer Geräte gekennzeichnet. Führende Anbieter konkurrieren häufig über technologische Innovationen, ein breites Produktportfolio (Implantate, Instrumente, Visualisierungs- und Flüssigkeitssysteme), Qualität und globale Vertriebsreichweite.

Frühere Berichte von The Insight Partners identifizierten eine Segmentierung nach Produkten wie Arthroskopen, Implantaten, Flüssigkeitsmanagementsystemen, Visualisierungssystemen, motorbetriebenen Shavern, HF-Systemen und anderen arthroskopischen Geräten.

Angesichts der steigenden Nachfrage in aufstrebenden Regionen und der weltweit wachsenden Anzahl von Eingriffen verschärft sich der Wettbewerb, da die Unternehmen versuchen, sich durch fortschrittliche Technologien (z. B. hochauflösende Visualisierung, minimalinvasive Instrumente, biokompatible Implantate), kosteneffiziente Lösungen und geografische Marktdurchdringung zu differenzieren.

Die wichtigsten Akteure des Marktes sind:

- Arthrex, Inc.

- CONMED Corporation

- Johnson and Johnson Services, Inc.

- KARL STORZ SE & Co. KG

- Medtronic

- Richard Wolf GmbH.

- Smith & Nephew

- Stryker Corporation

- Zimmer Biomet

Weitere Spieler, die im Rahmen der Recherche analysiert wurden:

- United Orthopedic Corporation

- Sklar Chirurgische Instrumente

- Cannuflow Inc.

- Parcus Medical

- Bioventus LLC

- Wright Medical Group NV

- Orthopädisches Implantatunternehmen (OIC)

- GPC Medical Ltd.

- Hofer GmbH

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- B. Braun Melsungen AG

Marktneuigkeiten und aktuelle Entwicklungen im Bereich Arthroskopiegeräte

- Stryker hat eine verbesserte Arthroskopie-Visualisierungsplattform vorgestellt, die über eine optimierte 4K-Bildgebung und eine verbesserte Weichteildifferenzierung verfügt, um die Präzision bei minimalinvasiven Eingriffen zu unterstützen.

- Arthrex erweiterte sein Portfolio um neue bioresorbierbare Nahtanker, die die Knochenintegration fördern und Komplikationen im Zusammenhang mit Metallimplantaten reduzieren sollen.

- Smith+Nephew hat eine digital integrierte Sportmedizin-Plattform eingeführt, die intelligente Arthroskopie-Instrumente mit chirurgischen Planungswerkzeugen verbindet, um die Effizienz der Arbeitsabläufe zu verbessern.

- ConMed erhielt die behördliche Zulassung für ein motorbetriebenes Resektionssystem der nächsten Generation, das mit einer Drehmomentmesstechnologie zur Verbesserung der Schnittkontrolle und der chirurgischen Genauigkeit ausgestattet ist.

- Karl Storz brachte eine KI-gestützte Bildoptimierungssoftware für Arthroskopietürme auf den Markt, die Anpassungen von Beleuchtung und Kontrast automatisiert, um die Echtzeit-Visualisierung zu verbessern.

Marktbericht für Arthroskopiegeräte: Abdeckung und Ergebnisse

Der Bericht „Markt für Arthroskopieverfahren und -produkte (2021–2034)“ von The Insight Partners bietet eine umfassende und strukturierte Analyse, die Folgendes beinhaltet:

- Marktgröße und Prognose (USD) auf globaler, regionaler und Länderebene für alle wichtigen Segmente (Produkt, Anwendung, Endnutzer, Geografie).

- Marktdynamik: Detaillierte Untersuchung der Triebkräfte, Hemmnisse, Chancen und aufkommenden Trends im Bereich der Arthroskopiegeräte.

- Wettbewerbsumfeld: Profilierung der wichtigsten Hersteller, Analyse der Marktkonzentration, Technologie-Benchmarking und strategische Einblicke.

- Segmentierungsbasierte Detailanalyse: Segmentierung nach Produkttypen, Anwendungs-/Arthroskopiearten, Endnutzerkategorien und regionalen Märkten.

- Prognoseszenarien: wahrscheinliche, optimistische und konservative Nachfrageprognosen für den Prognosezeitraum (bis 2031), die es den Beteiligten ermöglichen, kurz- und langfristige Chancen zu bewerten.

- Unterstützende Analysen: Wertschöpfungskette, regulatorisches Umfeld, Angebots- und Nachfrageübersicht sowie Wachstumsförderer und -hemmnisse.

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends