Marktbericht für Chips für künstliche Intelligenz 2027 nach Segmenten, Geografie, Dynamik, jüngsten Entwicklungen und strategischen Erkenntnissen

Markt für Chips für künstliche Intelligenz bis 2027 – Globale Analyse und Prognosen nach Segment (Rechenzentrum, Edge); Typ (CPU, GPU, ASIC, FPGA und andere); und Branchenvertikale (BFSI, Einzelhandel, IT und Telekommunikation, Automobil und Transport, Gesundheitswesen, Medien und Unterhaltung und andere)

- Status : Veröffentlicht

- Berichtscode : TIPEL00002486

- Kategorie : Elektronik und Halbleiter

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 13, 2024

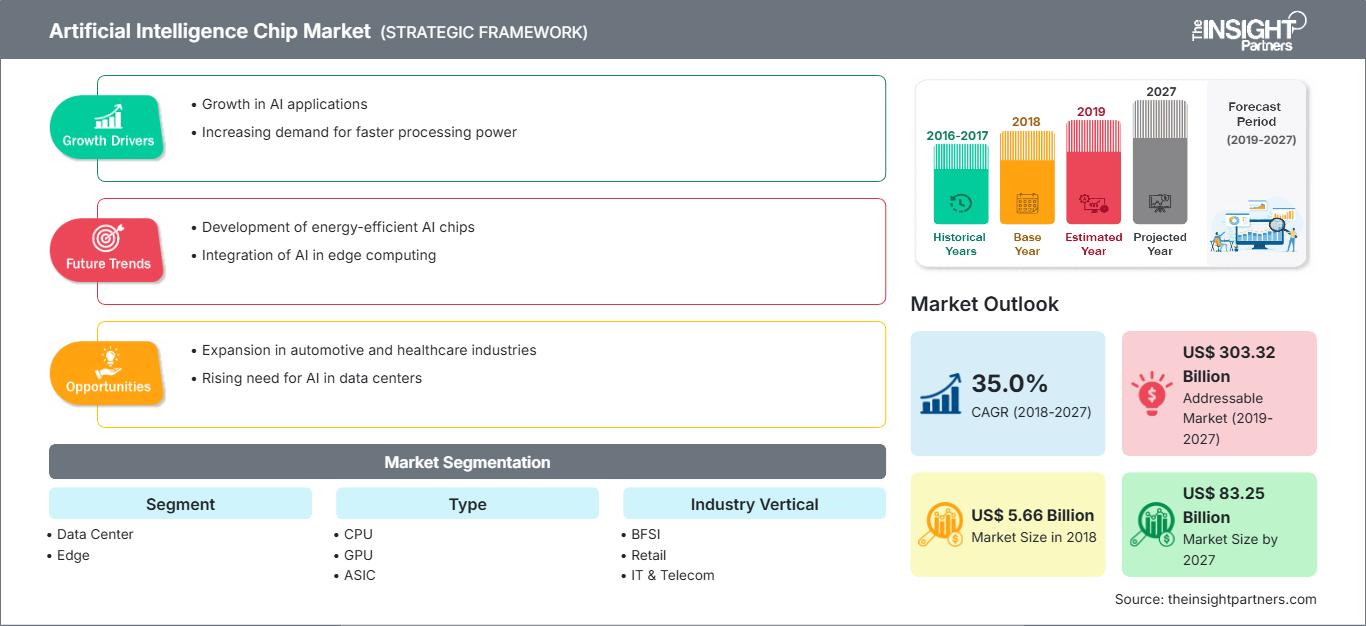

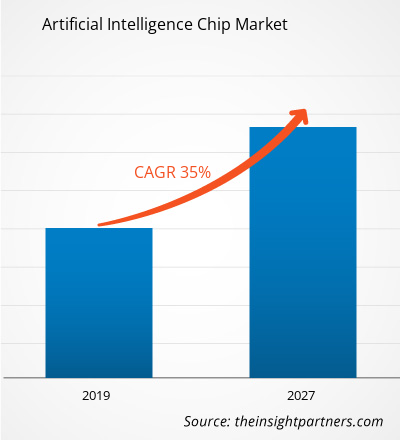

Der Markt für Chips für künstliche Intelligenz wurde 2018 auf 5.658,1 Millionen US-Dollar geschätzt und soll bis 2027 83.252,7 Millionen US-Dollar erreichen; für den Zeitraum 2019–2027 wird ein CAGR-Wachstum von 35,0 % erwartet.

Dank der Verfügbarkeit enormer Datenmengen und der enormen Skalierbarkeit cloudbasierter Rechenleistung hat sich künstliche Intelligenz in den letzten Jahren branchenübergreifend zu einem massiven Trend entwickelt. In der heutigen digitalen Welt sind Informationen der Schlüssel zum Erfolg und nachhaltigen Wachstum von Unternehmen. Die meisten Branchen, insbesondere der Dienstleistungssektor, sind stark auf Analysen angewiesen, um nützliche Geschäftseinblicke zu gewinnen und auf dem Markt wettbewerbsfähig zu bleiben. Unternehmen automatisieren kontinuierlich ihre Geschäftsprozesse, die früher entweder programmgesteuert oder manuell durchgeführt wurden. Mit der Weiterentwicklung von KI-Chips und der Einführung anwendungsspezifischer, kundenspezifischer Chips sind Unternehmen nun in der Lage, Echtzeitanalysen zu sammeln und Daten in umsetzbare Erkenntnisse umzuwandeln. Auf dem Markt für Chips für künstliche Intelligenz gibt es zahlreiche Anwendungsfälle für KI, die in verschiedenen Branchen erfolgreich implementiert werden.

Zu den wichtigsten Anwendungen der künstlichen Intelligenz, für die KI-Chips verwendet werden, gehören Maschinelles Lernen (ML), Verarbeitung natürlicher Sprache (NLP), Expertensysteme, Automatische Spracherkennung, KI-Planung und Computer Vision.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Chips zur künstlichen Intelligenz: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Künstliche Intelligenz und ihre Anwendungen wie maschinelles Lernen und Deep Learning haben in den letzten Jahren enorm zugenommen. KI wird in zahlreichen Bereichen umfassend eingesetzt, von Cloud-Computing-Anwendungen bis hin zu digitalen Assistenten und selbstfahrenden/autonomen Fahrzeugen. Angesichts der ständig zunehmenden Anwendungsfälle von KI und der sich entwickelnden Marktlandschaft sind Fortschritte bei den aktuellen Chips unverzichtbar geworden. KI wird hauptsächlich im Schulungsmarkt für Rechenzentren eingesetzt, wo NVIDIA Marktführer ist. Die Nachfrage nach anwendungsspezifischen, kundenspezifischen KI-Chips und Inferenz an Edge und in Rechenzentren sind jedoch die am schnellsten wachsenden Segmente im Markt für KI-Chips, und viele neue Startups gründen, um diesen Markt zu erschließen.

Segmenteinblicke

Basierend auf den Segmenten ist der Markt für Chips für künstliche Intelligenz in Rechenzentren/Cloud- und Edge-Anwendungen unterteilt. Rechenzentren hatten 2018 den größten Anteil am globalen Marktanteil. Künstliche Intelligenz-Chips werden derzeit vor allem in Rechenzentren und Cloud-Anwendungen eingesetzt. KI-Chips in Rechenzentren werden sowohl für Trainingszwecke als auch für Inferenzzwecke verwendet. Training ist ein Prozess, bei dem KI-Algorithmen Daten analysieren, lernen und diese Informationen dann nutzen, um auf reale Probleme zu reagieren. Während des Trainingsprozesses analysieren KI-Algorithmen riesige Datenmengen. Um Entwicklern dabei zu helfen, ihre KI-Technologie-Entwicklungsprozesse zu verkürzen, sollten Chiphersteller sich nicht nur auf die Verbesserung der Prozessorleistung konzentrieren, sondern ein komplettes Ökosystem bereitstellen, das Hardware, Frameworks und andere unterstützende Tools umfasst.

Einblicke in Typen

Basierend auf dem Typ ist der Markt für Chips für künstliche Intelligenz in CPU, ASIC, GPU, FPGA und andere unterteilt. Das GPU-Typsegment hatte 2018 den größten Anteil am globalen Marktanteil. Derzeit sind Grafikprozessoren (GPUs) in Anwendungen für künstliche Intelligenz die am häufigsten verwendete Hardware. Die hohe Parallelität und Speicherbandbreite von GPUs machen sie zur besten Option für Machine- und Deep-Learning-Anwendungen, insbesondere im Training. GPUs wurden ursprünglich verwendet, um eine große Anzahl von Multiplikations- und Additionsberechnungen beim Grafik-Rendering zu beschleunigen. Mit der steigenden Nachfrage nach Hochleistungsgrafiken stieg auch die Nachfrage nach leistungsstarken GPUs.

Die Marktteilnehmer konzentrieren sich auf Produktinnovationen und -entwicklungen, indem sie fortschrittliche Technologien und Funktionen in ihre Produkte integrieren, um mit der Konkurrenz mithalten zu können.

- Im März 2019 ging AMD eine Partnerschaft mit ScaleMP ein, die es AMD-Server-OEMs ermöglicht, Systeme mit 4, 8 und bis zu 128 Prozessorsockeln, bis zu 8.192 CPUs und 256 Terabyte gemeinsam genutztem Speicher zu erstellen.

- Im Juli 2018 stellte Google winzige neue KI-Chips, Edge TPU, für maschinelles Lernen auf dem Gerät vor. Edge TPU ist ein von Google speziell entwickelter anwendungsspezifischer integrierter Schaltkreis (ASIC), der für die Ausführung von KI am Edge konzipiert ist. Es bietet hohe Leistung bei geringem Platzbedarf und geringem Stromverbrauch und ermöglicht den Einsatz hochpräziser KI am Rand.

Chip für künstliche Intelligenz

Regionale Einblicke in den Markt für Chips für künstliche IntelligenzDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für KI-Chips im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Verteilung von KI-Chips in Nordamerika, Europa, dem asiatisch-pazifischen Raum, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika erörtert.

Umfang des Marktberichts zu Chips für künstliche Intelligenz

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2018 | US$ 5.66 Billion |

| Marktgröße nach 2027 | US$ 83.25 Billion |

| Globale CAGR (2018 - 2027) | 35.0% |

| Historische Daten | 2016-2017 |

| Prognosezeitraum | 2019-2027 |

| Abgedeckte Segmente |

By Segment

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer für Chips für künstliche Intelligenz: Verständnis ihrer Auswirkungen auf die Geschäftsdynamik

Der Markt für Chips für künstliche Intelligenz wächst rasant. Die steigende Nachfrage der Endnutzer ist auf Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile zurückzuführen. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für Chips zur künstlichen Intelligenz Übersicht der wichtigsten Akteure

- Rechenzentrum

- Edge

Markt für Chips für künstliche Intelligenz – nach Typ

- CPU

- GPU

- ASIC

- FPGA

- Sonstige

Markt für Chips für künstliche Intelligenz – nach Branchen

- BFSI

- Einzelhandel

- IT & Telekommunikation

- Automobil & Transport

- Gesundheitswesen

- Medien & Unterhaltung

- Sonstige

Markt für künstliche Intelligenz – nach Geografie

-

Nordamerika

- USA

- Kanada

- Mexiko

-

Europa

- Frankreich

- Deutschland

- Italien

- Russland

- Großbritannien

- Restliches Europa

-

Asien-Pazifik (APAC)

- Südkorea

- China

- Indien

- Australien

- Japan

- Restlicher Asien-Pazifik-Raum

-

Naher Osten & Afrika (MEA)

- Saudi-Arabien

- VAE

- Südafrika

- Rest von MEA

-

Südamerika (SAM)

- Brasilien

- Argentinien

- Rest von Südamerika (SAM)

Markt für Chips für künstliche Intelligenz – Firmenprofile

- Advanced Micro Devices, Inc.

- Google, Inc.

- Huawei Technologies Co., Ltd

- IBM

- Intel Corporation

- Micron Technology, Inc.

- NVIDIA Corporation

- QUALCOMM Incorporated

- Samsung Electronics Co., Ltd.

- Xilinx, Inc.

Naveen ist ein erfahrener Marktforschungs- und Beratungsexperte mit über 9 Jahren Erfahrung in kundenspezifischen, syndizierten und Beratungsprojekten. In seiner aktuellen Funktion als Associate Vice President hat er erfolgreich Stakeholder entlang der gesamten Projektwertschöpfungskette gemanagt und ist Autor von über 100 Forschungsberichten und über 30 Beratungsaufträgen. Seine Arbeit erstreckt sich auf Industrie- und Regierungsprojekte und trägt maßgeblich zum Kundenerfolg und zur datengesteuerten Entscheidungsfindung bei.

Naveen hat einen Ingenieursabschluss in Elektronik und Kommunikation von der VTU, Karnataka, und einen MBA in Marketing und Operations von der Manipal University. Er ist seit 9 Jahren aktives IEEE-Mitglied und nimmt an Konferenzen und technischen Symposien teil und engagiert sich ehrenamtlich auf Sektions- und regionaler Ebene. Vor seiner aktuellen Position arbeitete er als Associate Strategic Consultant bei IndustryARC und als Industrial Server Consultant bei Hewlett Packard (HP Global).

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends