Marktanalyse und Prognose für Bioprozesstechnologie nach Größe, Anteil, Wachstum, Trends 2028

Marktgröße und Prognose für Bioprozesstechnologie bis 2028 – Globale Analyse nach Typ (Bioprozess mit Zellkulturmedien, Bioprozess mit Chromatographie, Verbrauchsmaterialien und Zubehör usw.), Modalität (Einmalgebrauch und Mehrfachgebrauch) und Endbenutzer (akademische und medizinische Einrichtungen, biopharmazeutische Unternehmen, Forschungslabore usw.)

- Status : Veröffentlicht

- Berichtscode : TIPHE100001373

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 194

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 13, 2024

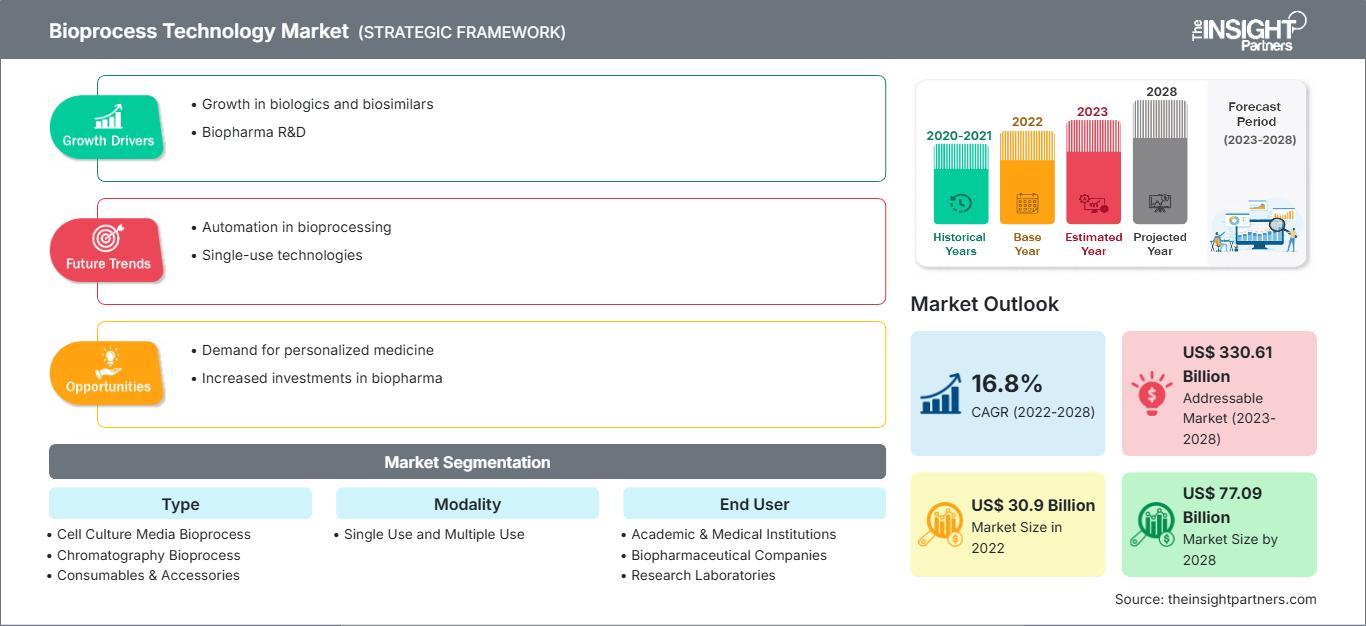

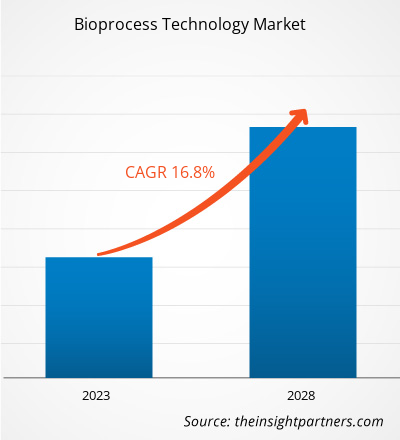

[Forschungsbericht]Der Markt für Bioprozesstechnologie wurde im Jahr 2022 auf 30.897,49 Millionen US-Dollar geschätzt und soll bis 2028 voraussichtlich 77.090,05 Millionen US-Dollar erreichen; von 2023 bis 2028 wird eine durchschnittliche jährliche Wachstumsrate (CAGR) von 16,8 % erwartet.

Sichtweise des Analysten

Die Vorteile der Bioprozesstechnik liegen in der Verwendung von niedrigerem Druck, niedrigeren Temperaturen und günstigeren pH-Werten. Der gesamte Prozess ist erneuerbar. Steigende F&E-Ausgaben für die Einführung neuer Arzneimittelverbindungen und die zunehmende Verbreitung chronischer Krankheiten. Strenge Regulierungsrichtlinien sind die einflussreichsten Faktoren für das starke Wachstum des Marktes für Bioprozesstechnologie. Darüber hinaus bietet die Einführung fortschrittlicher Bioprozesstechnologien lukrative Marktchancen für ein exponentielles Marktwachstum im Prognosezeitraum. Darüber hinaus ist das Aufkommen der automatisierten Echtzeit-Durchflusszytometrie (ART-FCM) ein zukünftiger Trend für das Marktwachstum zwischen 2023 und 2028. Laut der im Bericht dargestellten Segmentierung nach Typ entfällt der größte Anteil auf Zellkulturmedien-Bioprozesse; ebenso wird für Chromatographie-Bioprozesse im Prognosezeitraum (2023–2028) die höchste durchschnittliche jährliche Wachstumsrate (CAGR) erwartet. Darüber hinaus wird das Einwegsegment im Prognosezeitraum nach Modalität einen beträchtlichen Anteil an der Bioprozesstechnologie ausmachen. Hinsichtlich Endverbraucher wird das Segment der biopharmazeutischen Unternehmen das Marktwachstum für Bioprozesstechnologie im Prognosezeitraum dominieren.

Bioprozesstechnologie ist ein wichtiger Teil der Biotechnologie, der sich mit Prozessen befasst, bei denen lebende Materie oder deren Bestandteile mit Nährstoffen kombiniert werden, um Spezialchemikalien, Reagenzien und Biotherapeutika herzustellen. Zu den verschiedenen Phasen der Bioprozesstechnologie gehören die Vorbereitung von Substraten und Medien, die Auswahl und Optimierung von Biokatalysatoren, die Massenproduktion, die Weiterverarbeitung, die Aufreinigung und die Endverarbeitung. Bioprozesstechnologie wird in großem Umfang eingesetzt, von Lebensmitteln und Pharmazeutika bis hin zu Kraftstoffen und Chemikalien.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Bioprozesstechnologie: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Markteinblicke

Steigende Ausgaben für Forschung und Entwicklung zur Einführung neuer Arzneimittelverbindungen

Pharmaunternehmen investieren enorme Summen in Forschung und Entwicklung, um neue Moleküle mit verbesserter medizinischer und kommerzieller Wirksamkeit für verschiedene therapeutische Anwendungen einzuführen. Im Geschäftsjahr 2019/2020 schafften es 16 Pharmaunternehmen auf die Liste der 50 weltweit größten Unternehmen hinsichtlich ihrer gesamten Forschungs- und Entwicklungsinvestitionen. Novartis, Roche, Johnson & Johnson, Merck & Co, GlaxoSmithKline und Pfizer gehören zu den weltweit 10 größten Unternehmen mit hohen F&E-Investitionen.

F&E-Investitionen der großen Pharmaunternehmen

Unternehmen |

F&E-Investitionen im Jahr 2022 (Millionen US-Dollar) |

F&E-Investitionen im Jahr 2021 (Millionen US-Dollar) |

|

Gilead Sciences Inc |

27.305 |

27.281 |

|

Bristol-Myers Squibb Co |

46.159 |

46.385 |

|

Amgen Inc. |

26.323 |

25.979 |

|

Pfizer |

100.330 |

81.288 |

|

Merck & Co |

59.283 |

48.704 |

|

AbbVie Inc |

58.054 |

56.197 |

Hinweis: Die Währungsumrechnungskurse wurden, wo immer erforderlich, berücksichtigt.

Quelle: Jahresberichte von Unternehmen und Analyse von The Insight Partners

Der Patentablauf von Blockbuster-Molekülen, eine begrenzte Anzahl potenzieller Produkte in der Pipeline und die steigende Nachfrage nach Biologika haben Unternehmen dazu veranlasst, neue Technologien wie Einweg-Bioprozesstechnologien einzusetzen, um einen schnellen und kostengünstigen Durchlaufzeitprozess für Produkte zu ermöglichen. Hersteller von Einwegkomponenten und -systemen produzieren und montieren ihre Produkte typischerweise in Reinräumen, um sicherzustellen, dass sie keine schädlichen Partikel und Endotoxine in einen Bioprozess einbringen. Daher werden hohe Investitionen in Forschung und Entwicklung getätigt, um neue Arzneimittelverbindungen einzuführen und die Entwicklung von Bioprozesstechnologien zu unterstützen; diese Technologien unterstützen neue Bioproduktionskapazitäten und die damit verbundene Interoperabilität von Rohstoffen, Bioreaktoren und Einheitsvorgängen.

Typbasierte Erkenntnisse

Basierend auf dem Typ ist der Markt für Bioprozesstechnologie in Zellkulturmedien-Bioprozess, Chromatographie-Bioprozess, Verbrauchsmaterialien & Zubehör und Sonstiges segmentiert. Das Segment Zellkulturmedien-Bioprozess hielt 2022 den größten Marktanteil an der Bioprozesstechnologie, während für den Chromatographie-Bioprozess im Prognosezeitraum (2023–2028) die höchste durchschnittliche jährliche Wachstumsrate (CAGR) erwartet wird.

Modalitätsbasierte Erkenntnisse

Basierend auf der Modalität ist der globale Markt für Bioprozesstechnologie in Einweg- und Mehrwegprodukte unterteilt. Das Segment der Einwegprodukte hatte 2022 einen größeren Marktanteil in der Bioprozesstechnologie. Das Segment der Mehrfachprodukte soll im Prognosezeitraum eine höhere durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnen.

Endnutzerbasierte Erkenntnisse

In Bezug auf die Endnutzer ist der Markt für Bioprozesstechnologie in akademische und medizinische Einrichtungen, biopharmazeutische Unternehmen, Forschungslabore und andere unterteilt. Das Segment der biopharmazeutischen Unternehmen hatte 2022 den größten Marktanteil, während für akademische und medizinische Einrichtungen im Prognosezeitraum eine höhere CAGR erwartet wird.

Regionale Analyse

Nordamerika dominierte den Markt für Bioprozesstechnologie und verzeichnete den größten Anteil. Das Wachstum des Marktes für Bioprozesstechnologie in dieser Region ist auf die Präsenz großer Akteure zurückzuführen, die innovative Produkte (insbesondere im Zusammenhang mit Bioprozesstechnologie) auf den Markt bringen, auf die zunehmende Produkteinführung in der Region und auf den technologischen Fortschritt in der Bioprozesstechnologie. In Nordamerika verzeichnen die USA den größten Anteil an der Bioprozesstechnologie. Laut einem Bericht der Food and Drug Administration (FDA) leiden in den USA über 30 Millionen Menschen an etwa 7.000 lebensbedrohlichen seltenen Krankheiten, für die es nur wenige Behandlungsmöglichkeiten gibt. Die Entwicklung von Medikamenten, biologischen Präparaten und Geräten zur Behandlung seltener Krankheiten ist aufgrund mangelnder Kenntnisse über ihre Entstehungsgeschichte und der Schwierigkeiten bei der Durchführung klinischer Studien eine Herausforderung. Daher stellt die Entwicklung von Bioprozesstechnologien wie Gen- und Zelltherapien (CGTs) und Spezialpharmazeutika einen radikalen Wandel in der Behandlung seltener Krankheiten dar. Beispielsweise haben CGTs im Vergleich zu formulierten Medikamenten zur Behandlung seltener Krankheiten erhebliche gesundheitliche Vorteile gezeigt. In den USA laufen derzeit über 900 Anträge auf Zulassung neuer Prüfpräparate (IND) für Gentherapieprodukte. Darüber hinaus werden jährlich 10 bis 20 Gentherapien von der FDA zugelassen. Im August 2022 genehmigte die FDA zudem „Zynteglo (Betibeglogene Autotemcel)“ von Bluebird Bio. Es handelte sich um die teuerste Einzelanwendungszulassung eines Medikaments in den USA zur Behandlung einer seltenen neurologischen Erkrankung – der zerebralen Adrenoleukodystrophie (CALD).

Ebenso wird die Region Asien-Pazifik die höchste durchschnittliche jährliche Wachstumsrate (CAGR) im Markt für Bioprozesstechnologie aufweisen. Innerhalb der Region Asien-Pazifik wird China einen beträchtlichen Marktanteil im Markt für Bioprozesstechnologie halten. Laut dem Bericht „BioPlan Associates Top 1000 Biofacility Index and Biomanufacturers Database“ ist die globale Bioprozesskapazität seit dem letzten Jahrzehnt um durchschnittlich 12 % gestiegen. China ist als globaler Teilnehmer auf den Märkten für niedermolekulare und großmolekulare Medikamente gut positioniert und belegt weltweit den zweiten bzw. dritten Platz. Außerdem sind in China aufgrund der chinesischen Basis von Auftragsentwicklungs- und -herstellungsorganisationen (CDMOs) mehrere Entwickler von Zell- und Gentherapien ansässig, die etwa 25 % der Bioproduktionskapazität des Landes ausmachen. Daher verfügt China über beträchtliche Kapazitäten zur Bioproduktion, hält sich aber strikt an die globalen GMP-Standards, die Vertrauen in die Sicherheit und Wirksamkeit der Biologika schaffen.

Land |

Bioproduktionsanlage (L) |

Globale Kapazität (%) |

Geschätzte Kapazität CAGR (%) |

|

China |

1,77 Millionen |

10,2 |

15-20 |

Quelle: Globaler Vergleich der Bioproduktionskapazitäten; Daten aus dem BioPlan Associates Top 1000 Biofacility Index und der Biomanufacturers Database (CAGR = durchschnittliche jährliche Wachstumsrate).

Bioprozesstechnologie

Regionale Einblicke in den Markt für BioprozesstechnologieDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für Bioprozesstechnologie im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage in Nordamerika, Europa, dem asiatisch-pazifischen Raum, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika erörtert.

Umfang des Marktberichts zur Bioprozesstechnologie

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2022 | US$ 30.9 Billion |

| Marktgröße nach 2028 | US$ 77.09 Billion |

| Globale CAGR (2022 - 2028) | 16.8% |

| Historische Daten | 2020-2021 |

| Prognosezeitraum | 2023-2028 |

| Abgedeckte Segmente |

By Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktakteure im Bereich Bioprozesstechnologie: Verständnis ihrer Auswirkungen auf die Geschäftsdynamik

Der Markt für Bioprozesstechnologie wächst rasant. Die steigende Nachfrage der Endverbraucher ist auf Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile zurückzuführen. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für Bioprozesstechnologie Übersicht der wichtigsten Akteure

Merck KGaA, Sartorius AG, Thermo Fisher Scientific Inc, Corning Inc, STAMM Biotech, Lonza Group AG, Eppendorf SE, Repligen Corp, Danaher Corp und BioPharma Dynamics Ltd gehören zu den führenden Akteuren im globalen Marktwachstum für Bioprozesstechnologie. Mehrere andere wichtige Marktteilnehmer wurden analysiert, um einen ganzheitlichen Blick auf den Markt und sein Ökosystem zu erhalten. Der Bericht bietet detaillierte Markteinblicke, die den wichtigsten Akteuren helfen, Strategien für ihr Marktwachstum zu entwickeln. Einige Entwicklungen sind nachfolgend aufgeführt:

- Im Juni 2022 ist Merck eine Zusammenarbeit mit Agilent Technologies eingegangen, um prozessanalytische Technologien (PAT) voranzutreiben. PAT, das von globalen Regulierungsbehörden stark gefördert wird, ist ein wichtiger Wegbereiter für Echtzeitfreigabe und Bioprocessing 4.0.

- Im März 2020 brachte Sartorius den Einweg-Bioreaktor BIOSTAT STR Generation 3 und die Automatisierungsplattform BIOBRAIN auf den Markt, um Innovationen vorzustellen, die den Bereich der biopharmazeutischen Prozessentwicklung und -herstellung verändern werden. Biostat STR vereinfacht die Produktion von Biologika.

Unternehmensprofile

- Merck KGaA

- Sartorius AG

- Thermo Fisher Scientific Inc

- Corning Inc

- STAMM Biotech

- Lonza Group AG

- Eppendorf SE

- Repligen Corp

- Danaher Corp

- BioPharma Dynamics Ltd

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends