Marktbericht für verteilte Steuerungssysteme 2030 nach Segmenten, Geografie, Dynamik, jüngsten Entwicklungen und strategischen Erkenntnissen

Marktgröße und Prognose für verteilte Steuerungssysteme (2020–2030), Berichtsabdeckung zu globalen und regionalen Anteilen, Trends und Wachstumschancen: Nach Komponenten (Hardware, Software und Dienstleistungen) und Branchen (Öl und Gas, Stromerzeugung, Chemie, Lebensmittel und Getränke, Pharmazeutik und andere) sowie Geografie

- Status : Veröffentlicht

- Berichtscode : TIPRE00006986

- Kategorie : Elektronik und Halbleiter

- Anzahl der Seiten : 199

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : September 03, 2024

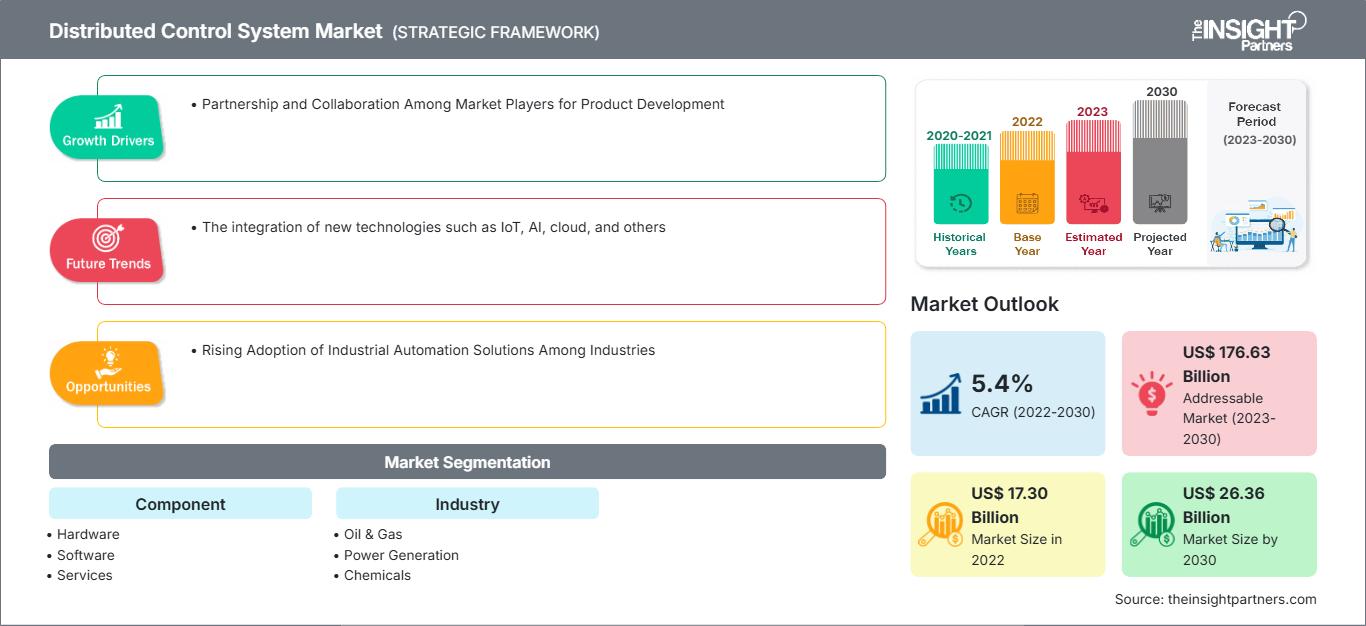

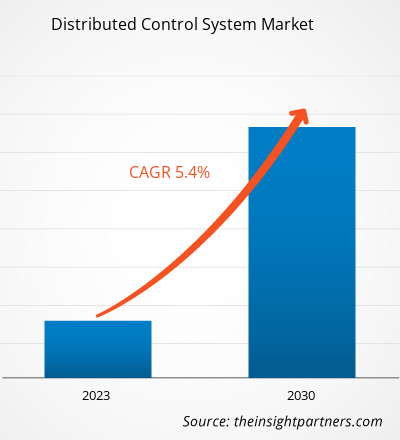

Der Markt für verteilte Steuerungssysteme soll von 17,30 Milliarden US-Dollar im Jahr 2022 auf 26,36 Milliarden US-Dollar im Jahr 2030 anwachsen. Für den Markt wird zwischen 2022 und 2030 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 5,4 % erwartet. Die Integration neuer Technologien wie IoT, KI, Cloud und andere wird voraussichtlich ein wichtiger Markttrend bleiben.

Marktanalyse für verteilte Steuerungssysteme

Die zunehmende Verbreitung industrieller Automatisierungslösungen in der Industrie und der wachsende Strom- und Energiesektor treiben den Markt an. Im Prognosezeitraum wird aufgrund des Baus neuer Produktionsanlagen ein Marktwachstum erwartet. Zudem schaffen Partnerschaften und Kooperationen zwischen Marktteilnehmern bei der Produkt- und Architekturentwicklung im Bereich DCS lukrative Möglichkeiten für den Markt.

Marktübersicht für verteilte Steuerungssysteme

Ein verteiltes Steuerungssystem (DCS) ist ein computergestütztes System, das aus Sensoren, Controllern und zugehörigen Computern besteht, die über eine Anlage verteilt sind. Jedes dieser Elemente erfüllt eine bestimmte Funktion, beispielsweise Datenerfassung, Prozesssteuerung, Datenspeicherung und grafische Darstellung. Die verschiedenen Komponenten kommunizieren über das lokale Netzwerk (LAN) der Anlage, auch Steuerungsnetzwerk genannt, mit einem Zentralrechner.

Das Prozessleitsystem automatisiert Industrieanlagen in kontinuierlichen und Batch-Prozessen und reduziert gleichzeitig die Risiken für Mensch und Umwelt. Die Systeme kommen in zahlreichen Branchen zum Einsatz, darunter im Bergbau, in der chemischen Produktion, im Transport- und Verarbeitungsbereich, in der Stromerzeugung, in der Wasser- und Abwasseraufbereitung sowie in der pharmazeutischen Verarbeitung.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für verteilte Steuerungssysteme: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Markttreiber und -chancen für verteilte Steuerungssysteme

Steigende Verbreitung industrieller Automatisierungslösungen in verschiedenen Branchen begünstigt den Markt

Industrielle Automatisierung wird allgemein als die Verwendung von Hardware und Komponenten zur Automatisierung von Systemen in Industrie- oder Fertigungsumgebungen definiert. Unternehmen starten eine Vielzahl von Programmen, um die Einführung industrieller Automatisierung zu fördern. So kooperierte beispielsweise Rockwell Automation im September 2023 mit BIC, um die digitale Transformation und Effizienz mithilfe des Manufacturing Execution Systems (MES) Plex voranzutreiben. Solche Unternehmensinitiativen werden das Wachstum des Marktes für verteilte Steuerungssysteme vorantreiben. Darüber hinaus verzeichnen die Öl- und Gas-, Petrochemie- und Pharmaindustrie ein rasantes Wachstum. Aufgrund der Existenz technologisch fortschrittlicher Unternehmen und der gestiegenen staatlichen Ausgaben für Forschung und Entwicklung sind die technologischen Fortschritte in diesen Industriezweigen ebenfalls hoch.

Partnerschaften und Zusammenarbeit zwischen Marktteilnehmern bei der Produktentwicklung

Viele Sektoren weltweit sind dramatisch gewachsen. Weltweit gibt es immer mehr Automatisierungsfirmen, die sich auf den Betrieb von IKT-Sektoren spezialisiert haben. So gab beispielsweise Vention, das in Quebec ansässige Unternehmen, das die einzige vollständig integrierte Fertigungsautomatisierungsplattform (MAP) entwickelt hat, im Oktober 2023 eine Investition von 15 Millionen US-Dollar aus dem Fonds de solidarité FTQ bekannt. Vention setzt sein robustes Wachstum mit der Unterstützung seiner Partner fort und verfolgt sein Ziel, die industrielle Automatisierung zu demokratisieren und so die Produktivität und Wettbewerbsfähigkeit von Fertigungsunternehmen zu steigern. Darüber hinaus haben Entdeckungen und Verbesserungen der Unternehmen den Einsatz fortschrittlicher Technologien verstärkt. So erweiterte beispielsweise ANYbotics im August 2023 seine Präsenz in Kanada, indem es MicroWatt Controls als Vertriebspartner auswählte. MicroWatt Controls mit Sitz in Calgary hat den Einsatz von Inspektionsrobotern in den Öl- und Gas-, Chemie-, Energie- und Bergbausektoren des Landes ausgeweitet. Die fortlaufende Entwicklung der Prozessindustrie dürfte die Nachfrage nach verteilten Steuerungssystemen auf dem kanadischen Markt steigern.

Segmentierungsanalyse des Marktberichts für verteilte Steuerungssysteme

Schlüsselsegmente, die zur Ableitung der Marktanalyse für verteilte Steuerungssysteme beigetragen haben, sind Komponenten und Industrie.

- Basierend auf Komponenten ist der Markt für verteilte Steuerungssysteme in Hardware, Software und Dienstleistungen unterteilt. Das Softwaresegment hatte 2022 einen größeren Marktanteil.

- Basierend auf Branchen ist der Markt in Öl & Gas, Stromerzeugung, Chemie, Lebensmittel & Getränke, Pharmazeutika und Sonstige unterteilt. Das Öl- & Gassegment hatte 2022 einen größeren Marktanteil.

Geografische Marktanteilsanalyse für verteilte Steuerungssysteme

Der geografische Umfang des Marktberichts für verteilte Steuerungssysteme ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten & Afrika sowie Süd- & Mittelamerika.

Der Markt in Europa wird im Prognosezeitraum aufgrund der expandierenden Automobilindustrie voraussichtlich wachsen. Die italienische Regierung unterstützt die Automobilindustrie stark. So standen der italienischen Regierung laut Gewerkschaft im Dezember 2023 etwa 6,5 Milliarden US-Dollar zur Unterstützung der Automobilindustrie zur Verfügung. Darüber hinaus einigten sich Fiat-Mutterkonzern Stellantis und die italienische Regierung im Juli 2023 darauf, die jährliche Automobilproduktion in Italien auf eine Million Einheiten zu steigern und damit den Abwärtstrend der letzten Jahre umzukehren. Das Wachstum in diesen Branchen wirkte sich positiv auf die industriellen Steuerungssysteme aus. Daher steigt die Nachfrage nach DCS in der Automobilbranche.

Markt für verteilte Steuerungssysteme

Die Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für verteilte Steuerungssysteme im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage für verteilte Steuerungssysteme in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.Umfang des Marktberichts zu verteilten Steuerungssystemen

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2022 | US$ 17.30 Billion |

| Marktgröße nach 2030 | US$ 26.36 Billion |

| Globale CAGR (2022 - 2030) | 5.4% |

| Historische Daten | 2020-2021 |

| Prognosezeitraum | 2023-2030 |

| Abgedeckte Segmente |

By Komponente

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer für verteilte Steuerungssysteme: Verständnis ihrer Auswirkungen auf die Geschäftsdynamik

Der Markt für Prozessleitsysteme wächst rasant. Die steigende Nachfrage der Endnutzer ist auf Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile zurückzuführen. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für verteilte Steuerungssysteme Übersicht der wichtigsten Akteure

Marktnachrichten und aktuelle Entwicklungen zu verteilten Steuerungssystemen

Der Markt für verteilte Steuerungssysteme wird durch die Erhebung qualitativer und quantitativer Daten aus Primär- und Sekundärforschung bewertet, die wichtige Unternehmenspublikationen, Verbandsdaten und Datenbanken umfasst. Einige der Entwicklungen auf dem Markt für verteilte Steuerungssysteme sind nachfolgend aufgeführt:

- ABB hat die neueste Version des verteilten Steuerungssystems DCS ABB Ability Symphony Plus vorgestellt, um die digitale Transformation in der Stromerzeugungs- und Wasserwirtschaft zu unterstützen. Die neueste Version von Symphony Plus wird die digitale Reise der Kunden verbessern, indem sie eine optimierte und sichere OPC UA1-Konnektivität zum Edge und zur Cloud bietet, ohne wichtige Steuerungs- und Automatisierungsfunktionen zu beeinträchtigen. (Quelle: ABB Ltd, Unternehmenswebsite, Februar 2023)

Bericht zum Markt für verteilte Steuerungssysteme: Abdeckung und Ergebnisse

Der „Markt für verteilte Steuerungssysteme – Größe und Prognose (2020–2030)“ Der Bericht bietet eine detaillierte Analyse des Marktes und deckt die folgenden Bereiche ab:

- Marktgröße und Prognose für verteilte Steuerungssysteme auf globaler, regionaler und Länderebene für alle abgedeckten wichtigen Marktsegmente

- Markttrends für verteilte Steuerungssysteme sowie Marktdynamik wie Treiber, Einschränkungen und wichtige Chancen

- Detaillierte PEST/Porters Five Forces- und SWOT-Analyse

- Marktanalyse für verteilte Steuerungssysteme mit wichtigen Markttrends, globalen und regionalen Rahmenbedingungen, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Branchenlandschafts- und Wettbewerbsanalyse mit Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und aktuellen Entwicklungen für den Markt für verteilte Steuerungssysteme

- Detaillierte Unternehmensprofile

Naveen ist ein erfahrener Marktforschungs- und Beratungsexperte mit über 9 Jahren Erfahrung in kundenspezifischen, syndizierten und Beratungsprojekten. In seiner aktuellen Funktion als Associate Vice President hat er erfolgreich Stakeholder entlang der gesamten Projektwertschöpfungskette gemanagt und ist Autor von über 100 Forschungsberichten und über 30 Beratungsaufträgen. Seine Arbeit erstreckt sich auf Industrie- und Regierungsprojekte und trägt maßgeblich zum Kundenerfolg und zur datengesteuerten Entscheidungsfindung bei.

Naveen hat einen Ingenieursabschluss in Elektronik und Kommunikation von der VTU, Karnataka, und einen MBA in Marketing und Operations von der Manipal University. Er ist seit 9 Jahren aktives IEEE-Mitglied und nimmt an Konferenzen und technischen Symposien teil und engagiert sich ehrenamtlich auf Sektions- und regionaler Ebene. Vor seiner aktuellen Position arbeitete er als Associate Strategic Consultant bei IndustryARC und als Industrial Server Consultant bei Hewlett Packard (HP Global).

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends