Marktanteil, Nachfrage und Wachstum des Marktes für grüne Kohlenstofffasern bis 2034

Marktgröße und Prognose für grüne Kohlenstofffasern (2021 - 2034), globaler und regionaler Marktanteil, Trend- und Wachstumschancenanalyse. Berichtsabdeckung: Nach Typ (zerkleinerte und gefräste recycelte Kohlenstofffasern), Quelle (Automobilschrott, Luft- und Raumfahrtschrott und Sonstige) und Anwendung (Luft- und Raumfahrt, Automobilindustrie, Windenergie, Sportartikel und Sonstige).

- Status : Demnächst

- Berichtscode : TIPRE00029863

- Kategorie : Chemikalien und Materialien

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : March 09, 2026

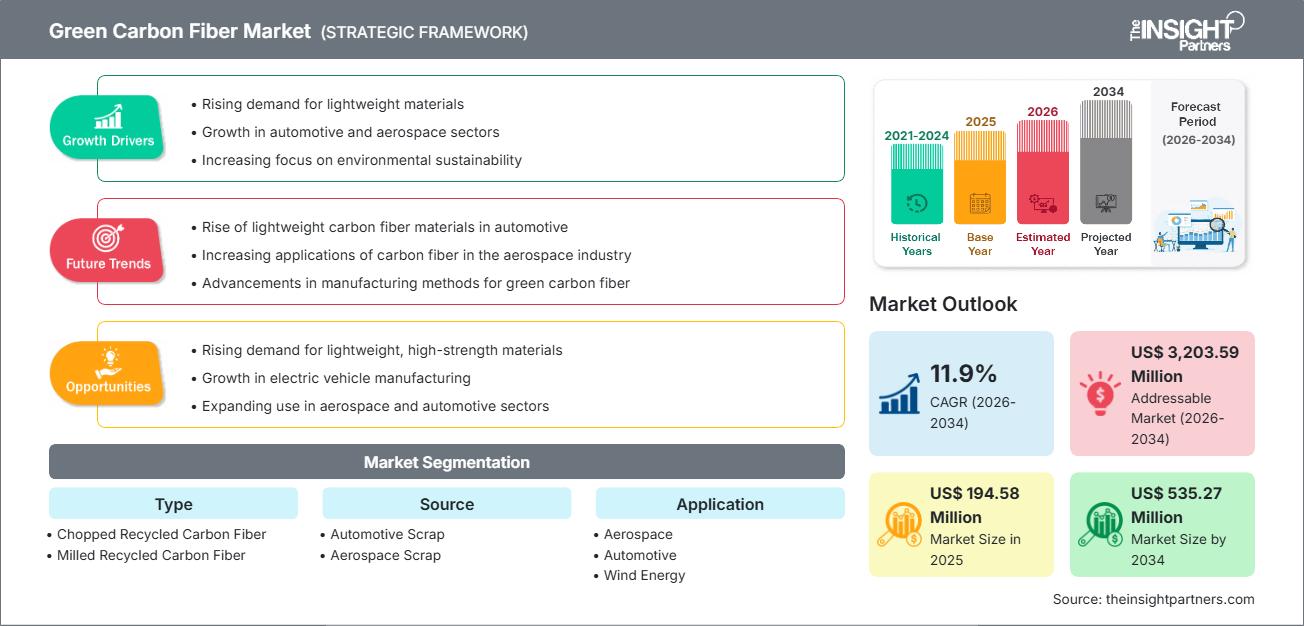

Der globale Markt für grüne Kohlenstofffasern wird bis 2034 voraussichtlich ein Volumen von 535,27 Millionen US-Dollar erreichen, gegenüber 194,58 Millionen US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Prognosezeitraum 2026–2034 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 11,9 % verzeichnen wird.

Zu den wichtigsten Marktdynamiken zählen der weltweit zunehmende Fokus auf die Dekarbonisierung der Industrie, der steigende regulatorische Druck zur Vermeidung von Verbundwerkstoffabfällen auf Deponien sowie die deutliche Verlagerung hin zu Kreislaufwirtschaftsmodellen in der Hochleistungsproduktion. Darüber hinaus dürfte der Markt von der wachsenden Verwendung von Recyclingmaterialien in Massenmarktanwendungen, dem Ausbau spezialisierter Recyclinganlagen im asiatisch-pazifischen Raum und in Europa sowie dem verstärkten Einsatz nachhaltiger Fasern in Großprojekten wie Offshore-Windparks und Elektrofahrzeugflotten der nächsten Generation profitieren.

Marktanalyse für grüne Kohlenstofffasern

Die Marktanalyse für grüne Kohlenstofffasern zeigt eine Verlagerung hin zu hochwertigen Sekundärmaterialien, da Hersteller der Nachhaltigkeit über den gesamten Lebenszyklus und der Kosteneffizienz Priorität einräumen. Beschaffungstrends deuten auf eine Aufspaltung des Marktes in hochwertige, aus der Luft- und Raumfahrt recycelte Fasern und die Verarbeitung großer Mengen von Altfasern aus der Automobilindustrie hin. Strategische Chancen ergeben sich in der thermoplastischen Compoundierung und im Formpressen, wo die mechanischen Eigenschaften recycelter Kohlenstofffasern einen klaren Wettbewerbsvorteil gegenüber herkömmlichen Glasfasern oder Neuware bieten. Die Analyse stellt außerdem fest, dass das Marktwachstum von der Optimierung von Faserrückgewinnungsverfahren wie Pyrolyse und Solvolyse abhängt, um eine hohe Zugfestigkeit zu gewährleisten. Die Wettbewerbsdifferenzierung hängt nun maßgeblich von der Fähigkeit ab, gleichmäßige Faserlängen und reine Oberflächenchemikalien zu liefern, die eine überlegene Haftung in neuen Verbundwerkstoffmatrizen ermöglichen. Dieser Ansatz hilft spezialisierten Recyclingunternehmen, in einem zunehmend von Umweltauflagen geprägten Markt Premiumpreise zu erzielen.

Marktübersicht für grüne Kohlenstofffasern

Nachhaltige Verbundwerkstoffe haben sich von Nischenprodukten zu gängigen Industrielösungen entwickelt. Grüne Kohlenstofffasern umfassen hochpräzise gefräste Fasern, präzisionsgeschnittene Kurzfasern und Vliesstoffe aus recycelten Rohstoffen. Sowohl globale Chemiekonzerne als auch Startups der Kreislaufwirtschaft konkurrieren auf diesem Markt und nutzen dafür Abfallquellen wie Produktionsreste und ausgediente Strukturen. Die steigende Nachfrage nach Leichtbau zur Verbesserung der Reichweite von Elektrofahrzeugen und der Effizienz von Windkraftanlagen hat die Beliebtheit grüner Kohlenstofffasern als umweltfreundliche Lösung erhöht. Nordamerika und Europa sind aufgrund ihrer etablierten Luft- und Raumfahrt- sowie Automobilindustrie führend im Umsatz, während der asiatisch-pazifische Raum den Ausbau der Recyclinginfrastruktur und die zunehmende Akzeptanz im Einzelhandel für Konsumgüter vorantreibt. Der US-Markt ist hochentwickelt, angetrieben von nachhaltigkeitsorientierten Luft- und Raumfahrtkonzernen und der breiten Verfügbarkeit fortschrittlicher Recyclingtechnologien. Der Wettbewerb zwischen den Marken fördert eine größere Materialvielfalt und den Einsatz nachhaltiger Harze zur Entwicklung vollständig grüner Verbundsysteme.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für grüne Kohlenstofffasern: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen für grüne Kohlenstofffasern

Markttreiber:

- Strenge Umweltauflagen und Deponieverbote: Viele Regionen führen strenge Regeln für die Entsorgung von Verbundabfällen ein. Dieser regulatorische Druck, zusammen mit dem wachsenden Interesse an abfallfreier Produktion, treibt die Beliebtheit von recycelten Kohlenstofffasern voran.

- Kosteneffizienz im Vergleich zu Primär-Kohlenstofffasern: Die Herstellung von Recyclingfasern verbraucht deutlich weniger Energie und ist kostengünstiger als die von Primär-PAN-basierten Fasern. Da Unternehmen bestrebt sind, ihre Materialkosten zu optimieren, verzeichnen nachhaltige Alternativen weiterhin stetige Absatzsteigerungen.

- Rasante Expansion der Elektrofahrzeugproduktion: Der Wandel der Automobilindustrie hin zur Elektrifizierung hat traditionelle Hürden für Recyclingmaterialien beseitigt. Dies zeigt sich besonders deutlich in der rasanten Verbreitung von geschnittenen und gemahlenen Fasern für nicht-strukturelle Innenraum- und Motorraumkomponenten.

Marktchancen:

- Expansion in die Bereiche Unterhaltungselektronik und Sportartikel: Neben der industriellen Nutzung bietet grüne Kohlenstofffaser bedeutende Möglichkeiten bei hochsteifen Gehäusen für Laptops und leichten Rahmen für Fahrräder und Tennisschläger.

- Wachstum der Infrastruktur für erneuerbare Energien: Die Bildung strategischer Partnerschaften zwischen Windkraftanlagenherstellern und Recyclingunternehmen könnte den Zugang zu margenstarken Marktsegmenten erleichtern, in denen recycelte Fasern zur Verstärkung massiver Turbinenschaufeln verwendet werden.

- Diversifizierung hin zu fortschrittlichen thermoplastischen Granulaten: Für Hersteller bietet sich eine wachsende Möglichkeit, durch die Entwicklung von kohlenstofffaserverstärkten Granulaten für 3D-Druck und Spritzguss gezielt in bestimmte Fertigungsbereiche vorzudringen.

Marktbericht für grüne Kohlenstofffasern: Segmentierungsanalyse

Der Marktanteil von grünen Kohlenstofffasern wird in verschiedenen Segmenten analysiert, um ein besseres Verständnis seiner Struktur, seines Wachstumspotenzials und der aufkommenden Trends zu ermöglichen. Nachfolgend ist der in Branchenberichten übliche Segmentierungsansatz dargestellt:

Nach Typ:

- Gehackte recycelte Kohlenstofffaser: Ein dominantes Segment, das aufgrund seiner Vielseitigkeit und einfachen Verarbeitung in großem Umfang in Vliesmatten und zur Verstärkung von thermoplastischen Spritzgussteilen eingesetzt wird.

- Gemahlene recycelte Kohlenstofffaser: Ein schnell wachsender Nischenmarkt, bei dem Fasern zu einem feinen Pulver vermahlen werden. Dieses wird zunehmend für Anwendungen bevorzugt, die eine verbesserte elektrische Leitfähigkeit oder Oberflächengüte bei Beschichtungen und Harzen erfordern.

Laut Quelle:

- Automobilschrott: Bleibt ein wichtiger Kanal für Rohstoffe in großen Mengen und profitiert von der Ausweitung der Programme zur Fahrzeugleichterung sowie von Produktionsresten.

- Luft- und Raumfahrtabfälle: Die wertvollste Quelle, die aus ausgemusterten Flugzeugen und Prepreg-Abfällen gewonnene Fasern mit hohem Modul liefert und so leistungsstarke Sekundäranwendungen ermöglicht.

Auf Antrag:

- Luft- und Raumfahrt: Verwendung von recycelten Fasern für Innenverkleidungen, Kanäle und nicht kritische Strukturbauteile zur Erreichung der Netto-Null-Ziele des Unternehmens.

- Automobilindustrie: Die am schnellsten wachsende Anwendung, insbesondere für Chassis-Paneele, Bodenstrukturen und Batteriegehäuse in Elektrofahrzeugen.

- Wind Energy: Bietet eine ausgewählte, aber wachsende Palette an Verstärkungsoptionen für Holmkappen und Rotorblattkomponenten in der Branche der erneuerbaren Energien.

- Sportartikel: Angetrieben durch die Nachfrage der Verbraucher nach umweltfreundlicher Hochleistungsausrüstung wie Golfschlägern, Hockeyschlägern und Fahrradrahmen.

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Süd- und Mittelamerika

- Naher Osten und Afrika

Berichtsumfang zum Markt für grüne Kohlenstofffasern

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 194,58 Millionen US-Dollar |

| Marktgröße bis 2034 | 535,27 Millionen US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 11,9 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nach Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte der Akteure im Markt für grüne Kohlenstofffasern: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für grüne Kohlenstofffasern wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Verbraucherbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

Marktanteilsanalyse für grüne Kohlenstofffasern nach Regionen

Der asiatisch-pazifische Raum wird aufgrund massiver Investitionen in Windenergie und die Produktion von Elektrofahrzeugen in den kommenden Jahren voraussichtlich das schnellste Wachstum verzeichnen. Auch Europa und Nordamerika bieten zahlreiche ungenutzte Möglichkeiten für fortschrittliche Recyclingtechnologien und die hochwertige Rückgewinnung von Luft- und Raumfahrtmaterialien.

Der Markt für grüne Kohlenstofffasern befindet sich in einem tiefgreifenden Wandel und entwickelt sich von einem Nischenthema in der Forschung und Entwicklung zu einem entscheidenden industriellen Rohstoff für die Klimaneutralität. Das Wachstum wird durch den dringenden Bedarf an Gewichtsreduzierung bei Flugzeugen, den Produktionsboom von Elektrofahrzeugen und den massiven Ausbau der Infrastruktur für erneuerbare Energien angetrieben. Nachfolgend finden Sie eine Zusammenfassung der Marktanteile und Trends nach Regionen:

Nordamerika

- Marktanteil: Ein bedeutendes Segment, das von einer starken Luft- und Raumfahrtindustrie und der Präsenz führender Recycling-Innovatoren geprägt ist.

-

Wichtigste Einflussfaktoren:

- Starke Nachfrage aus dem Verteidigungssektor nach nachhaltigen Leichtbaumaterialien

- Bundesanreize für saubere Energie und heimische Kreislaufwirtschaft

- Hohe Konzentration von Luft- und Raumfahrtschrott großer Flugzeughersteller

- Trends: Erfolgreiche Einführung von Recyclingfasern in 3D-Druckfilamenten und Ausbau kommerzieller Solvolyseanlagen.

Europa

- Marktanteil: Besitzt weltweit den größten Marktanteil, was auf strenge EU-Richtlinien zum Recycling von Altfahrzeugen und zur Klimaneutralität zurückzuführen ist.

-

Wichtigste Einflussfaktoren:

- Riesige Automobilproduktionsbasis in Deutschland und Frankreich, die umweltfreundliche Materialien priorisiert

- Etablierte Verarbeitungsinfrastruktur für die Verwertung von Verbundabfällen

- Starke staatliche Unterstützung für Initiativen zur Kreislaufwirtschaft

- Trends: Eine strategische Neuausrichtung hin zur Verwendung von Recyclingfasern in der Infrastruktur des öffentlichen Verkehrs und ein Fokus auf Hochleistungs-Vliesmatten.

Asien-Pazifik

- Marktanteil: Die am schnellsten wachsende Region, wobei China und Japan die Hauptmotoren für den Verbrauch nachhaltiger Materialien darstellen.

-

Wichtigste Einflussfaktoren:

- Riesige Verbrauchergruppe sucht umweltfreundliche Elektronik und Sportartikel

- Staatlich unterstützte Initiativen mit dem Ziel, ein globales Zentrum für die Produktion von Elektrofahrzeugen zu werden.

- Rasanter Ausbau von Offshore-Windkraftanlagen, der hochentwickelte Verbundwerkstoffe erfordert

- Trends: Starke Abhängigkeit von automatisierten Sortiertechnologien und großtechnische Herstellung von geschnittenen Fasern für die Elektronikindustrie.

Süd- und Mittelamerika

- Marktanteil: Aufstrebender Markt mit zunehmendem Fokus auf erneuerbare Energien in Ländern wie Brasilien und Chile.

-

Wichtigste Einflussfaktoren:

- Zunehmende Investitionen in massive Windparkanlagen, die hochsteife, leichte Rotorblätter erfordern

- Modernisierung der regionalen Luft- und Raumfahrtmontagebetriebe zur Erfüllung internationaler Nachhaltigkeitsstandards

- Trends: Zunahme lokaler Recyclinganlagen zur Bewältigung der steigenden Menge an Industrieabfällen aus der wachsenden regionalen Automobilteilefertigung.

Naher Osten und Afrika

- Marktanteil: Entwicklungsmarkt mit hohem Potenzial, das mit strategischen Veränderungen im Energiesektor und der fortgeschrittenen Fertigung zusammenhängt.

-

Wichtigste Einflussfaktoren:

- Strategische Investitionen in Smart Cities und fortschrittliche Infrastrukturprojekte in der Golfregion

- Wachsendes Interesse an Wasserstoff-Brennstoffzellentechnologien und dem damit verbundenen Bedarf an leichten Speicherbehältern

- Trends: Aufbau von Pyrolyseanlagen im Pilotmaßstab und Fokus auf die Verwendung von Recyclingfasern für die großtechnische Entsalzung und Energiespeicherinfrastruktur.

Hohe Marktdichte und starker Wettbewerb

Der Wettbewerb verschärft sich aufgrund der Präsenz etablierter Marktführer wie Toray Industries, SGL Carbon und der Mitsubishi Chemical Group. Regionale Recyclingexperten und Nischenanbieter wie Vartega Inc., Gen 2 Carbon und Carbon Conversions tragen ebenfalls zu einem vielfältigen und schnell wachsenden Marktumfeld bei.

Dieses wettbewerbsintensive Umfeld zwingt die Anbieter dazu, sich durch Folgendes zu differenzieren:

- Leistungsvalidierung: Hervorzuheben ist, dass recycelte Fasern über 90 % der Steifigkeit von Neufasern beibehalten können, was sie zu einer überlegenen Alternative für gewichtssensible Anwendungen macht.

- Transparenz der Lieferkette: Die Produzenten kontrollieren den gesamten Lebenszyklus, von der Sammlung von Abfällen in Luft- und Raumfahrtwerken bis zur Lieferung verarbeiteter Fasern an Automobilhersteller, und gewährleisten dabei ethische und nachvollziehbare Standards.

- Innovative Verarbeitung: Neue Technologien wie KI-gestützte Sortierung und energiearmes chemisches Recycling tragen zur Herstellung hochwertiger Pulver und Bündel bei, die weltweit in hochwertigen Konsumgütern verwendet werden.

Chancen und strategische Schritte

- Partnerschaften mit führenden Automobil- und Luftfahrtherstellern sichern langfristige Schrottlieferverträge. Dies gewährleistet eine stabile Rohstoffversorgung mit Automobil- und Luftfahrtschrott und bietet den Herstellern gleichzeitig eine verlässliche Möglichkeit, ihre Klimaneutralitätsziele zu erreichen.

- Entwicklung firmeneigener chemischer Behandlungen (Schlichten) für Recyclingfasern zur Verbesserung ihrer Haftung an thermoplastischen Harzen. Dadurch erreichen grüne Kohlenstofffasern mechanische Eigenschaften, die denen von Neuware sehr nahekommen, und erschließen so margenstarke Strukturbauteile.

- Grüne Kohlenstofffasern sollten in wachstumsstarken Bereichen wie der urbanen Luftmobilität (UAM/Lufttaxis) und der Wasserstoffspeicherung eingesetzt werden. Diese Anwendungen erfordern ein extrem geringes Gewicht und können die etwas höheren Kosten fortschrittlicher Recyclingmaterialien verkraften.

Die wichtigsten Unternehmen, die auf dem Markt für grüne Kohlenstofffasern tätig sind, sind:

- Procotex Corp SA

- Stems Inc.

- Sigmatex (UK) Ltd

- Shocker Composites LLC

- Carbon Conversions Co

- SGL Carbon SE

- Toray Industries Inc

- Gen 2 Carbon Ltd

- Catack-H Co Ltd

- Innovatives Recycling

Hinweis: Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge geordnet.

Neuigkeiten und aktuelle Entwicklungen auf dem Markt für grüne Kohlenstofffasern

- Im Oktober 2025 gab Toray Industries, Inc. die Entwicklung einer Recyclingtechnologie bekannt, die verschiedene kohlenstofffaserverstärkte Kunststoffe (CFK) aus Duroplasten zersetzen kann, wobei die Festigkeit und Oberflächenqualität der Fasern erhalten bleiben. Das Unternehmen nutzte diese Technologie zur Herstellung eines Vliesstoffs aus recycelten Kohlenstofffasern.

- Im Mai 2025 kündigten Syensqo und Vartega eine technische und kommerzielle Zusammenarbeit an, um ein Ökosystem zu schaffen, das den Einsatz von recycelten Kohlenstofffaserprodukten aus der Industrie in Hochleistungsanwendungen fördert.

Marktbericht zu grünen Kohlenstofffasern: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für grüne Kohlenstofffasern (2021–2034)“ bietet eine detaillierte Analyse des Marktes und deckt folgende Bereiche ab:

- Marktgröße und Prognose für grüne Kohlenstofffasern auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt werden

- Trends im Markt für grüne Kohlenstofffasern sowie Marktdynamiken wie Treiber, Hemmnisse und wichtige Chancen

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für grüne Kohlenstofffasern: Wichtige Markttrends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Rahmenbedingungen und aktuelle Marktentwicklungen

- Branchenlandschafts- und Wettbewerbsanalyse mit Fokus auf Marktkonzentration, Heatmap-Analyse, prominente Akteure und aktuelle Entwicklungen auf dem Markt für grüne Kohlenstofffasern.

- Detaillierte Unternehmensprofile

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends