Marktwachstum, Größe, Anteil, Trends, Analyse der wichtigsten Akteure und Prognose zur Behandlung von im Krankenhaus erworbenen Infektionen bis 2030

Marktgröße und Prognosen für die Behandlung von im Krankenhaus erworbenen Infektionen (2020 – 2030), globaler und regionaler Anteil, Trends und Berichtsabdeckung zur Analyse von Wachstumschancen: Nach Arzneimittelklasse (antibakterielle Arzneimittel, antivirale Arzneimittel, Antimykotika und andere), Infektionstyp (Harnwegsinfektionen, beatmungsassoziierte Pneumonie, Wundinfektionen, Blutbahninfektionen und andere Krankenhausinfektionen), Vertriebskanal (Krankenhausapotheken, Einzelhandelsapotheken, E-Commerce und andere) und Geografie (Nordamerika, Europa, Asien-Pazifik, Süd- und Mittelamerika sowie Naher Osten und Afrika)

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00029976

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 171

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 11, 2024

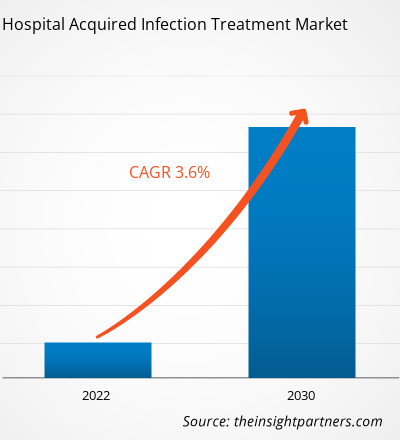

[Forschungsbericht] Der Markt für die Behandlung von im Krankenhaus erworbenen Infektionen soll von 15.099,19 Millionen US-Dollar im Jahr 2022 auf 19.978,39 Millionen US-Dollar im Jahr 2030 wachsen; von 2022 bis 2030 wird eine durchschnittliche jährliche Wachstumsrate (CAGR) von 3,6 % erwartet.

Markteinblicke und Analystenansichten:

Im Krankenhaus erworbene Infektionen (HAIs), auch bekannt als nosokomiale Infektionen, können in einer Vielzahl von Umgebungen auftreten, darunter Krankenhäuser, Langzeitpflegeeinrichtungen und ambulante Einrichtungen, und sie können auch nach der Entlassung auftreten. HAIs können auch Berufsinfektionen sein, die das Gesundheitspersonal betreffen. Die wichtigsten Faktoren, die das Wachstum des Marktes für die Behandlung von im Krankenhaus erworbenen Infektionen vorantreiben, sind die hohe Prävalenz von HAIs und der zunehmende Fokus auf Patientensicherheit und qualitativ hochwertige Pflege. Die Bedrohung durch antimikrobielle Resistenz behindert jedoch das Wachstum des Marktes für die Behandlung von im Krankenhaus erworbenen Infektionen .

Wachstumstreiber und -hemmnisse:

Beispiele für im Gesundheitswesen auftretende Infektionen (HAIs) sind zentralvenöse Katheter-assoziierte Blutstrominfektionen, katheterassoziierte Harnwegsinfektionen und beatmungsassoziierte Pneumonie. Diese Infektionen, die als Wundinfektionen bezeichnet werden, können auch an Operationsstellen auftreten. Laut dem 2021 veröffentlichten Bericht „2020 National and State Healthcare-Associated Infections Progress Report“ der Centers for Disease Control and Prevention (CDC) nahmen die Fälle zentralvenöser Katheter-assoziierter Blutstrominfektionen, Methicillin-resistenter Staphylococcus aureus (MRSA)-Bakteriämie und beatmungsassoziierter Ereignisse in den USA zwischen 2019 und 2020 um 24 %, 35 % bzw. 15 % zu.

Darüber hinaus sind Harnwegsinfektionen (HWI) laut dem Bericht des National Healthcare Safety Network (NHSN) vom Januar 2022 die fünfthäufigste Art von im Gesundheitswesen auftretenden Infektionen. HWI machen mehr als 9,5 % der Erkrankungen in Akutkrankenhäusern aus. Katheterassoziierte Harnwegsinfektionen (CAUTI) werden durch Harnkatheter verursacht, die zum Ablassen von Urin aus der Blase verwendet werden. CAUTI ist eine der häufigsten Infektionen bei hospitalisierten Patienten mit HWI. Laut den Centers for Disease Control and Prevention (CDC) stehen fast 75 % der Infektionen mit einem Harnkatheter im Zusammenhang. Während ihres Krankenhausaufenthalts müssen 15 % bis 25 % der hospitalisierten Patienten Harnkatheter verwenden. Die längere Verwendung von Harnkathetern ist der größte Risikofaktor für CAUTI. Komplikationen bei CAUTI führen zu Leiden des Patienten, längeren Krankenhausaufenthalten, erhöhten Behandlungskosten und sogar zum Tod.

Darüber hinaus sind Harnwegsinfektionen laut CDC jedes Jahr für mehr als 13.000 Todesfälle verantwortlich. Eine akute unkomplizierte Blasenentzündung verursacht etwa sechs Tage Beschwerden und führt zu etwa 7 Millionen Arztbesuchen pro Jahr, die Kosten in Höhe von 1,6 Milliarden US-Dollar verursachen. Infolgedessen stellt die steigende Zahl der HAI-Fälle eine erhebliche finanzielle Belastung für das Gesundheitssystem dar. Die zunehmende Verbreitung von CAUTI in Verbindung mit der gestiegenen Nachfrage nach Medikamenten zur Behandlung treibt den Markt an.

Allerdings stellt die antimikrobielle Resistenz eine große Herausforderung für die Behandlung von HAI dar, da sie die Wirksamkeit vorhandener antimikrobieller Mittel begrenzt und die Entwicklung neuer Behandlungsstrategien und antimikrobieller Alternativen erforderlich macht, um resistente Krankheitserreger wirksam zu bekämpfen.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für die Behandlung von im Krankenhaus erworbenen Infektionen: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Berichtssegmentierung und -umfang:

Der globale Markt für die Behandlung von im Krankenhaus erworbenen Infektionen ist nach Arzneimittelklasse, Infektionstyp und Vertriebskanal segmentiert. Basierend auf der Arzneimittelklasse ist der Markt für die Behandlung von im Krankenhaus erworbenen Infektionen in antibakterielle Medikamente, antivirale Medikamente, antimykotische Medikamente und andere unterteilt. Basierend auf dem Infektionstyp wird die Behandlung von im Krankenhaus erworbenen Infektionen in Harnwegsinfektionen, beatmungsassoziierte Pneumonie, Wundinfektionen, Blutbahninfektionen und andere Krankenhausinfektionen unterschieden. Basierend auf dem Vertriebskanal ist der Markt in Krankenhausapotheken, Einzelhandelsapotheken, E-Commerce und andere segmentiert. Der Markt für die Behandlung von im Krankenhaus erworbenen Infektionen ist geografisch segmentiert in Nordamerika (USA, Kanada und Mexiko), Europa (Deutschland, Frankreich, Italien, Großbritannien, Russland und das übrige Europa), Asien-Pazifik (Australien, China, Japan, Indien, Südkorea und der restliche Asien-Pazifik-Raum), den Nahen Osten und Afrika (Südafrika, Saudi-Arabien, die Vereinigten Arabischen Emirate und der restliche Nahe Osten und Afrika) sowie Süd- und Mittelamerika (Brasilien, Argentinien und der restliche Süd- und Mittelamerika).

Segmentanalyse:

Der Markt für die Behandlung von im Krankenhaus erworbenen Infektionen ist nach Arzneimittelklassen in antibakterielle Arzneimittel, antivirale Arzneimittel, antimykotische Arzneimittel und andere unterteilt. Das Segment der antibakteriellen Arzneimittel hatte 2022 den größten Marktanteil und wird voraussichtlich zwischen 2022 und 2030 die höchste durchschnittliche jährliche Wachstumsrate verzeichnen.

Der Markt für die Behandlung von im Krankenhaus erworbenen Infektionen ist nach Infektionstyp in Harnwegsinfektionen , beatmungsassoziierte Pneumonie, Wundinfektionen, Blutbahninfektionen und andere Krankenhausinfektionen unterteilt. Das Segment Harnwegsinfektionen hatte 2022 den größten Marktanteil. Es wird jedoch erwartet, dass das Segment beatmungsassoziierte Pneumonie von 2022 bis 2030 die höchste durchschnittliche jährliche Wachstumsrate verzeichnet.

Der Markt für die Behandlung von im Krankenhaus erworbenen Infektionen ist nach Vertriebskanälen in Krankenhausapotheken, Einzelhandelsapotheken, E-Commerce und andere unterteilt. Im Jahr 2022 hatte das Segment der Krankenhausapotheken den größten Marktanteil, und es wird erwartet, dass dasselbe Segment zwischen 2022 und 2030 die höchste durchschnittliche jährliche Wachstumsrate verzeichnet.

Regionale Analyse:

Geografisch ist der globale Markt für die Behandlung von Krankenhausinfektionen in fünf Hauptregionen unterteilt: Nordamerika, Europa, Asien-Pazifik, Süd- und Mittelamerika sowie Naher Osten und Afrika.

Im Jahr 2022 hatte Nordamerika den größten Anteil am weltweiten Markt für die Behandlung von im Krankenhaus erworbenen Infektionen. In den USA gibt es eine hohe Prävalenz von HAI, was das Wachstum des Marktes für die Behandlung von im Krankenhaus erworbenen Infektionen vorantreibt. Laut CDC hat an jedem beliebigen Tag etwa 1 von 31 Krankenhauspatienten mindestens eine HAI. Ebenso können HAIs und andere Infektionen laut dem Office of Disease Prevention and Health Promotion zu Sepsis führen und verursachen in den USA jährlich etwa 1,7 Millionen Krankheitsfälle und 270.000 Todesfälle. Somit treibt die hohe Prävalenz von HAI unter den Menschen in den USA das Wachstum des Marktes für die Behandlung von im Krankenhaus erworbenen Infektionen an.

Branchenentwicklungen und zukünftige Chancen:

Nachfolgend sind verschiedene Initiativen wichtiger Akteure auf dem globalen Markt für die Behandlung von im Krankenhaus erworbenen Infektionen aufgeführt:

- Im Mai 2023 gab Innoviva Specialty Therapeutics bekannt, dass die US-amerikanische Food and Drug Administration (FDA) XACDURO (Sulbactam zur Injektion; Durlobactam zur Injektion) zugelassen hat, das für die intravenöse Anwendung bei Patienten ab 18 Jahren zur Behandlung von im Krankenhaus erworbener bakterieller Pneumonie und beatmungsassoziierter bakterieller Pneumonie (HABP/VABP) zugelassen ist, die durch anfällige Isolate des Acinetobacter baumannii-calcoaceticus-Komplexes (Acinetobacter) verursacht wird. Innoviva Specialty Therapeutics gab an, dass es sich auf die Bereitstellung innovativer Therapien in der Intensivpflege und bei Infektionskrankheiten konzentriert.

- Im Mai 2023 gaben Forscher des Indian Institute of Science Education and Research (IISER), Pune und des Central Drug Research Institute (CSIR-CDRI), Lucknow bekannt, dass sie ein potenzielles neues Antibiotikum gegen Acinetobacter baumannii entdeckt hätten, das häufig HAIs verursacht.

- Im September 2020 gab Shionogi & Co Ltd bekannt, dass die FDA einen ergänzenden Antrag auf Zulassung eines neuen Arzneimittels (sNDA) für FETROJA (Cefiderocol) zur Behandlung von Patienten ab 18 Jahren mit im Krankenhaus erworbener bakterieller Lungenentzündung und beatmungsassoziierter bakterieller Lungenentzündung (HABP/VABP) genehmigt habe, die durch anfällige gramnegative Mikroorganismen wie Enterobacter cloacae-Komplex, Klebsiella pneumoniae, Acinetobacter baumannii-Komplex, Escherichia coli, Pseudomonas aeruginosa und Serratia marcescens verursacht werde.

- Im Juni 2020 gab Merck bekannt, dass die US-amerikanische Food and Drug Administration (FDA) einen ergänzenden Zulassungsantrag (sNDA) für RECARBRIO (Imipenem, Cilastatin und Relebactam) zur Behandlung von Patienten ab 18 Jahren genehmigt hat, die an im Krankenhaus erworbener bakterieller Pneumonie und beatmungsassoziierter bakterieller Pneumonie (HABP/VABP) leiden, die durch anfällige gramnegative Mikroorganismen wie Acinetobacter calcoaceticus-baumannii-Komplex, Klebsiella oxytoca, Klebsiella pneumoniae, Enterobacter cloacae, Escherichia coli, Haemophilus influenzae, Klebsiella aerogenes, Pseudomonas aeruginosa und Serratia marcescens verursacht werden.

Regionale Einblicke in den Markt für die Behandlung von im Krankenhaus erworbenen Infektionen

Die regionalen Trends und Faktoren, die den Markt für die Behandlung von im Krankenhaus erworbenen Infektionen während des gesamten Prognosezeitraums beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie für die Behandlung von im Krankenhaus erworbenen Infektionen in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Markt für die Behandlung von im Krankenhaus erworbenen Infektionen

Umfang des Marktberichts zur Behandlung von im Krankenhaus erworbenen Infektionen

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2022 | 15.099,19 Millionen US-Dollar |

| Marktgröße bis 2030 | 19.978,39 Millionen US-Dollar |

| Globale CAGR (2022 - 2030) | 3,6 % |

| Historische Daten | 2020-2022 |

| Prognosezeitraum | 2022–2030 |

| Abgedeckte Segmente |

Nach Arzneimittelklasse

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmerdichte für die Behandlung von Krankenhausinfektionen: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für die Behandlung von Krankenhausinfektionen wächst rasant. Dies wird durch die steigende Nachfrage der Endnutzer aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts vorangetrieben. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung von Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten Unternehmen, die auf dem Markt für die Behandlung von im Krankenhaus erworbenen Infektionen tätig sind, sind:

- Merck & Co Inc

- Pfizer Inc

- AbbVie Inc

- Paratek Pharmaceuticals Inc

- Eugia US LLC

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für die Behandlung von Krankenhausinfektionen

Wettbewerbslandschaft und Schlüsselunternehmen:

Merck & Co Inc, Pfizer Inc, AbbVie Inc, Paratek Pharmaceuticals Inc, Eugia US LLC, Abbott Laboratories, Cumberland Pharmaceuticals Inc, Innoviva Specialty Therapeutics Inc, Cipla Ltd und Eli Lilly and Company gehören zu den führenden Akteuren auf dem Markt für die Behandlung von im Krankenhaus erworbenen Infektionen. Diese Unternehmen konzentrieren sich auf neue Technologien, die Weiterentwicklung bestehender Produkte und die geografische Expansion, um die weltweit wachsende Verbrauchernachfrage zu erfüllen und ihr Produktangebot in Spezialportfolios zu erweitern.

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends