Beschaffungs-as-a-Service-Markt – Erkenntnisse aus globaler und regionaler Analyse – Prognose bis 2031

Marktgröße und Prognose für Procurement as a Service (2021–2031), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalysen: Nach Komponente (Strategische Beschaffung, Ausgabenmanagement, Kategoriemanagement, Prozessmanagement, Vertragsmanagement und Transaktionsmanagement), Unternehmensgröße (KMU und Großunternehmen), Endbenutzer (IT und Telekommunikation, Konsumgüter und Einzelhandel, Fertigung, Energie und Versorgung, Gesundheitswesen, Gastgewerbe und Tourismus und andere) und Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00005963

- Kategorie : Technologie, Medien und Telekommunikation

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : May 16, 2024

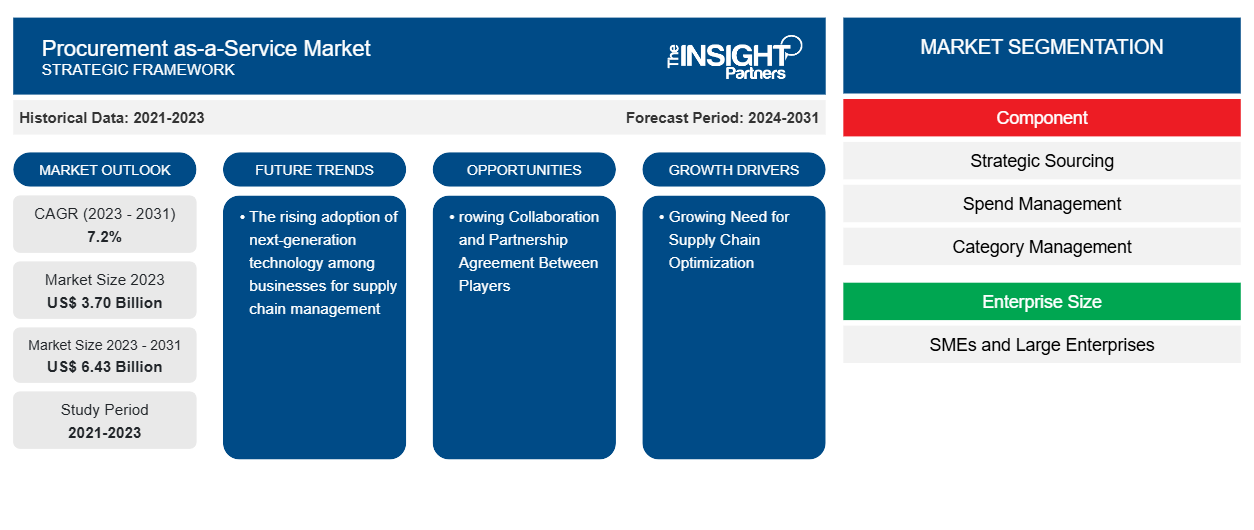

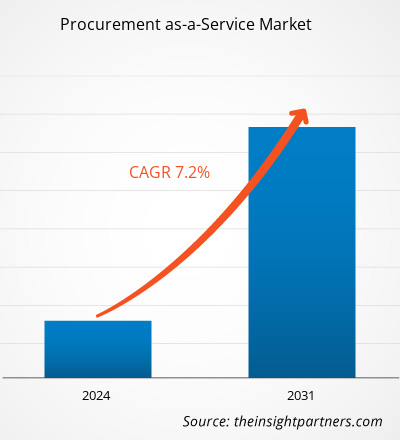

Das Marktvolumen für Beschaffung als Dienstleistung wird voraussichtlich von 3,70 Milliarden US-Dollar im Jahr 2023 auf 6,43 Milliarden US-Dollar im Jahr 2031 anwachsen. Der Markt wird voraussichtlich zwischen 2023 und 2031 eine durchschnittliche jährliche Wachstumsrate von 7,2 % verzeichnen. Die zunehmende Einführung von Technologien der nächsten Generation in Unternehmen für das Lieferkettenmanagement wird wahrscheinlich ein wichtiger Markttrend für Beschaffung als Dienstleistung bleiben.

Beschaffung als Service – Marktanalyse

Der Beschaffungs-as-a-Service-Markt wächst rasant aufgrund des wachsenden Bedarfs an Lieferkettenoptimierung und der zunehmenden Anzahl von Import- und Exportaktivitäten weltweit. Der Markt wächst stetig, angetrieben von staatlichen Initiativen zur Förderung der Digitalisierung zur Automatisierung des Arbeitsablaufs. Darüber hinaus bieten die wachsenden Kooperations- und Partnerschaftsvereinbarungen zwischen den Akteuren lukrative Möglichkeiten für Marktwachstum.

Beschaffung als Service – Marktübersicht

Procurement as a Service (PaaS) ist ein Modell für das Outsourcing von Beschaffungen, das Ressourcen (Mitarbeiter, Tools und Wissen) kombiniert, um die Beschaffungsanforderungen eines Unternehmens zu erfüllen. Viele Unternehmen nutzen heute Computer, um ihren gesamten Einkaufsprozess von der ersten Anfrage bis zur endgültigen Rechnung zu verwalten. Darüber hinaus werden bei der digitalen Beschaffung bahnbrechende Technologien eingesetzt, um die Transaktionsautomatisierung zu erleichtern. Darüber hinaus ermöglicht es vorausschauende und proaktive Vorgänge wie strategische Beschaffung und Lieferantenmanagement, was die Betriebskosten eines Unternehmens senkt. Der Markt wird durch den zunehmenden Bedarf der Unternehmen an der Rationalisierung von Beschaffungsvorgängen unter Einhaltung von Compliance-Vorschriften und Verträgen angetrieben.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlose Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Beschaffungs-as-a-Service-Markt: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Treiber und Chancen des Beschaffungs-as-a-Service-Marktes

Wachsender Bedarf an Lieferkettenoptimierung

Supply Chain Manager nutzen häufig Beschaffungsmanagementdienste, um die gesamten Abläufe der Lieferkette zu überwachen. Diese Dienste ermöglichen es Supply Chain Managern, potenzielle Probleme in der Lieferkette deutlich vorherzusehen und Ressourcen entsprechend neu zu verteilen. Darüber hinaus kann Beschaffung als Service zuverlässige datengesteuerte Lösungen generieren, mit denen die Effizienz von Geschäftsprozessen verbessert wird. Beschaffungsmanagementsoftware bietet ausnahmebasierte Prozessmanagementsysteme, die Benutzern dabei helfen, stabile Abläufe zu verwalten und die abteilungsübergreifende Transparenz zu erhöhen. Daher investieren Verbraucher zunehmend in Beschaffungsmanagementsoftware, um die Transparenz in der Lieferkette, die Offenlegung von Bestellungen und Versanddaten aufrechtzuerhalten.

Wachsende Zusammenarbeit und Partnerschaftsvereinbarungen zwischen den Akteuren – eine Chance auf dem Procurement-as-a-Service-Markt

Der technologische Fortschritt und die steigende Nachfrage der Marktteilnehmer nach Cloud-Computing , KI, Datenanalyse und ML-Technologie zur Verbesserung ihrer Serviceangebote schaffen Chancen auf dem Markt. Darüber hinaus ermutigt die wachsende Nachfrage der Verbraucher nach technologisch fortschrittlichen Diensten die Marktteilnehmer, innovative Lösungen zu entwickeln oder ihre bestehenden Portfolios um Funktionen zu erweitern. So unterzeichnete Corbus, LLC im November 2022 eine Lieferketten-Beschaffungspartnerschaftsvereinbarung mit GIS, um einzigartige Lösungen zu entwickeln. Diese Partnerschaft unterstützt GIS dabei, Infrastruktur und Ressourcen an Kunden in Europa, Lateinamerika, Nordamerika, Asien sowie dem Nahen Osten und Afrika zu liefern.

Segmentierungsanalyse des Beschaffungs-as-a-Service-Marktberichts

Wichtige Segmente, die zur Ableitung der Marktanalyse für Beschaffung als Service beigetragen haben, sind Komponente, Unternehmensgröße und Endbenutzer.

- Basierend auf den Komponenten ist der Markt in strategische Beschaffung, Ausgabenmanagement, Kategoriemanagement, Prozessmanagement, Vertragsmanagement und Transaktionsmanagement segmentiert. Das Segment Ausgabenmanagement hatte im Jahr 2023 einen größeren Marktanteil.

- In Bezug auf die Unternehmensgröße ist der Markt in KMU und Großunternehmen unterteilt. Das Segment der Großunternehmen hatte im Jahr 2023 einen größeren Marktanteil.

- Auf der Grundlage des Endverbrauchers ist der Markt in IT und Telekommunikation, Konsumgüter und Einzelhandel, Fertigung, Energie und Versorgung, Gesundheitswesen, Gastgewerbe und Tourismus und andere segmentiert. Das Fertigungssegment hielt im Jahr 2023 den größten Marktanteil.

Procurement as-a-Service Marktanteilsanalyse nach Geografie

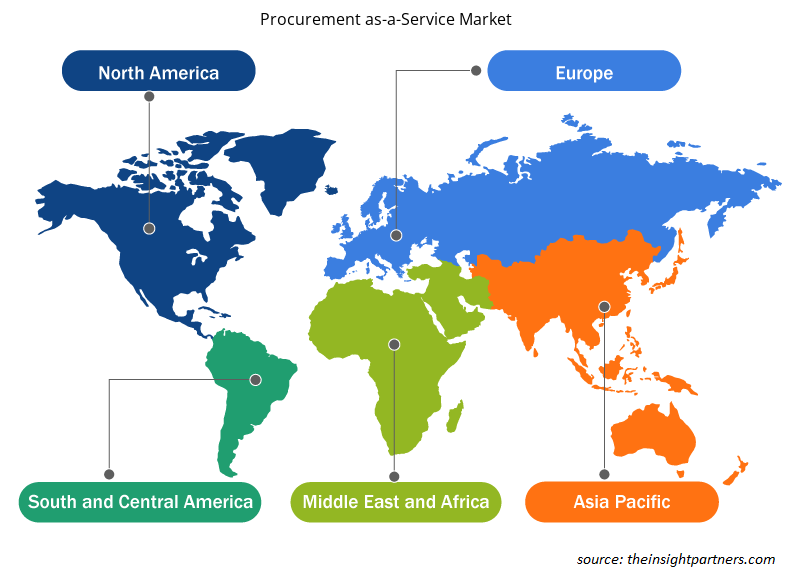

Der geografische Umfang des Marktberichts zum Thema Beschaffung als Dienstleistung ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Südamerika/Süd- und Mittelamerika.

In Bezug auf den Umsatz hatte Nordamerika den größten Marktanteil im Bereich Beschaffung als Dienstleistung, was auf den technologischen Fortschritt und die Integration von KI, Blockchain und anderen Technologien zur Verbesserung der Lieferkette zurückzuführen ist. Erhebliche staatliche Investitionen zur Förderung der Digitalisierung von Unternehmen beflügeln den Markt in der Region. Die zunehmende Digitalisierung ermutigt Marktteilnehmer, digitale Technologien zur Optimierung ihrer Beschaffungsprozesse einzusetzen, was den Markt in Nordamerika beflügelt.

Regionale Einblicke in den Beschaffungs-as-a-Service-Markt

Die regionalen Trends und Faktoren, die den Procurement-as-a-Service-Markt während des Prognosezeitraums beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie von Procurement-as-a-Service in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Procurement-as-a-Service-Markt

Umfang des Marktberichts „Procurement as a Service“

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2023 | 3,70 Milliarden US-Dollar |

| Marktgröße bis 2031 | 6,43 Milliarden US-Dollar |

| Globale CAGR (2023 - 2031) | 7,2 % |

| Historische Daten | 2021-2023 |

| Prognosezeitraum | 2024–2031 |

| Abgedeckte Segmente |

Nach Komponente

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Akteure auf dem Procurement-as-a-Service-Markt: Die Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Beschaffung als Dienstleistung wächst rasant. Die Nachfrage der Endnutzer steigt aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung von Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten Unternehmen, die auf dem Procurement-as-a-Service-Markt tätig sind, sind:

- Accenture

- CAPGEMINI SE

- Corbus

- GmbH

- Genpact Ltd.

- GEP

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Erhalten Sie einen Überblick über die wichtigsten Akteure auf dem Procurement-as-a-Service-Markt

Neuigkeiten und aktuelle Entwicklungen zum Procurement-as-a-Service-Markt

Der Beschaffungs-as-a-Service-Markt wird durch die Erhebung qualitativer und quantitativer Daten nach Primär- und Sekundärforschung bewertet, die wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken umfasst. Im Folgenden finden Sie eine Liste der Entwicklungen auf dem Markt für Beschaffungs-as-a-Service und Strategien:

- Im Februar 2024 arbeiten Vodafone Group Plc und International Machine Business Corp auf Branchenebene zusammen und leiten die GSMA Post-Quantum Telco Network Taskforce, die ihre Partner und Kunden auf ihrem Weg in die Quantensicherheit unterstützen wird, insbesondere angesichts der Einführung der Post-Quanten-Kryptografie in der gesamten globalen Telekommunikationslieferkette . (Quelle: Vodafone Group Plc, Pressemitteilung, 2024)

Marktbericht zu Beschaffung als Service – Abdeckung und Ergebnisse

Der Bericht „Procurement-as-a-Service-Marktgröße und -prognose (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Marktgröße und Prognose auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Projekts abgedeckt sind

- Marktdynamik wie Treiber, Beschränkungen und wichtige Chancen

- Wichtige Zukunftstrends

- Detaillierte PEST/Porters Five Forces- und SWOT-Analyse

- Globale und regionale Marktanalyse mit wichtigen Markttrends, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und aktuellen Entwicklungen

- Detaillierte Firmenprofile

Ankita ist eine dynamische Marktforschungs- und Beratungsexpertin mit über 8 Jahren Erfahrung in den Bereichen Technologie, Medien, IKT sowie Elektronik und Halbleiter. Sie hat über 100 Beratungs- und Forschungsaufträge für globale Kunden wie Microsoft, Oracle, NEC Corporation, SAP, KPMG und Expeditors International erfolgreich geleitet und durchgeführt. Zu ihren Kernkompetenzen gehören Marktbewertung, Datenanalyse, Prognose, Strategieformulierung, Wettbewerbsbeobachtung und das Verfassen von Berichten. Ankita ist versiert in der Abwicklung kompletter Projektzyklen – von der Angebotserstellung vor dem Verkauf und Kundengesprächen bis hin zur Bereitstellung umsetzbarer Erkenntnisse nach dem Verkauf. Sie ist versiert in der Leitung funktionsübergreifender Teams, der Strukturierung komplexer Forschungsmodule und der Ausrichtung von Lösungen an kundenspezifischen Geschäftszielen. Ihre ausgezeichneten Kommunikationsfähigkeiten, Führungsqualitäten und Präsentationsfähigkeiten haben es ihr ermöglicht, in einem schnelllebigen und sich entwickelnden Marktumfeld stets wertorientierte Ergebnisse zu liefern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends