Tendencias, demanda y crecimiento del mercado de camas de hospital hasta 2034

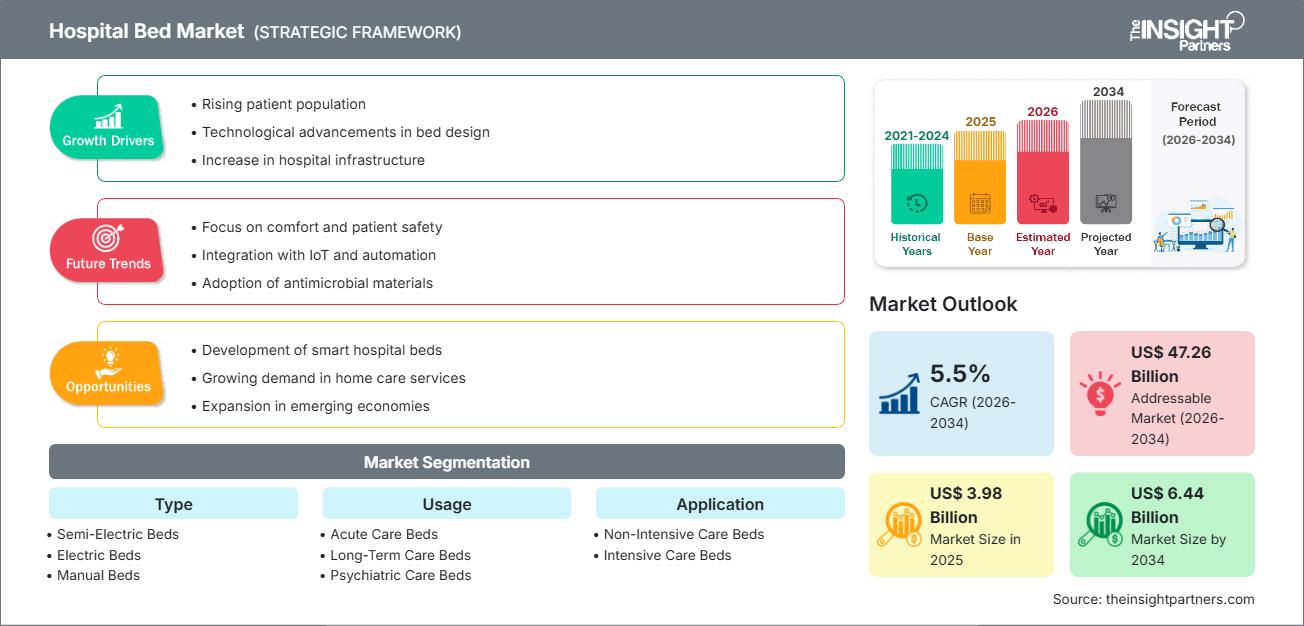

Datos históricos : 2021-2024 | Año base : 2025 | Período de pronóstico : 2026-2034Tamaño y pronóstico del mercado de camas de hospital (2021-2034), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por tipo (camas semieléctricas, eléctricas y manuales), uso (camas de cuidados intensivos, de larga duración, psiquiátricas y otras), aplicación (camas de cuidados no intensivos y de cuidados intensivos) y usuario final (hospitales y clínicas, centros de atención a personas mayores, centros de cirugía ambulatoria y centros de atención domiciliaria).

- Estado : Próxima

- Código de informe : TIPRE00029326

- Categoría : Bienes de consumo

- Número de páginas : 150

- Formatos de informe disponibles :

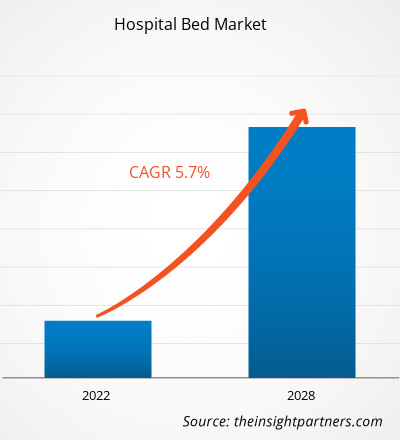

Se proyecta que el tamaño del mercado mundial de camas de hospital alcance los 6.440 millones de dólares estadounidenses para 2034, desde los 3.980 millones de dólares estadounidenses en 2025. Se anticipa que el mercado registre una CAGR del 5,5 % durante el período de pronóstico 2026-2034.

Las dinámicas clave del mercado incluyen un mayor enfoque global en la modernización de la infraestructura médica, el aumento de las tasas de ingreso de pacientes por enfermedades crónicas e infecciosas, y una transición significativa hacia soluciones integradas de salud digital. Además, se espera que el mercado se beneficie del crecimiento de la población geriátrica que requiere cuidados a largo plazo, la expansión de la capacidad sanitaria en las economías emergentes y la creciente inclusión de tecnologías de monitorización inteligente en unidades de cuidados intensivos de alto valor.

Análisis del mercado de camas de hospital

El análisis del mercado de camas hospitalarias indica un período de transformación en el que los profesionales sanitarios están evolucionando más allá de la funcionalidad mecánica básica hacia ecosistemas clínicos integrados. Los datos actuales del mercado revelan un aumento en la demanda de camas que actúen como centros de diagnóstico, capaces de recopilar datos continuamente para facilitar la enfermería predictiva. Si bien el segmento de camas manuales sigue siendo un producto básico de alto volumen en mercados rurales y emergentes sensibles a los costos, los segmentos eléctricos y semieléctricos están captando mayor valor gracias a una ergonomía superior y la reducción del esfuerzo físico del cuidador. El análisis estratégico sugiere que la diferenciación en el mercado está cada vez más determinada por la capacidad del fabricante para integrar sensores de prevención de lesiones por presión y detección de caídas directamente en el marco de la cama. Además, el mercado está experimentando un impulso local hacia camas sostenibles y ecodiseñadas que reduzcan la huella de carbono a lo largo de su ciclo de vida, en consonancia con las iniciativas globales de atención sanitaria ecológica.

Descripción general del mercado de camas de hospital

El mercado de camas de hospital ha evolucionado, pasando de ofrecer simples plataformas de descanso a dispositivos médicos sofisticados, esenciales para la atención centrada en el paciente. Los análisis actuales del sector destacan que las camas de hospital se clasifican ahora no solo por su fuente de alimentación, sino también por su aplicación clínica especializada, como la atención bariátrica, psiquiátrica o pediátrica. El mercado de camas de hospital presenta un sólido panorama competitivo, donde las marcas líderes utilizan recubrimientos antimicrobianos y diseños modulares para abordar la creciente amenaza de las infecciones nosocomiales (IAH). En regiones desarrolladas como Norteamérica y Europa, el mercado se ve impulsado por un ciclo de reemplazo donde la infraestructura obsoleta se sustituye por camas inteligentes que se conectan sin problemas a los historiales clínicos electrónicos (HCE). Mientras tanto, en la región Asia-Pacífico, la rápida construcción de hospitales y el auge del turismo médico están impulsando una afluencia masiva de unidades de cuidados intensivos de alta gama y camas médico-quirúrgicas estándar, posicionando a la región como el segmento geográfico de mayor crecimiento.

El mercado estadounidense es un mercado maduro y sofisticado que se caracteriza por una infraestructura sanitaria avanzada y altos estándares clínicos. El crecimiento se ve impulsado por el envejecimiento demográfico y la creciente incidencia de enfermedades crónicas, que requieren hospitalizaciones prolongadas. Los hospitales priorizan cada vez más las camas inteligentes y conectadas para mejorar la seguridad del paciente y la eficiencia operativa.

Personalice este informe según sus necesidades

Obtenga PERSONALIZACIÓN GRATUITAMercado de camas de hospital: Perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Impulsores y oportunidades del mercado de camas de hospital

Factores impulsores del mercado:

- Aumento de la población geriátrica mundial: el aumento de ciudadanos de edad avanzada aumenta significativamente la demanda de camas especializadas que atiendan problemas de movilidad y el manejo de la salud a largo plazo relacionada con la edad.

- Integración tecnológica en la atención al paciente: la adopción de camas inteligentes impulsadas por IoT e IA que monitorean los signos vitales del paciente y automatizan el reposicionamiento está impulsando un ciclo de reemplazo de equipos manuales obsoletos.

- Expansión de la infraestructura de atención de salud: Las importantes inversiones gubernamentales y privadas en la construcción de nuevos hospitales de múltiples especialidades, particularmente en los países en desarrollo, están creando una demanda constante de camas médicas.

Oportunidades de mercado:

- Creciente demanda de soluciones de atención médica domiciliaria: más allá de los hospitales tradicionales, existe una oportunidad creciente de camas de calidad hospitalaria diseñadas para entornos de atención domiciliaria, centrándose en la portabilidad y la facilidad de uso para los cuidadores familiares.

- Crecimiento en salud conductual especializada: la expansión de la infraestructura de salud mental presenta oportunidades para camas de atención psiquiátrica diseñadas con características específicas de seguridad y antiligaduras.

- Modernización de las unidades de cuidados intensivos: las alianzas estratégicas entre fabricantes de camas y proveedores de software médico pueden facilitar la implementación de camas de UCI conectadas y de alto margen en departamentos de alta agudeza.

Análisis de segmentación del informe de mercado de camas de hospital

La cuota de mercado de camas de hospital se analiza en varios segmentos para comprender mejor su estructura, potencial de crecimiento y tendencias emergentes. A continuación, se presenta el enfoque de segmentación estándar utilizado en la mayoría de los informes del sector:

Por tipo:

- Camas semieléctricas: un segmento versátil que combina el ajuste manual de altura con controles eléctricos para la cabeza y los pies, lo que las hace populares en clínicas de nivel medio y en atención domiciliaria.

- Camas eléctricas: el nicho de más rápido crecimiento, que ofrece automatización total y funciones avanzadas de monitoreo de pacientes, preferidas por instalaciones de cuidados intensivos y agudos de alta gama.

- Camas manuales: el principal impulsor del volumen en mercados con limitaciones presupuestarias y clínicas rurales debido a su simple confiabilidad mecánica y rentabilidad.

Por uso:

- Camas de cuidados agudos: diseñadas para el tratamiento a corto plazo de lesiones o enfermedades graves, centrándose en la alta rotación de pacientes y la facilidad de desinfección.

- Camas para cuidados de larga duración: Dirigidas a hogares de ancianos y centros de rehabilitación donde la comodidad y la prevención de úlceras por presión son requisitos principales.

- Camas para atención psiquiátrica: diseños especializados que priorizan la seguridad y se utilizan en centros de salud conductual para minimizar el riesgo del paciente y garantizar la durabilidad.

Por aplicación:

- Camas de cuidados intensivos: Camas de alto valor equipadas con sensores avanzados y soporte para equipos de monitoreo de vida utilizados en UCI.

- Camas de cuidados no intensivos: camas médicas estándar utilizadas en salas generales y salas de recuperación para pacientes estables.

Por usuario final:

- Hospitales y clínicas: el principal contribuyente a los ingresos, impulsado por las continuas actualizaciones de infraestructura y los altos volúmenes de pacientes.

- Centros de atención para personas mayores: un segmento en crecimiento impulsado por el cambio demográfico mundial hacia una población de mayor edad que requiere apoyo de vida asistida.

- Centros de cirugía ambulatoria: Beneficiándose de la tendencia hacia los procedimientos ambulatorios y la necesidad de camas de recuperación de alta calidad.

- Entornos de atención domiciliaria: un canal emergente de alto crecimiento para camas médicas adaptadas para uso residencial.

Por geografía:

- América del norte

- Europa

- Asia-Pacífico

- América del Sur y Central

- Oriente Medio y África

Alcance del informe del mercado de camas de hospital

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2025 | 3.980 millones de dólares estadounidenses |

| Tamaño del mercado en 2034 | US$ 6.44 mil millones |

| CAGR global (2026-2034) | 5,5% |

| Datos históricos | 2021-2024 |

| Período de pronóstico | 2026-2034 |

| Segmentos cubiertos |

Por tipo

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de camas de hospital: comprensión de su impacto en la dinámica empresarial

El mercado de camas de hospital está creciendo rápidamente, impulsado por la creciente demanda del usuario final debido a factores como la evolución de las preferencias del consumidor, los avances tecnológicos y un mayor conocimiento de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades del consumidor y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

Análisis de la cuota de mercado de camas de hospital por geografía

Se prevé que Asia-Pacífico experimente el mayor crecimiento en los próximos años. Los mercados emergentes de América del Sur y Central, Oriente Medio y África también ofrecen numerosas oportunidades sin explotar para la expansión de los fabricantes de mobiliario médico y los proveedores de instalaciones especializadas.

El mercado de camas hospitalarias está experimentando una transformación significativa, pasando de la utilidad manual tradicional a ecosistemas médico-quirúrgicos de alto valor. El crecimiento se ve impulsado por la creciente prevalencia de enfermedades crónicas, el aumento de la demanda de capacidad especializada en UCI y la expansión de la atención a largo plazo. A continuación, se presenta un resumen de la cuota de mercado y las tendencias por región:

1. América del Norte

- Cuota de mercado: posee una participación líder a nivel mundial, impulsada por la adopción de tecnología de primera calidad y un alto gasto en atención médica.

-

Factores clave:

- Reemplazo generalizado de camas tradicionales por sistemas inteligentes para reducir las enfermedades adquiridas en el hospital

- Fuerte financiación gubernamental para mejoras en cuidados críticos y ampliaciones de centros de traumatología

- Creciente preferencia por camas de atención médica domiciliaria de alta tecnología para la recuperación posoperatoria

- Tendencias: Integración de sensores impulsados por IA para el monitoreo continuo de pacientes y un enfoque en diseños bariátricos específicos para satisfacer las necesidades demográficas.

2. Europa

- Cuota de mercado: Posee una participación global significativa, sustentada por sólidos sistemas de salud pública en Alemania, Francia y el Reino Unido.

-

Factores clave:

- Normas regulatorias estrictas para la seguridad del paciente y la protección ergonómica del personal de enfermería

- Infraestructura de procesamiento establecida para la esterilización y el mantenimiento de camas de hospital a gran escala

- El envejecimiento de la población impulsa una alta demanda de camas de rehabilitación y cuidados de larga duración

- Tendencias: Un cambio estratégico hacia camas ecodiseñadas que utilizan materiales sostenibles y superficies avanzadas de control de infecciones para cumplir con los estándares del Pacto Verde Europeo.

3. Asia-Pacífico

- Cuota de mercado: La región de más rápido crecimiento, con China e India actuando como los principales impulsores del desarrollo de la infraestructura hospitalaria.

-

Factores clave:

- Masivas inversiones públicas y privadas en la construcción de hospitales inteligentes y centros multidisciplinarios

- Urbanización rápida e iniciativas gubernamentales para mejorar la proporción de camas por paciente

- Segmentos de ingresos medios y altos en ascenso que buscan experiencias de hospitalización de lujo occidentalizadas

- Tendencias: Fuerte dependencia de los contratos B2B para implementaciones de camas a gran escala y crecimiento de centros de fabricación locales para modelos manuales y eléctricos.

4. América del Sur y Central

- Cuota de mercado: Mercado emergente con un sector hospitalario privado en crecimiento en países como Brasil y Chile.

-

Factores clave:

- Modernización de las instalaciones existentes para atraer el turismo médico y mejorar los resultados de los pacientes locales

- Aumentar la concienciación sobre las camas especializadas para la maternidad y la atención psiquiátrica

- Transición de camas manuales a semieléctricas en clínicas privadas urbanas

- Tendencias: Crecimiento de centros quirúrgicos ambulatorios boutique y la introducción de cadenas de suministro desde la granja hasta la cama para el mantenimiento localizado de equipos.

5. Oriente Medio y África

- Cuota de mercado: Desarrollo de un mercado en transición hacia estándares de atención médica formalizados a través de inversiones estratégicas.

-

Factores clave:

- Proyectos hospitalarios a gran escala en Arabia Saudita y los Emiratos Árabes Unidos (por ejemplo, Neom y Dubai Healthcare City)

- Alta demanda de camas duraderas y de bajo mantenimiento en climas áridos

- Enfoque estratégico en aumentar la seguridad alimentaria local y la resiliencia de la cadena de suministro médico

- Tendencias: Implementación de tecnologías modernas de ordeño y refrigeración (para camas terapéuticas) y un enfoque en el soporte de alto contenido nutricional para entornos hospitalarios pediátricos.

Alta densidad de mercado y competencia

La competencia se intensifica debido a la presencia de líderes consolidados como Baxter International Inc. (Hillrom), Stryker Corporation y Getinge AB. Especialistas regionales y empresas de nicho como LINET Group SE (República Checa) y Paramount Bed Co., Ltd. (Japón), junto con innovadores en equipos médicos como Invacare Corporation y Arjo AB, también contribuyen a un panorama de mercado diverso y en rápida expansión.

Este entorno competitivo impulsa a los proveedores a diferenciarse mediante:

- Transformación digital: posicionar las camas de hospital como centros inteligentes que recopilan datos, alertan a las enfermeras sobre el movimiento de los pacientes y se integran con los registros médicos electrónicos.

- Enfoque de aplicación especializada: ofrecemos soluciones personalizadas para necesidades clínicas específicas, incluidas camas pediátricas, marcos bariátricos y plataformas de UCI especializadas.

- Control de la cadena de suministro: gestión del proceso de principio a fin, desde el diseño ergonómico hasta el ensamblaje local, para garantizar la calidad y el cumplimiento.

Oportunidades y movimientos estratégicos

- Asociarse con plataformas de salud digital de alta gama y proveedores de TI para aprovechar la creciente demanda de camas de hospital conectadas e inteligentes en los mercados de Asia-Pacífico y América del Norte.

- Incorporar prácticas de fabricación sostenibles y certificaciones de economía circular para atraer a administradores de atención médica y agencias de salud pública conscientes del medio ambiente.

Las principales empresas que operan en el mercado de camas de hospital son:

- Hill-Rom Holdings, Inc. (Baxter)

- Stryker

- Arjo

- Corporación Invacare

- PARAMOUNT BED CO., LTD.

- Productos de salud GF, Inc.

- Malvestio SpA

- Span America (Corporación Savaria)

- Industrias Savion

- Stiegelmeyer GmbH & Co. KG

- Medstrom

Descargo de responsabilidad: Las empresas enumeradas anteriormente no están clasificadas en ningún orden particular.

Noticias y desarrollos recientes del mercado de camas de hospital

- En septiembre de 2025, Invacare anunció el lanzamiento de la nueva cama Accent Medical Profiling Bed, diseñada para mejorar el descanso, el sueño y la independencia diaria. Ofrece soluciones cómodas que cumplen con los más altos estándares de seguridad y calidad. La nueva Accent no es la excepción y ofrece una solución de calidad sencilla, asequible y sin concesiones.

- En febrero de 2025, Stryker anunció el lanzamiento de la cama de hospital ProCeed, que ofrece simplicidad y mejora la atención en diversas regiones. ProCeed contribuye a la seguridad de los pacientes y los equipos de atención gracias a diversos elementos de diseño, como la baja altura de la cama, que facilita la movilidad del paciente y reduce el riesgo de lesiones por caídas.

Informe de mercado de camas de hospital: cobertura y resultados

El informe Tamaño y pronóstico del mercado de camas de hospital (2021-2034) proporciona un análisis detallado del mercado que cubre las siguientes áreas:

- Tamaño del mercado de camas de hospital y pronóstico a nivel global, regional y nacional para todos los segmentos clave del mercado cubiertos bajo el alcance

- Tendencias del mercado de camas de hospital, así como dinámicas del mercado como impulsores, restricciones y oportunidades clave

- Análisis PEST y FODA detallado

- Análisis del mercado de camas de hospital que cubre las tendencias clave del mercado, el marco global y regional, los principales actores, las regulaciones y los desarrollos recientes del mercado.

- Análisis del panorama industrial y de la competencia que abarca la concentración del mercado, el análisis de mapas de calor, los actores destacados y los desarrollos recientes en el mercado de camas de hospital.

- Perfiles detallados de empresas

- Análisis histórico (2 años), año base, pronóstico (7 años) con CAGR

- Análisis PEST y FODA

- Tamaño del mercado, valor/volumen: global, regional y nacional

- Industria y panorama competitivo

- Conjunto de datos de Excel

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias

Desbloquea descuentos exclusivos en informes

Consultar ahora

Obtenga una muestra gratuita para - Mercado de camas de hospital

Obtenga una muestra gratuita para - Mercado de camas de hospital